Learning Objectives

Distinguish Processcosting and Job –Costing

Record the flow of materials, labor, and

overhead through a process cost system.

Compute the equivalent units and cost per

equivalent unit( Primarily for WIP ending)

Assign costs to units completed and units in

process

3.

Process Costing System

Is a costing method most commonly used in industries that

produce essentially homogeneous (i.E. Uniform) products in

mass on a continuous basis.

Each unit receives the same amounts of direct materials

costs, direct labor costs, and manufacturing overhead

Unit costs are computed by dividing total costs incurred by

the number of units of output from the production process

Similarities

Both systemsassign( trace and allocate) material,

labor, and overhead costs assigned to products to

compute unit costs.

Both systems use the same manufacturing accounts:

Raw Materials,

Work in Process, and

Finished Goods accounts .

The flow of costs is basically the same in both systems.

6.

Differences

Process costingis used when a single identical product is

produced is mass on a continuing basis , where as Job-

order costing is used when many different jobs are worked

on each period.

Process costing systems accumulate costs by department.

Job-order costing systems accumulated costs by individual

jobs.

Process costing systems use department production reports

to accumulate costs. Job-order costing systems use job

sheets to accumulate costs.

Process costing systems compute unit costs by department.

Job-order costing systems compute unit costs by job.

8

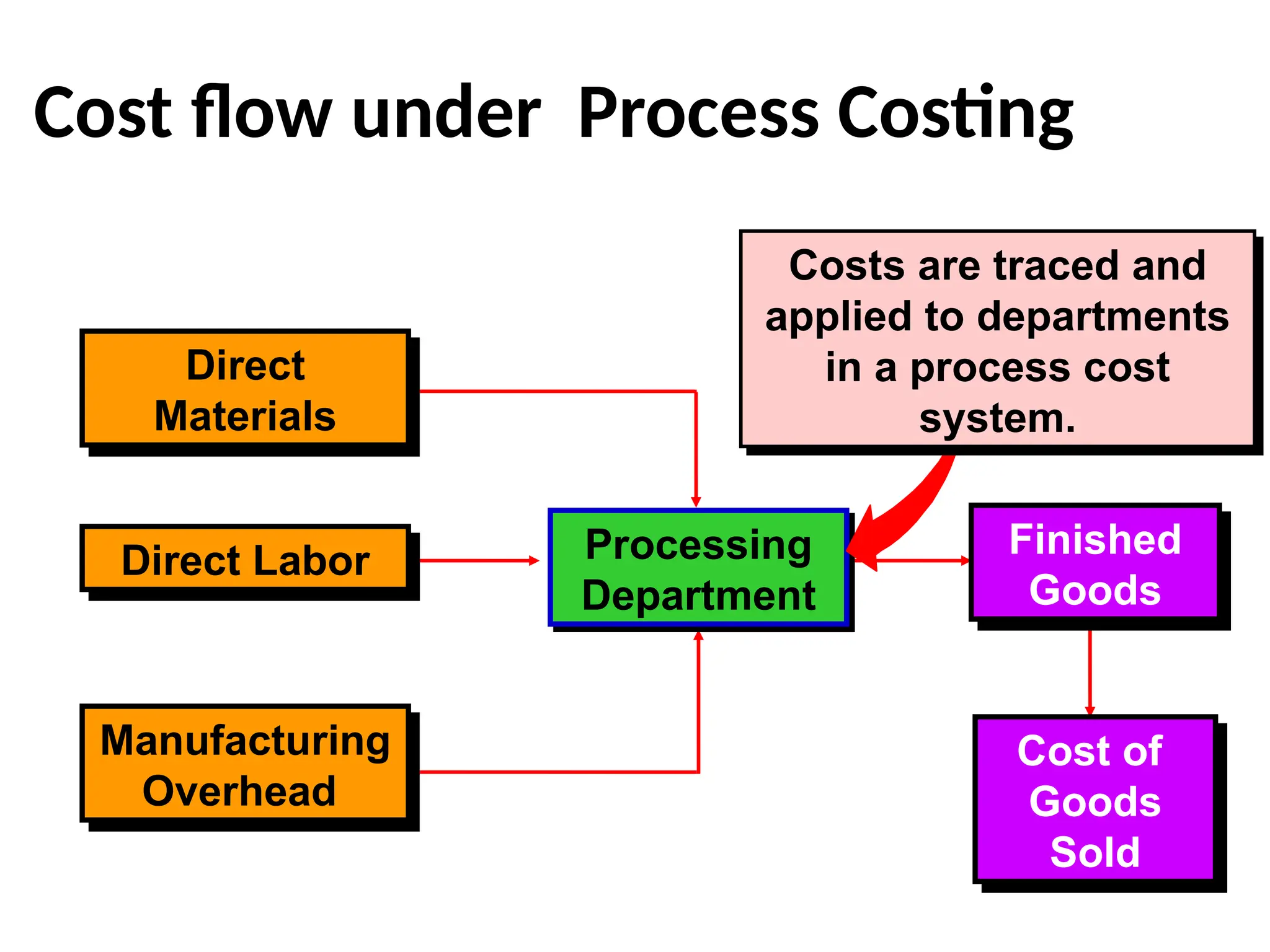

Cost Flow underProcess –

Costing

Assume a Coca-Cola Company with two

subsequent production departments

• Mixing Department

• Bottling Department

9.

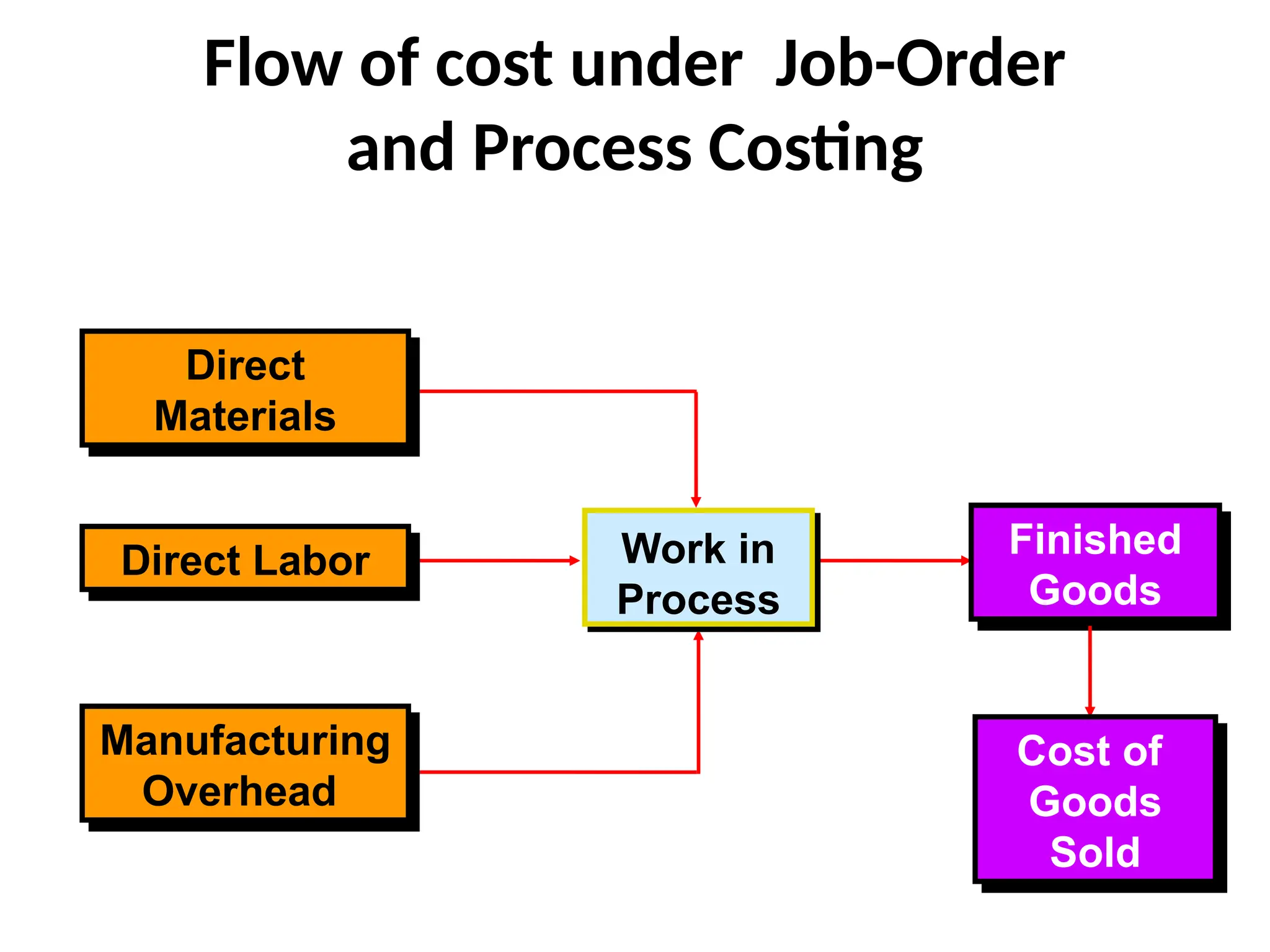

Flow of costunder Job-Order

and Process Costing

Finished

Goods

Cost of

Goods

Sold

Work in

Process

Direct

Materials

Direct Labor

Manufacturing

Overhead

10.

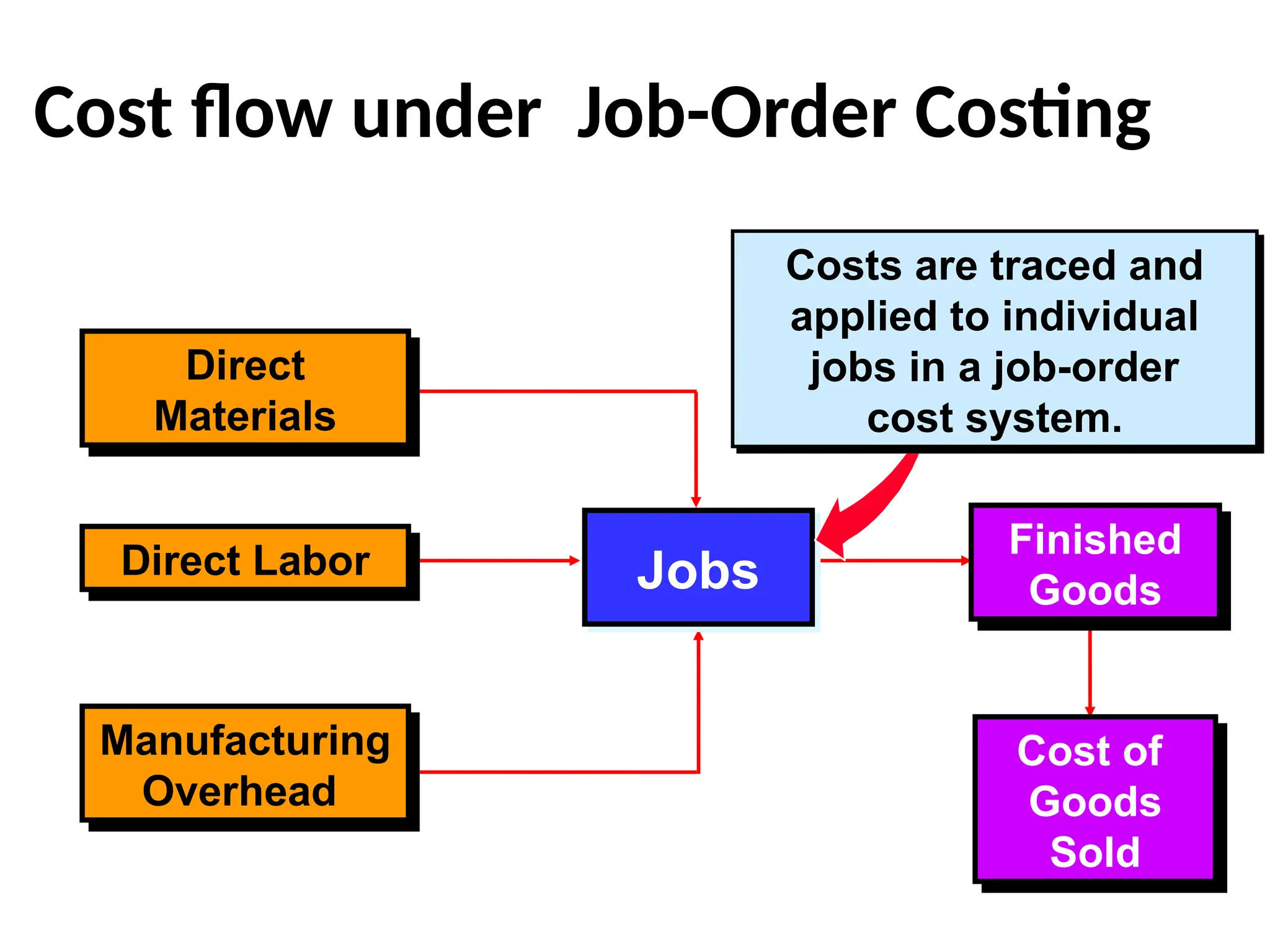

Cost flow underJob-Order Costing

Finished

Goods

Cost of

Goods

Sold

Direct Labor

Manufacturing

Overhead

Jobs

Costs are traced and

applied to individual

jobs in a job-order

cost system.

Direct

Materials

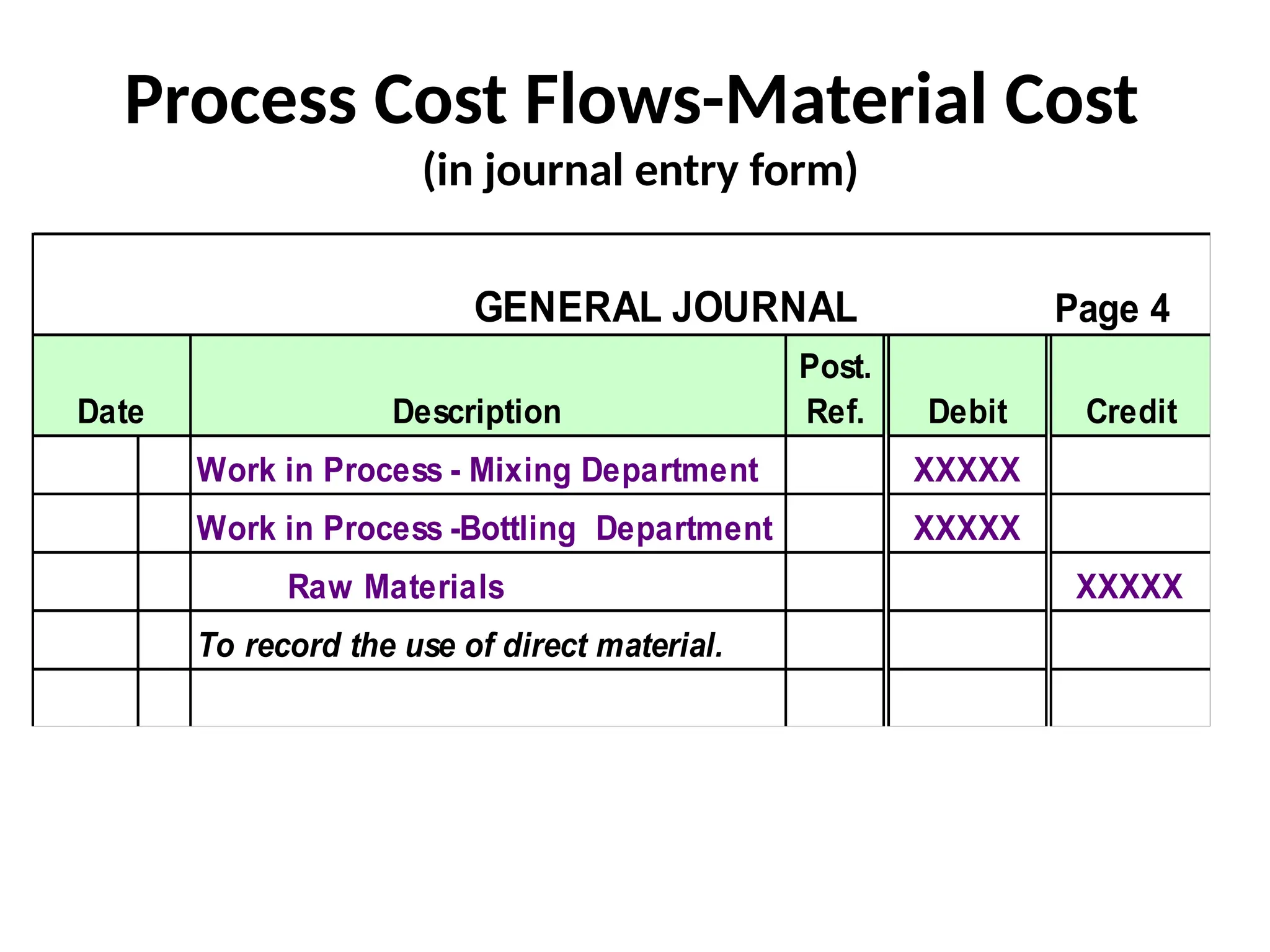

Process Cost Flows-MaterialCost

(in journal entry form)

GENERAL JOURNAL Page 4

Date Description

Post.

Ref. Debit Credit

Work in Process - Mixing Department XXXXX

Work in Process -Bottling Department XXXXX

Raw Materials XXXXX

To record the use of direct material.

13.

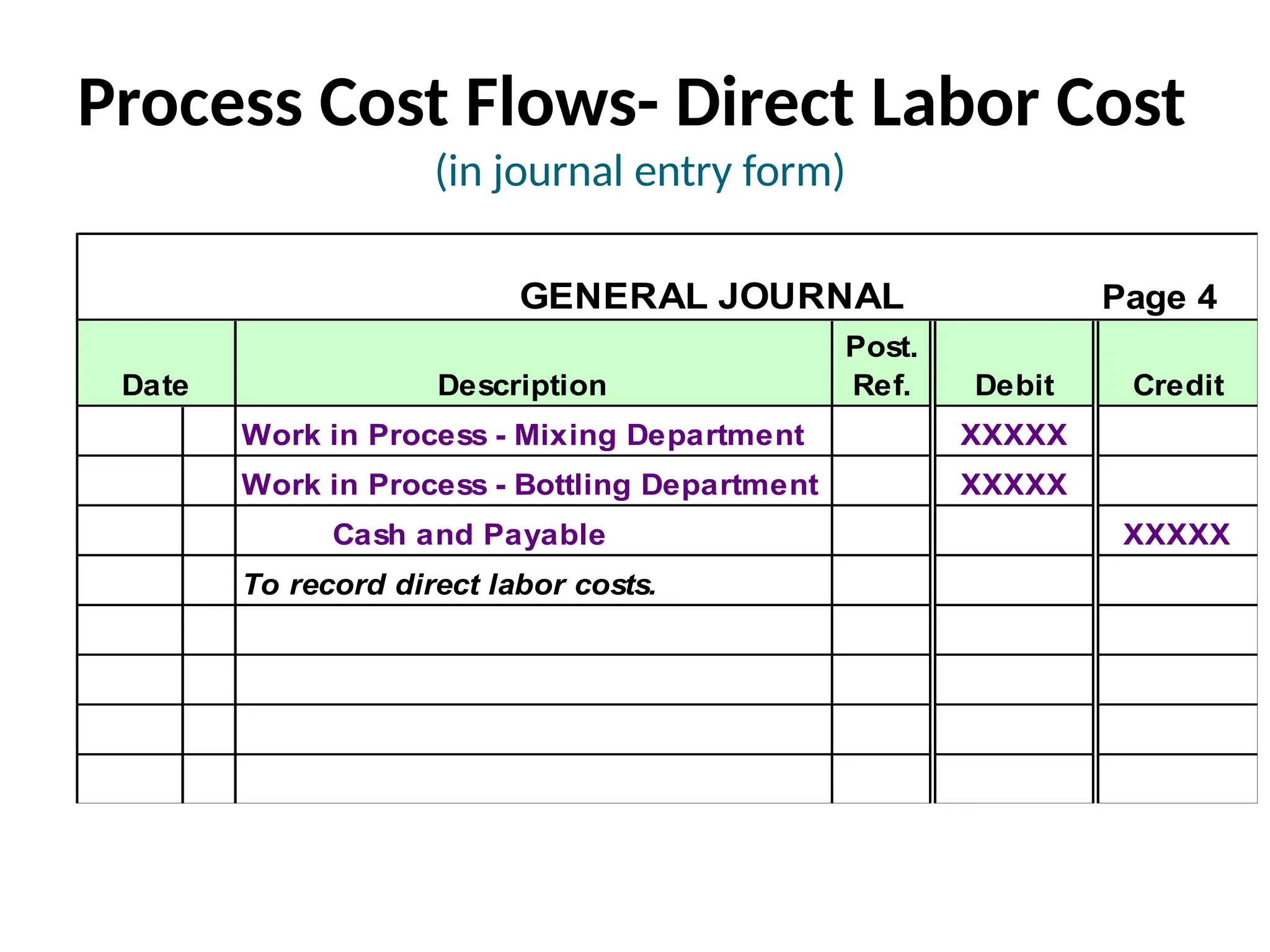

Process Cost Flows-Direct Labor Cost

(in journal entry form)

GENERAL JOURNAL Page 4

Date Description

Post.

Ref. Debit Credit

Work in Process - Mixing Department XXXXX

Work in Process - Bottling Department XXXXX

Cash and Payable XXXXX

To record direct labor costs.

14.

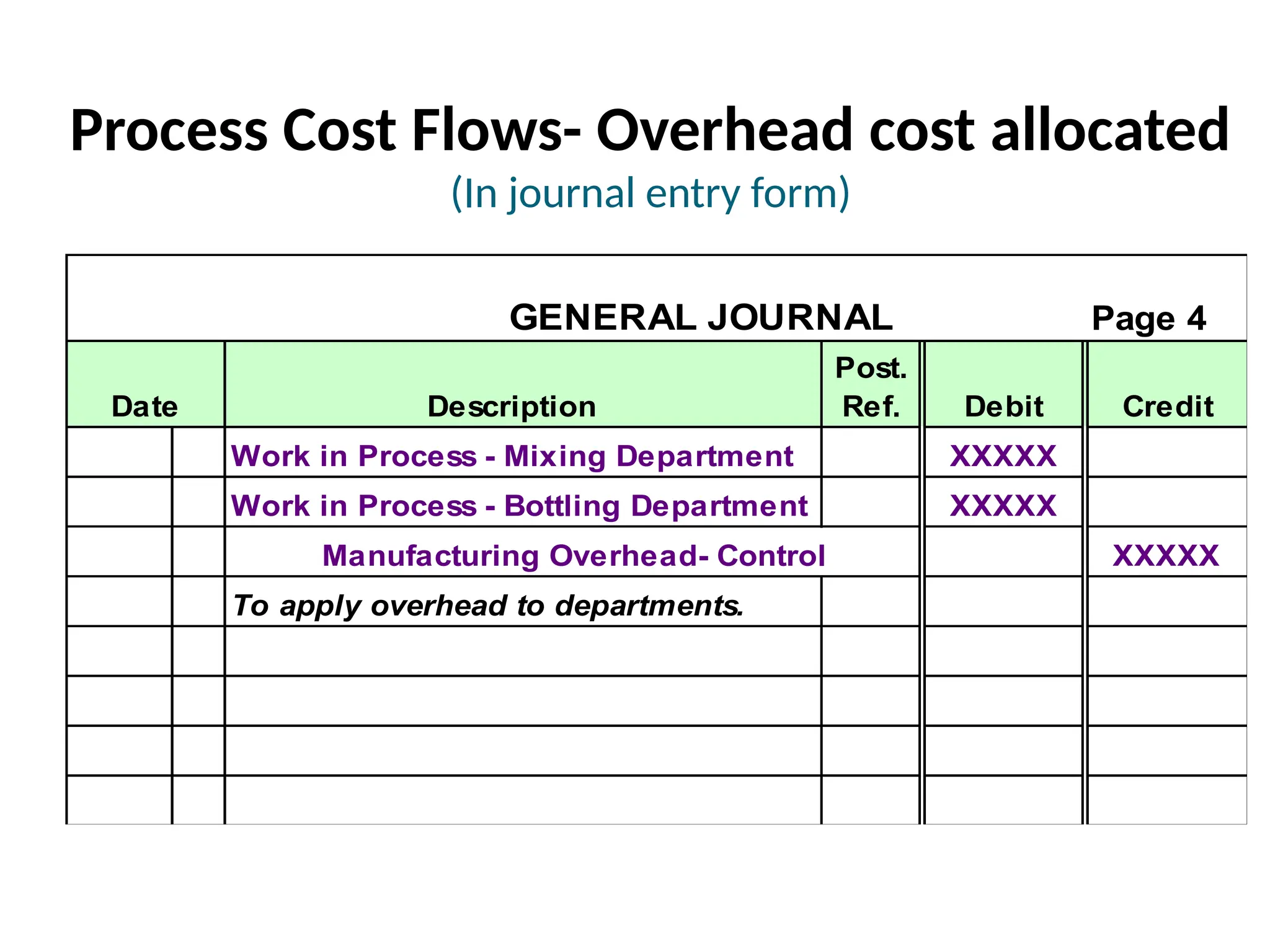

Process Cost Flows-Overhead cost allocated

(In journal entry form)

GENERAL JOURNAL Page 4

Date Description

Post.

Ref. Debit Credit

Work in Process - Mixing Department XXXXX

Work in Process - Bottling Department XXXXX

Manufacturing Overhead- Control XXXXX

To apply overhead to departments.

15.

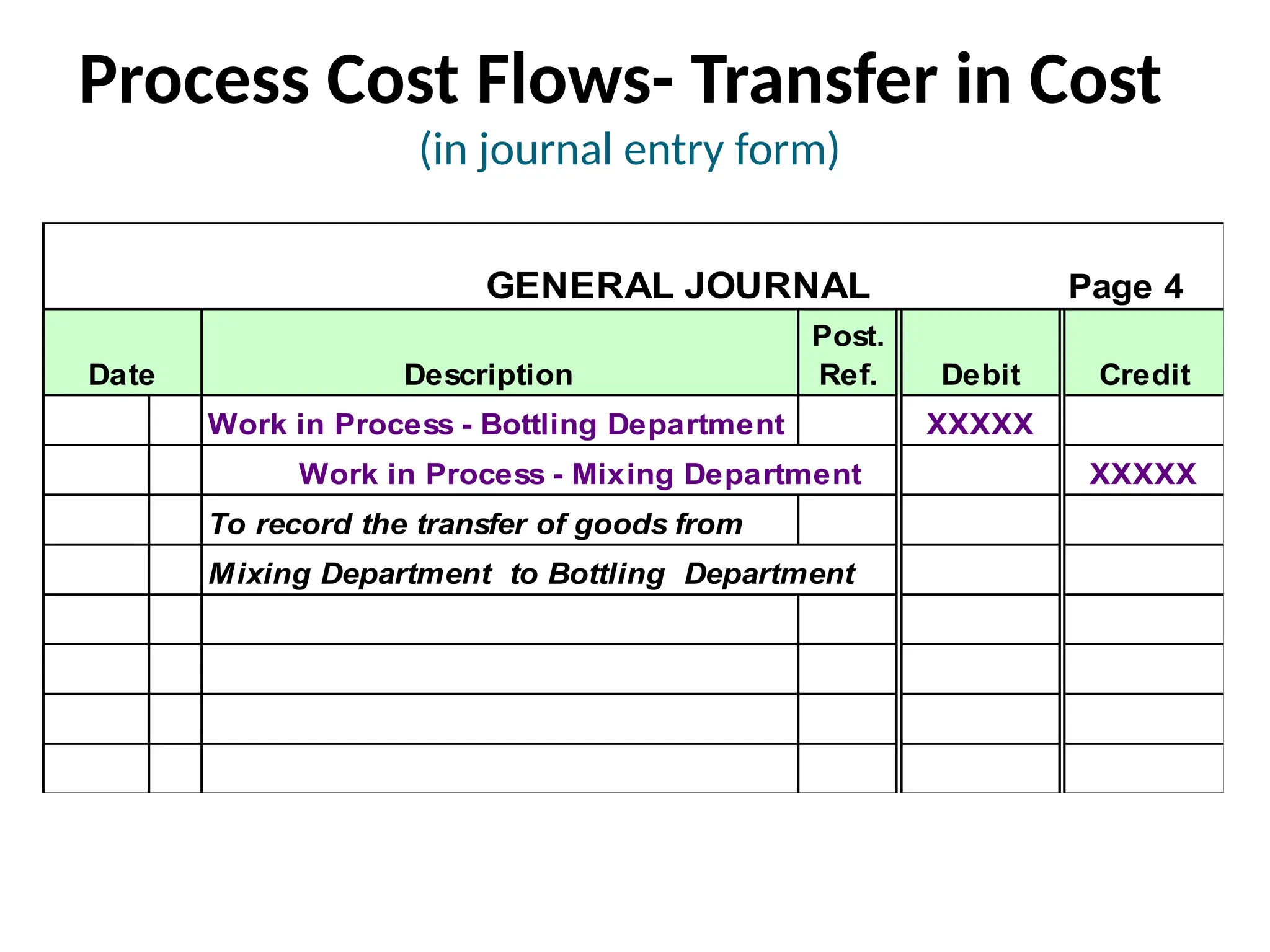

Process Cost Flows-Transfer in Cost

(in journal entry form)

GENERAL JOURNAL Page 4

Date Description

Post.

