Downloaded 33 times

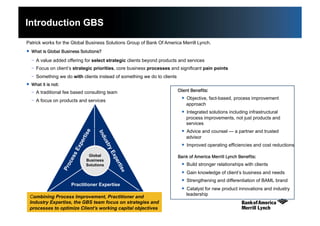

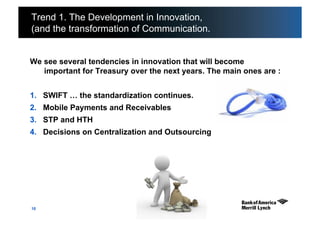

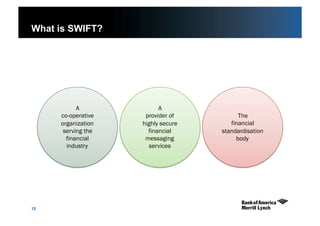

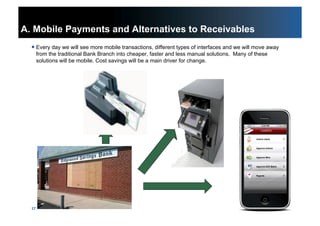

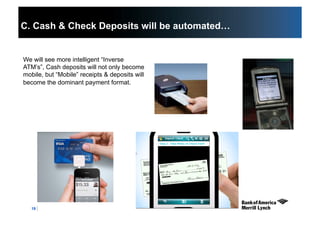

Patrick Peters-Buhler, Director of GBS at Bank of America Merrill Lynch, gave a presentation on the future of cash management over the next five years. He discussed two main trends - developments in innovation including increased use of mobile payments, straight-through processing, and decisions around centralization and outsourcing. The second trend is developments in regulation such as SEPA standardization, digital invoicing, and increased IRS oversight of cash management. Peters-Buhler said treasurers should not be intimidated by the uncharted landscape and that opportunities exist within regulations to drive efficiency and add value.