Downloaded 16 times

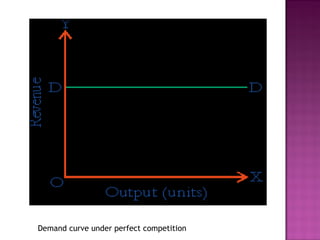

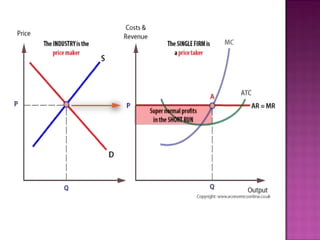

The document discusses the characteristics of perfect competition. Key points include: - Under perfect competition there are many small buyers and sellers of homogeneous products, with free entry and exit from the market. Firms are price takers and competition is based on price. - In the short run, individual firms have a perfectly elastic demand curve and produce at the quantity where marginal revenue equals marginal cost, given the fixed market price. - In the long run, firms enter and exit the industry to earn normal profits, resulting in economic equilibrium with price equal to minimum average cost for all firms.