Ref. Debit Credit

Work in Process - Bottling Department XXXXX

Work in Process - Mixing Department XXXXX

To record the transfer of goods from

Mixing Department to Bottling Department

16.

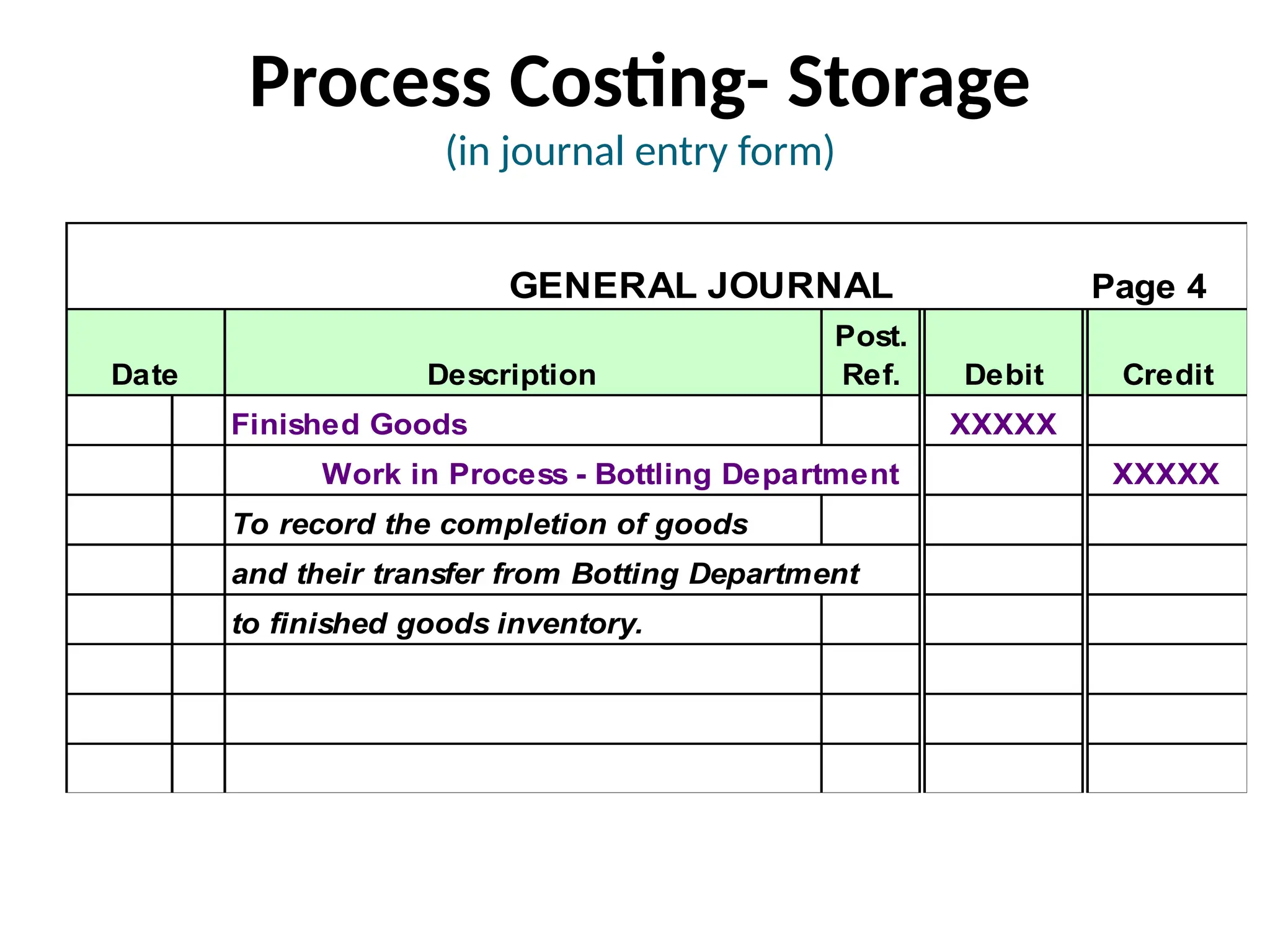

Process Costing- Storage

(injournal entry form)

GENERAL JOURNAL Page 4

Date Description

Post.

Ref. Debit Credit

Finished Goods XXXXX

Work in Process - Bottling Department XXXXX

To record the completion of goods

and their transfer from Botting Department

to finished goods inventory.

17.

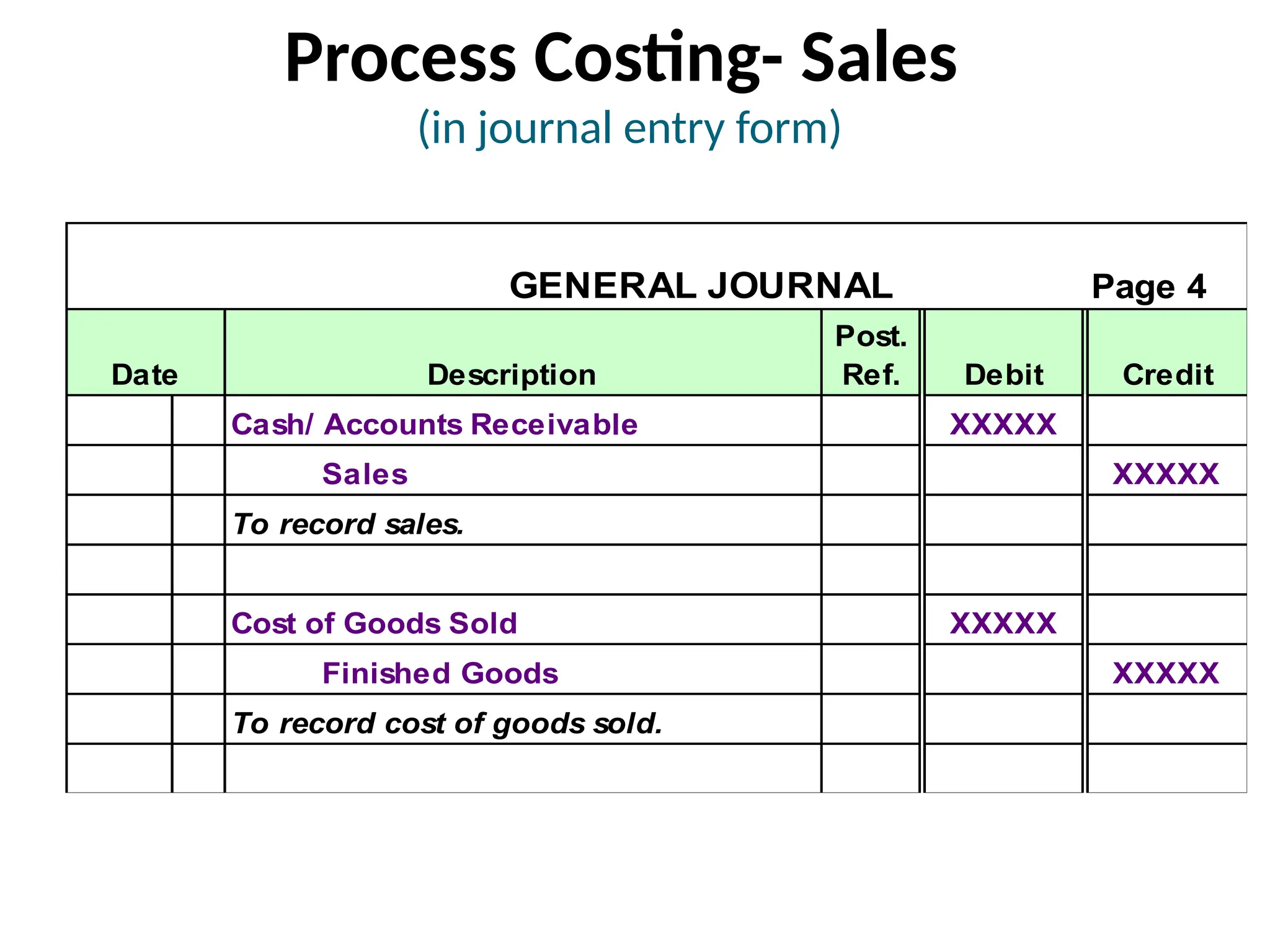

Process Costing- Sales

(injournal entry form)

GENERAL JOURNAL Page 4

Date Description

Post.

Ref. Debit Credit

Cash/ Accounts Receivable XXXXX

Sales XXXXX

To record sales.

Cost of Goods Sold XXXXX

Finished Goods XXXXX

To record cost of goods sold.

18.

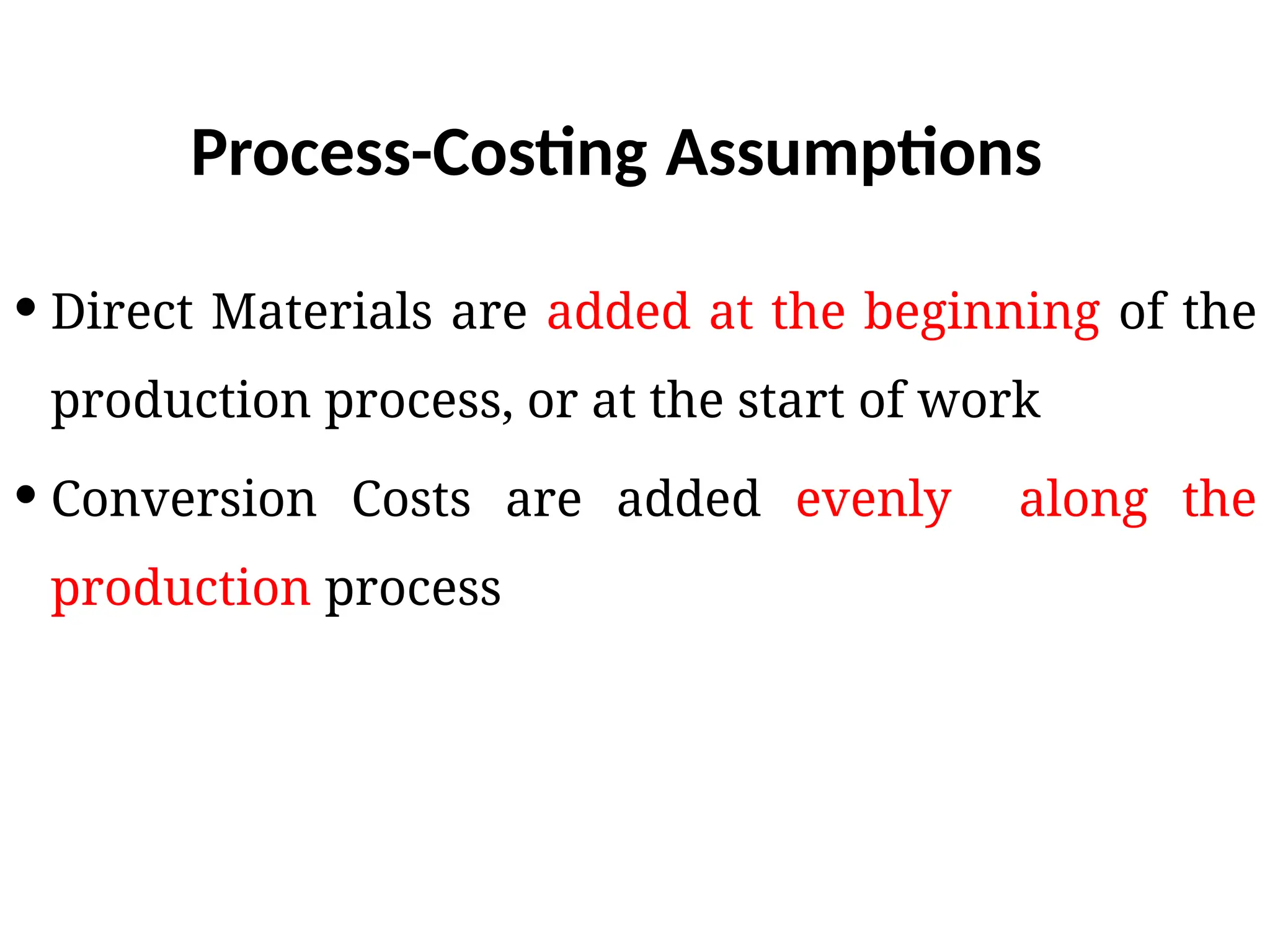

Process-Costing Assumptions

DirectMaterials are added at the beginning of the

production process, or at the start of work

Conversion Costs are added evenly along the

production process

19.

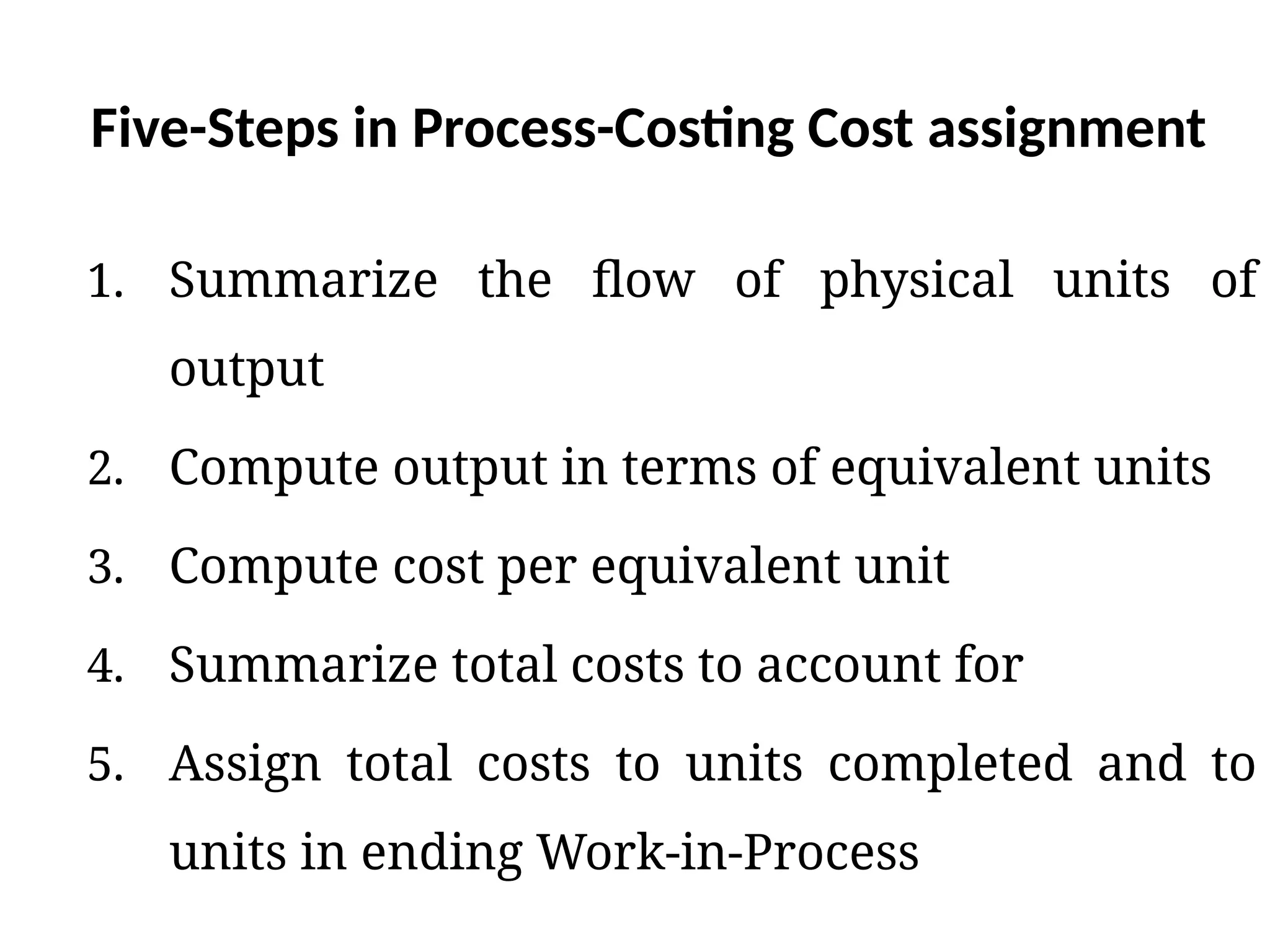

Five-Steps in Process-CostingCost assignment

1. Summarize the flow of physical units of

output

2. Compute output in terms of equivalent units

3. Compute cost per equivalent unit

4. Summarize total costs to account for

5. Assign total costs to units completed and to

units in ending Work-in-Process

20.

26

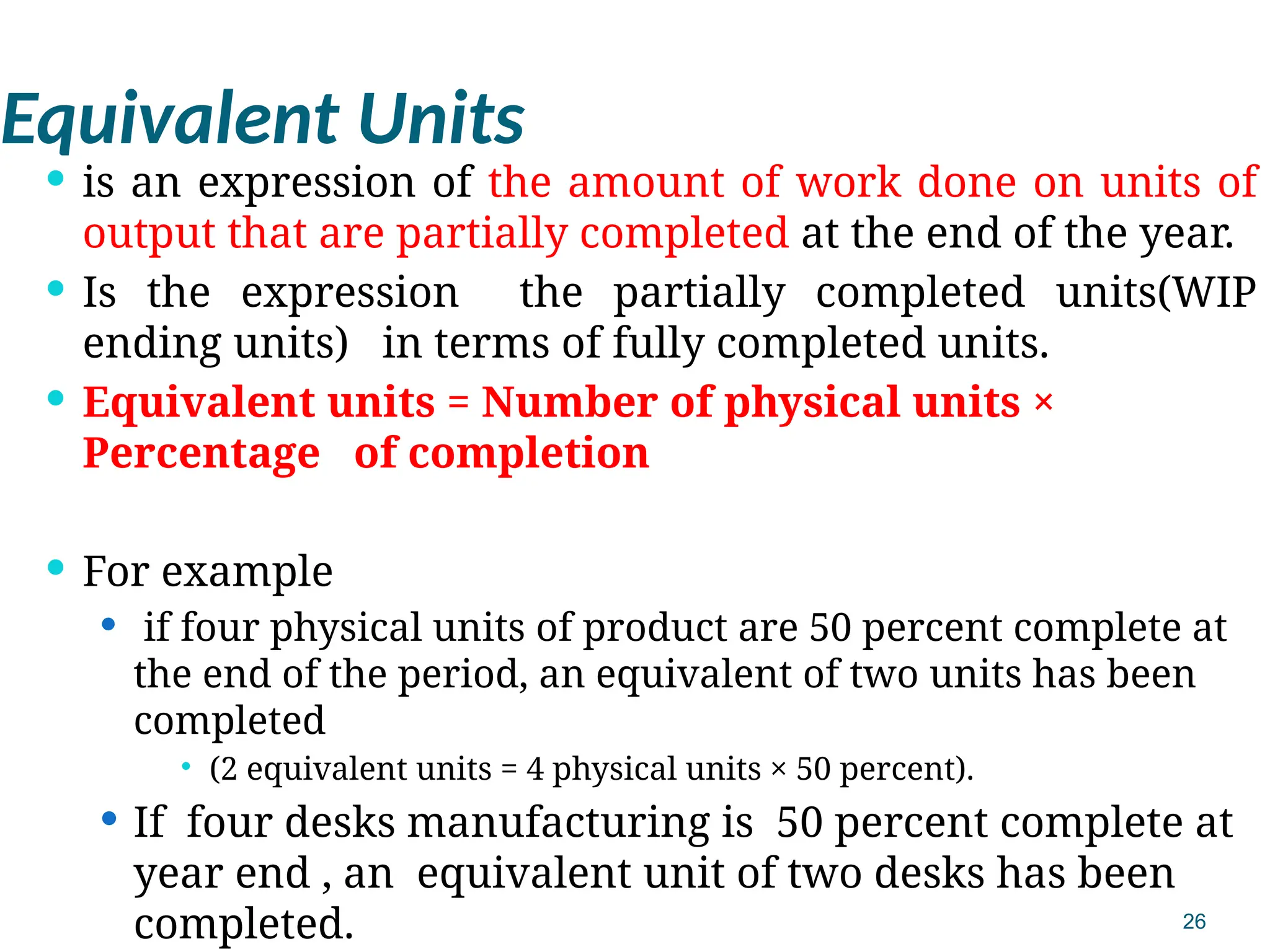

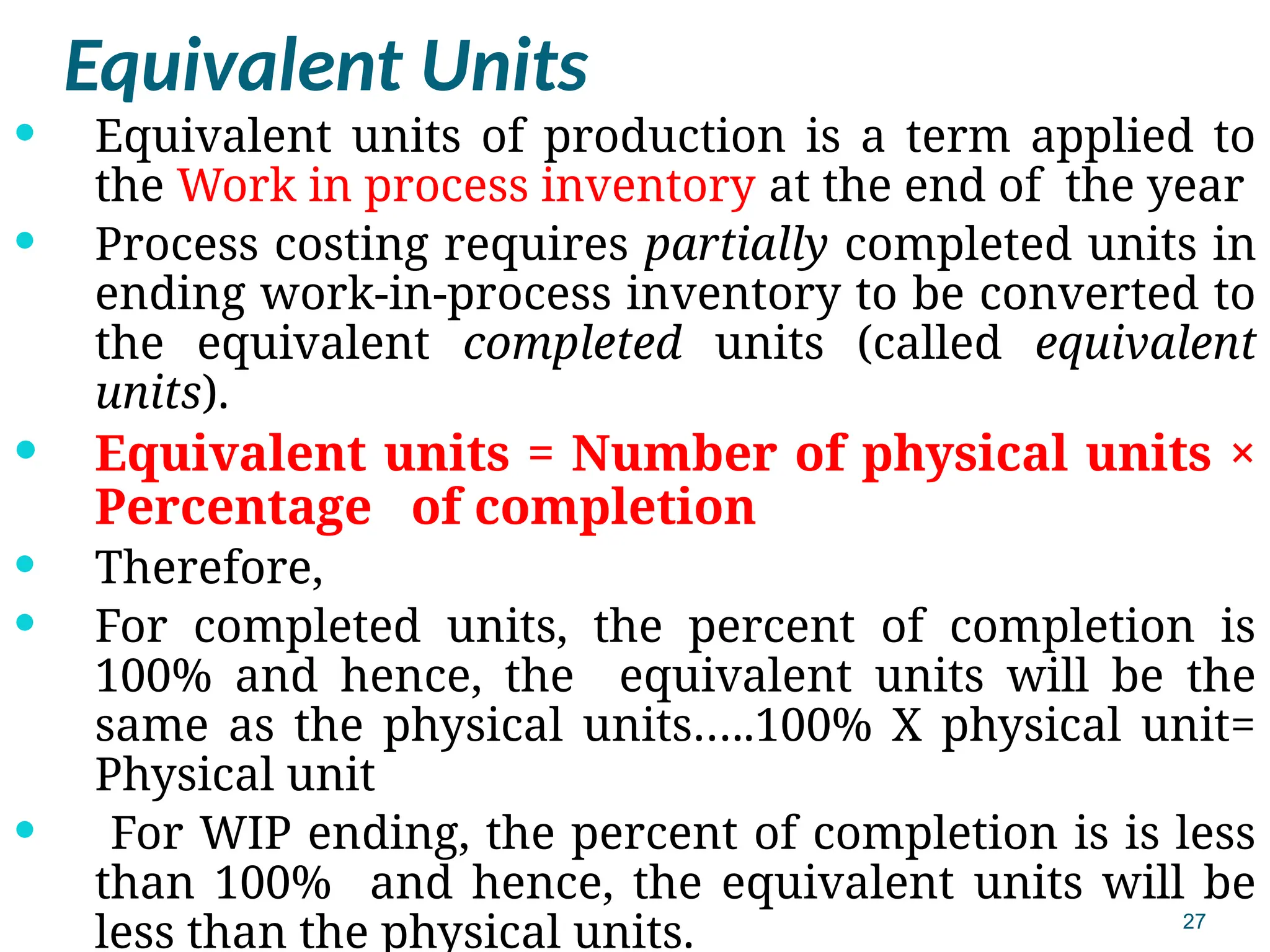

Equivalent Units

isan expression of the amount of work done on units of

output that are partially completed at the end of the year.

Is the expression the partially completed units(WIP

ending units) in terms of fully completed units.

Equivalent units = Number of physical units ×

Percentage of completion

For example

if four physical units of product are 50 percent complete at

the end of the period, an equivalent of two units has been

completed

(2 equivalent units = 4 physical units × 50 percent).

If four desks manufacturing is 50 percent complete at

year end , an equivalent unit of two desks has been

completed.

21.

27

Equivalent Units

Equivalentunits of production is a term applied to

the Work in process inventory at the end of the year

Process costing requires partially completed units in

ending work-in-process inventory to be converted to

the equivalent completed units (called equivalent

units).

Equivalent units = Number of physical units ×

Percentage of completion

Therefore,

For completed units, the percent of completion is

100% and hence, the equivalent units will be the

same as the physical units…..100% X physical unit=

Physical unit

For WIP ending, the percent of completion is is less

than 100% and hence, the equivalent units will be

less than the physical units.

22.

