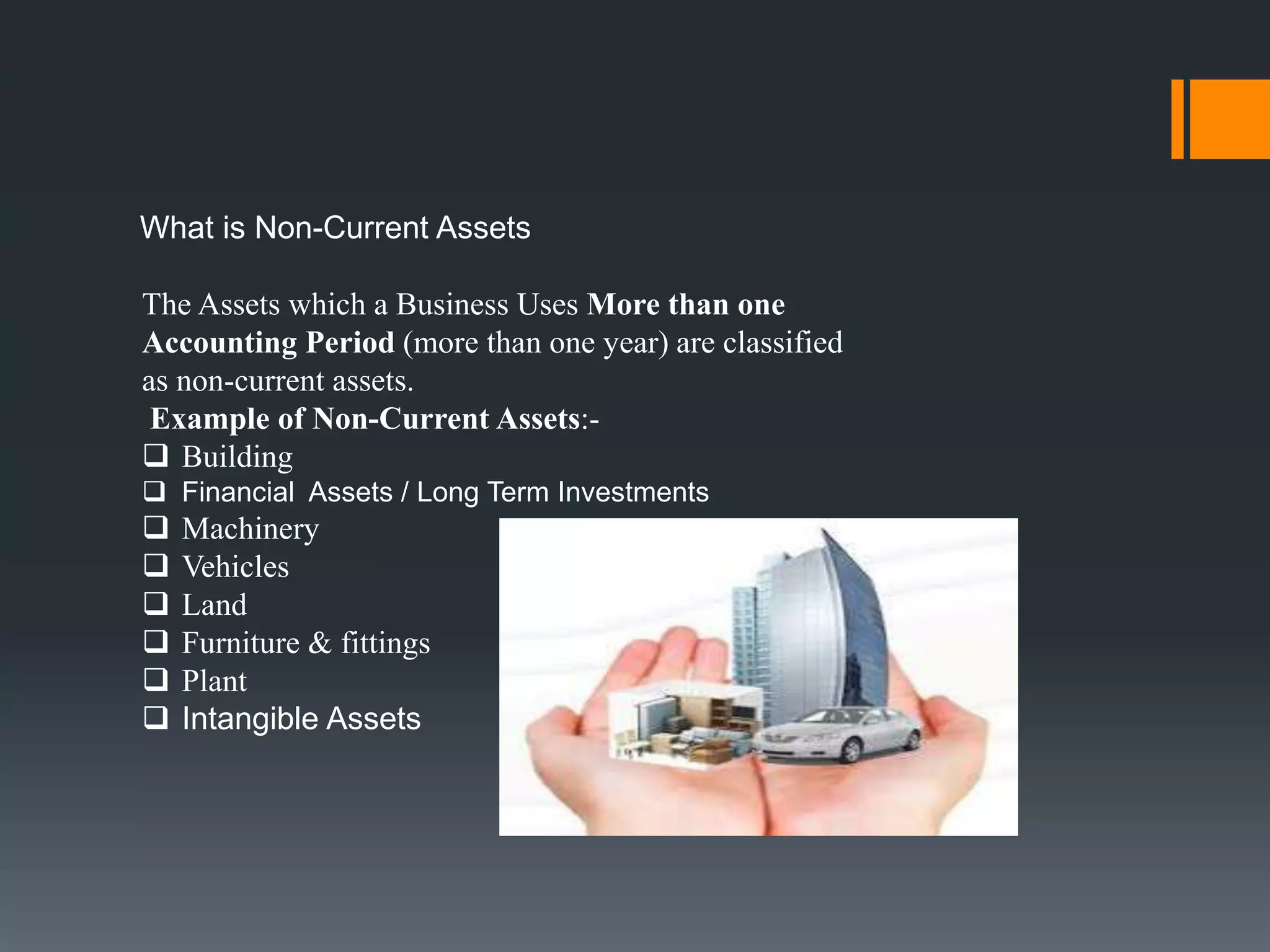

This document discusses non-current assets and depreciation in financial accounting. It defines non-current assets as assets used by a business for more than one accounting period, providing examples like buildings, machinery, and land. It then defines depreciation as the allocation of an asset's original cost over its useful life, reducing its value each year on the balance sheet. Finally, it outlines common methods for calculating depreciation charges, such as the straight-line method and reducing balance method.