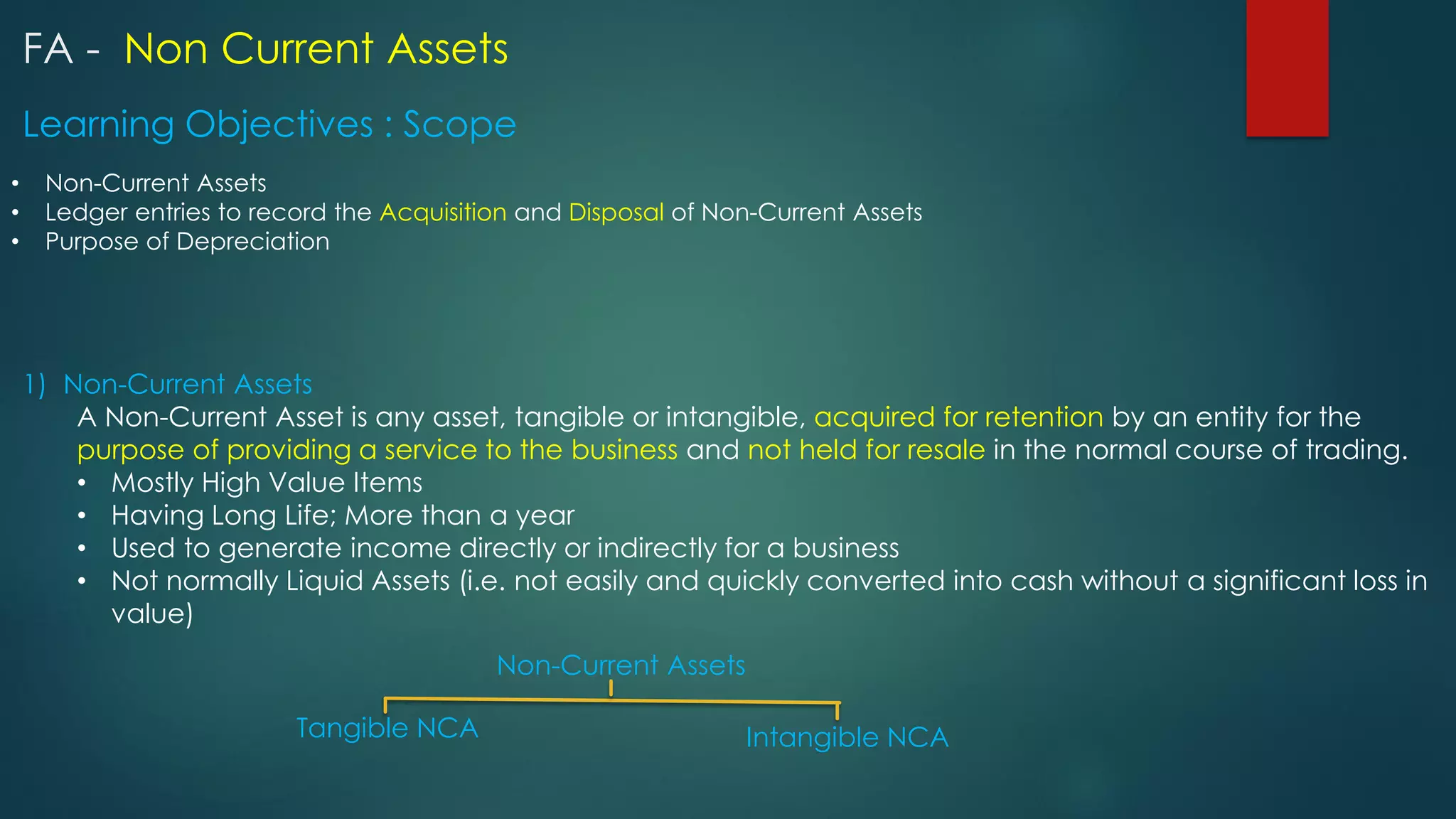

FA - NonCurrent Assets

• Non-Current Assets

• Ledger entries to record the Acquisition and Disposal of Non-Current Assets

• Purpose of Depreciation

Learning Objectives : Scope

1) Non-Current Assets

A Non-Current Asset is any asset, tangible or intangible, acquired for retention by an entity for the

purpose of providing a service to the business and not held for resale in the normal course of trading.

• Mostly High Value Items

• Having Long Life; More than a year

• Used to generate income directly or indirectly for a business

• Not normally Liquid Assets (i.e. not easily and quickly converted into cash without a significant loss in

value)

Non-Current Assets

Intangible NCA

Tangible NCA

2.

Plant & Machineries

MotorVehicles

Computer Equipment

Tangible Non Current Assets

Furnitures & Fixtures

Office Factory Sales Centre Coal Mines Quarries Oil Well

These all assets used in business to

carry on business activity and

generate economic benefits – Used up

cost should be matched with

Economic Benefits

Land & Buildings - Premises

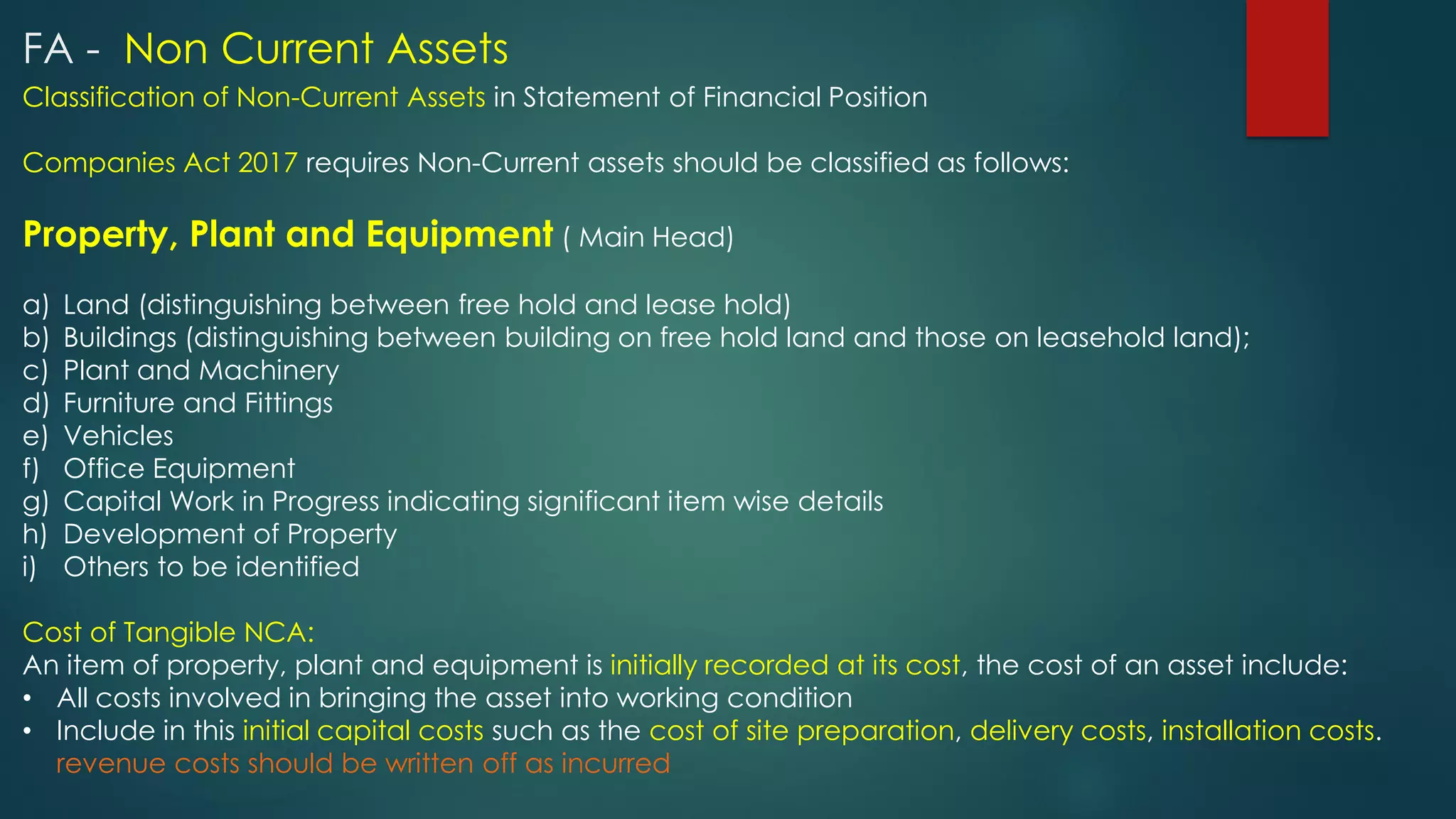

FA - Non Current Assets

3.

