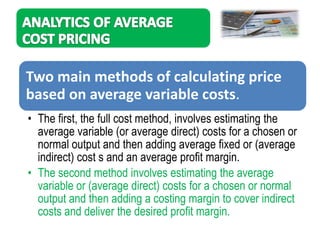

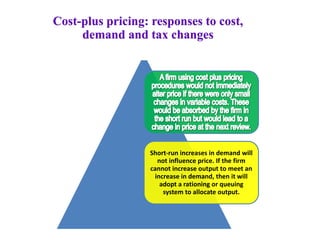

Download as PDF, PPTX

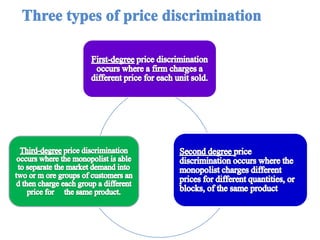

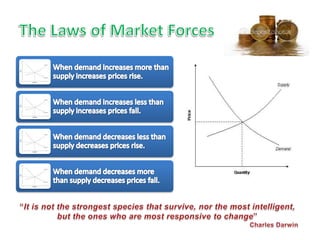

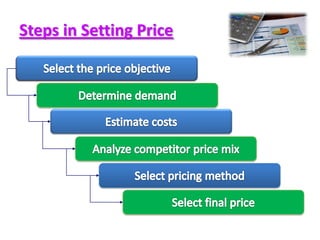

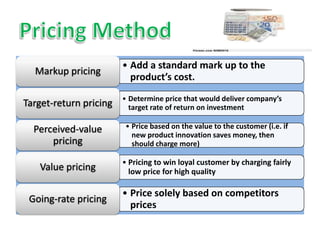

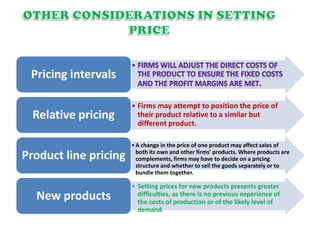

This document discusses various pricing strategies and considerations for setting prices. It defines what a price is and lists objectives a company may want to achieve through pricing, such as profitability, market share, or product positioning. The document also covers types of pricing like cost-based pricing, markup pricing, target-return pricing, and perceived-value pricing. Factors that influence pricing decisions are also examined, including customer demand, marketing mix, economic conditions, and customer perceived value.

![Human Resource Information System [HRIS] MBA defence](https://cdn.slidesharecdn.com/ss_thumbnails/hrisresearchppt21-131125023046-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)