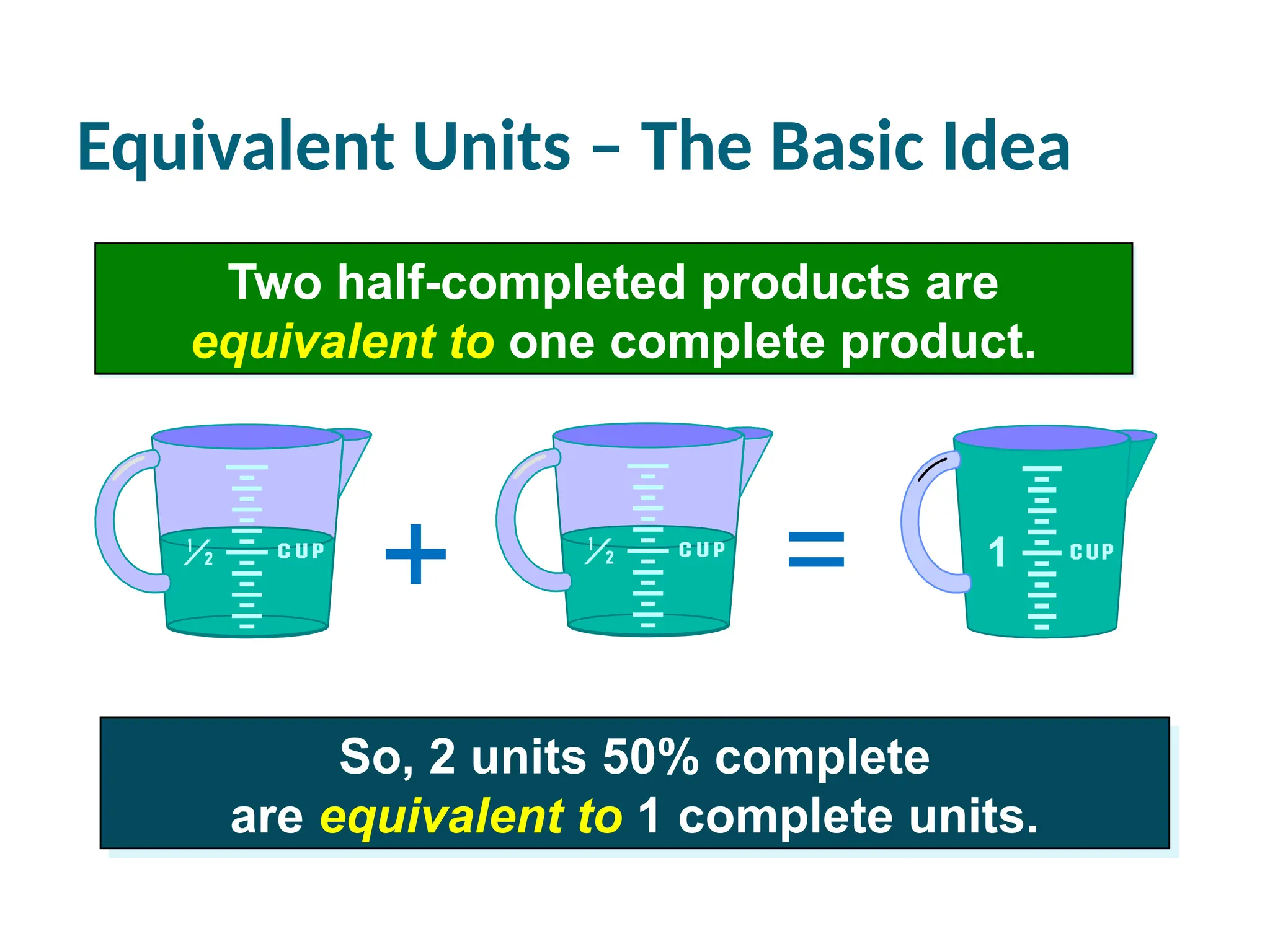

Equivalent Units –The Basic Idea

Two half-completed products are

equivalent to one complete product.

So, 2 units 50% complete

are equivalent to 1 complete units.

+ = 1

23.

29

Illustrating Example -ProcessCosting

Assume Coca-Cola Chemical Company Produces Coke

and uses process costing system to account for its

operation.

The soft drink is produced in two processing

departments: the Mixing Department and the Bottling

Department.

The product is bottled in 300ml bottles.

24.

30

Part I: MixingDepartment

In the Mixing Department, various ingredients are

added at the start of the process

costs are accumulated in two pools, one for direct

material and another for all conversion costs.

Direct material is added at the beginning of the

process

conversion costs are applied evenly through out the

process.

Data for the first month of operation (September) of

the Mixing Department is given below:

25.

31

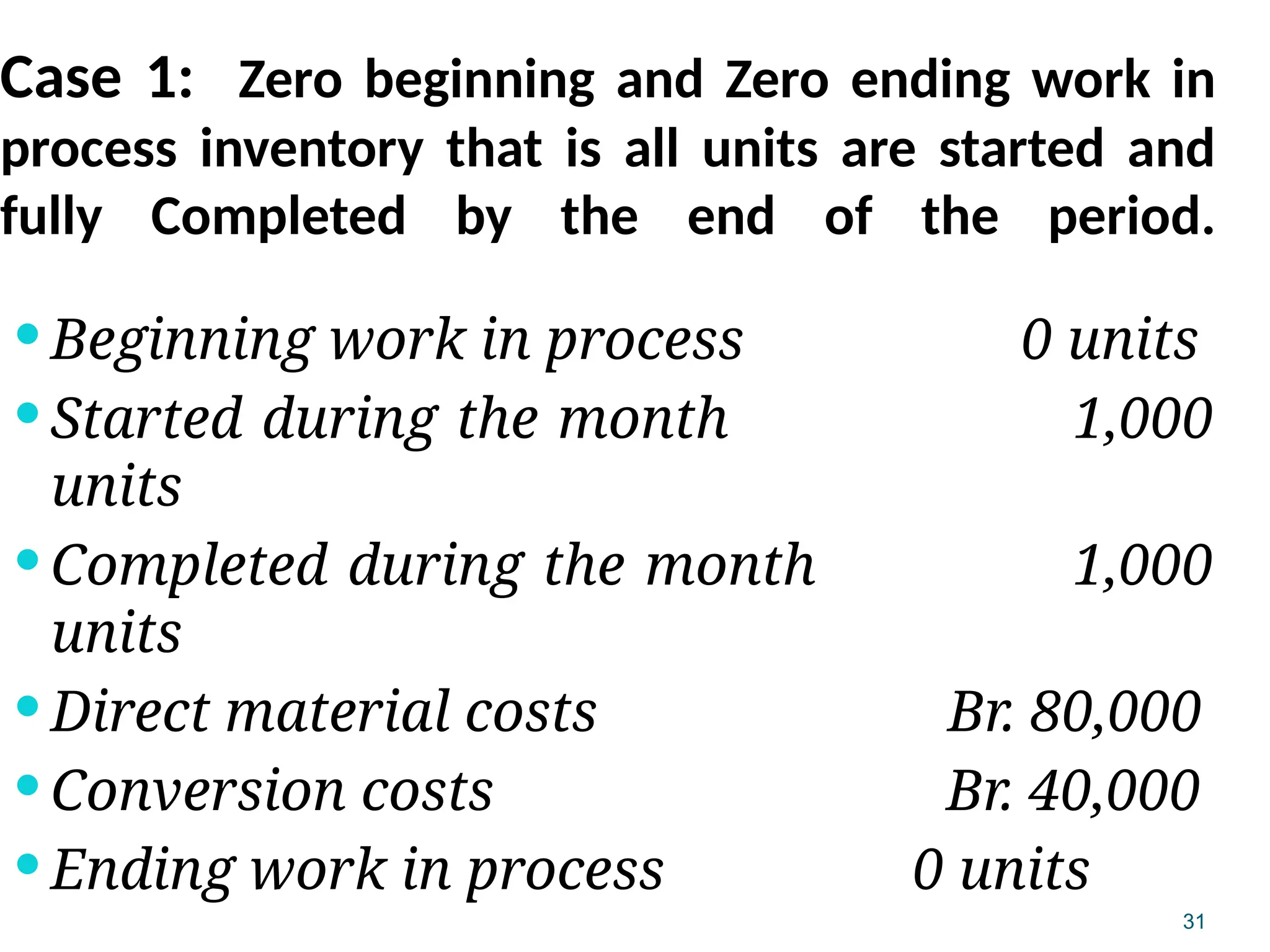

Case 1: Zerobeginning and Zero ending work in

process inventory that is all units are started and

fully Completed by the end of the period.

Beginning work in process 0 units

Started during the month 1,000

units

Completed during the month 1,000

units

Direct material costs Br. 80,000

Conversion costs Br. 40,000

Ending work in process 0 units

26.

32

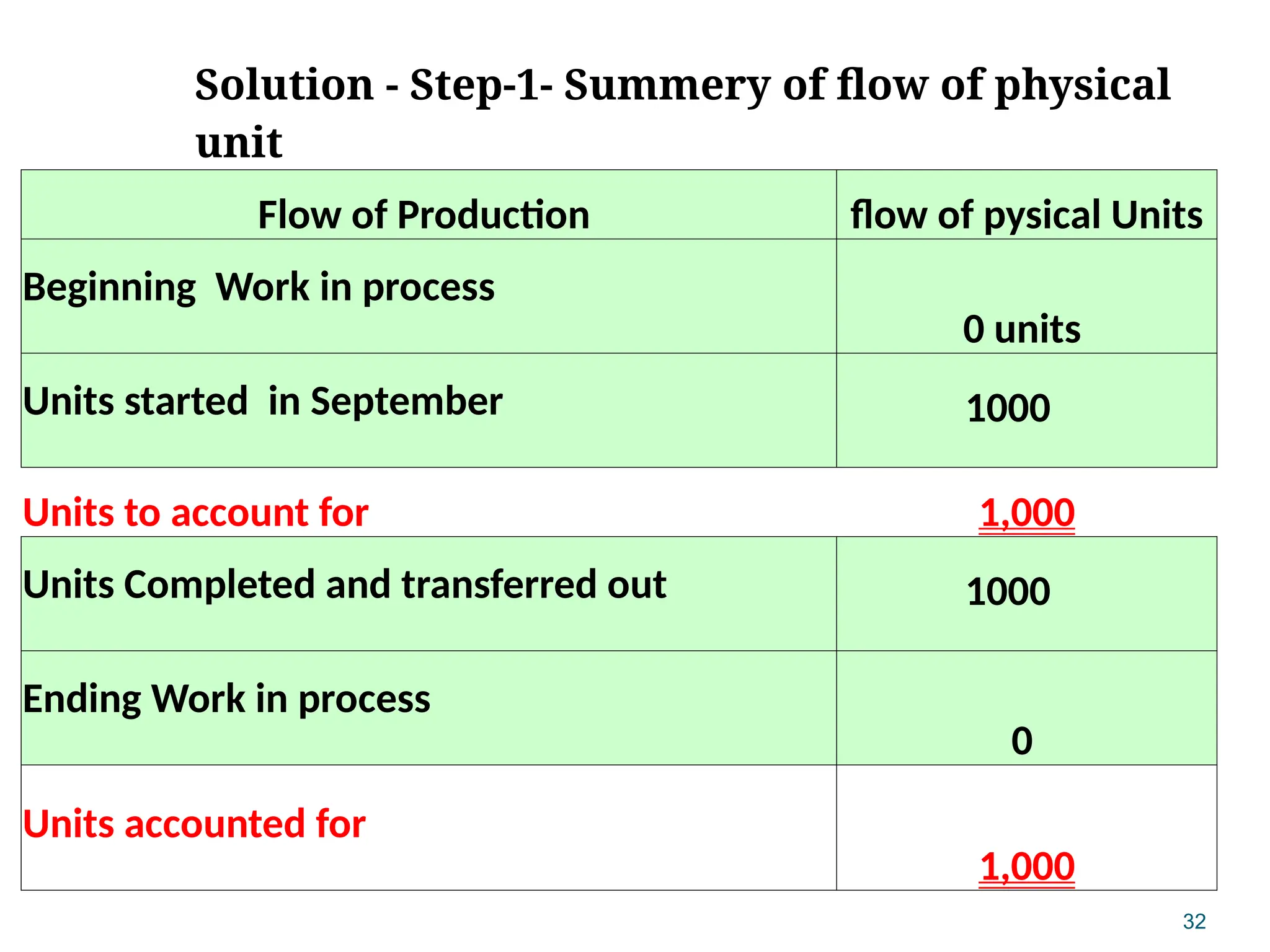

Solution - Step-1-Summery of flow of physical

unit

Flow of Production flow of pysical Units

Beginning Work in process

0 units

Units started in September 1000

Units to account for 1,000

Units Completed and transferred out 1000

Ending Work in process

0

Units accounted for

1,000

27.

33

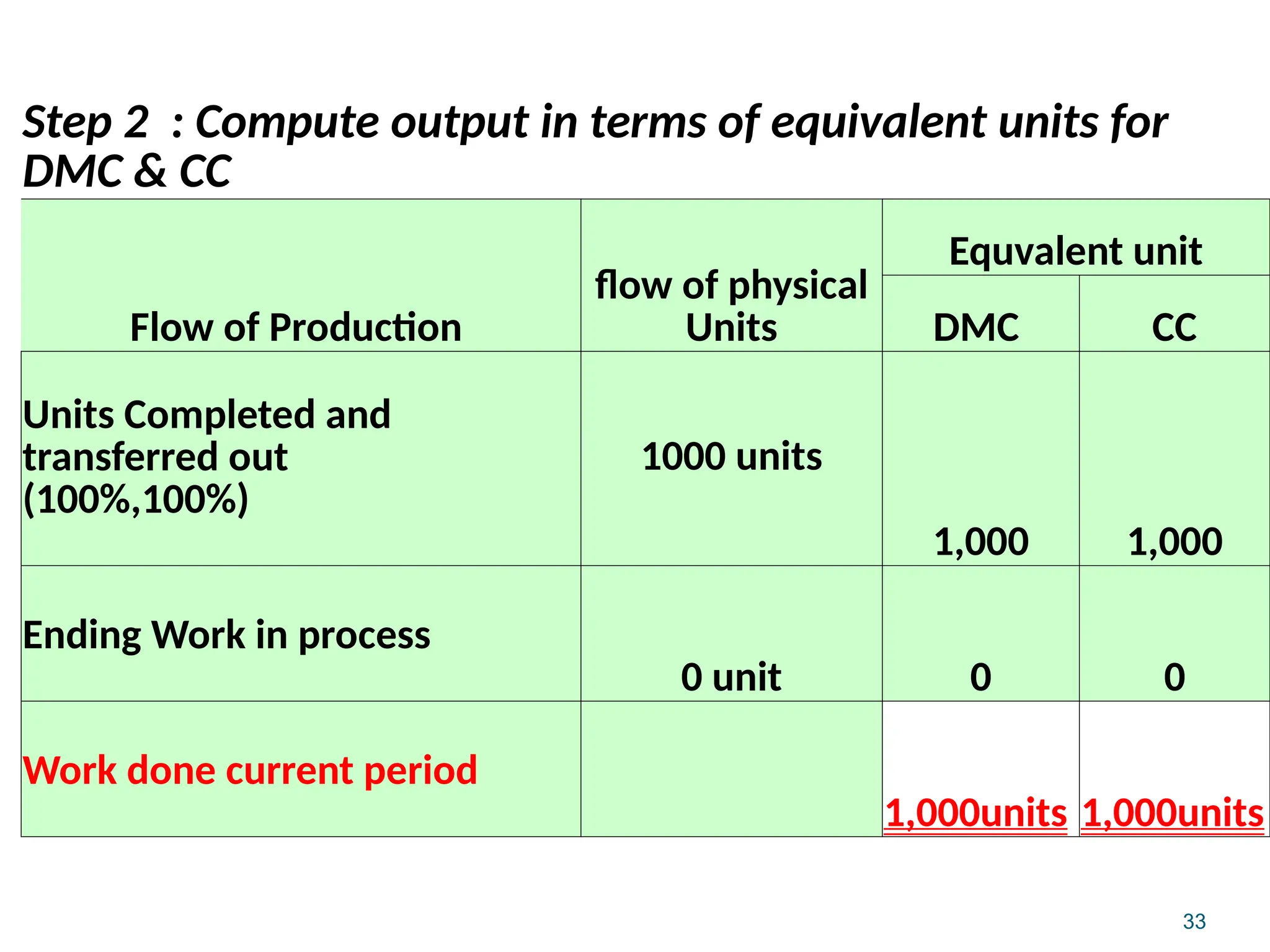

Step 2 :Compute output in terms of equivalent units for

DMC & CC

Flow of Production

flow of physical

Units

Equvalent unit

DMC CC

Units Completed and

transferred out

(100%,100%)

1000 units

1,000 1,000

Ending Work in process

0 unit 0 0

Work done current period

1,000units 1,000units

28.

34

Step 3 &4: flow of cost and Cost per Equivalent units

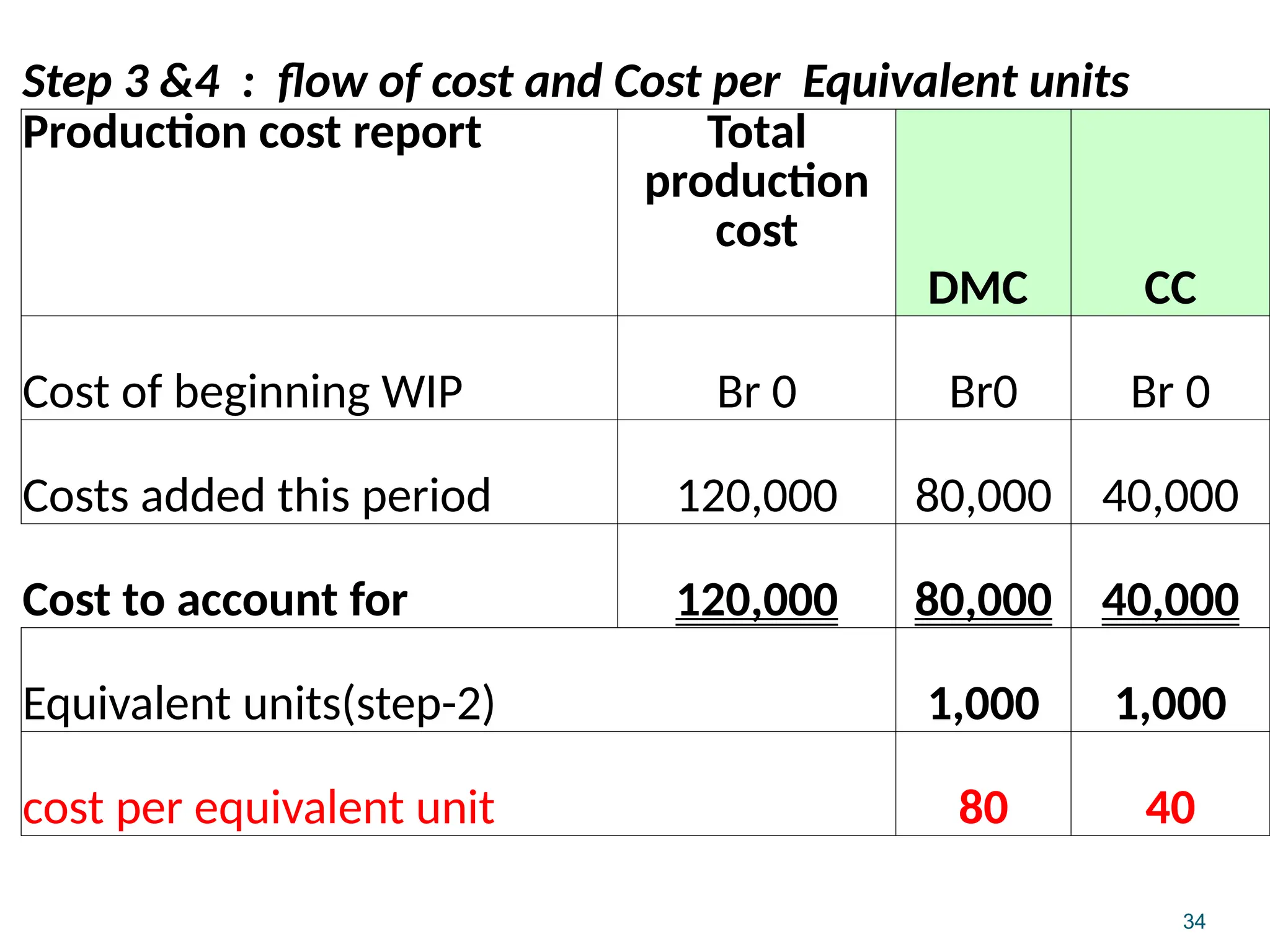

Production cost report Total

production

cost

DMC CC

Cost of beginning WIP Br 0 Br0 Br 0

Costs added this period 120,000 80,000 40,000

Cost to account for 120,000 80,000 40,000

Equivalent units(step-2) 1,000 1,000

cost per equivalent unit 80 40

29.

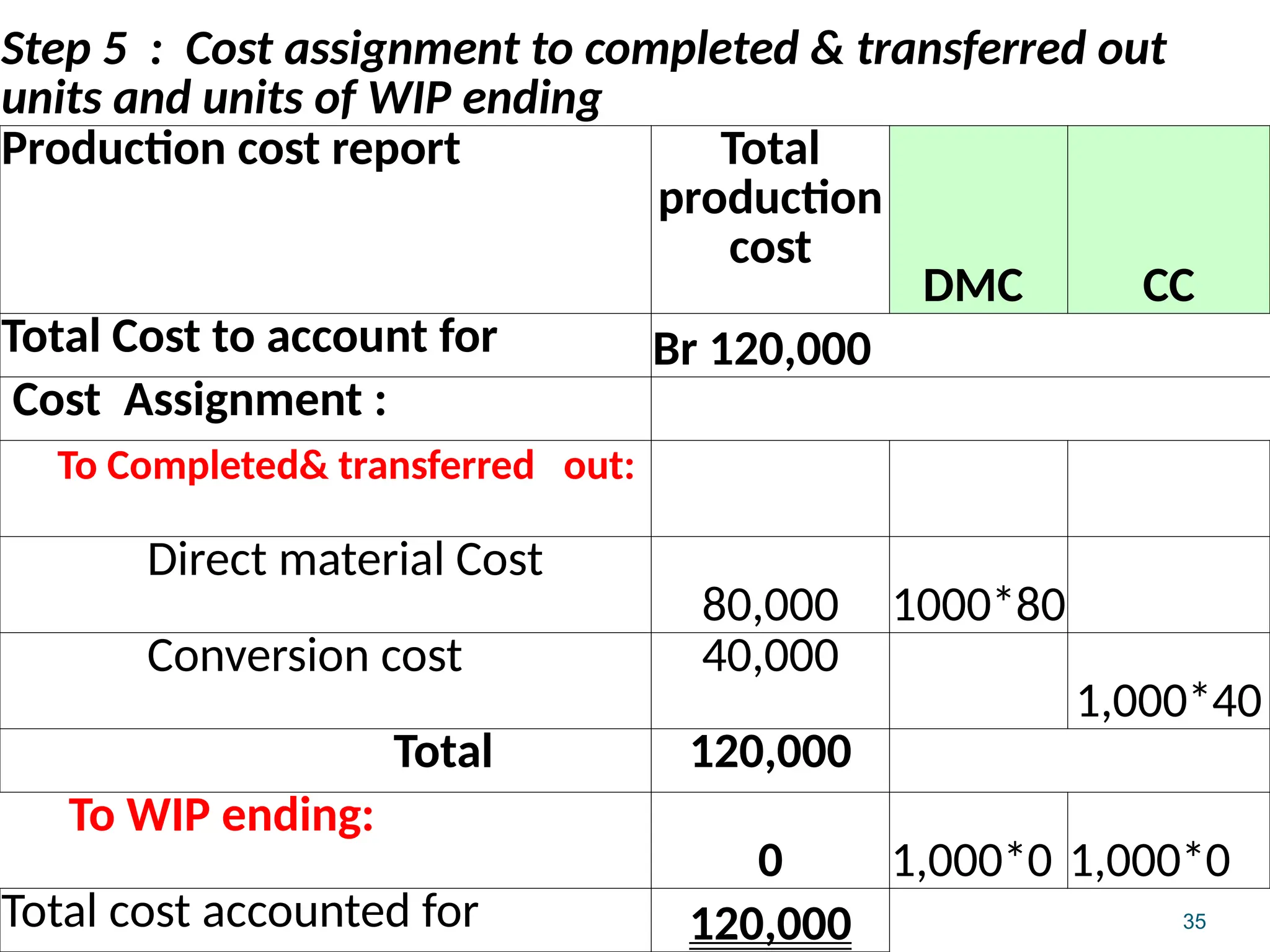

35

Step 5 :Cost assignment to completed & transferred out

units and units of WIP ending

Production cost report Total

production

cost

DMC CC

Total Cost to account for Br 120,000

Cost Assignment :

To Completed& transferred out:

Direct material Cost

80,000 1000*80

Conversion cost 40,000

1,000*40

Total 120,000

To WIP ending:

0 1,000*0 1,000*0

Total cost accounted for 120,000

30.

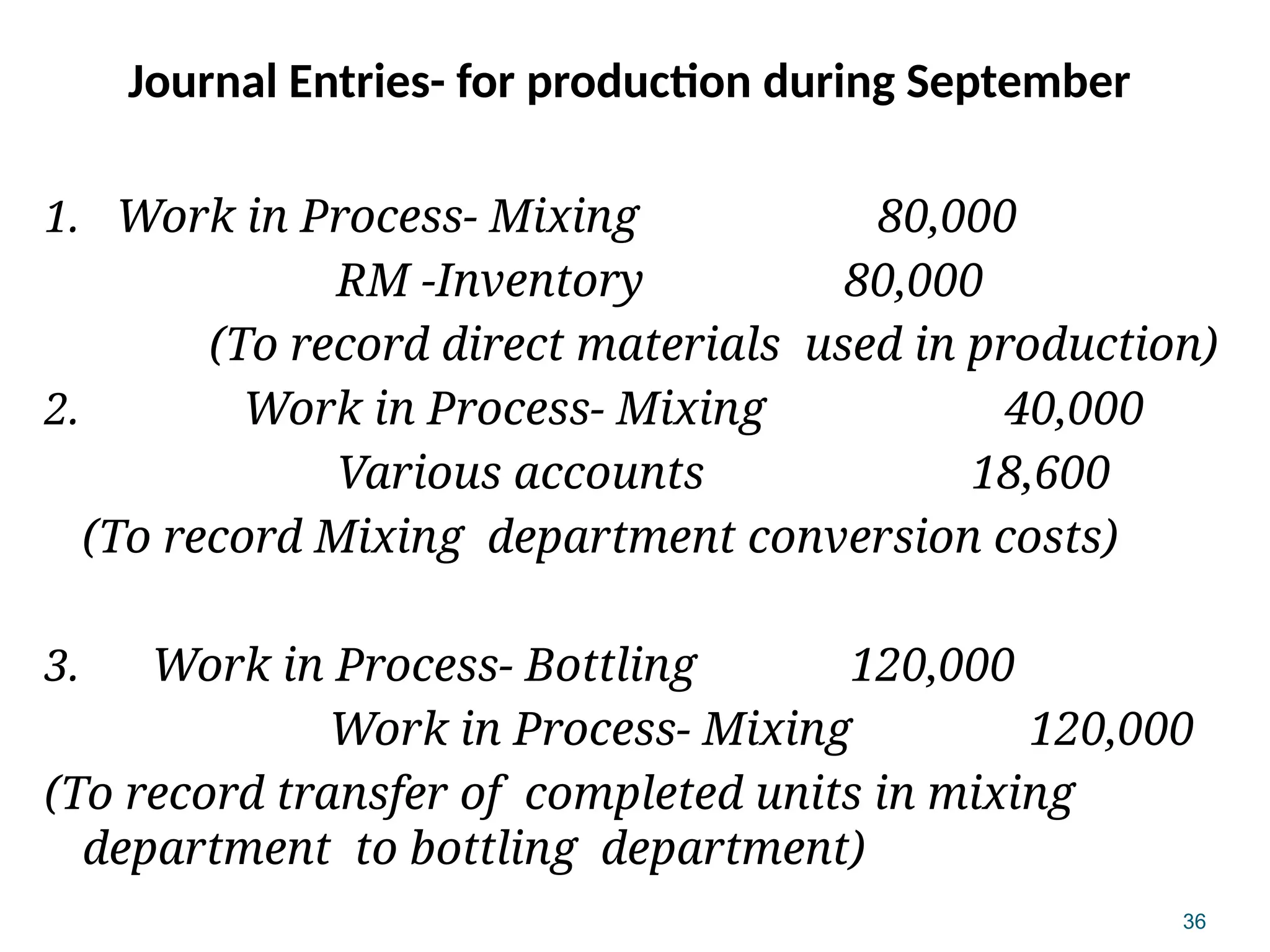

36

Journal Entries- forproduction during September

1. Work in Process- Mixing 80,000

RM -Inventory 80,000

(To record direct materials used in production)

2. Work in Process- Mixing 40,000

Various accounts 18,600

(To record Mixing department conversion costs)

3. Work in Process- Bottling 120,000

Work in Process- Mixing 120,000

(To record transfer of completed units in mixing

department to bottling department)

31.