Classification of Non-CurrentAssets in Statement of Financial Position

Companies Act 2017 requires Non-Current assets should be classified as follows:

Property, Plant and Equipment ( Main Head)

a) Land (distinguishing between free hold and lease hold)

b) Buildings (distinguishing between building on free hold land and those on leasehold land);

c) Plant and Machinery

d) Furniture and Fittings

e) Vehicles

f) Office Equipment

g) Capital Work in Progress indicating significant item wise details

h) Development of Property

i) Others to be identified

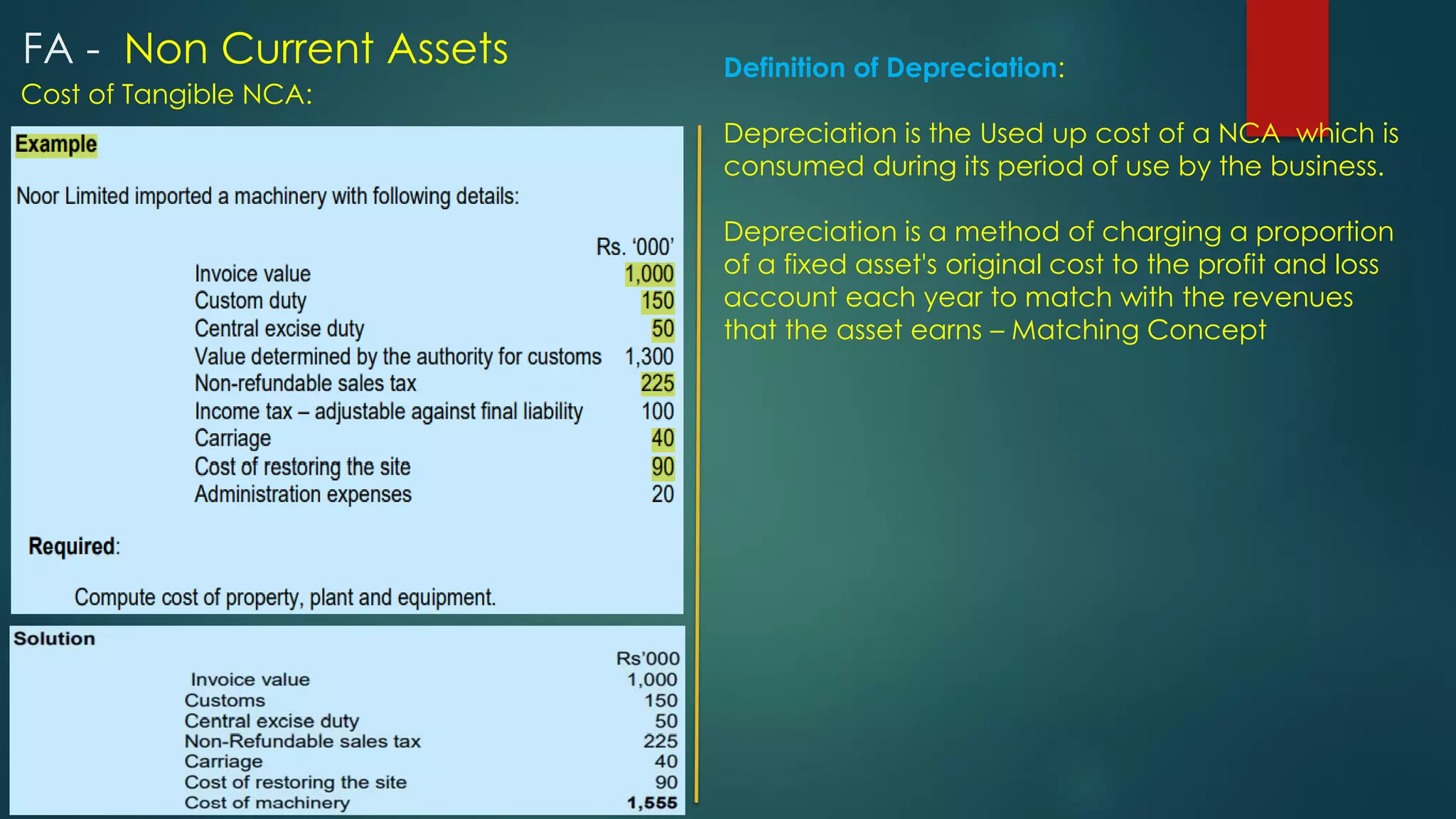

Cost of Tangible NCA:

An item of property, plant and equipment is initially recorded at its cost, the cost of an asset include:

• All costs involved in bringing the asset into working condition

• Include in this initial capital costs such as the cost of site preparation, delivery costs, installation costs.

revenue costs should be written off as incurred

FA - Non Current Assets

4.

Cost of TangibleNCA:

Definition of Depreciation:

Depreciation is the Used up cost of a NCA which is

consumed during its period of use by the business.

Depreciation is a method of charging a proportion

of a fixed asset's original cost to the profit and loss

account each year to match with the revenues

that the asset earns – Matching Concept

FA - Non Current Assets

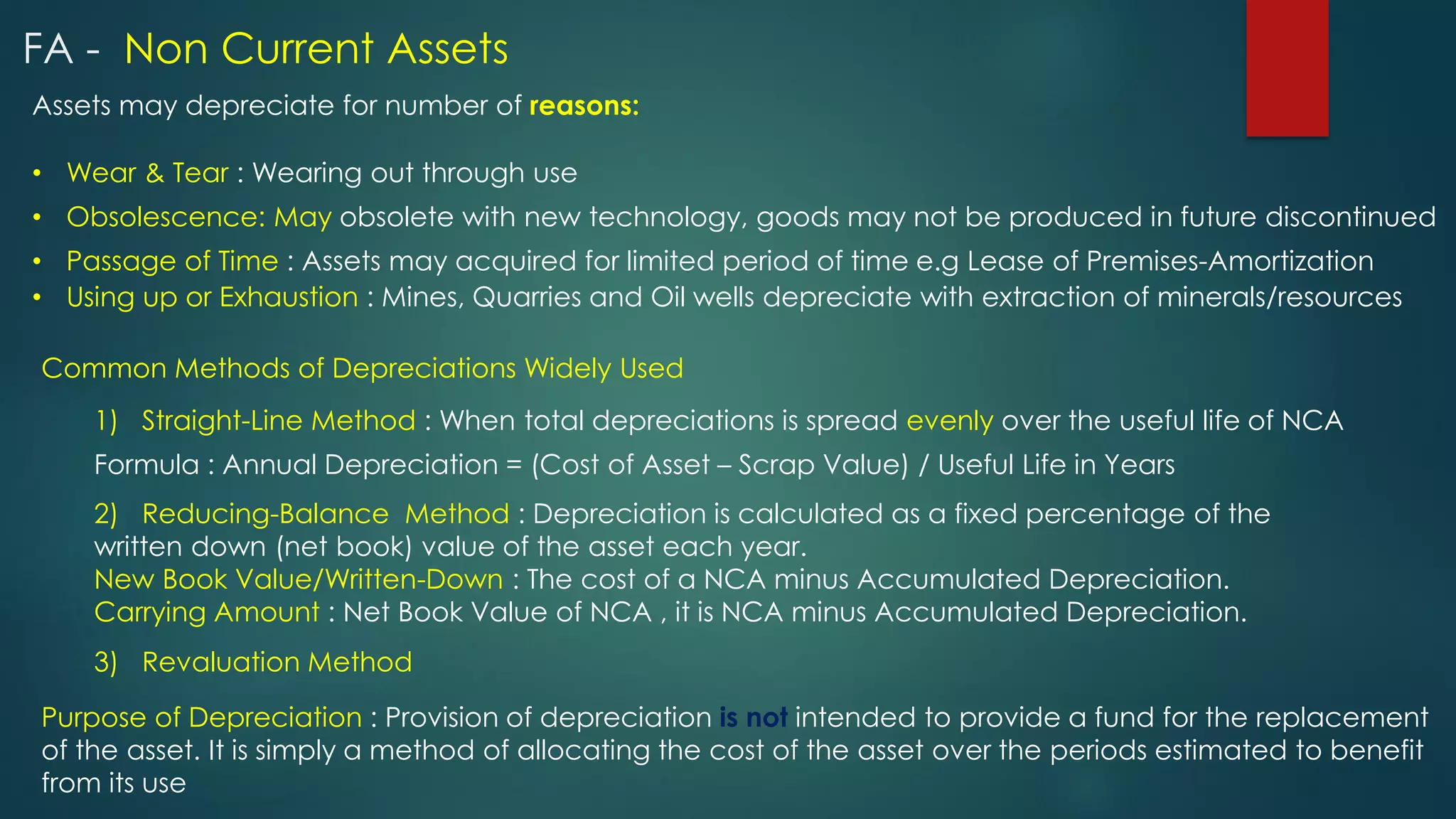

5.

