Downloaded 56 times

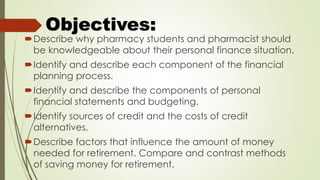

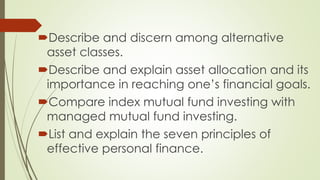

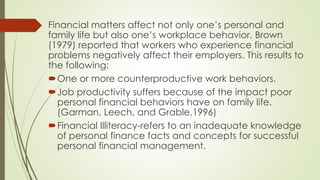

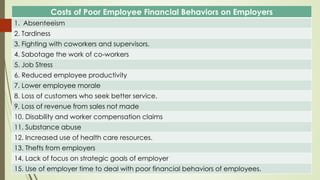

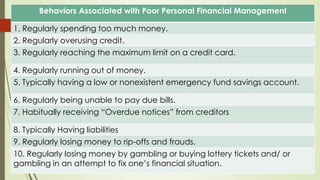

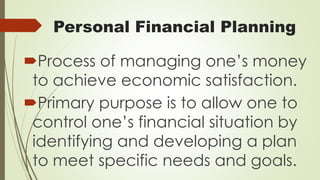

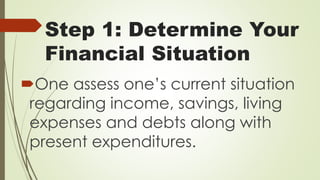

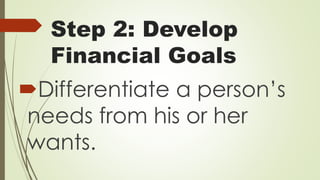

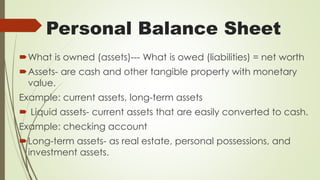

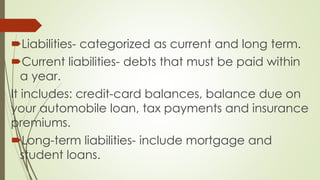

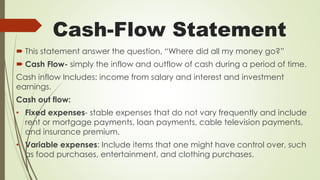

The document outlines objectives for teaching pharmacy students and pharmacists about personal finance. It discusses the importance of financial literacy for employees and the costs of poor financial behaviors for employers, such as absenteeism and reduced productivity. The summary also describes the key steps in personal financial planning, including determining one's financial situation, setting goals, evaluating alternatives, creating an action plan, and reevaluating. It defines personal balance sheets and cash flow statements as tools for financial planning.

![Chapter 1[1]](https://cdn.slidesharecdn.com/ss_thumbnails/chapter11-150306090427-conversion-gate01-thumbnail.jpg?width=640&height=640&fit=bounds)

![Chapter 2[1]](https://cdn.slidesharecdn.com/ss_thumbnails/chapter21-150306090428-conversion-gate01-thumbnail.jpg?width=640&height=640&fit=bounds)

![2 lab metabolic_changes_in_organic_medicinals[2]](https://cdn.slidesharecdn.com/ss_thumbnails/2labmetabolicchangesinorganicmedicinals2-150306090407-conversion-gate01-thumbnail.jpg?width=640&height=640&fit=bounds)

![Bio sci 8_lec_001[2]](https://cdn.slidesharecdn.com/ss_thumbnails/biosci8lec0012-150306090424-conversion-gate01-thumbnail.jpg?width=640&height=640&fit=bounds)

![1 lab physico-chemical_properties_of_drugs[1]](https://cdn.slidesharecdn.com/ss_thumbnails/1labphysico-chemicalpropertiesofdrugs1-150306090358-conversion-gate01-thumbnail.jpg?width=640&height=640&fit=bounds)

![3 lec metabolic_changes_in_drugs[1]](https://cdn.slidesharecdn.com/ss_thumbnails/3lecmetabolicchangesindrugs1-150306090419-conversion-gate01-thumbnail.jpg?width=640&height=640&fit=bounds)