37

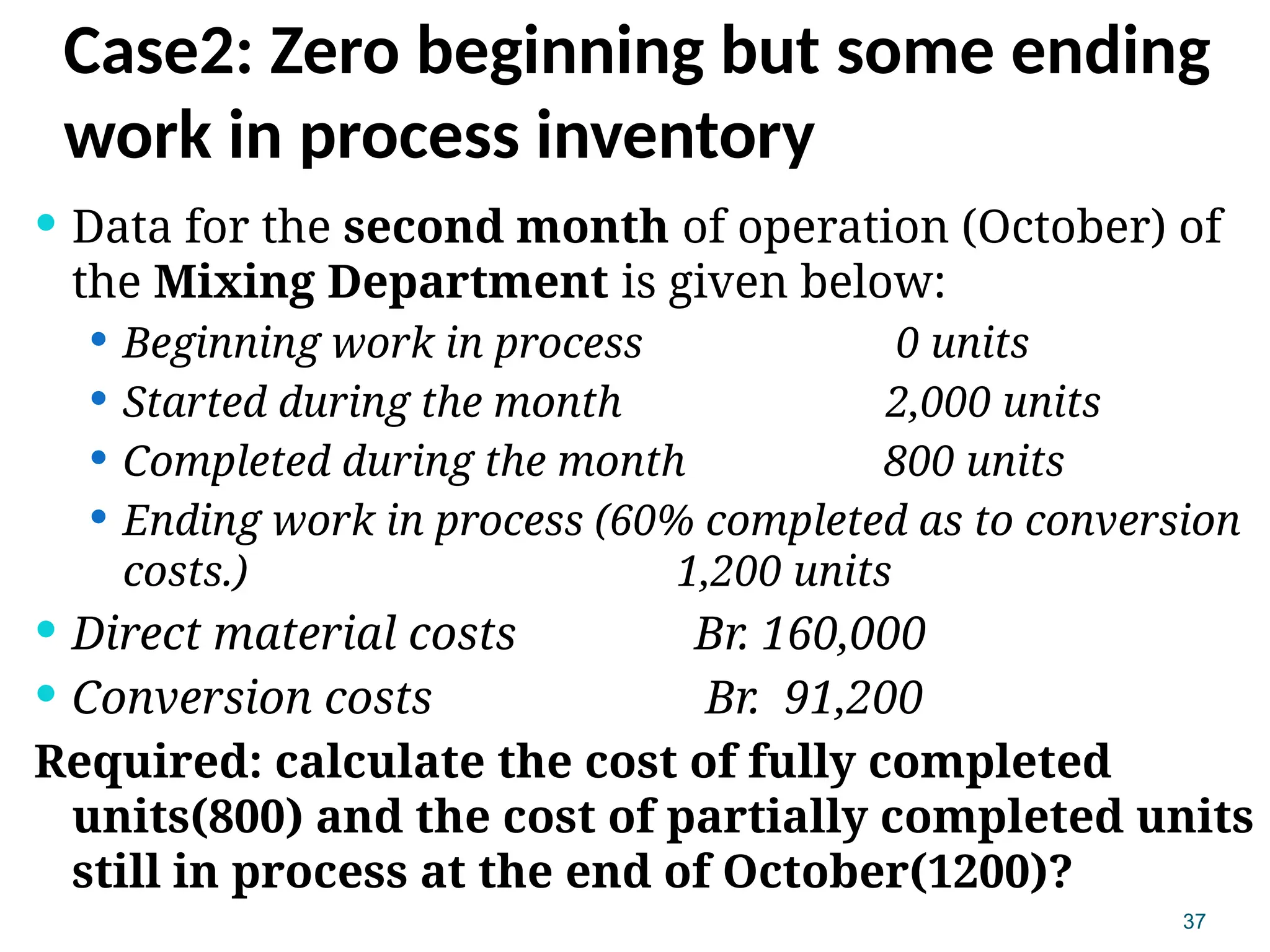

Case2: Zero beginningbut some ending

work in process inventory

Data for the second month of operation (October) of

the Mixing Department is given below:

Beginning work in process 0 units

Started during the month 2,000 units

Completed during the month 800 units

Ending work in process (60% completed as to conversion

costs.) 1,200 units

Direct material costs Br. 160,000

Conversion costs Br. 91,200

Required: calculate the cost of fully completed

units(800) and the cost of partially completed units

still in process at the end of October(1200)?

32.

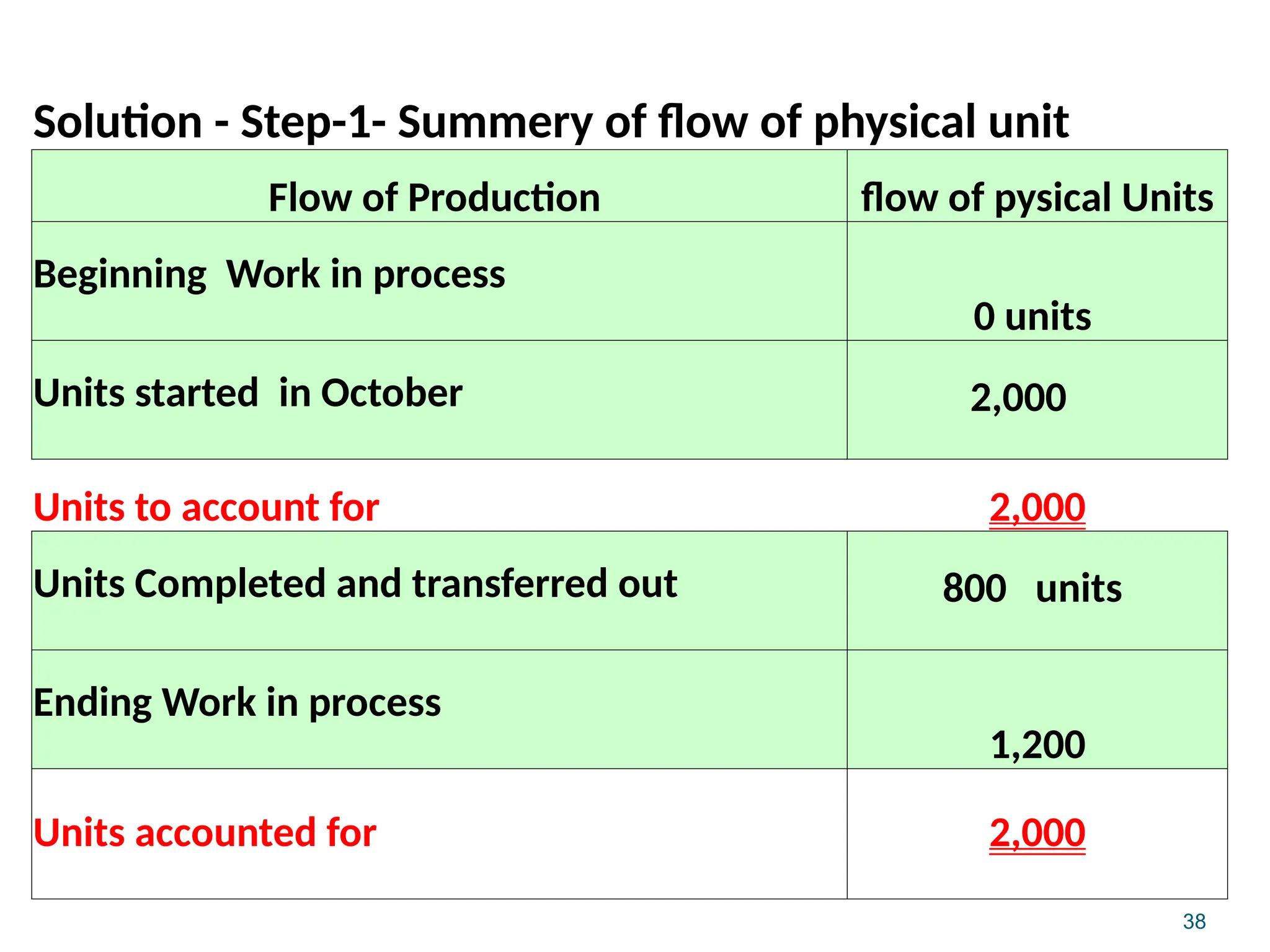

38

Solution - Step-1-Summery of flow of physical unit

Flow of Production flow of pysical Units

Beginning Work in process

0 units

Units started in October 2,000

Units to account for 2,000

Units Completed and transferred out 800 units

Ending Work in process

1,200

Units accounted for 2,000

33.

39

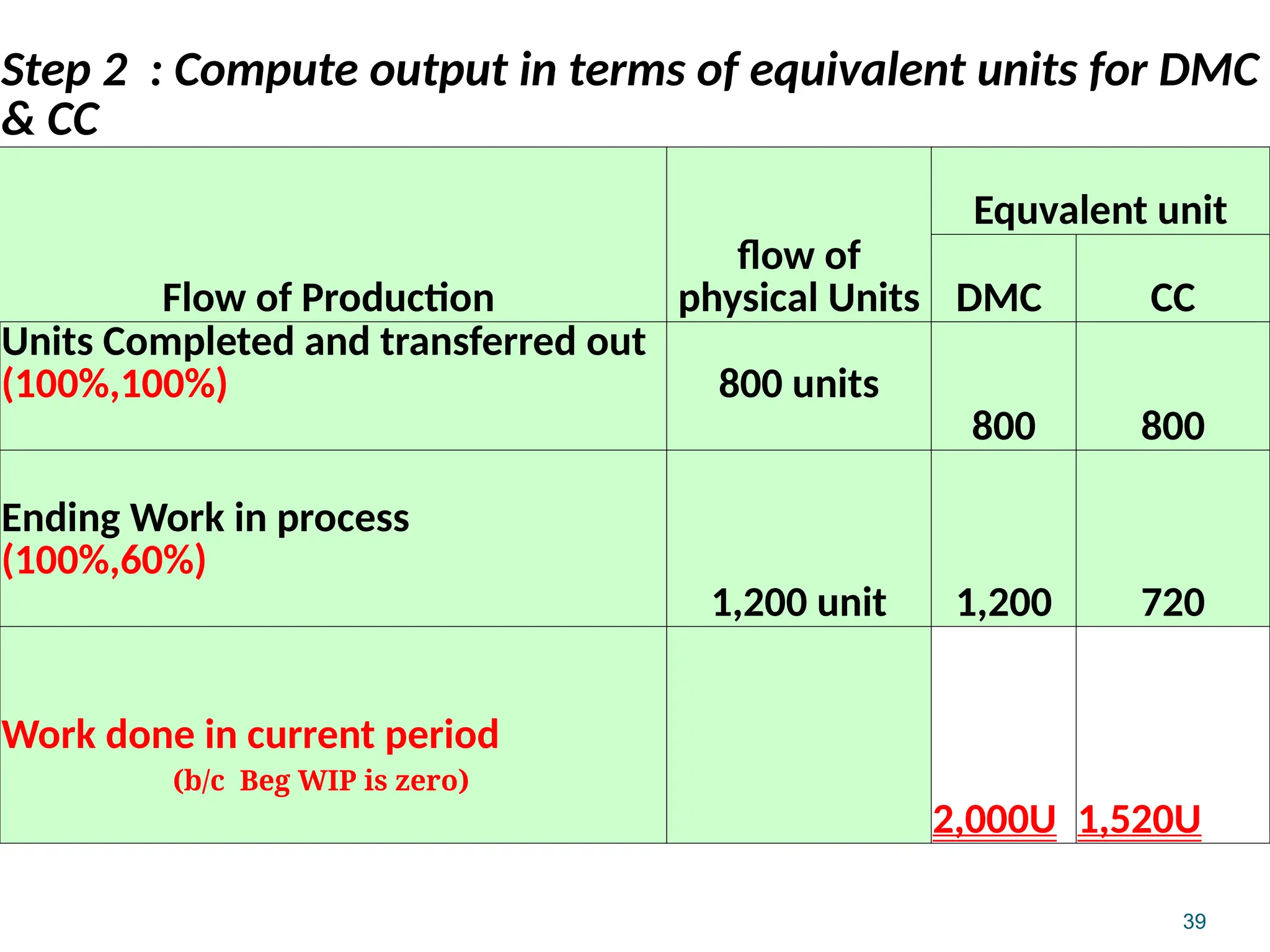

Step 2 :Compute output in terms of equivalent units for DMC

& CC

Flow of Production

flow of

physical Units

Equvalent unit

DMC CC

Units Completed and transferred out

(100%,100%) 800 units

800 800

Ending Work in process

(100%,60%)

1,200 unit 1,200 720

Work done in current period

(b/c Beg WIP is zero)

2,000U 1,520U

34.

40

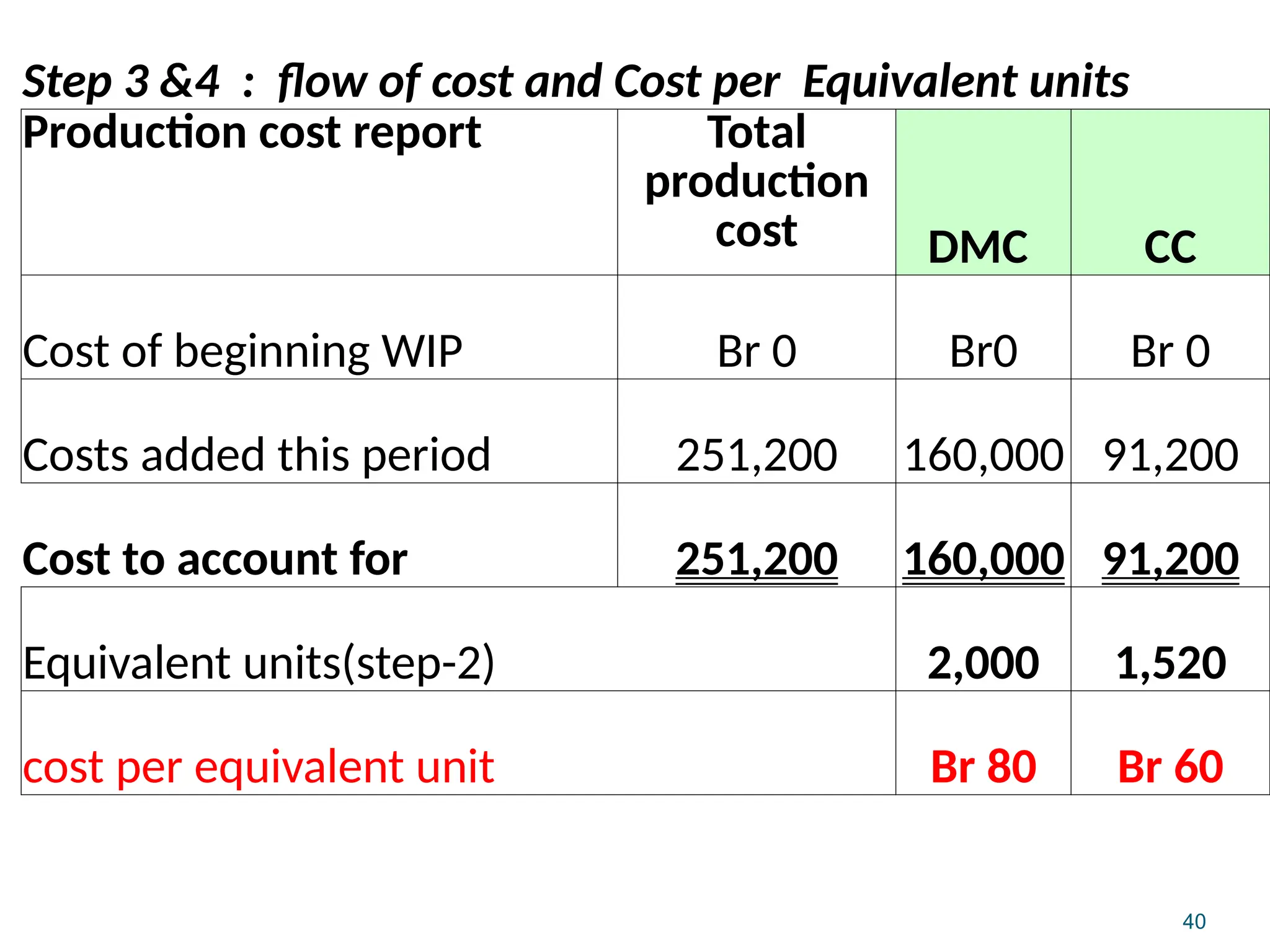

Step 3 &4: flow of cost and Cost per Equivalent units

Production cost report Total

production

cost DMC CC

Cost of beginning WIP Br 0 Br0 Br 0

Costs added this period 251,200 160,000 91,200

Cost to account for 251,200 160,000 91,200

Equivalent units(step-2) 2,000 1,520

cost per equivalent unit Br 80 Br 60

35.

41

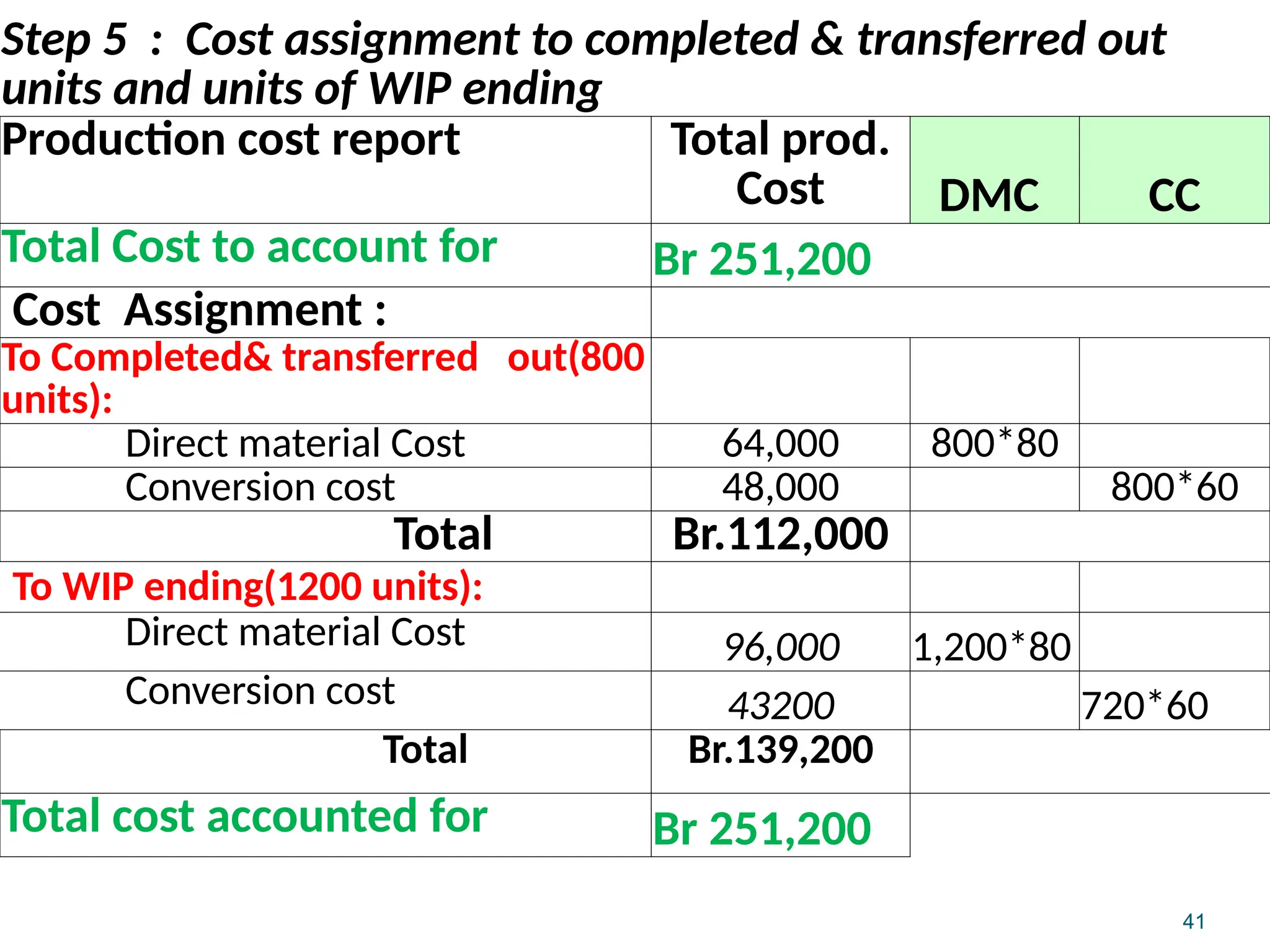

Step 5 :Cost assignment to completed & transferred out

units and units of WIP ending

Production cost report Total prod.

Cost DMC CC

Total Cost to account for Br 251,200

Cost Assignment :

To Completed& transferred out(800

units):

Direct material Cost 64,000 800*80

Conversion cost 48,000 800*60

Total Br.112,000

To WIP ending(1200 units):

Direct material Cost 96,000 1,200*80

Conversion cost 43200 720*60

Total Br.139,200

Total cost accounted for Br 251,200

36.

42

Journal Entries- forproduction during October

1. Work in Process- Mixing 160,000

RM -Inventory 160,000

(To record direct materials used in production)

2. Work in Process- Mixing 91,200

Various accounts 91,200

(To record Mixing department conversion costs)

3. Work in Process- Bottling 112,000

Work in Process- Mixing 112,000

(To record transfer units completed to bottling

department)

37.

43

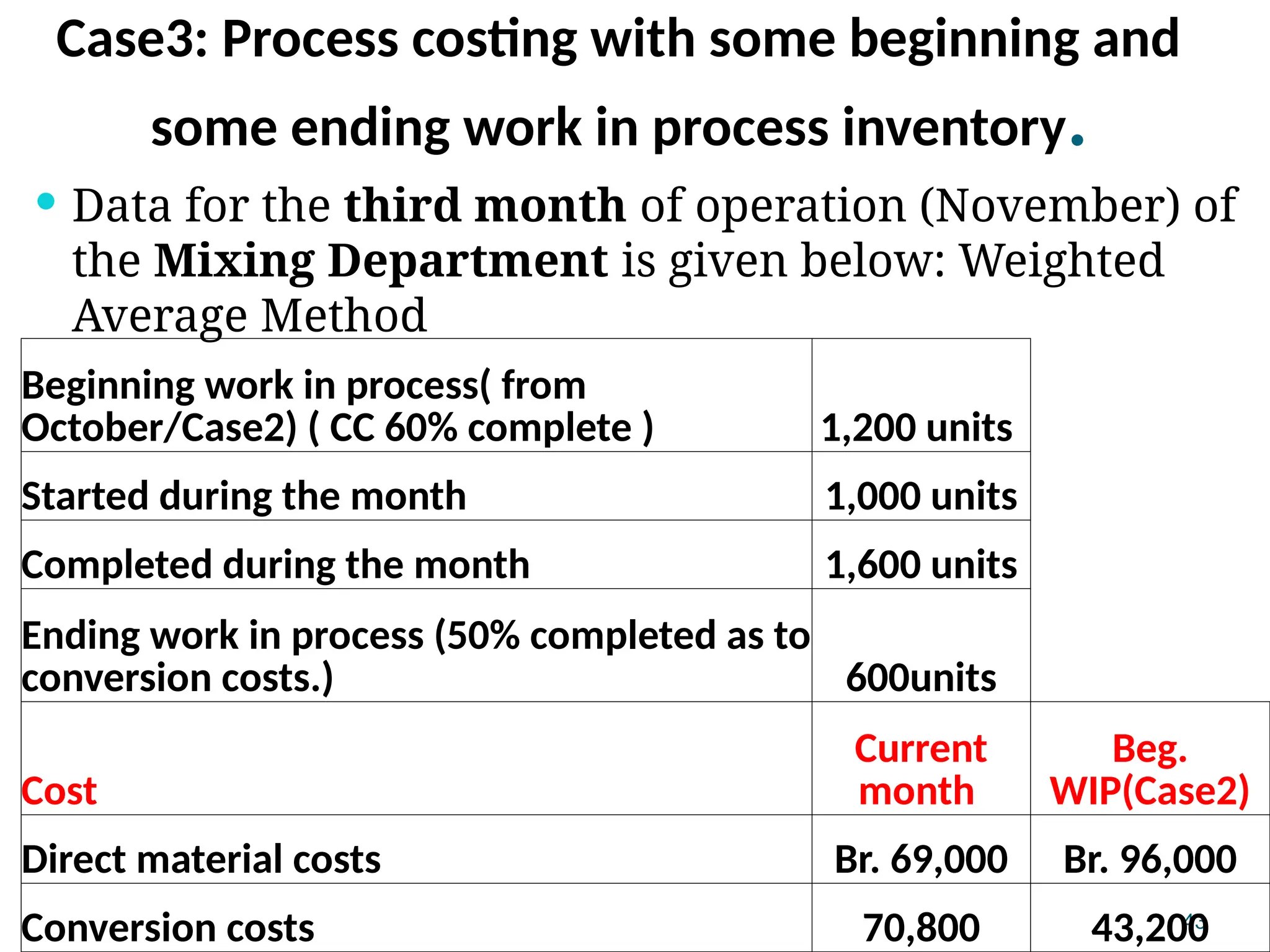

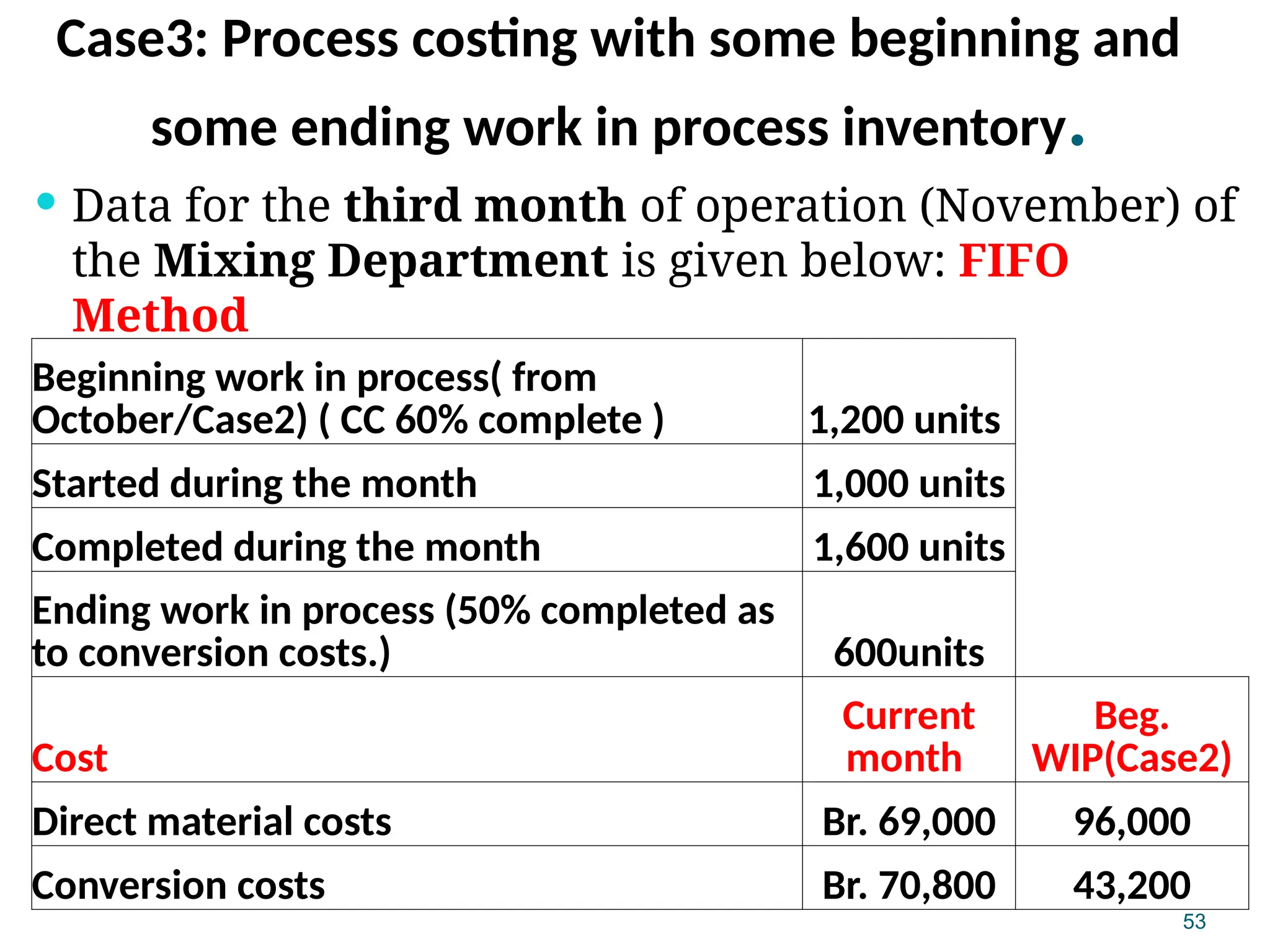

Case3: Process costingwith some beginning and

some ending work in process inventory.