Assets may depreciatefor number of reasons:

• Wear & Tear : Wearing out through use

Common Methods of Depreciations Widely Used

1) Straight-Line Method : When total depreciations is spread evenly over the useful life of NCA

• Obsolescence: May obsolete with new technology, goods may not be produced in future discontinued

• Passage of Time : Assets may acquired for limited period of time e.g Lease of Premises-Amortization

• Using up or Exhaustion : Mines, Quarries and Oil wells depreciate with extraction of minerals/resources

2) Reducing-Balance Method : Depreciation is calculated as a fixed percentage of the

written down (net book) value of the asset each year.

New Book Value/Written-Down : The cost of a NCA minus Accumulated Depreciation.

Carrying Amount : Net Book Value of NCA , it is NCA minus Accumulated Depreciation.

Formula : Annual Depreciation = (Cost of Asset – Scrap Value) / Useful Life in Years

Purpose of Depreciation : Provision of depreciation is not intended to provide a fund for the replacement

of the asset. It is simply a method of allocating the cost of the asset over the periods estimated to benefit

from its use

3) Revaluation Method

FA - Non Current Assets

6.

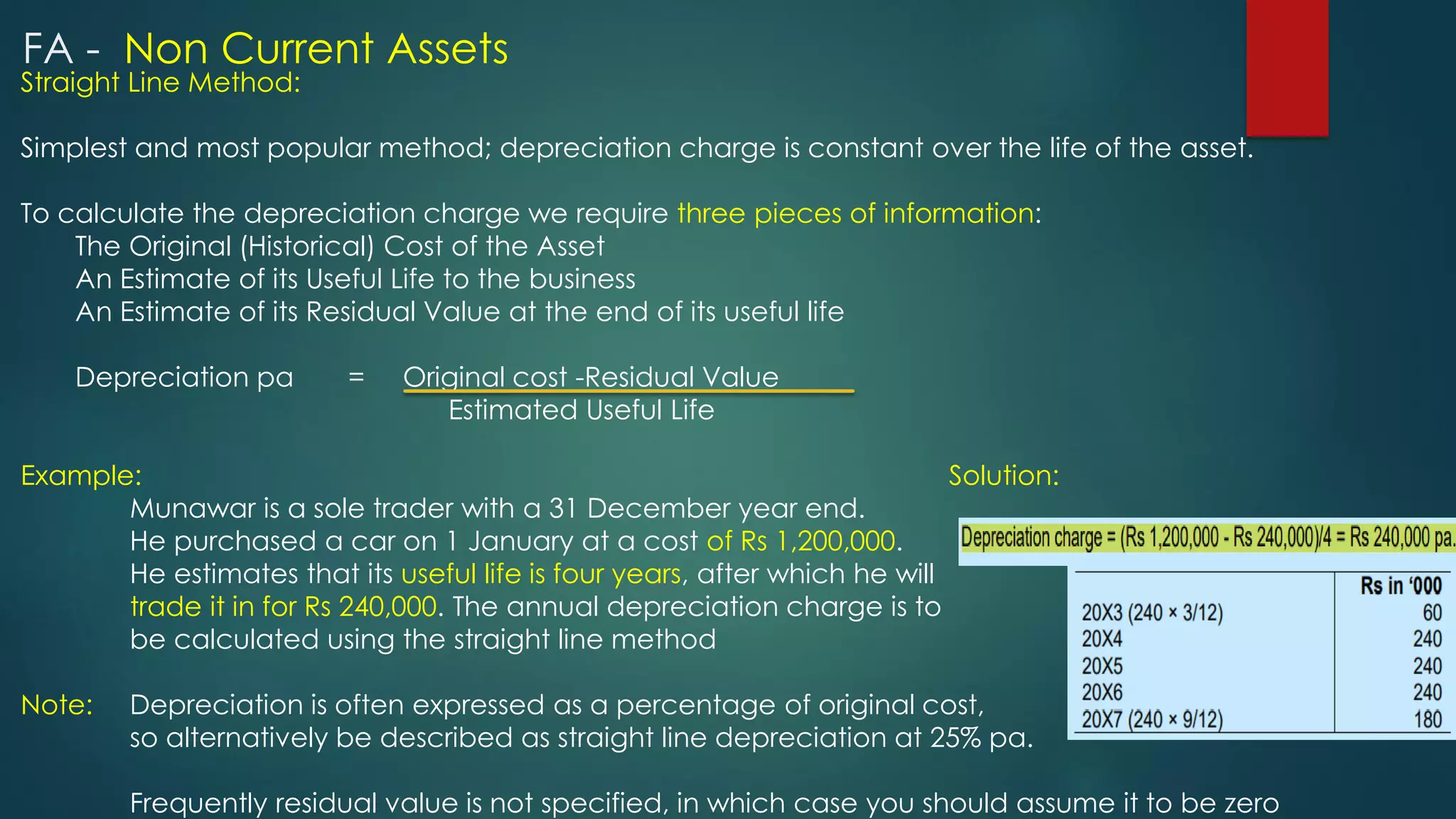

Straight Line Method:

Simplestand most popular method; depreciation charge is constant over the life of the asset.

To calculate the depreciation charge we require three pieces of information:

The Original (Historical) Cost of the Asset

An Estimate of its Useful Life to the business

An Estimate of its Residual Value at the end of its useful life

Depreciation pa = Original cost -Residual Value

Estimated Useful Life

Example: Solution:

Munawar is a sole trader with a 31 December year end.

He purchased a car on 1 January at a cost of Rs 1,200,000.

He estimates that its useful life is four years, after which he will

trade it in for Rs 240,000. The annual depreciation charge is to

be calculated using the straight line method

Note: Depreciation is often expressed as a percentage of original cost,

so alternatively be described as straight line depreciation at 25% pa.

Frequently residual value is not specified, in which case you should assume it to be zero

FA - Non Current Assets

7.

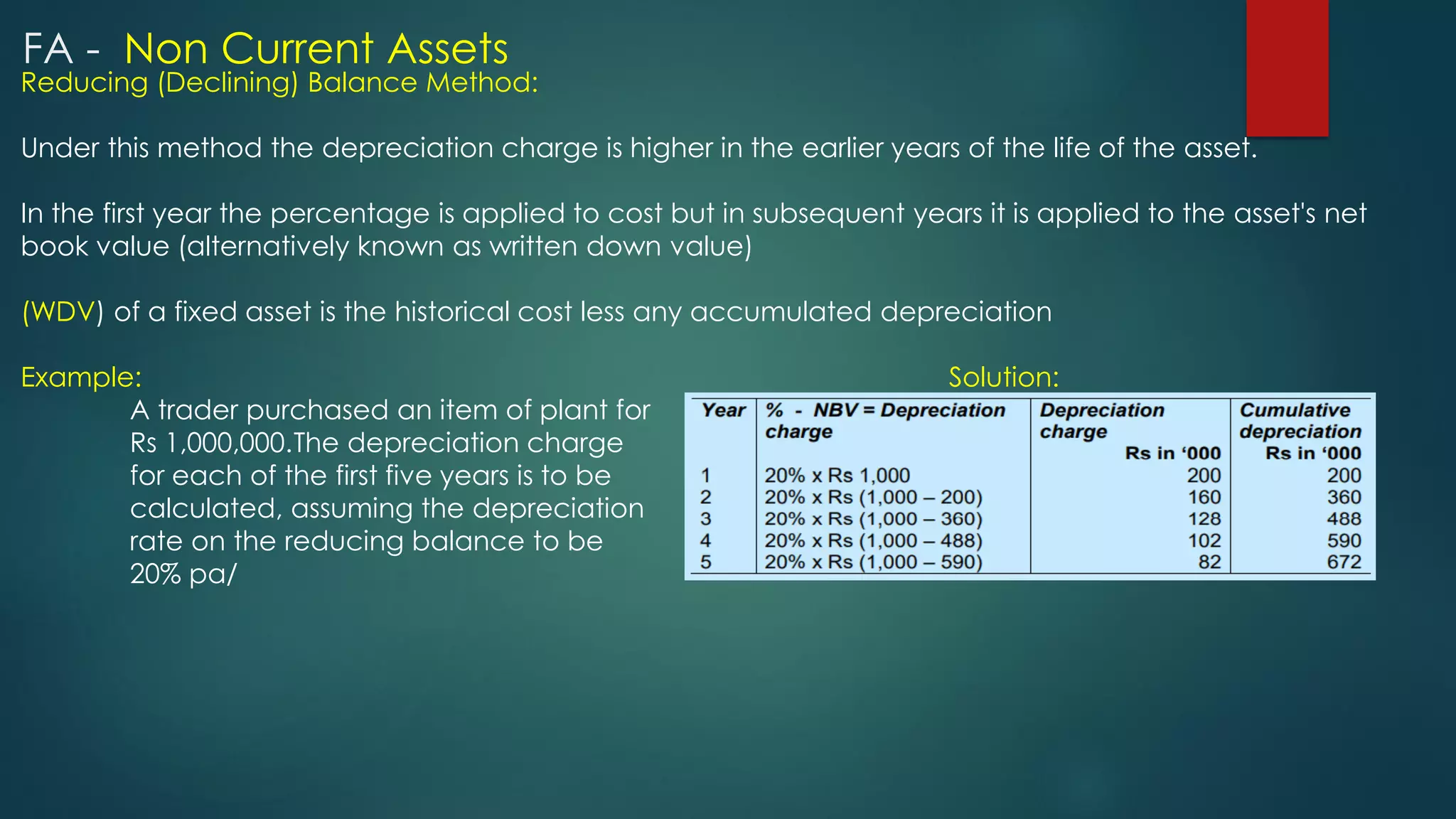

Reducing (Declining) BalanceMethod:

Under this method the depreciation charge is higher in the earlier years of the life of the asset.

