Download to read offline

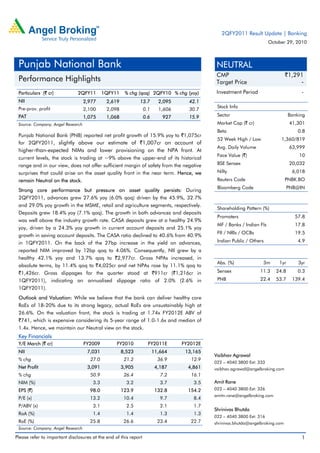

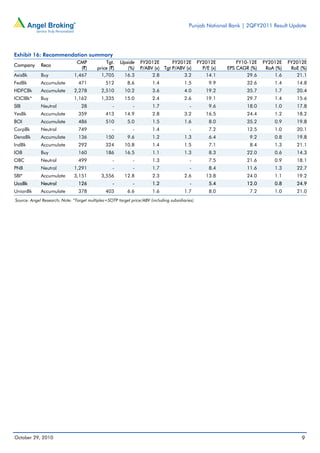

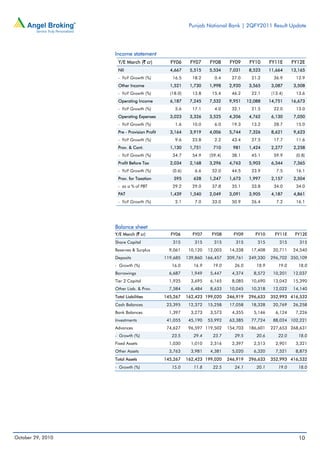

Punjab National Bank reported a 15.9% rise in net profit to Rs. 1,075 crore for the second quarter of FY2011, slightly above estimates. While core performance was strong with advances and deposits growing above industry levels, asset quality pressures persisted with gross NPAs rising 11.4% over the previous quarter. Going forward, net interest margins are expected to decline from current high levels as deposit rates are reviewed to fund credit growth. The stock currently trades at a premium to historical valuation ranges, limiting near-term upside.

![[JMFL] Repco Home Finance - Initiating Coverage 14 February 14](https://cdn.slidesharecdn.com/ss_thumbnails/285959be-4151-414b-9ce8-566368515d1b-160616063208-thumbnail.jpg?width=640&height=640&fit=bounds)