Data for the third month of operation (November) of

the Mixing Department is given below: Weighted

Average Method

Beginning work in process( from

October/Case2) ( CC 60% complete ) 1,200 units

Started during the month 1,000 units

Completed during the month 1,600 units

Ending work in process (50% completed as to

conversion costs.) 600units

Cost

Current

month

Beg.

WIP(Case2)

Direct material costs Br. 69,000 Br. 96,000

Conversion costs 70,800 43,200

38.

44

When bothWIP beginning and ending have balances

, there two methods of process costing accounting:

1. Weighted Average Method

2. FIFO Method

39.

45

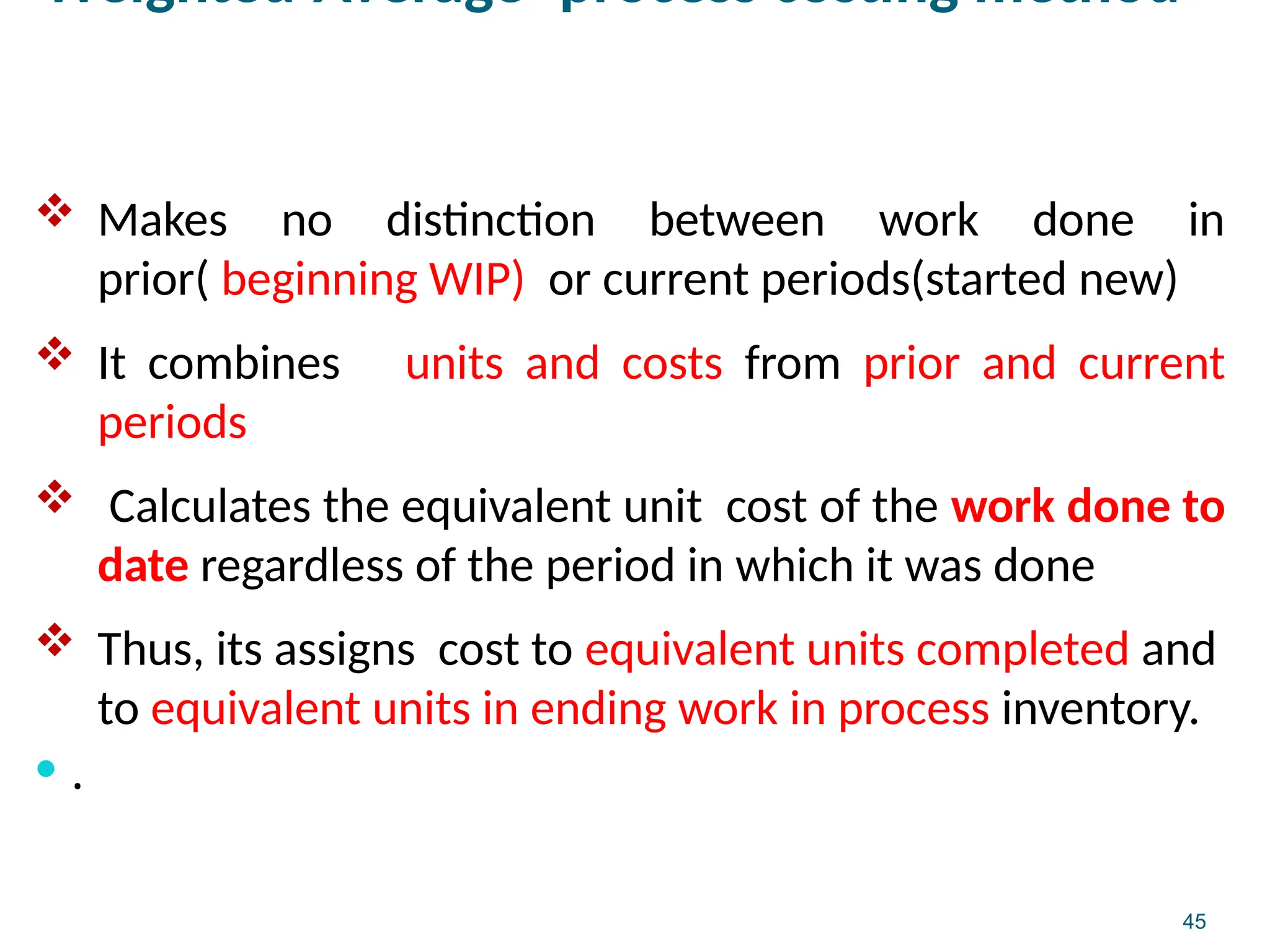

Weighted-Average -process costingmethod

Makes no distinction between work done in

prior( beginning WIP) or current periods(started new)

It combines units and costs from prior and current

periods

Calculates the equivalent unit cost of the work done to

date regardless of the period in which it was done

Thus, its assigns cost to equivalent units completed and

to equivalent units in ending work in process inventory.

.

40.

46

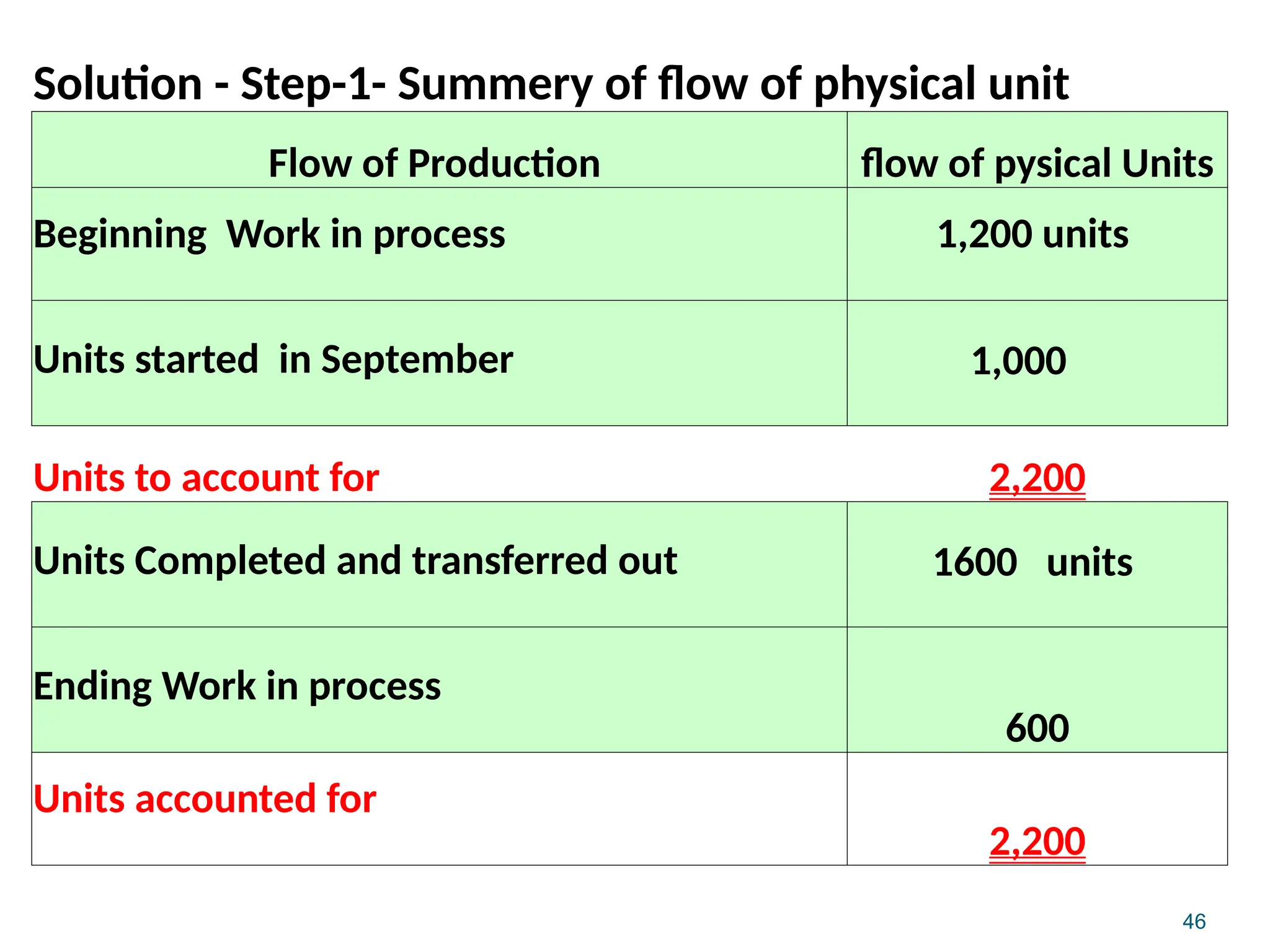

Solution - Step-1-Summery of flow of physical unit

Flow of Production flow of pysical Units

Beginning Work in process 1,200 units

Units started in September 1,000

Units to account for 2,200

Units Completed and transferred out 1600 units

Ending Work in process

600

Units accounted for

2,200

41.

47

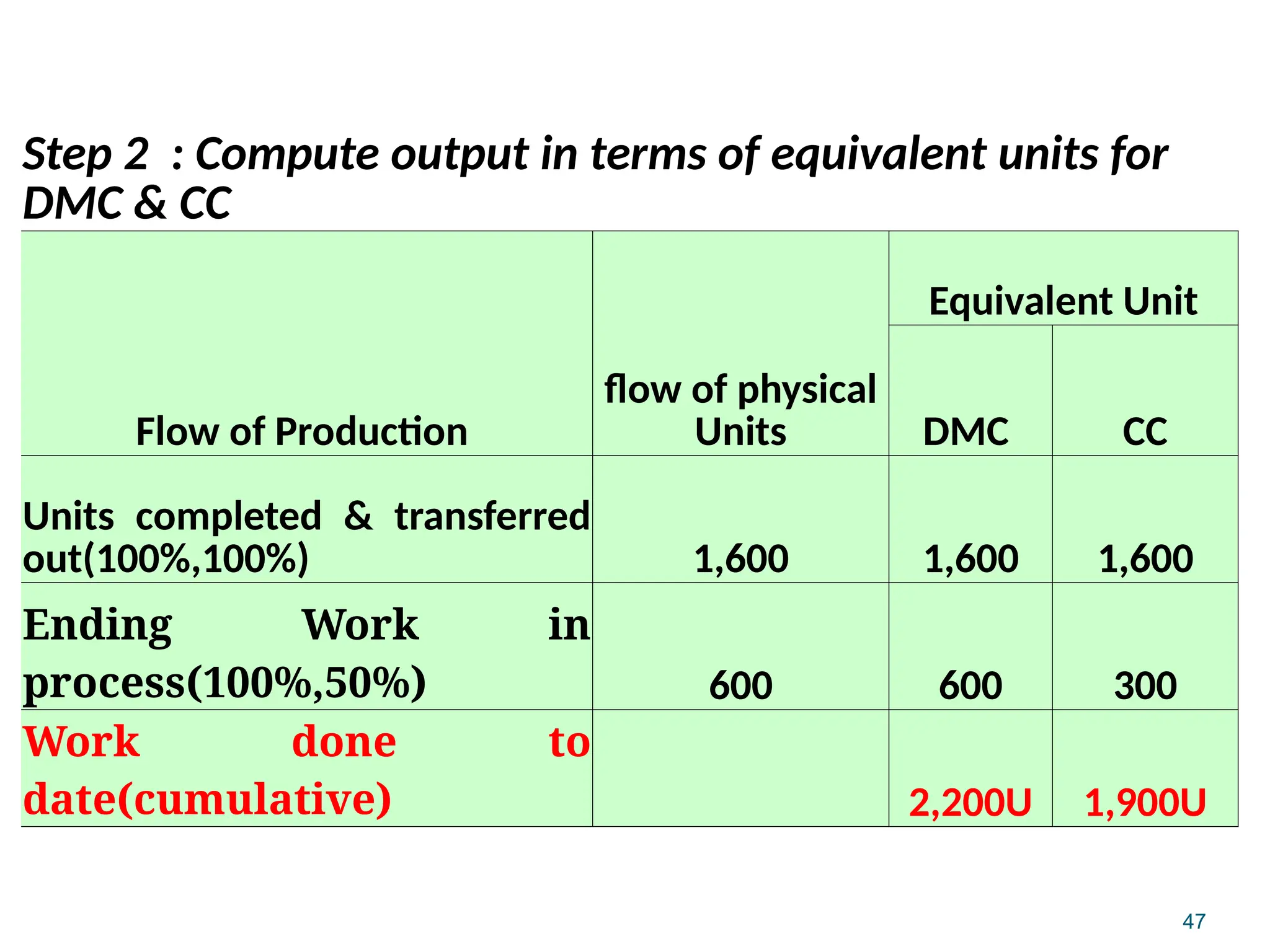

Step 2 :Compute output in terms of equivalent units for

DMC & CC

Flow of Production

flow of physical

Units

Equivalent Unit

DMC CC

Units completed & transferred

out(100%,100%) 1,600 1,600 1,600

Ending Work in

process(100%,50%) 600 600 300

Work done to

date(cumulative) 2,200U 1,900U

42.

48

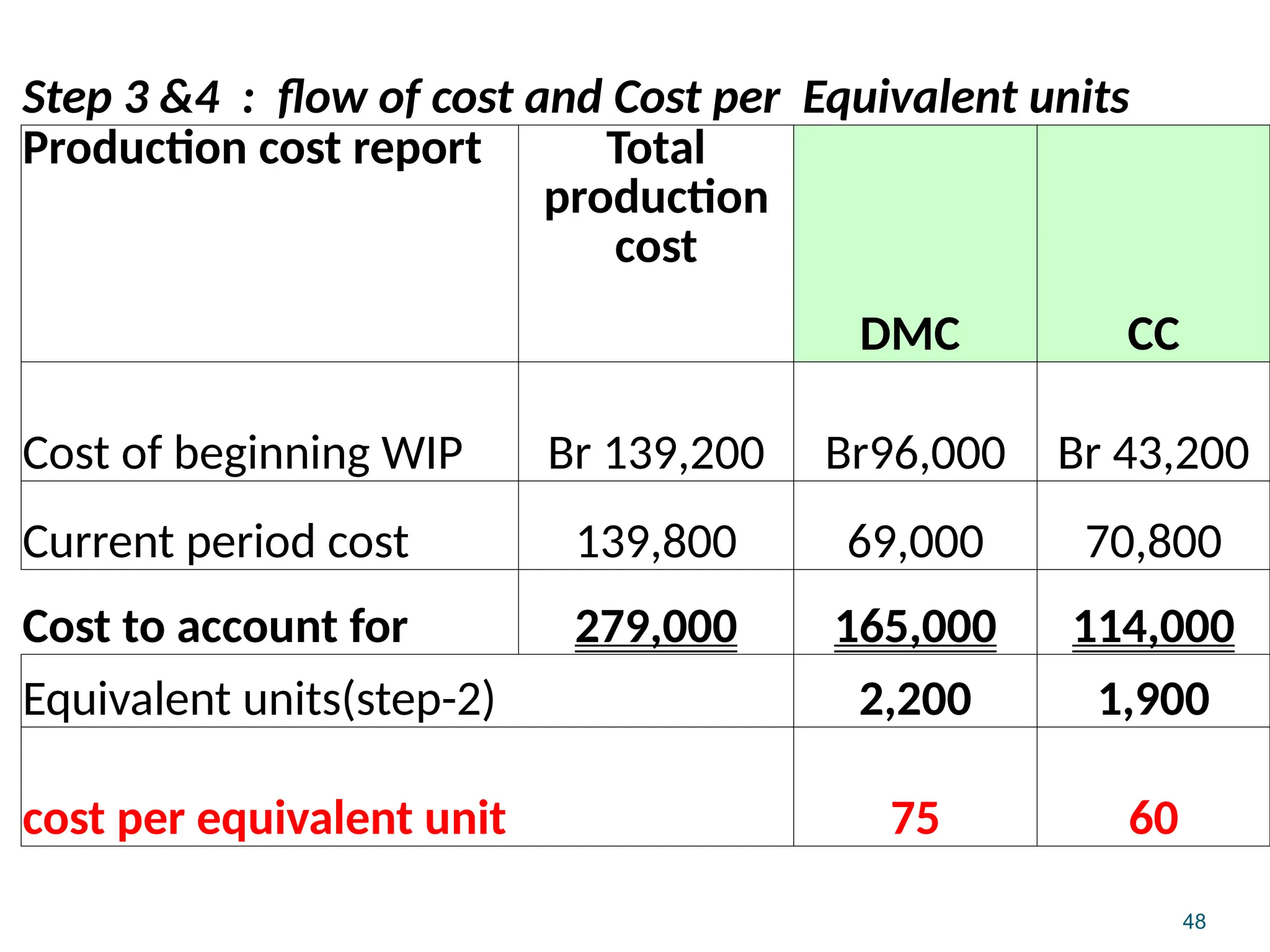

Step 3 &4: flow of cost and Cost per Equivalent units

Production cost report Total

production

cost

DMC CC

Cost of beginning WIP Br 139,200 Br96,000 Br 43,200

Current period cost 139,800 69,000 70,800

Cost to account for 279,000 165,000 114,000

Equivalent units(step-2) 2,200 1,900

cost per equivalent unit 75 60

43.

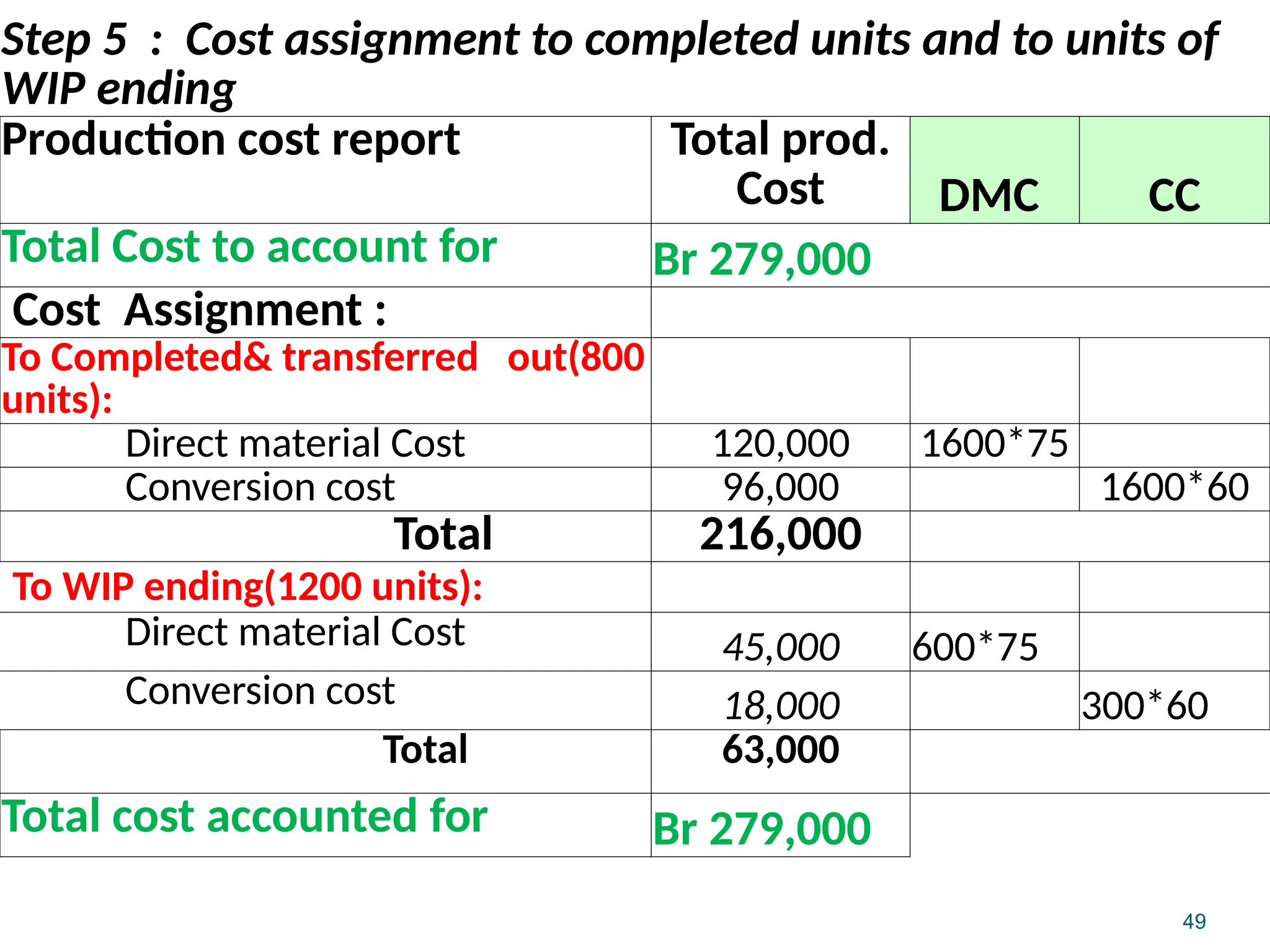

49

Step 5 :Cost assignment to completed units and to units of

WIP ending

Production cost report Total prod.

Cost DMC CC

Total Cost to account for Br 279,000

Cost Assignment :

To Completed& transferred out(800

units):

Direct material Cost 120,000 1600*75

Conversion cost 96,000 1600*60

Total 216,000

To WIP ending(1200 units):

Direct material Cost 45,000 600*75

Conversion cost 18,000 300*60

Total 63,000

Total cost accounted for Br 279,000

44.

50

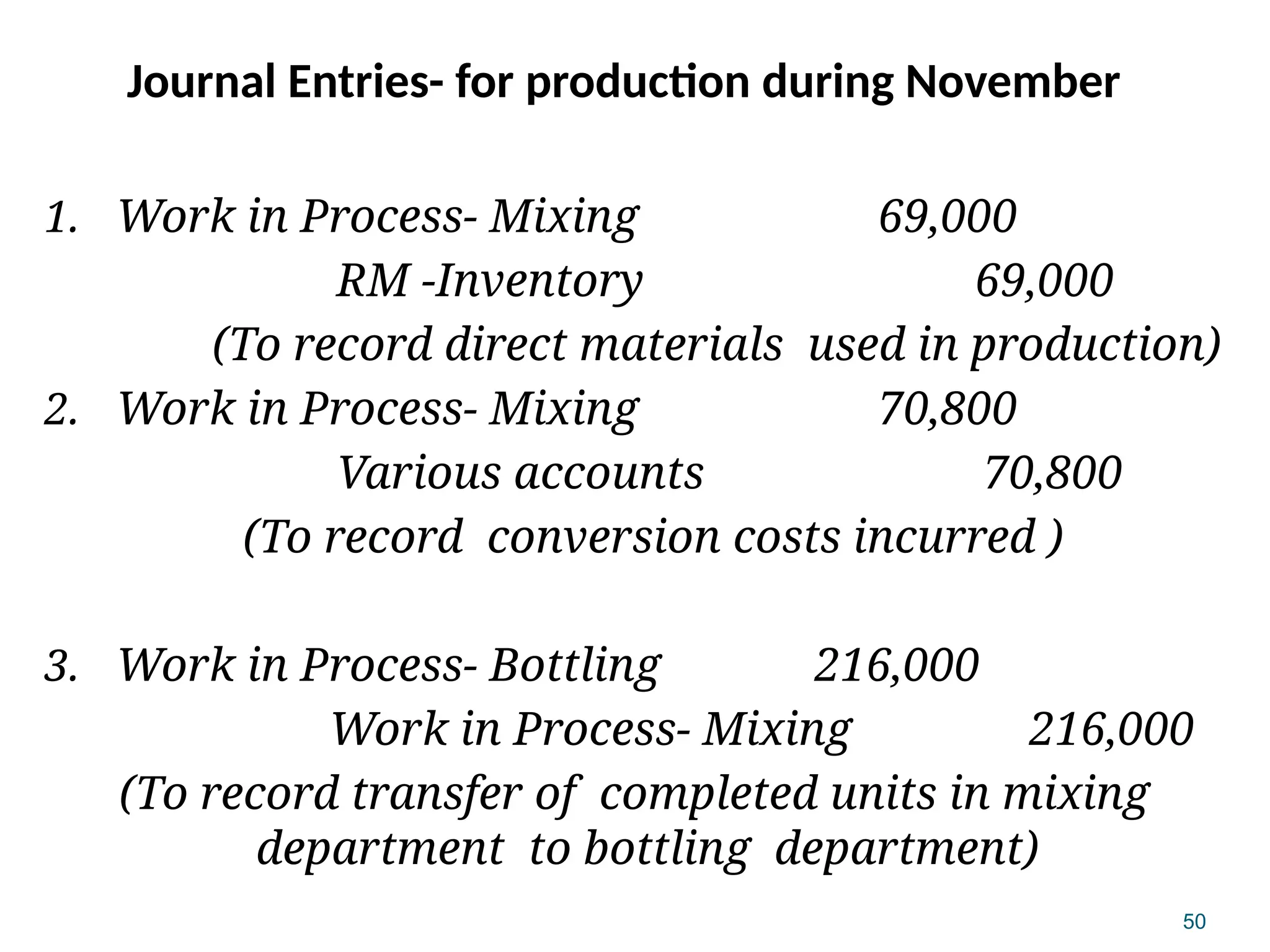

Journal Entries- forproduction during November

1. Work in Process- Mixing 69,000

RM -Inventory 69,000

(To record direct materials used in production)

2. Work in Process- Mixing 70,800

Various accounts 70,800

(To record conversion costs incurred )

3. Work in Process- Bottling 216,000

Work in Process- Mixing 216,000

(To record transfer of completed units in mixing

department to bottling department)

45.