In the first year the percentage is applied to cost but in subsequent years it is applied to the asset's net

book value (alternatively known as written down value)

(WDV) of a fixed asset is the historical cost less any accumulated depreciation

Example: Solution:

A trader purchased an item of plant for

Rs 1,000,000.The depreciation charge

for each of the first five years is to be

calculated, assuming the depreciation

rate on the reducing balance to be

20% pa/

FA - Non Current Assets

8.

Straight-Line Method :When total depreciations is spread evenly over the useful life of NCA

Walkthrough : Machine Cost US$ 20,000, Useful Life 5 Years, Scrap Value US$ 5000

Formula : Annual Depreciation = (Cost of Asset – Scrap Value) / Useful Life in Years

Annual Depreciation = (20,000 – 5000) / 5 = US$ 3000 per annum

Machine Account (At Cost)

Year 1

Provision for Depreciation Machinery A/C

Bank 20,000

=====

Year 2

Balance c/d

Year 1 20,000

=====

Balance b/d

20,000

20,000 20,000

20,000

=====

=====

=====

Year 2 Balance c/d

Income Statement

Balance c/d

Balance c/d

Year 3 Year 3

Year 4

Year 4

Balance b/d

Balance b/d

Balance b/d

Balance b/d

=====

=====

=====

=====

20,000 20,000

20,000

Year 5 Year 5

=====

20,000

Balance b/d

Balance b/d

Balance b/d

Balance b/d

Balance c/d

Balance c/d

Balance c/d

Balance c/d

Year 1

Year 1 3,000

9,000

12,000

12,000

15,000

3,000

=====

=====

=====

=====

--------

=====

---------

Year 2

Year 2 3,000

Income Statement

Income Statement

Income Statement

Income Statement

3,000

3,000

6,000

3,000

3,000

6,000

6,000

Year 3

Year 3

6,000

--------

--------

-------- --------

-------- --------

=====

=====

=====

=====

=====

9,000

9,000

Year 4

Year 4

9,000

12,000

Balance c/d

15,000 15,000

Year 5

Year 5 12,000

Depreciation Expense Debit US$ 3,000

Provision for Depreciation Machinery A/C Credit US$ 3,000

FA - Non Current Assets

9.

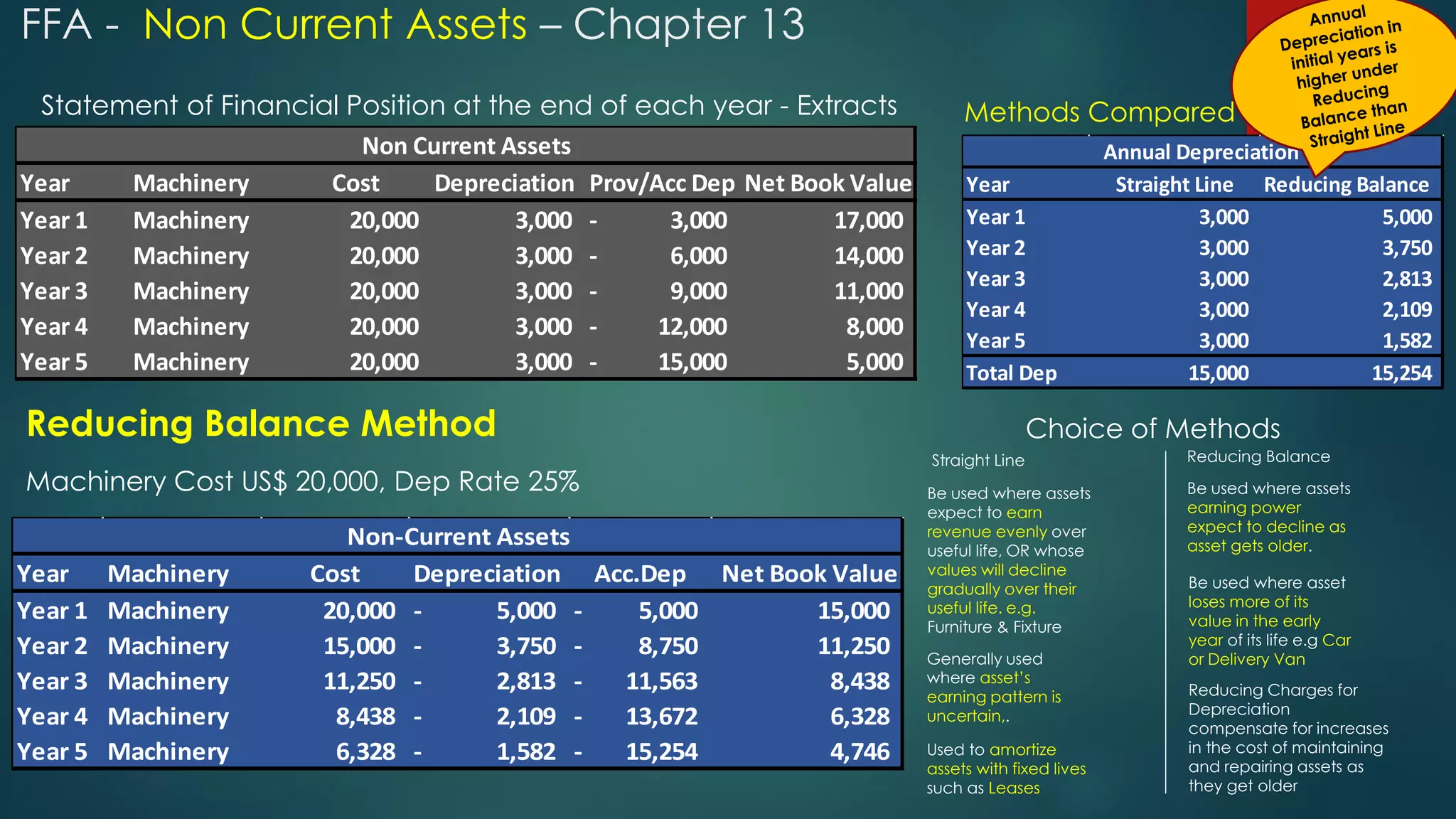

Statement of FinancialPosition at the end of each year - Extracts

Reducing Balance Method

Methods Compared

Choice of Methods

Year Straight Line Reducing Balance

Year 1 3,000 5,000

Year 2 3,000 3,750

Year 3 3,000 2,813

Year 4 3,000 2,109

Year 5 3,000 1,582

Total Dep 15,000 15,254

Annual Depreciation

Be used where assets

expect to earn

revenue evenly over

useful life, OR whose

values will decline

gradually over their

useful life. e.g.

Furniture & Fixture

Reducing Balance

Straight Line

Generally used

where asset’s

earning pattern is

uncertain,.

Used to amortize

assets with fixed lives

such as Leases

Be used where assets

earning power

expect to decline as

asset gets older.

