Downloaded 33 times

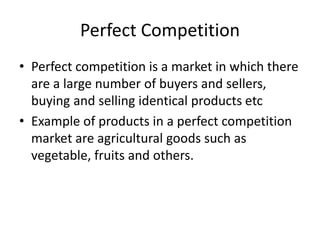

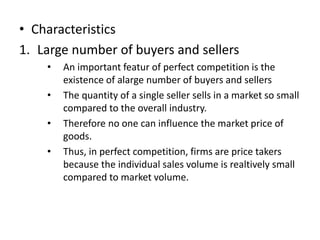

1. Perfect competition is characterized by many small firms and buyers, homogeneous products, free entry and exit, and perfect information. 2. Under perfect competition, firms are price takers and cannot influence the market price. They must sell at the going market price. 3. In the short run, a perfectly competitive firm will produce at the quantity where marginal revenue equals marginal cost to maximize profits. In the long run, firms will enter or exit the market until economic profits are driven down to zero.