51

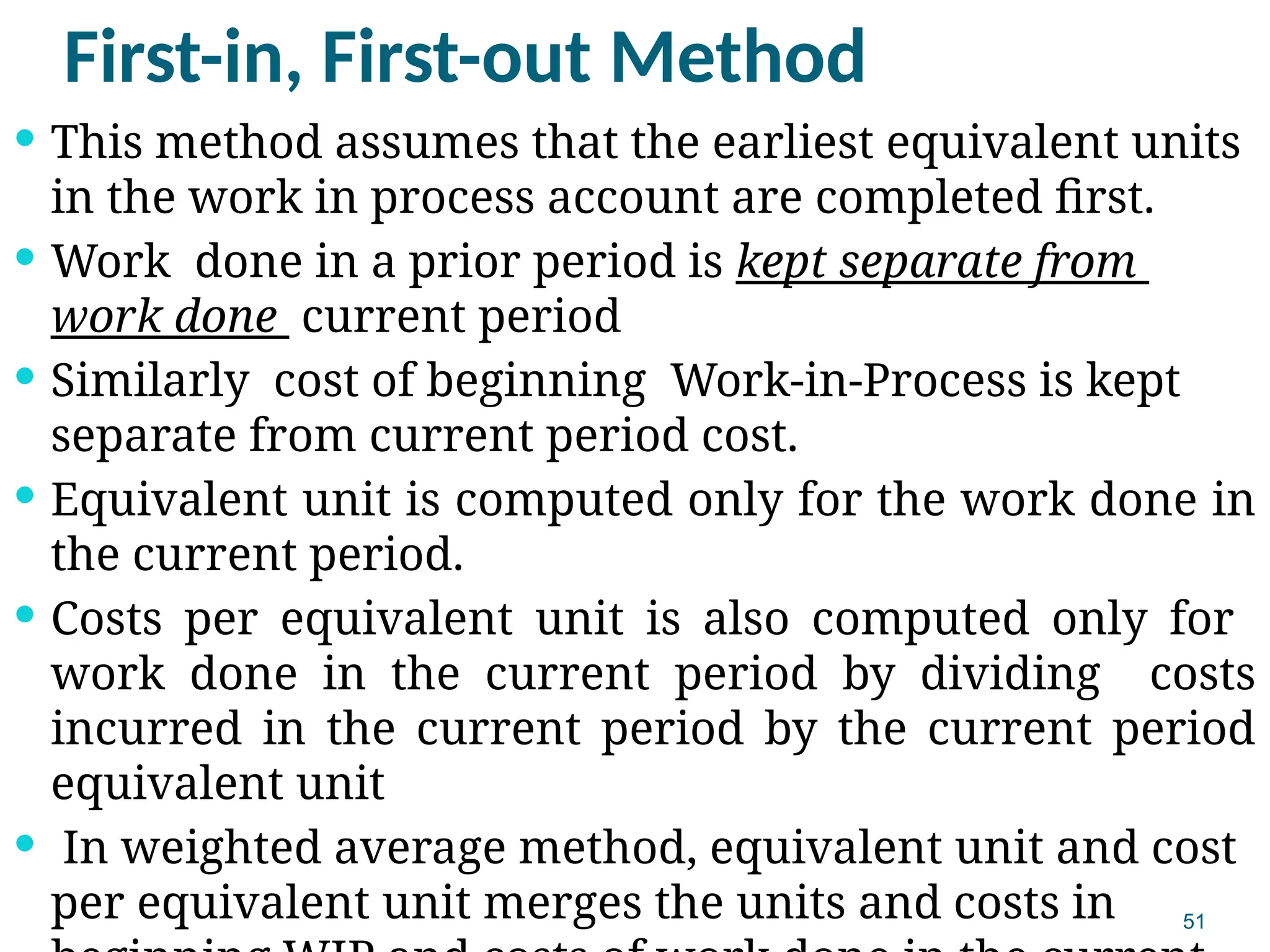

First-in, First-out Method

This method assumes that the earliest equivalent units

in the work in process account are completed first.

Work done in a prior period is kept separate from

work done current period

Similarly cost of beginning Work-in-Process is kept

separate from current period cost.

Equivalent unit is computed only for the work done in

the current period.

Costs per equivalent unit is also computed only for

work done in the current period by dividing costs

incurred in the current period by the current period

equivalent unit

In weighted average method, equivalent unit and cost

per equivalent unit merges the units and costs in

46.

52

First-in, First-out Methodcont…

Cost Assignment

Assigns the cost of beginning work-in process to

completed units

Assigns the cost of current period :

First to cost to complete beginning WIP

Next to completed units from new start

Lastly to units of ending work in process

Example: Assume the previous data of weighted average

method

47.

53

Case3: Process costingwith some beginning and

some ending work in process inventory.

Data for the third month of operation (November) of

the Mixing Department is given below: FIFO

Method

Beginning work in process( from

October/Case2) ( CC 60% complete ) 1,200 units

Started during the month 1,000 units

Completed during the month 1,600 units

Ending work in process (50% completed as

to conversion costs.) 600units

Cost

Current

month

Beg.

WIP(Case2)

Direct material costs Br. 69,000 96,000

Conversion costs Br. 70,800 43,200

48.

54

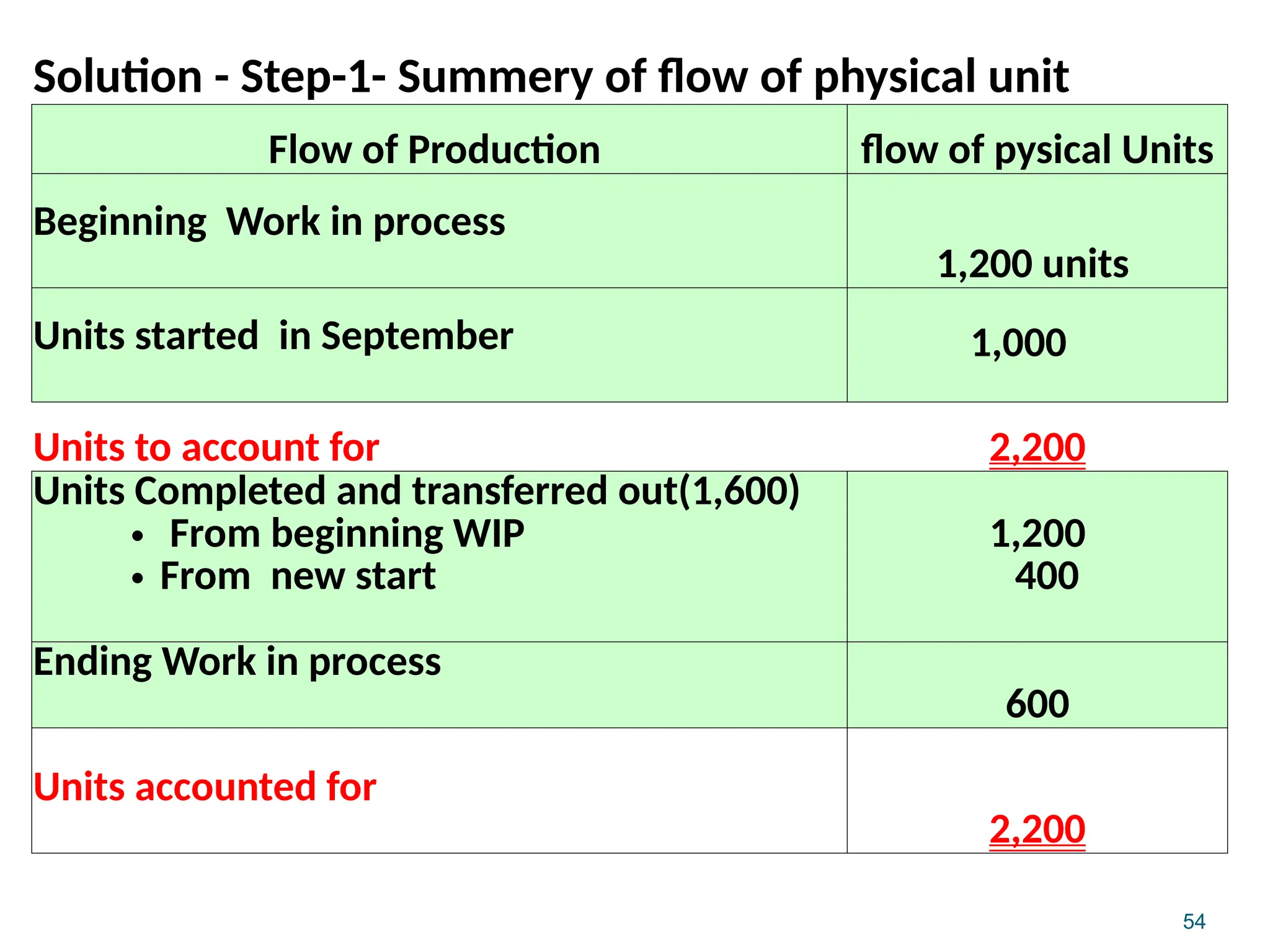

Solution - Step-1-Summery of flow of physical unit

Flow of Production flow of pysical Units

Beginning Work in process

1,200 units

Units started in September 1,000

Units to account for 2,200

Units Completed and transferred out(1,600)

• From beginning WIP

• From new start

1,200

400

Ending Work in process

600

Units accounted for

2,200

49.

55

Step 2 :Compute equivalent units for the work done in

the current month

Flow of Production

flow of

physical Units

Equivalent unit

DMC CC

Units completed & transferred

out

• From Beg. WIP(0%,40%)

•From new start (100%,100%)

1,200

400

0

400

480

400

Ending Work in process

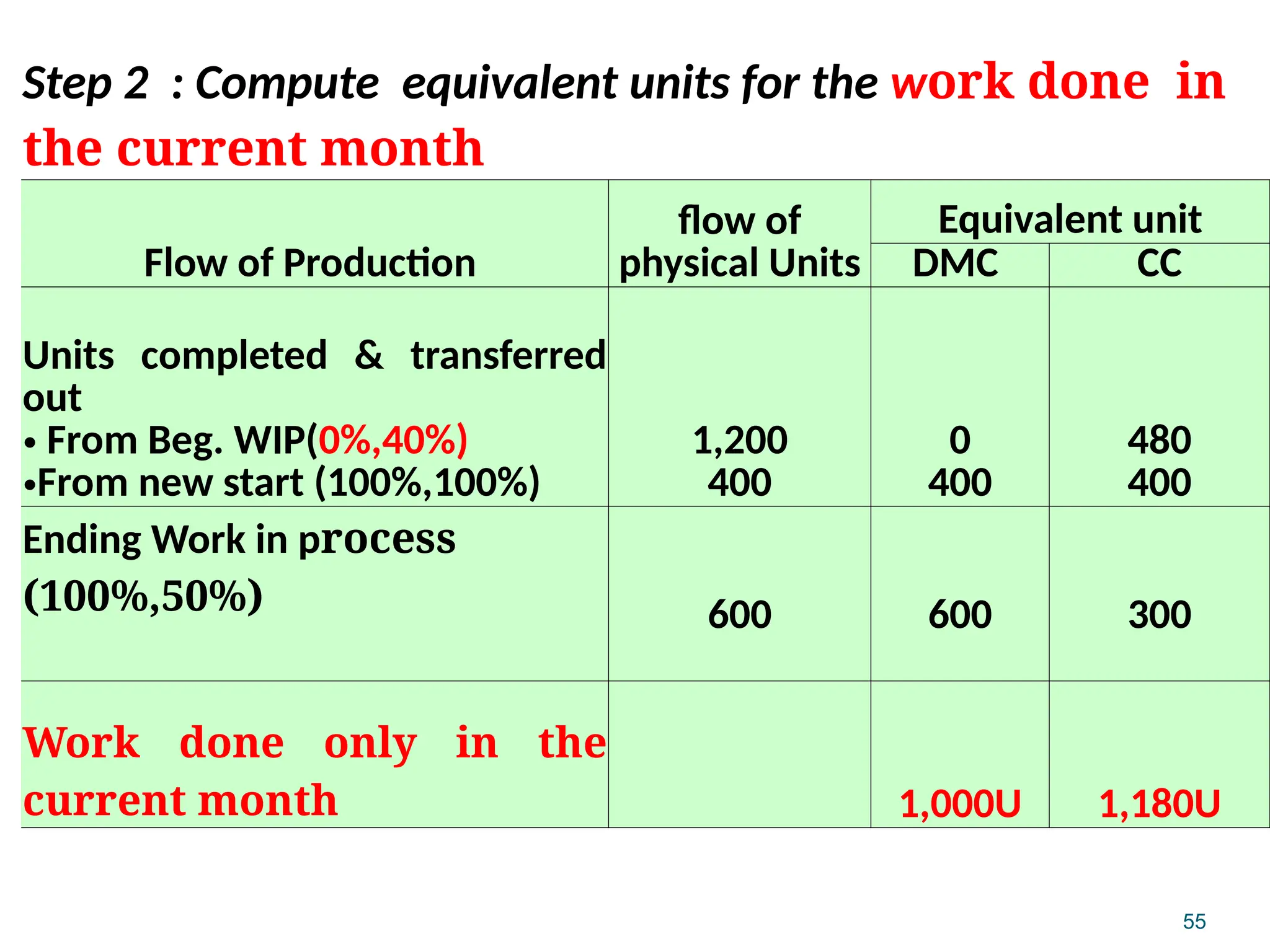

(100%,50%) 600 600 300

Work done only in the

current month 1,000U 1,180U

50.

56

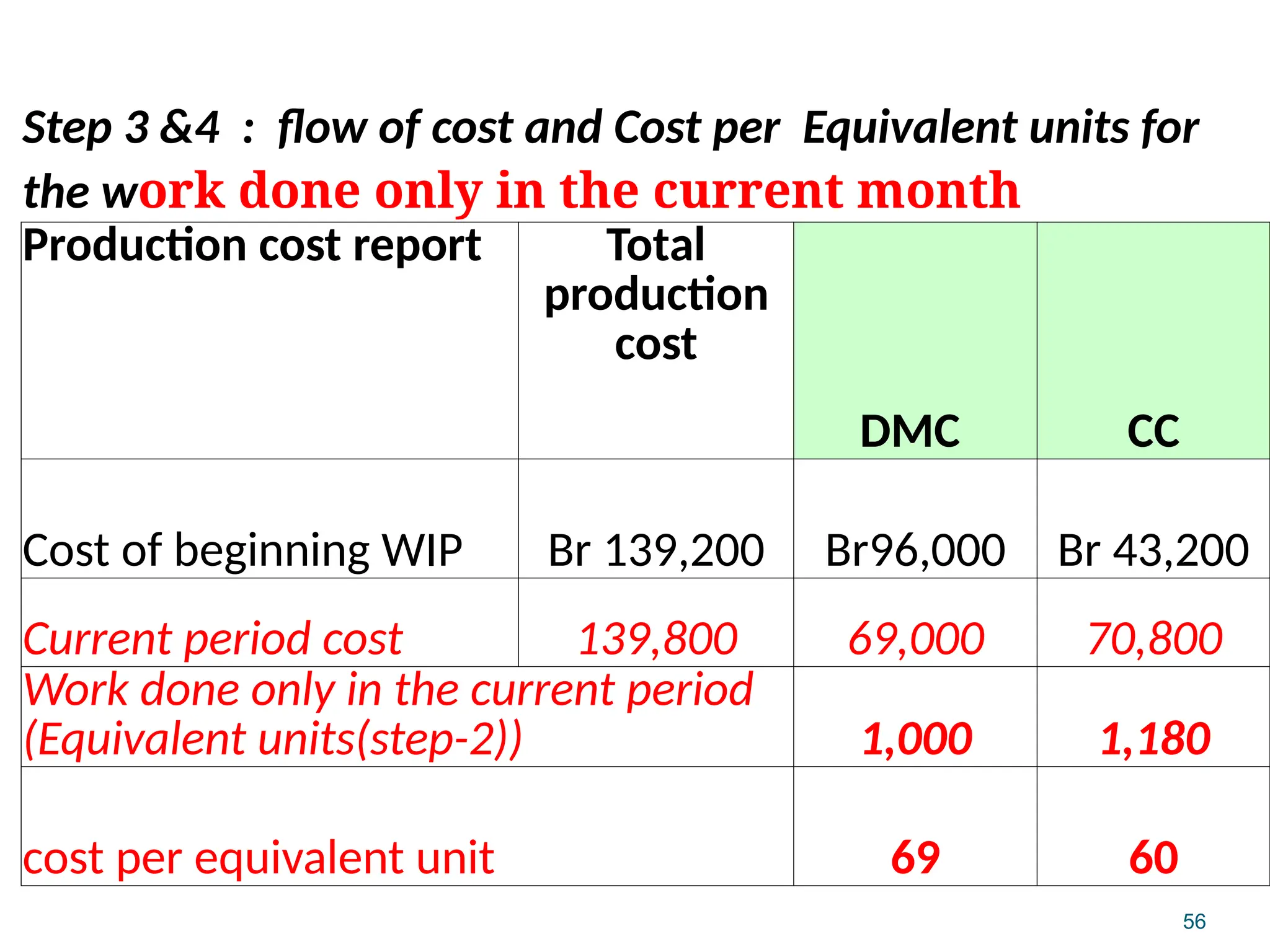

Step 3 &4: flow of cost and Cost per Equivalent units for

the work done only in the current month

Production cost report Total

production

cost

DMC CC

Cost of beginning WIP Br 139,200 Br96,000 Br 43,200

Current period cost 139,800 69,000 70,800

Work done only in the current period

(Equivalent units(step-2)) 1,000 1,180

cost per equivalent unit 69 60

51.

57

Step 5 :Cost assignment

Production cost report Total Cost DMC CC

Total Cost to account for Br 279,000

Cost Assignment :

To Completed& transferred

out(1600 units):

From Beginning WIP(1,200U)

Cost carried forward 139,200 96,000 43,200

Cost to complete them 28,800 0*69 480*60

From new start (400U) 51,600 400*69 400*60

Total 219,600

To WIP ending(600 units):

Direct material Cost 41,400 600*69

Conversion cost 18,000 300*60

Total 59,400

Total cost accounted for Br 279,000

52.

58

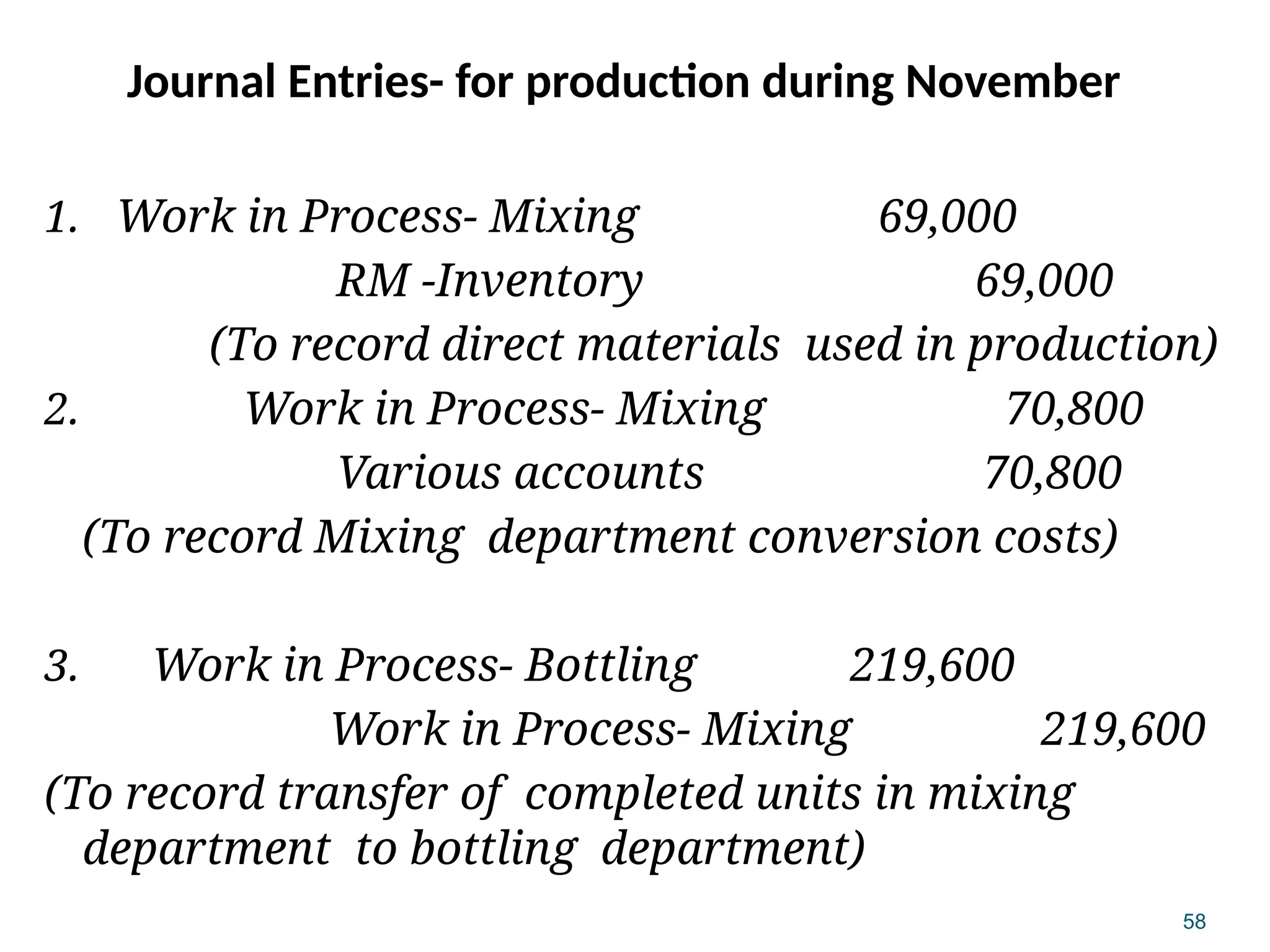

Journal Entries- forproduction during November

1. Work in Process- Mixing 69,000

RM -Inventory 69,000

(To record direct materials used in production)

2. Work in Process- Mixing 70,800

Various accounts 70,800

(To record Mixing department conversion costs)

3. Work in Process- Bottling 219,600

Work in Process- Mixing 219,600

(To record transfer of completed units in mixing

department to bottling department)

53.

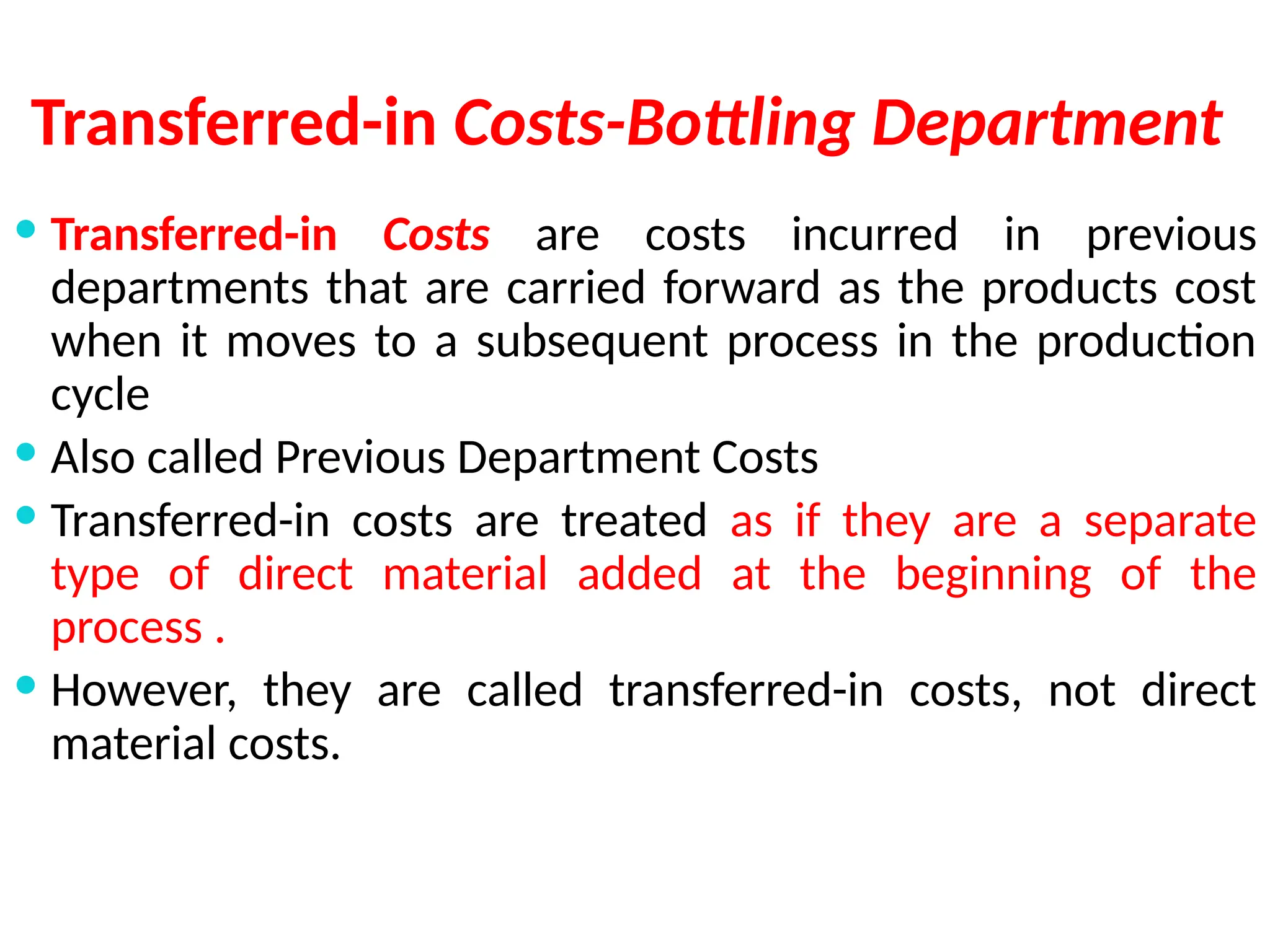

Transferred-in Costs-Bottling Department

Transferred-in Costs are costs incurred in previous

departments that are carried forward as the products cost

when it moves to a subsequent process in the production

cycle

Also called Previous Department Costs

Transferred-in costs are treated as if they are a separate

type of direct material added at the beginning of the

process .

However, they are called transferred-in costs, not direct

material costs.

54.

60

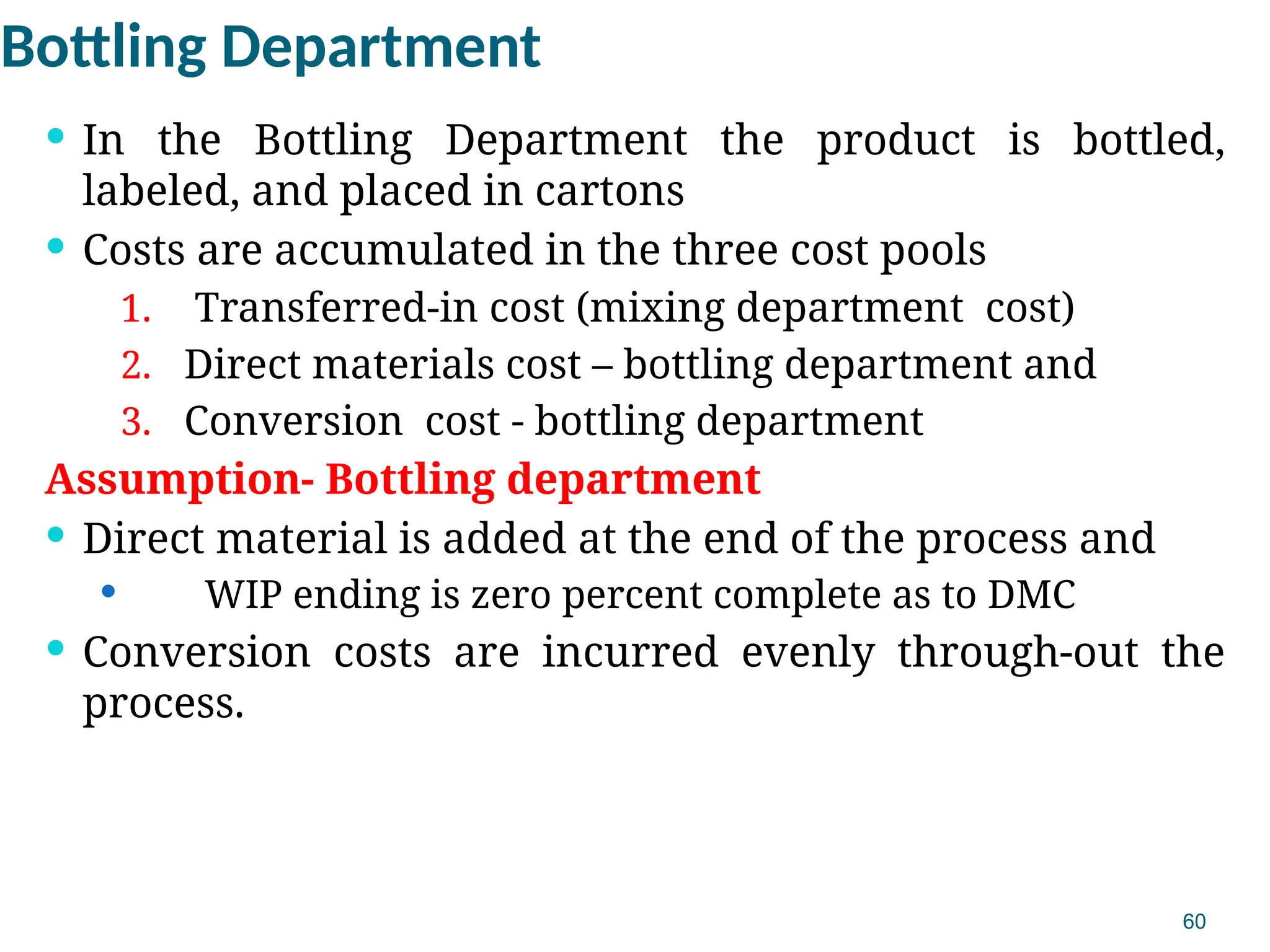

Bottling Department

Inthe Bottling Department the product is bottled,

labeled, and placed in cartons

Costs are accumulated in the three cost pools

1. Transferred-in cost (mixing department cost)

2. Direct materials cost – bottling department and

3. Conversion cost - bottling department

Assumption- Bottling department

Direct material is added at the end of the process and

WIP ending is zero percent complete as to DMC

Conversion costs are incurred evenly through-out the

process.