Be used where asset

loses more of its

value in the early

year of its life e.g Car

or Delivery Van

Reducing Charges for

Depreciation

compensate for increases

in the cost of maintaining

and repairing assets as

they get older

Year Machinery Cost Depreciation Acc.Dep Net Book Value

Year 1 Machinery 20,000 5,000

- 5,000

- 15,000

Year 2 Machinery 15,000 3,750

- 8,750

- 11,250

Year 3 Machinery 11,250 2,813

- 11,563

- 8,438

Year 4 Machinery 8,438 2,109

- 13,672

- 6,328

Year 5 Machinery 6,328 1,582

- 15,254

- 4,746

Non-Current Assets

Machinery Cost US$ 20,000, Dep Rate 25%

Year Machinery Cost Depreciation Prov/Acc Dep Net Book Value

Year 1 Machinery 20,000 3,000 3,000

- 17,000

Year 2 Machinery 20,000 3,000 6,000

- 14,000

Year 3 Machinery 20,000 3,000 9,000

- 11,000

Year 4 Machinery 20,000 3,000 12,000

- 8,000

Year 5 Machinery 20,000 3,000 15,000

- 5,000

Non Current Assets

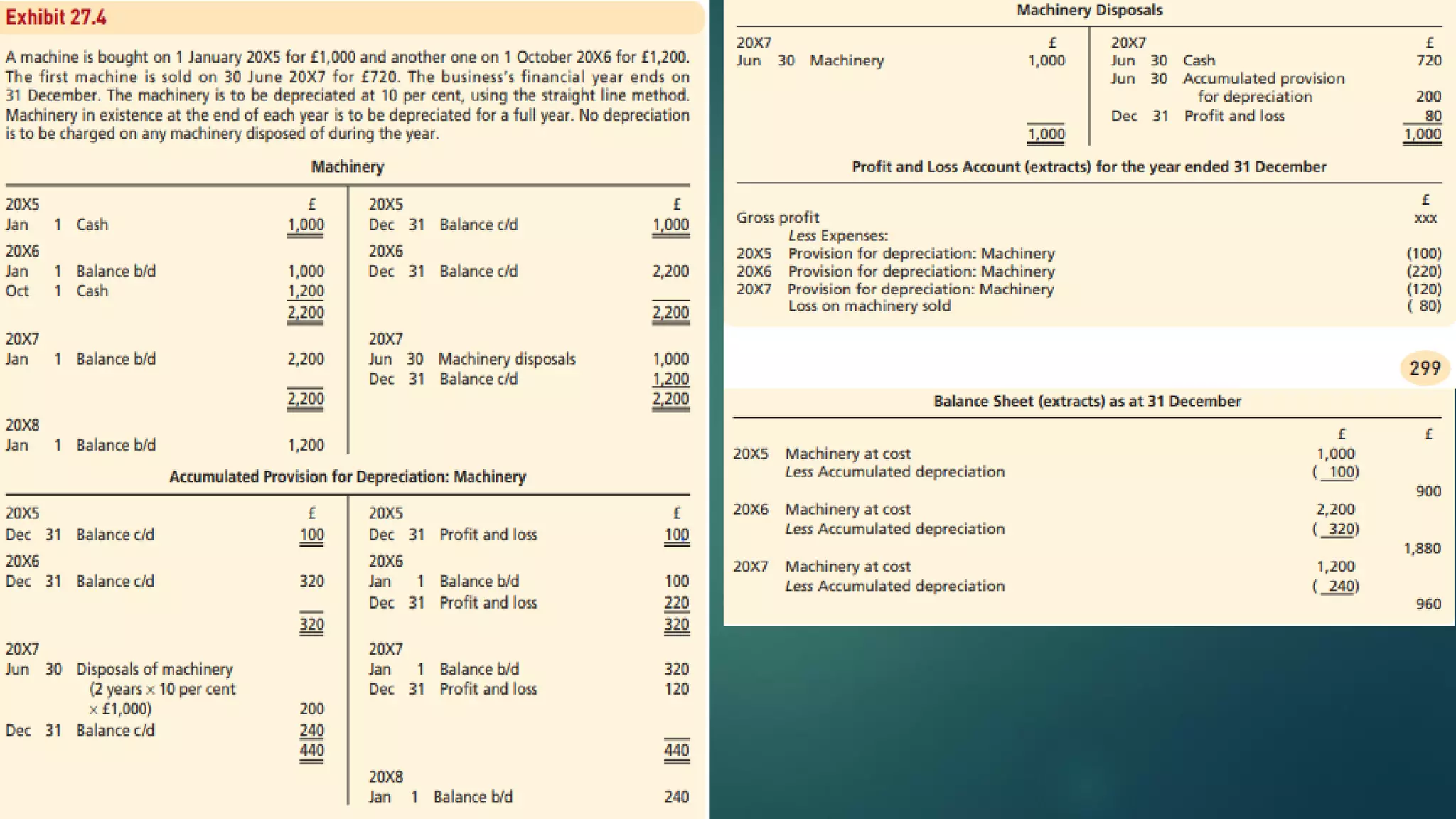

FFA - Non Current Assets – Chapter 13

10.

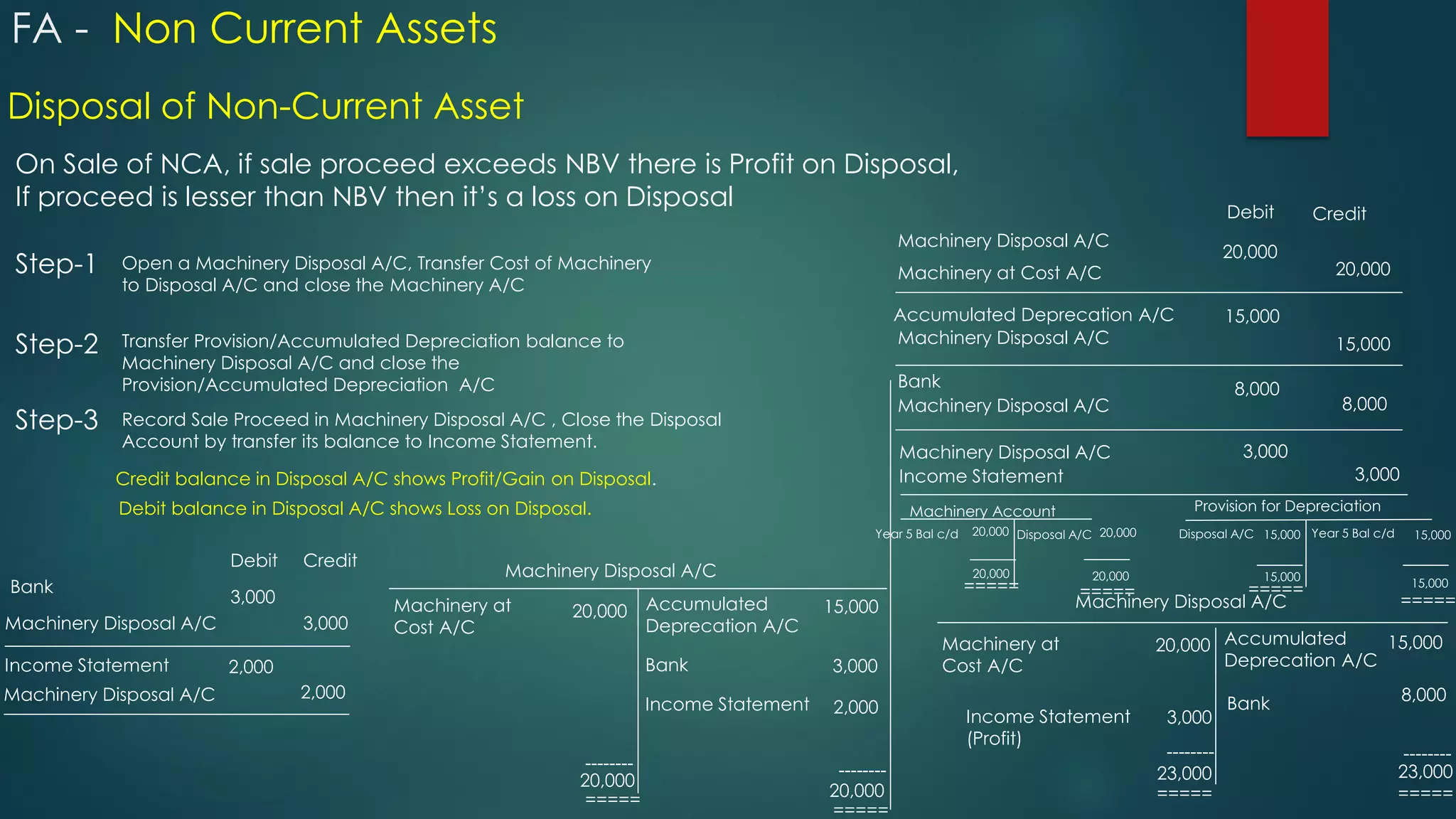

Disposal of Non-CurrentAsset

Step-1 Machinery at Cost A/C

Open a Machinery Disposal A/C, Transfer Cost of Machinery

to Disposal A/C and close the Machinery A/C

Debit Credit

20,000

On Sale of NCA, if sale proceed exceeds NBV there is Profit on Disposal,

If proceed is lesser than NBV then it’s a loss on Disposal

Machinery Disposal A/C

20,000

Step-2

Step-3

Transfer Provision/Accumulated Depreciation balance to

Machinery Disposal A/C and close the

Provision/Accumulated Depreciation A/C

Record Sale Proceed in Machinery Disposal A/C , Close the Disposal

Account by transfer its balance to Income Statement.

Credit balance in Disposal A/C shows Profit/Gain on Disposal.

Debit balance in Disposal A/C shows Loss on Disposal.

Machinery Disposal A/C

Accumulated Deprecation A/C

15,000

15,000

Machinery Disposal A/C

Bank

3,000

3,000

8,000

8,000

Machinery Disposal A/C

20,000

Machinery at

Cost A/C

Accumulated

Deprecation A/C

15,000

Bank 8,000

Income Statement

-------- --------

3,000

Income Statement

(Profit)

Machinery Disposal A/C

23,000

23,000

=====

=====

Debit Credit

Bank

Machinery Disposal A/C 3,000

3,000

Income Statement

Machinery Disposal A/C 2,000

2,000

Machinery Disposal A/C

Machinery at

Cost A/C

20,000 Accumulated

Deprecation A/C

15,000

Bank

Income Statement

3,000

2,000

--------

--------

=====

===== 20,000

20,000

Provision for Depreciation

Machinery Account

=====

=====

=====

=====

20,000 20,000

20,000

20,000

Year 5 Bal c/d Disposal A/C Year 5 Bal c/d 15,000

15,000

15,000

15,000

Disposal A/C

FA - Non Current Assets

11.

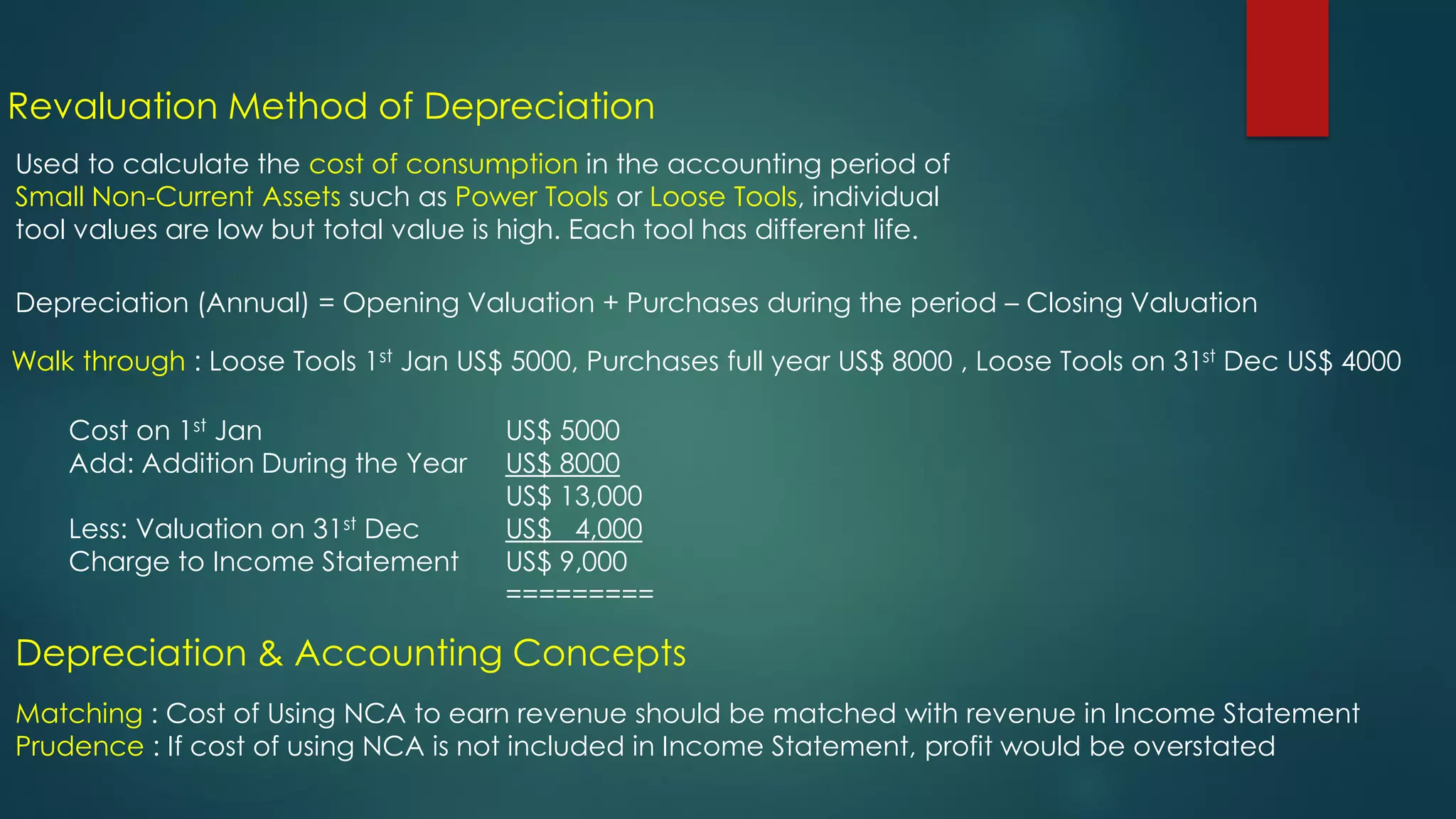

Revaluation Method ofDepreciation

Used to calculate the cost of consumption in the accounting period of

Small Non-Current Assets such as Power Tools or Loose Tools, individual

tool values are low but total value is high. Each tool has different life.

Depreciation (Annual) = Opening Valuation + Purchases during the period – Closing Valuation

Walk through : Loose Tools 1st Jan US$ 5000, Purchases full year US$ 8000 , Loose Tools on 31st Dec US$ 4000

Cost on 1st Jan US$ 5000

Add: Addition During the Year US$ 8000

US$ 13,000

Less: Valuation on 31st Dec US$ 4,000

Charge to Income Statement US$ 9,000

=========

Depreciation & Accounting Concepts

Matching : Cost of Using NCA to earn revenue should be matched with revenue in Income Statement

Prudence : If cost of using NCA is not included in Income Statement, profit would be overstated

12.

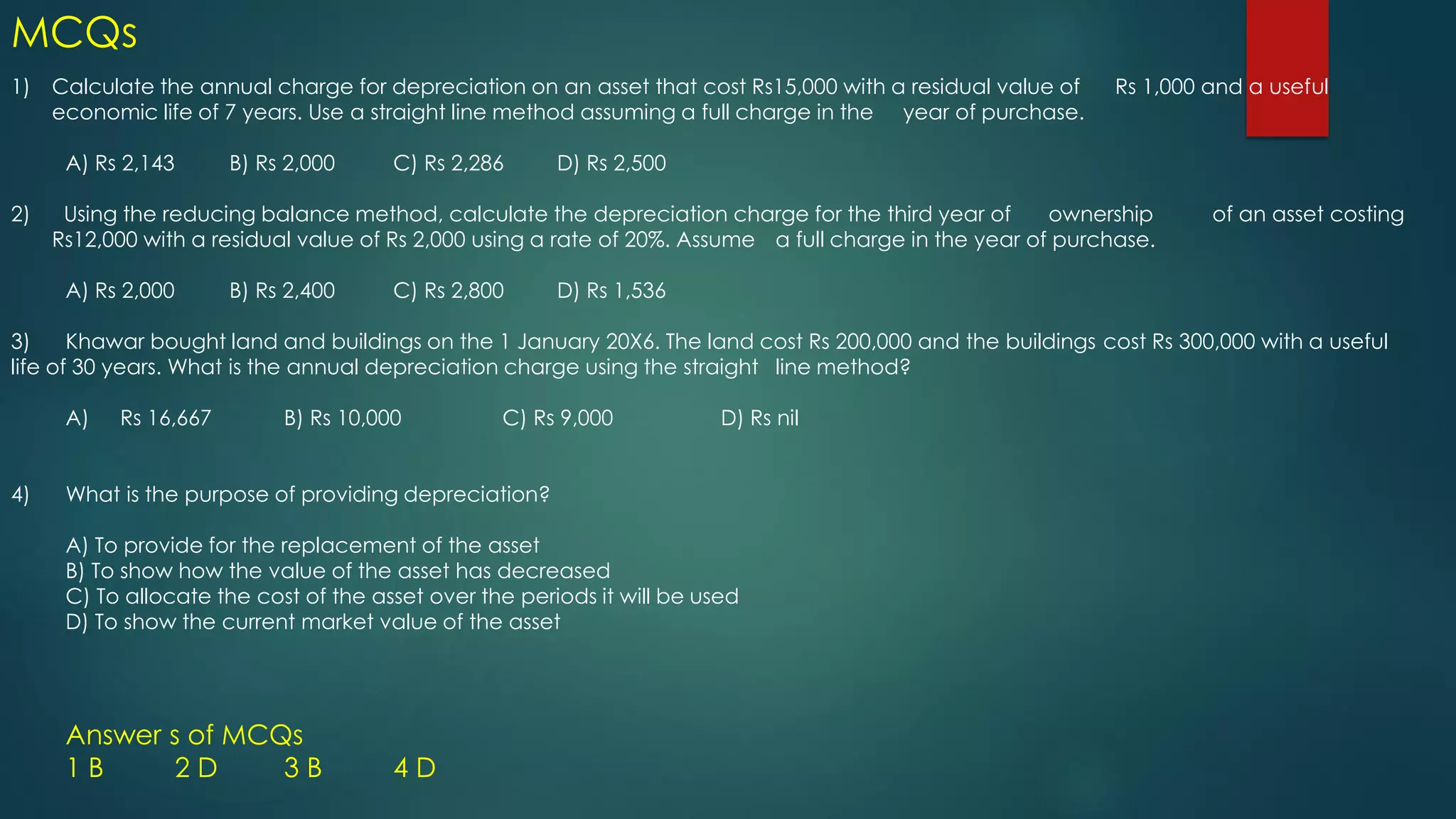

1) Calculate theannual charge for depreciation on an asset that cost Rs15,000 with a residual value of Rs 1,000 and a useful

economic life of 7 years. Use a straight line method assuming a full charge in the year of purchase.