55.

61

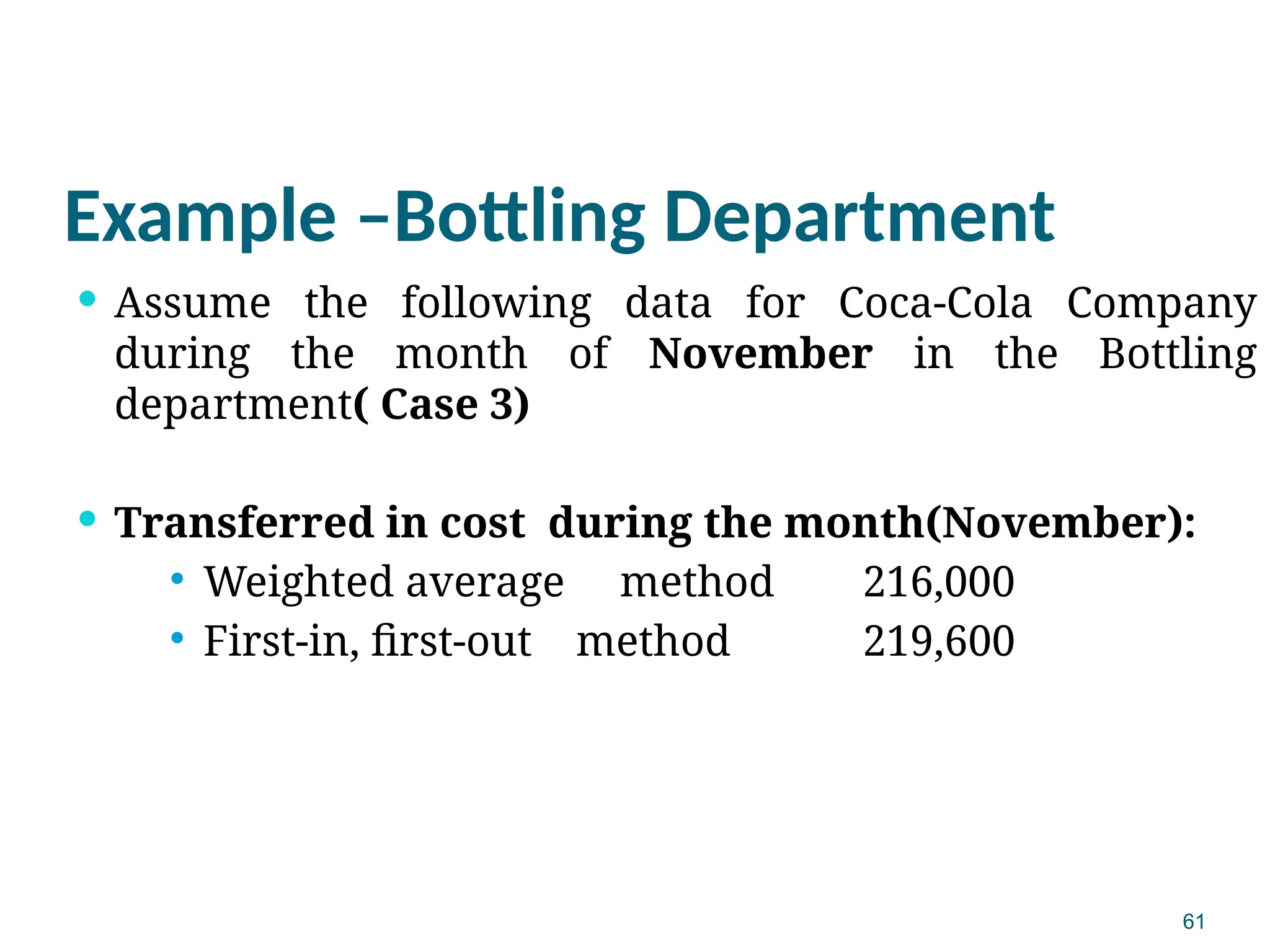

Example –Bottling Department

Assume the following data for Coca-Cola Company

during the month of November in the Bottling

department( Case 3)

Transferred in cost during the month(November):

Weighted average method 216,000

First-in, first-out method 219,600

56.

62

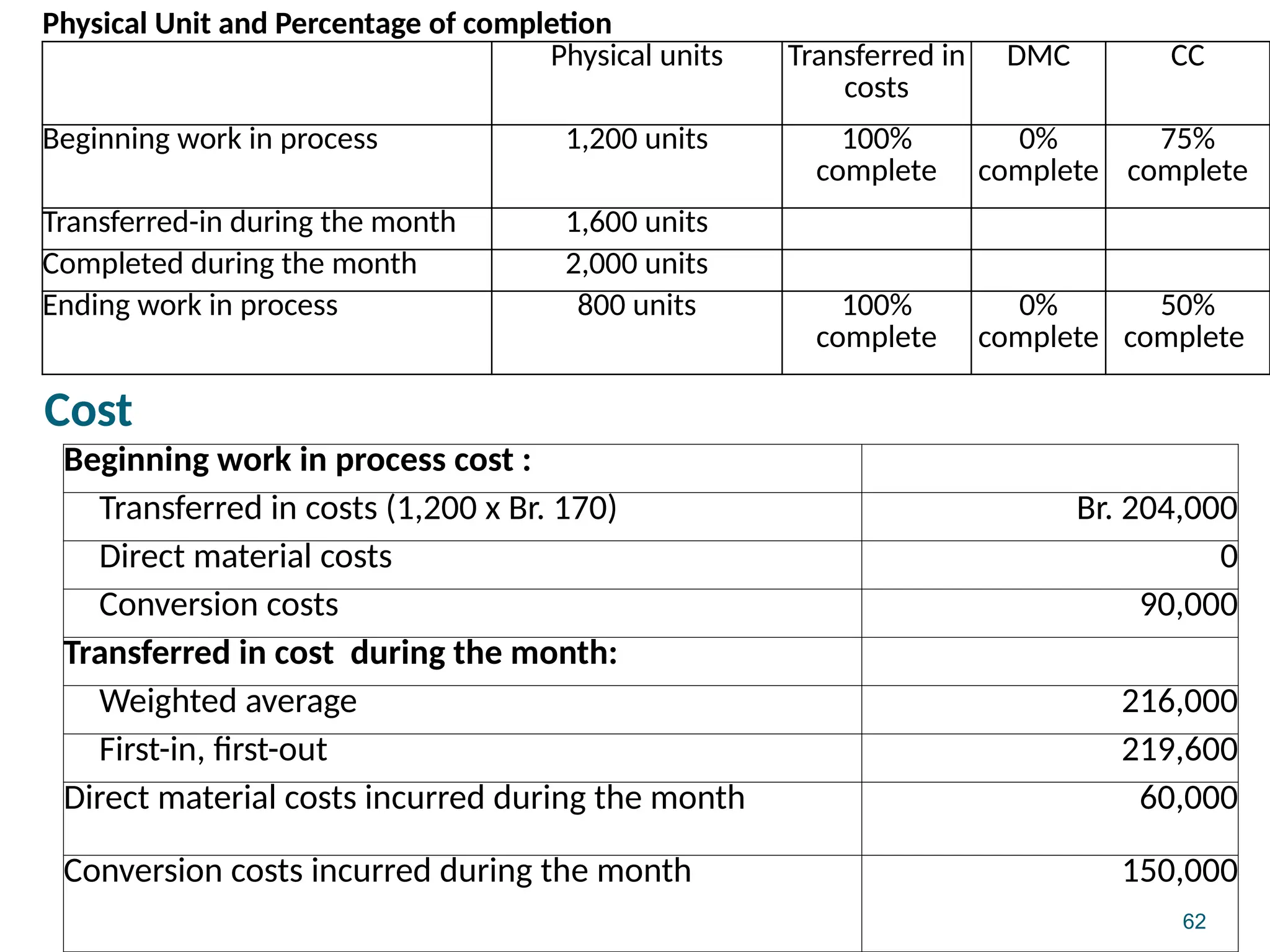

Physical Unit andPercentage of completion

Physical units Transferred in

costs

DMC CC

Beginning work in process 1,200 units 100%

complete

0%

complete

75%

complete

Transferred-in during the month 1,600 units

Completed during the month 2,000 units

Ending work in process 800 units 100%

complete

0%

complete

50%

complete

Cost

Beginning work in process cost :

Transferred in costs (1,200 x Br. 170) Br. 204,000

Direct material costs 0

Conversion costs 90,000

Transferred in cost during the month:

Weighted average 216,000

First-in, first-out 219,600

Direct material costs incurred during the month 60,000

Conversion costs incurred during the month 150,000

57.

63

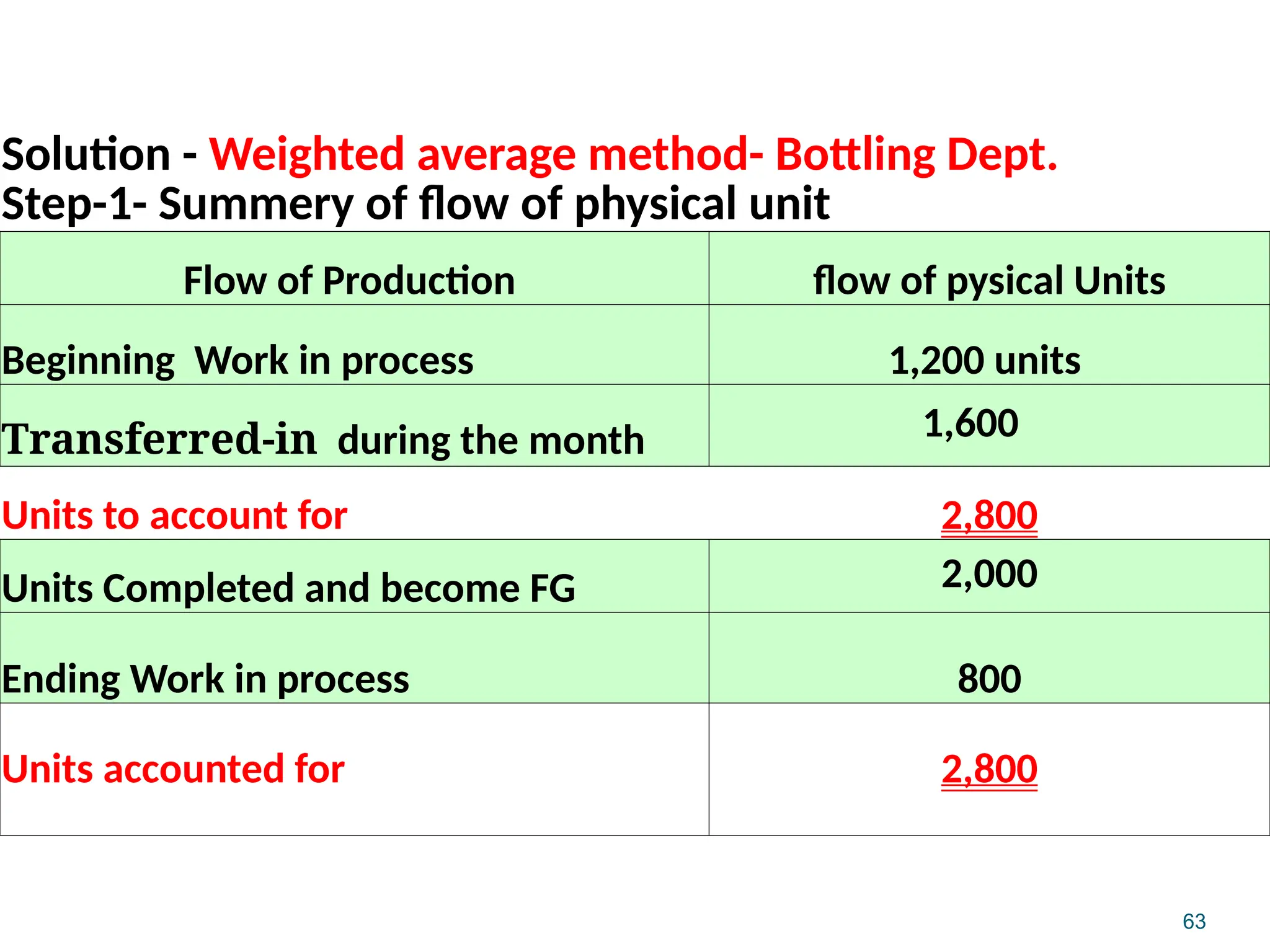

Solution - Weightedaverage method- Bottling Dept.

Step-1- Summery of flow of physical unit

Flow of Production flow of pysical Units

Beginning Work in process 1,200 units

Transferred-in during the month 1,600

Units to account for 2,800

Units Completed and become FG 2,000

Ending Work in process 800

Units accounted for 2,800

58.

64

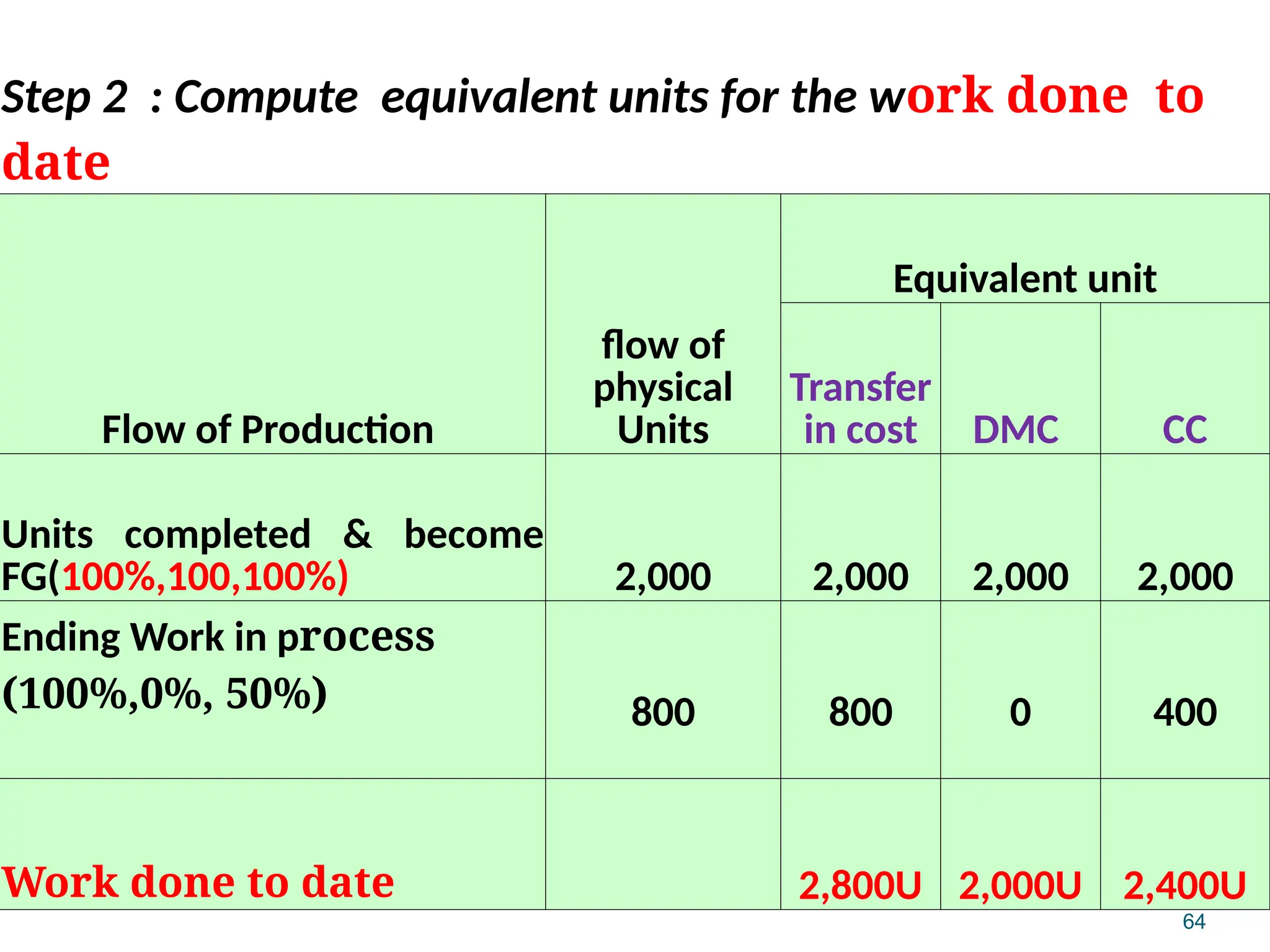

Step 2 :Compute equivalent units for the work done to

date

Flow of Production

flow of

physical

Units

Equivalent unit

Transfer

in cost DMC CC

Units completed & become

FG(100%,100,100%) 2,000 2,000 2,000 2,000

Ending Work in process

(100%,0%, 50%) 800 800 0 400

Work done to date 2,800U 2,000U 2,400U

59.

65

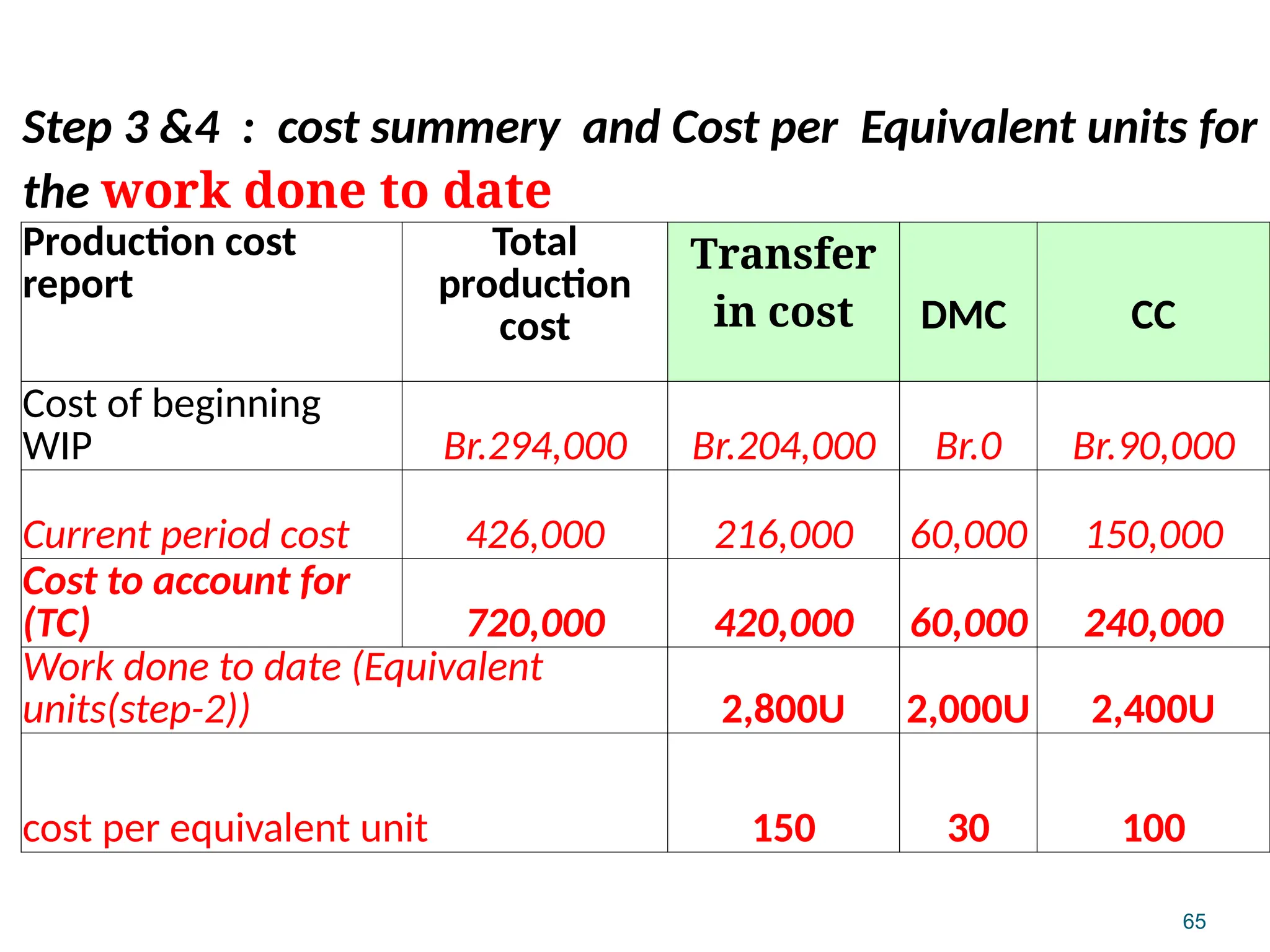

Step 3 &4: cost summery and Cost per Equivalent units for

the work done to date

Production cost

report

Total

production

cost

Transfer

in cost DMC CC

Cost of beginning

WIP Br.294,000 Br.204,000 Br.0 Br.90,000

Current period cost 426,000 216,000 60,000 150,000

Cost to account for

(TC) 720,000 420,000 60,000 240,000

Work done to date (Equivalent

units(step-2)) 2,800U 2,000U 2,400U

cost per equivalent unit 150 30 100

60.

66

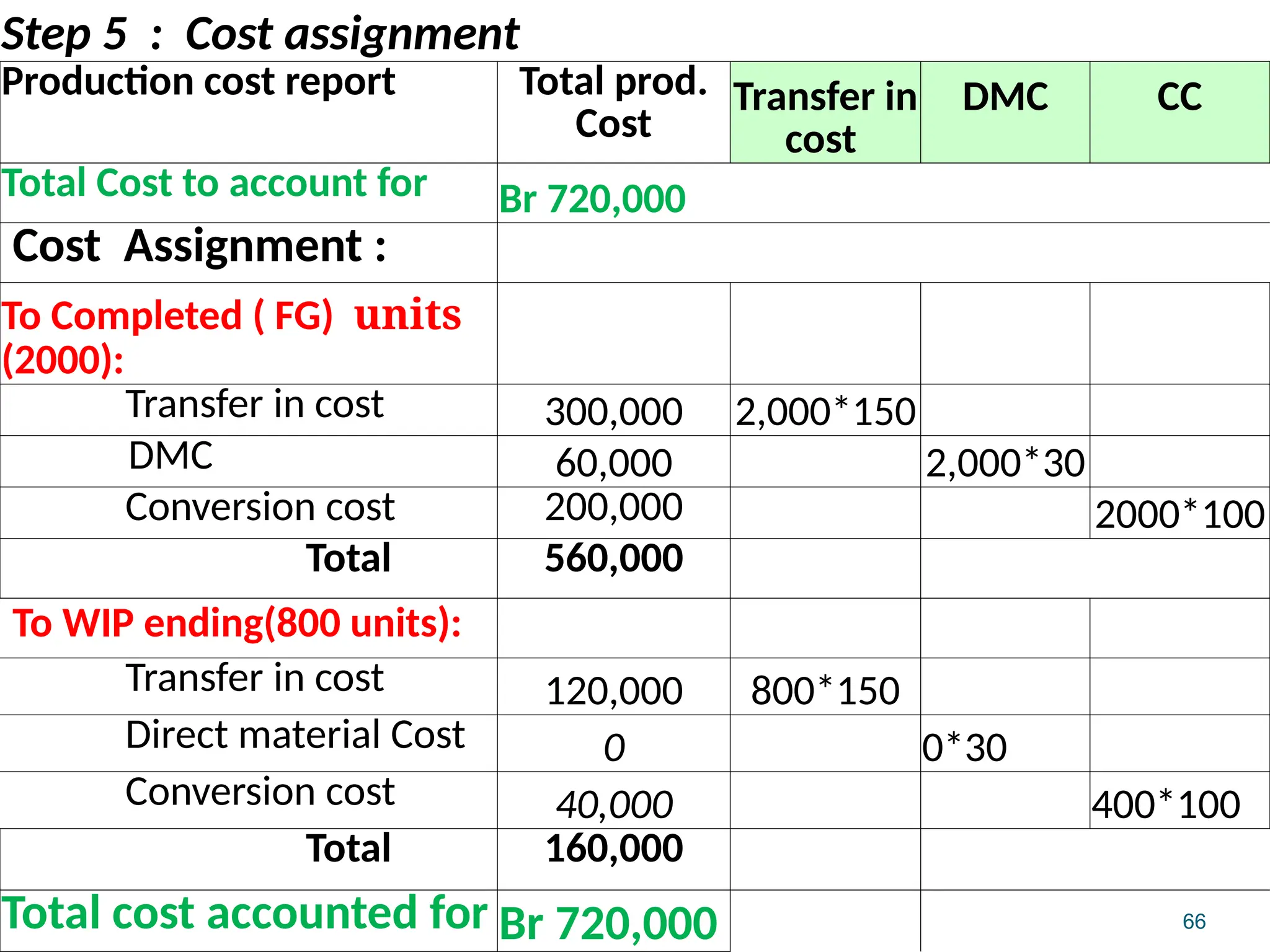

Step 5 :Cost assignment

Production cost report Total prod.

Cost

Transfer in

cost

DMC CC

Total Cost to account for Br 720,000

Cost Assignment :

To Completed ( FG) units

(2000):

Transfer in cost 300,000 2,000*150

DMC 60,000 2,000*30

Conversion cost 200,000 2000*100

Total 560,000

To WIP ending(800 units):

Transfer in cost 120,000 800*150

Direct material Cost 0 0*30

Conversion cost 40,000 400*100

Total 160,000

Total cost accounted for Br 720,000

61.

67

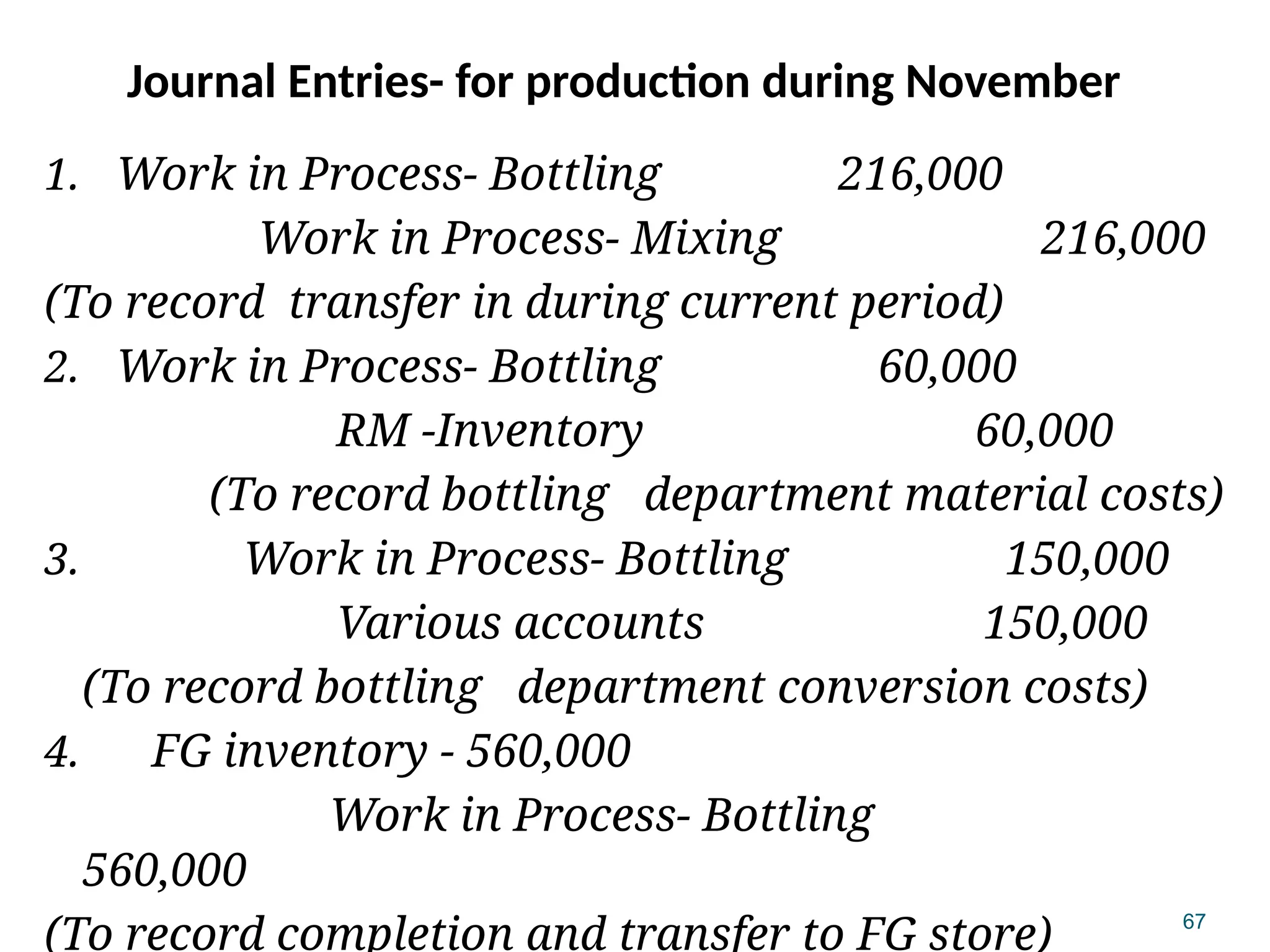

Journal Entries- forproduction during November

1. Work in Process- Bottling 216,000

Work in Process- Mixing 216,000

(To record transfer in during current period)

2. Work in Process- Bottling 60,000

RM -Inventory 60,000

(To record bottling department material costs)

3. Work in Process- Bottling 150,000

Various accounts 150,000

(To record bottling department conversion costs)

4. FG inventory - 560,000

Work in Process- Bottling

560,000

(To record completion and transfer to FG store)

69

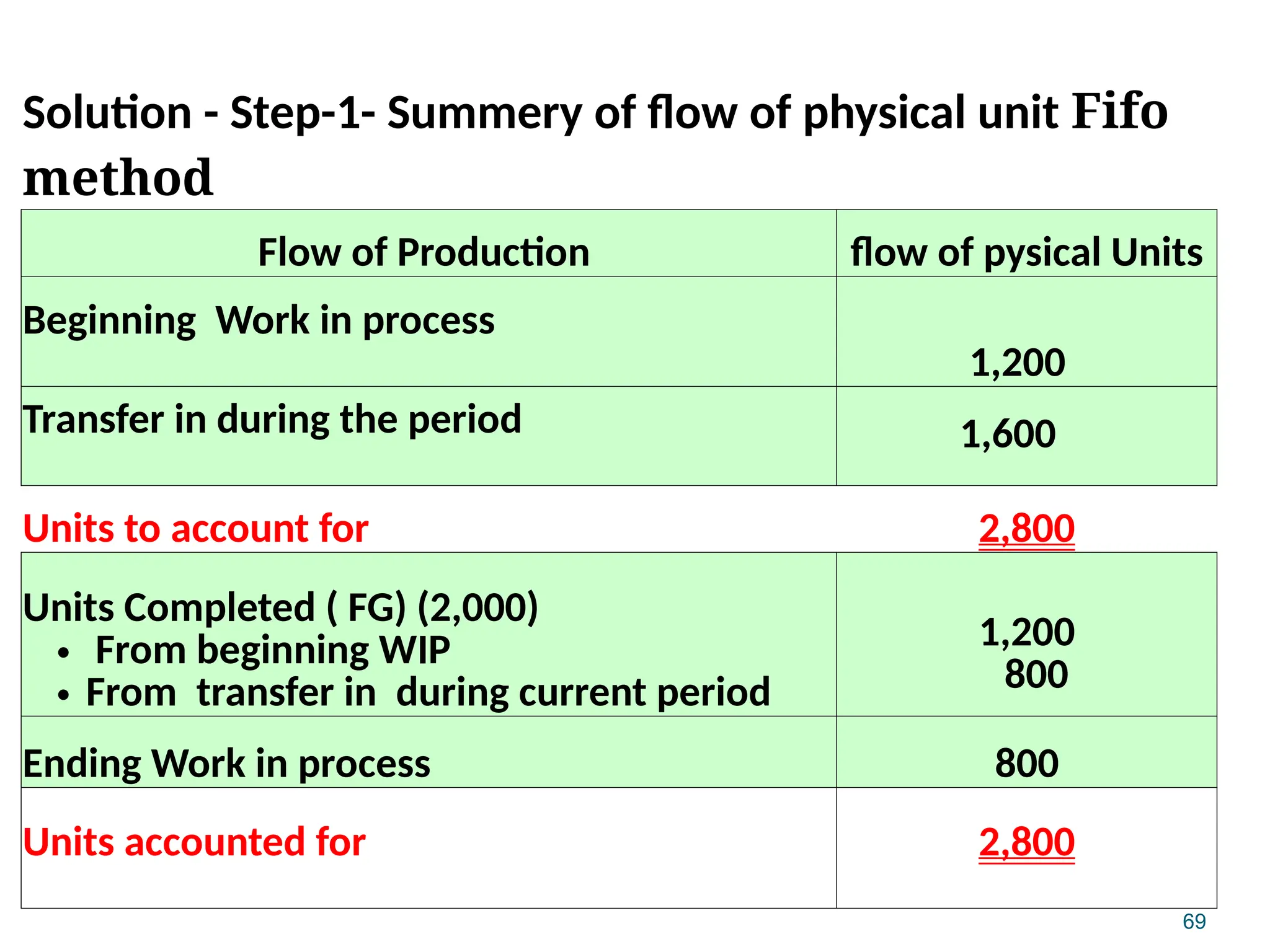

Solution - Step-1-Summery of flow of physical unit Fifo

method

Flow of Production flow of pysical Units

Beginning Work in process

1,200

Transfer in during the period 1,600

Units to account for 2,800

Units Completed ( FG) (2,000)

• From beginning WIP

• From transfer in during current period

1,200

800

Ending Work in process 800

Units accounted for 2,800

64.

70

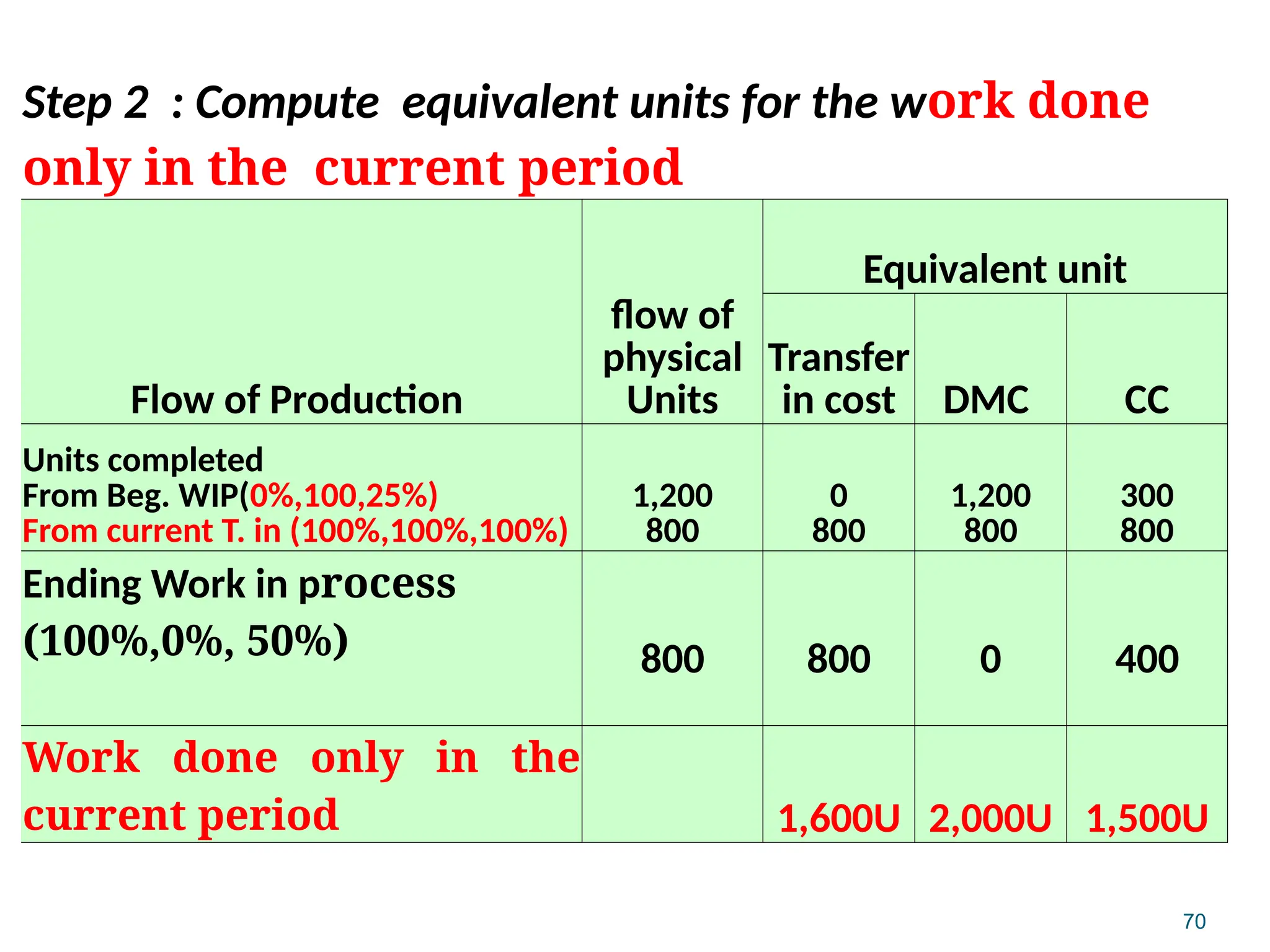

Step 2 :Compute equivalent units for the work done

only in the current period

Flow of Production

flow of

physical

Units

Equivalent unit

Transfer

in cost DMC CC

Units completed

From Beg. WIP(0%,100,25%)

From current T. in (100%,100%,100%)

1,200

800

0

800

1,200

800

300

800

Ending Work in process

(100%,0%, 50%) 800 800 0 400

Work done only in the

current period 1,600U 2,000U 1,500U

65.

71

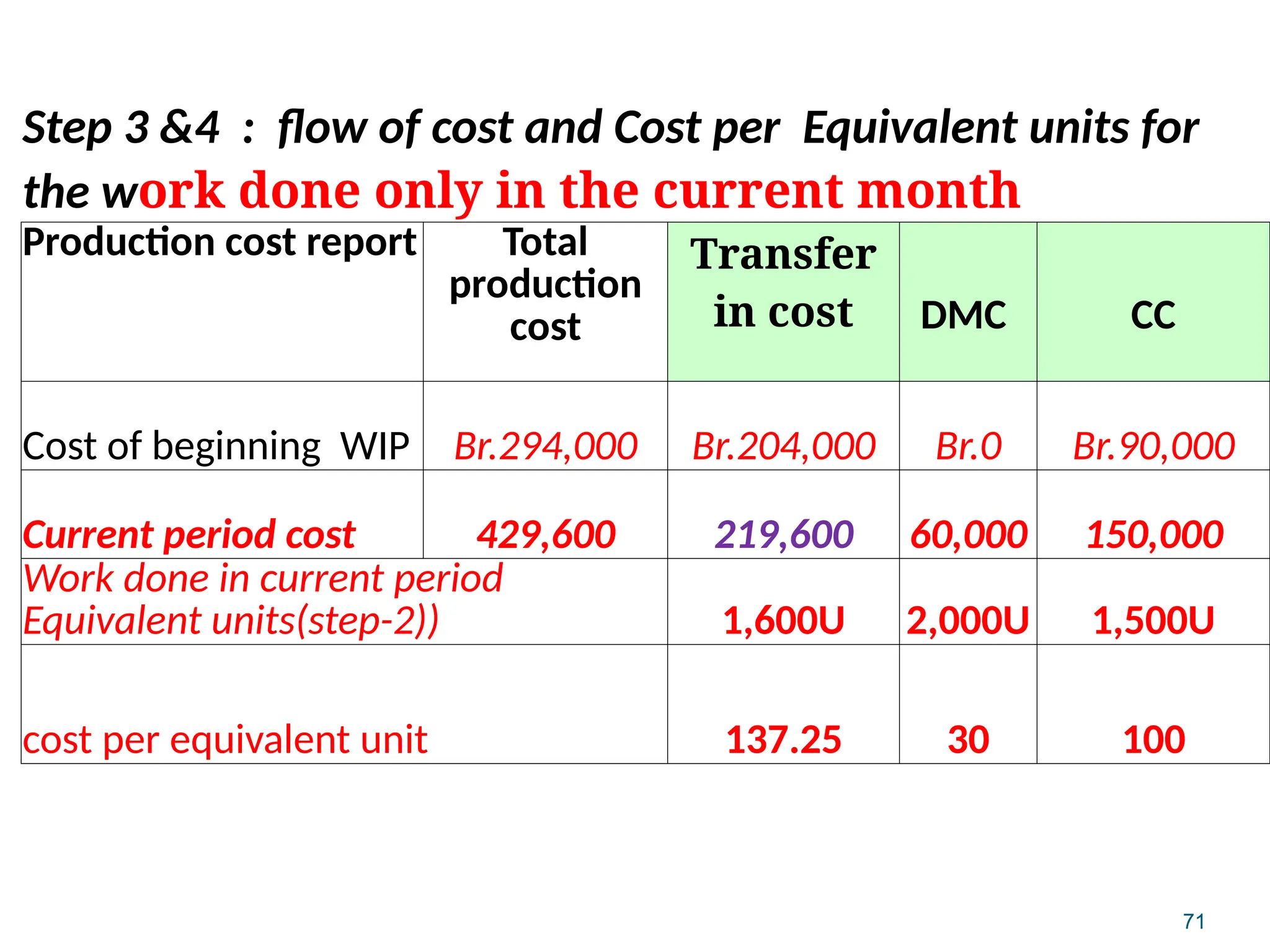

Step 3 &4: flow of cost and Cost per Equivalent units for

the work done only in the current month

Production cost report Total

production

cost

Transfer

in cost DMC CC

Cost of beginning WIP Br.294,000 Br.204,000 Br.0 Br.90,000

Current period cost 429,600 219,600 60,000 150,000

Work done in current period

Equivalent units(step-2)) 1,600U 2,000U 1,500U

cost per equivalent unit 137.25 30 100

66.

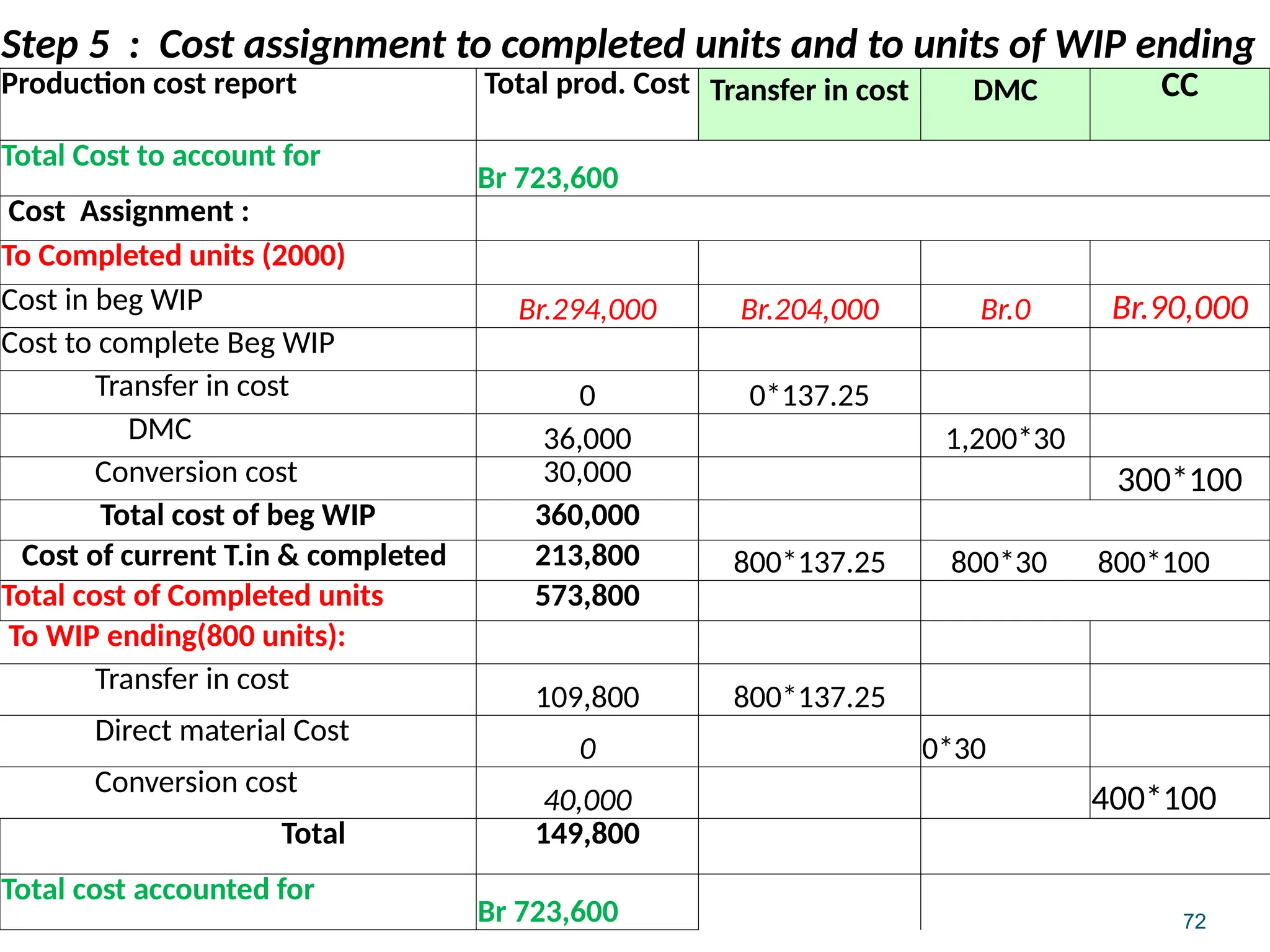

72

Step 5 :Cost assignment to completed units and to units of WIP ending

Production cost report Total prod. Cost Transfer in cost DMC CC

Total Cost to account for

Br 723,600

Cost Assignment :

To Completed units (2000)

Cost in beg WIP Br.294,000 Br.204,000 Br.0 Br.90,000

Cost to complete Beg WIP

Transfer in cost 0 0*137.25

DMC 36,000 1,200*30

Conversion cost 30,000 300*100

Total cost of beg WIP 360,000

Cost of current T.in & completed 213,800 800*137.25 800*30 800*100

Total cost of Completed units 573,800

To WIP ending(800 units):

Transfer in cost

109,800 800*137.25

Direct material Cost

0 0*30

Conversion cost

40,000 400*100

Total 149,800

Total cost accounted for

Br 723,600

67.

73

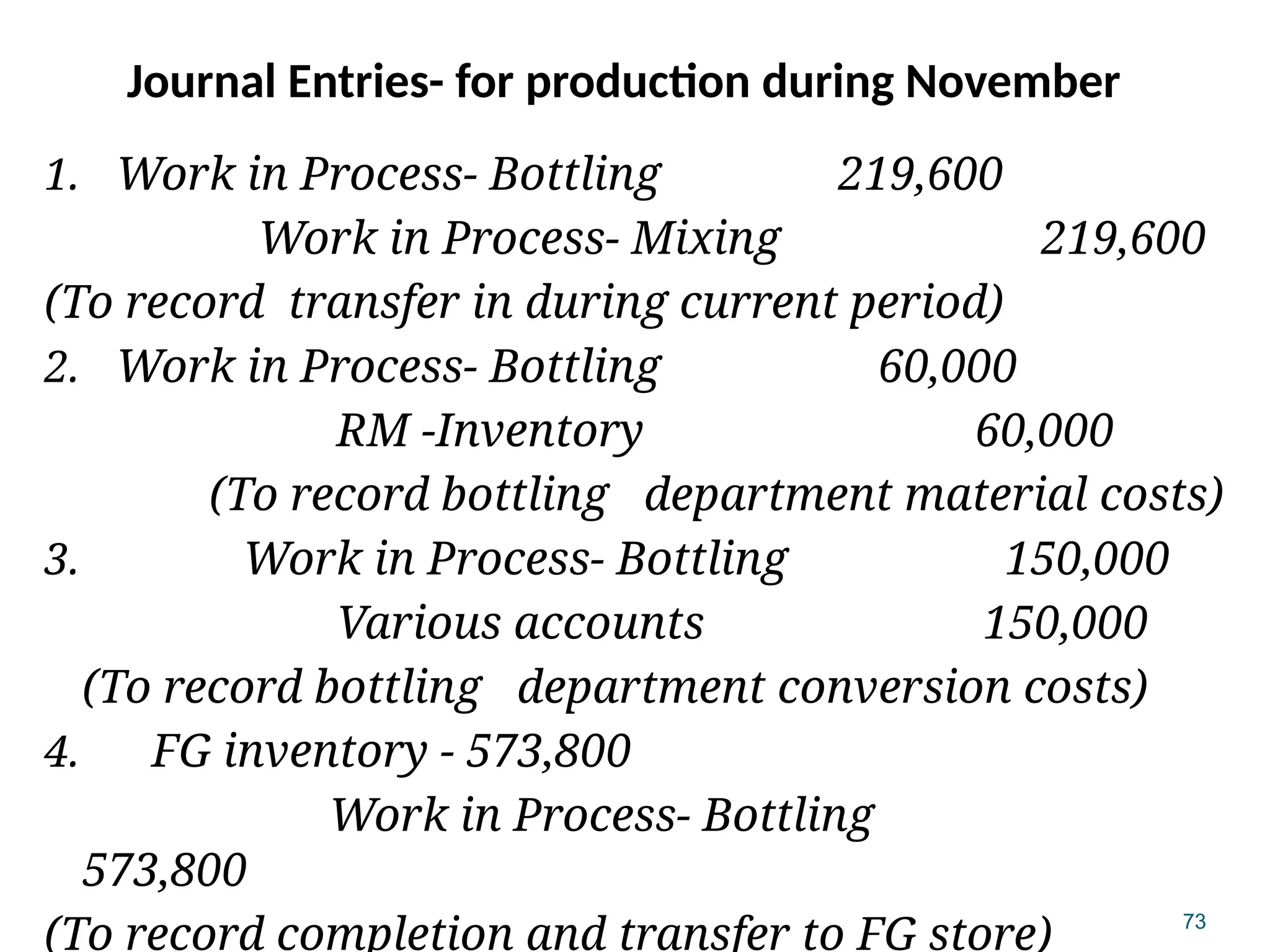

Journal Entries- forproduction during November

1. Work in Process- Bottling 219,600

Work in Process- Mixing 219,600

(To record transfer in during current period)

2. Work in Process- Bottling 60,000

RM -Inventory 60,000

(To record bottling department material costs)

3. Work in Process- Bottling 150,000

Various accounts 150,000

(To record bottling department conversion costs)

4. FG inventory - 573,800

Work in Process- Bottling

573,800

(To record completion and transfer to FG store)

#3 The difference between job order and process costing system is, thus, the extent of the averaging used to compute unit cost. In job order costing each job differs in terms of material used, labor incurred, and manufacturing overhead. Hence, it is impossible to assign the same cost for different jobs. On the contrary, identical units produced in mass took equal amount of direct material, direct labor, and manufacturing overhead. Thus, the unit cost can be found by dividing total cost by the number of units produced.

#5 Job-order and process costing are similar in that they both deal with assigning materials, labor and overhead to products as a way to calculate the unit product cost.

Both systems use raw materials inventory, work in process inventory, and finished goods inventory.

The flow of costs is similar, but not exactly the same, in the two systems.

#6 Process costing is best suited for the production of a single product that is continuously produced for a long period of time. Recall the mixing and bottling of Coca-Cola from Chapter Three. Job-order costing is best suited when jobs are produced as discrete projects. For example, building a house.

Process costing accumulates costs by department, while job-order costing accumulates costs by individual jobs.

Process costing uses a fundamental document called a department production report, while job-order costing uses the job cost sheet.

In process costing unit cost is computed by department, while in job-order systems unit cost is computed by job.

While there are similarities between the two systems, there are also significant differences.

#9 In all manufacturing systems, direct material, direct labor, and manufacturing overhead are charged to Work in Process Inventory. As we complete the production process, goods are transferred to the Finished Goods Inventory. Finally, when we sell the finished goods, we transfer the cost to cost of goods sold.

#10 In a job-order cost system costs are traced to individual jobs. All of the jobs in process make up the company’s Work in Process Inventory.

#11 In a process costing systems, costs are traced to departments that process the goods. In some companies there may be several processing departments that goods must pass through to become finished goods.

#12 Part I

Direct materials can be requisitioned for use in both Department A and Department B. These direct materials are likely to be different in nature.

#13 The journal entry that shows the requisition of direct materials for use in Processing Departments A and B, is to debit the processing department of the direct materials requisitioned and credit Raw Materials Inventory. Notice that the direct materials are placed into a separate work in process account for each processing department.

#14 Direct labor is transferred from the wages payable account into the work in process account of departments A and B depending upon where the individual employee worked.

#15 Manufacturing overhead is applied to each processing department based on a predetermined rate for each department. The predetermined rate does not have to be based on the same cost driver for each processing department.

#16 Here is the journal entry to place the direct labor into the work in process inventory of departments A and B.

#17 This is the journal entry we use to apply overhead to the work in process inventory of each of the processing departments.

#18 The cost of units complete as to processing in Department A are transferred into Department B for additional work.. Department B has incurred additional costs to work on units that were in process at the beginning of the period. The transferred-in costs from Department A are added to the manufacturing costs incurred in Department B.

#19 To transfer the costs, we debit the work in process inventory in Department B, and credit, or reduce, the work in process inventory in Department A.

#20 Here we see the transfer of completed goods our of Work in Process – Department B and into Finished Goods Inventory. The costs transferred represent the cost of good manufactured.

#21 The necessary journal entry is to debit finished goods inventory and credit work in process inventory in Department B to transfer finished production.

#22 Once we sell finished goods, we debit cost of goods sold and credit finished goods inventory.

#23 If we assume the company uses the perpetual inventory system, two entries are required to record a sale. The first entry is to record the sale and account receivable. The second entry is to transfer the finished goods sold to cost of goods sold.

Sales are recorded at selling price and cost of good sold is recorded at cost. The difference between the two is the gross margin on the sale.

#28 The basic idea behind equivalent units is quite easy to understand, but the computation of equivalent can become complex. Here we can say the two half-completed units of production are equal to one complete unit. Using this logic, we can say that 10,000 units that are 70% complete are equivalent, or the same as, 7,000 complete units.