A) Rs 2,143 B) Rs 2,000 C) Rs 2,286 D) Rs 2,500

2) Using the reducing balance method, calculate the depreciation charge for the third year of ownership of an asset costing

Rs12,000 with a residual value of Rs 2,000 using a rate of 20%. Assume a full charge in the year of purchase.

A) Rs 2,000 B) Rs 2,400 C) Rs 2,800 D) Rs 1,536

3) Khawar bought land and buildings on the 1 January 20X6. The land cost Rs 200,000 and the buildings cost Rs 300,000 with a useful

life of 30 years. What is the annual depreciation charge using the straight line method?

A) Rs 16,667 B) Rs 10,000 C) Rs 9,000 D) Rs nil

4) What is the purpose of providing depreciation?

A) To provide for the replacement of the asset

B) To show how the value of the asset has decreased

C) To allocate the cost of the asset over the periods it will be used

D) To show the current market value of the asset

Answer s of MCQs

1 B 2 D 3 B 4 D

MCQs

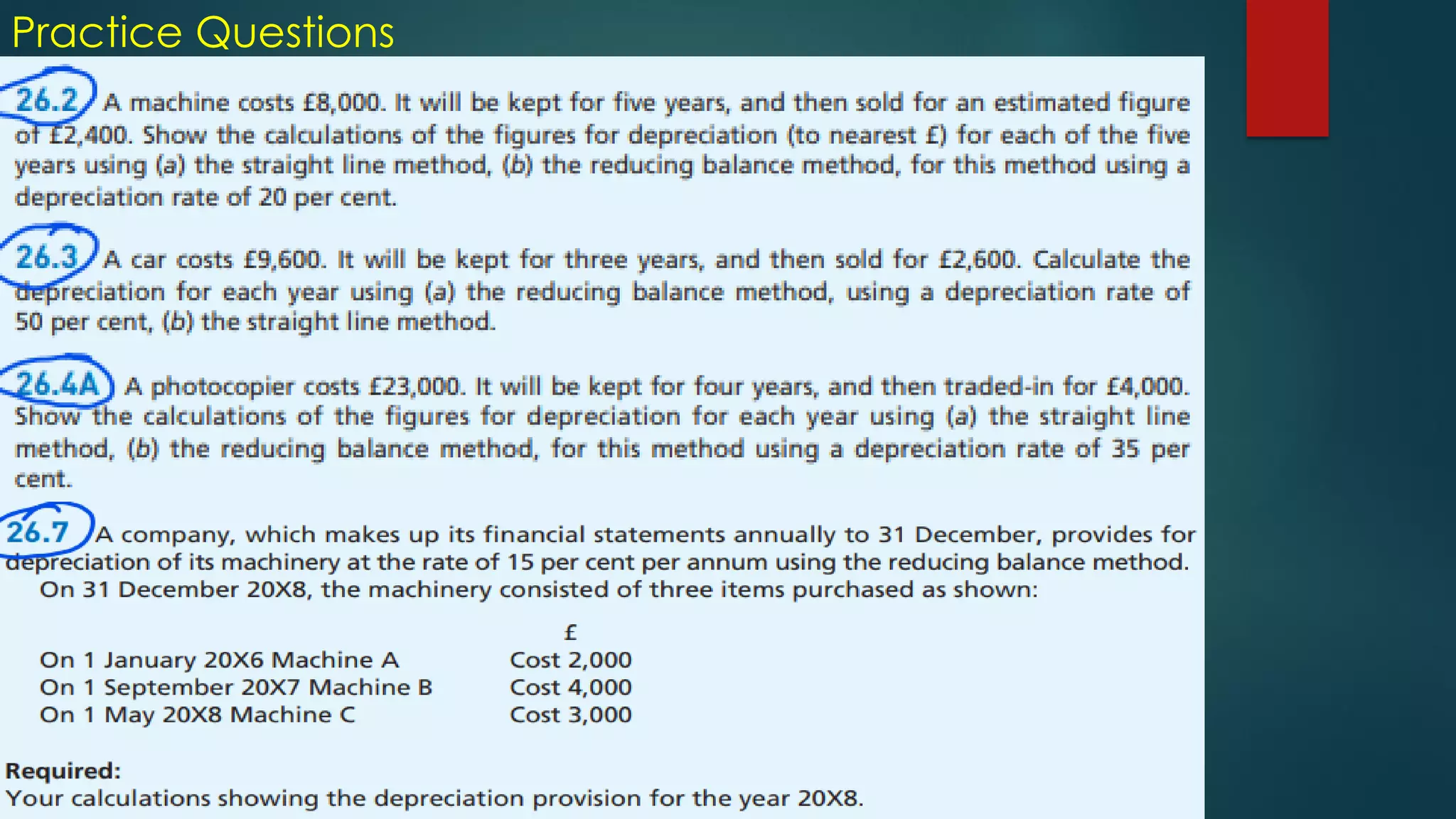

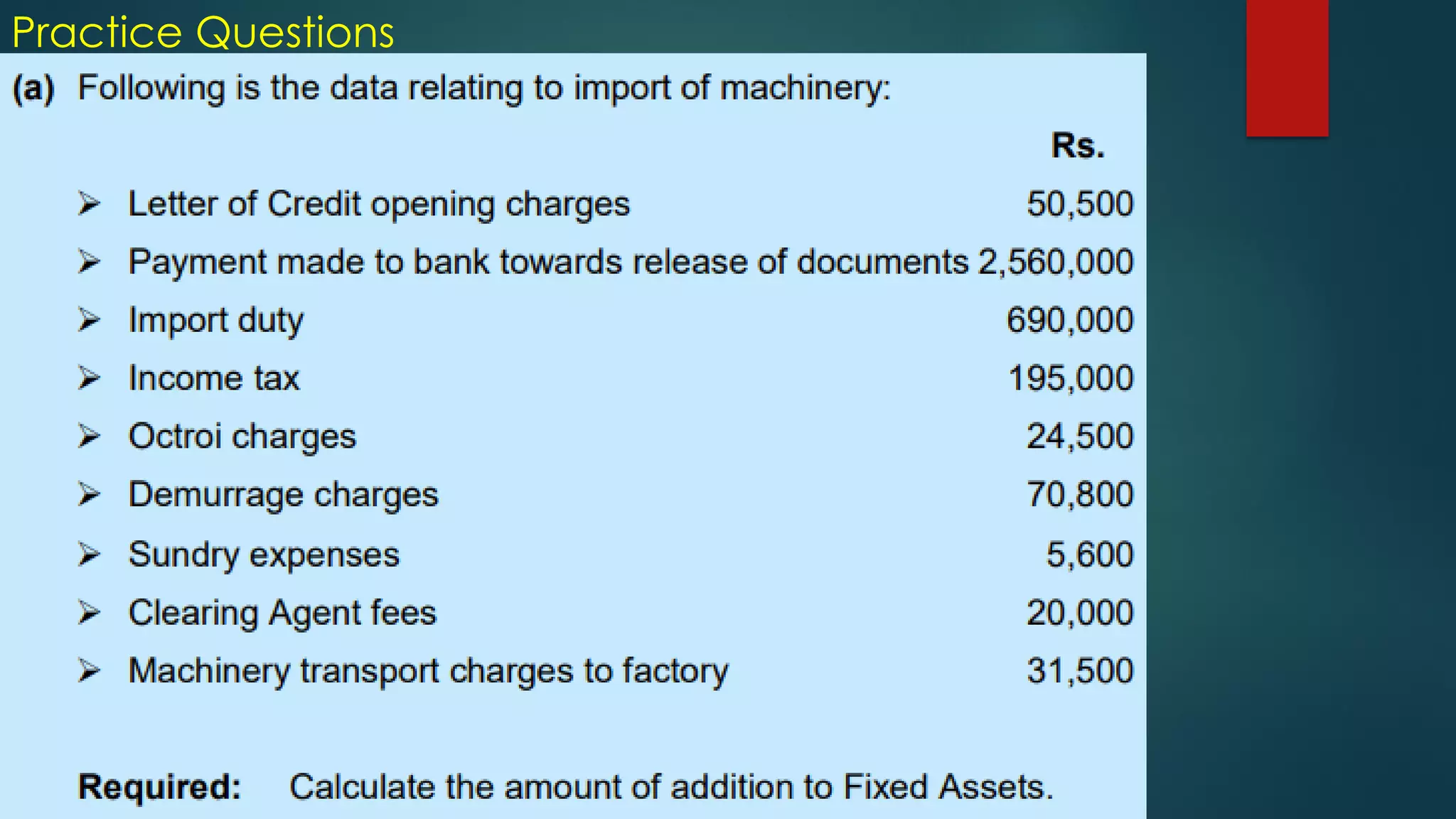

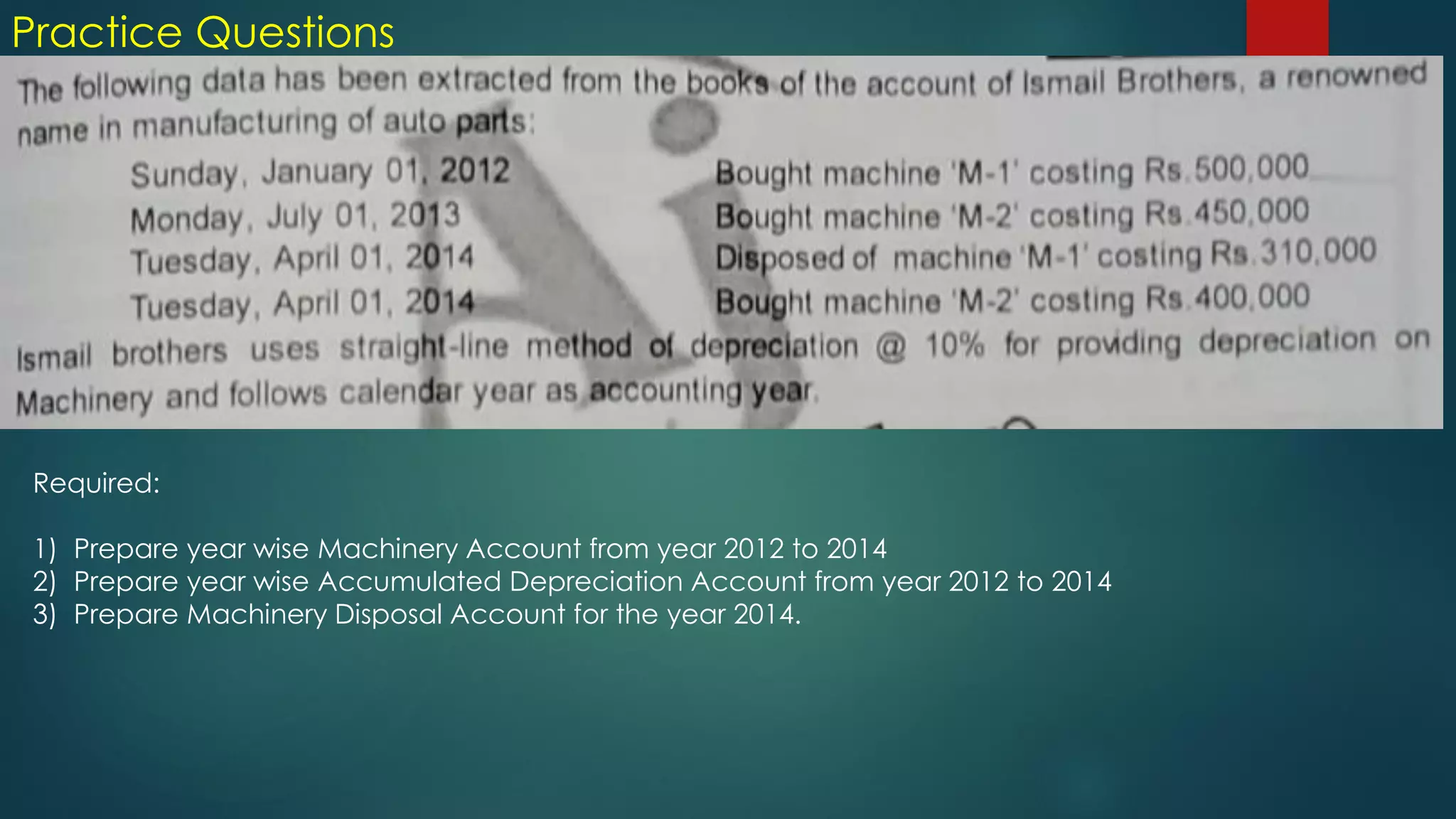

Practice Questions

Required:

1) Prepareyear wise Machinery Account from year 2012 to 2014

2) Prepare year wise Accumulated Depreciation Account from year 2012 to 2014

3) Prepare Machinery Disposal Account for the year 2014.

17.

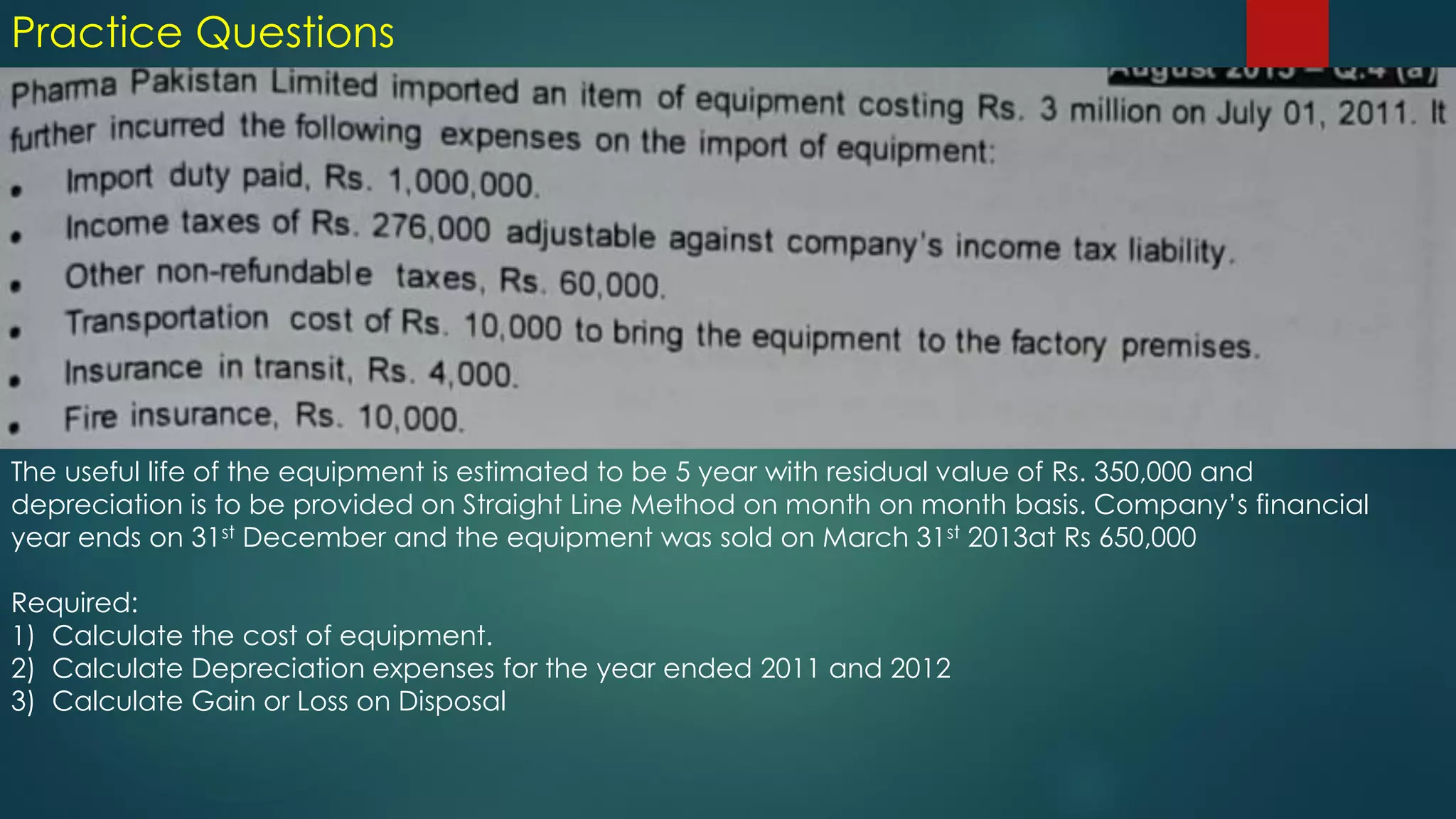

Practice Questions

The usefullife of the equipment is estimated to be 5 year with residual value of Rs. 350,000 and

depreciation is to be provided on Straight Line Method on month on month basis. Company’s financial

year ends on 31st December and the equipment was sold on March 31st 2013at Rs 650,000

Required:

1) Calculate the cost of equipment.

2) Calculate Depreciation expenses for the year ended 2011 and 2012

3) Calculate Gain or Loss on Disposal