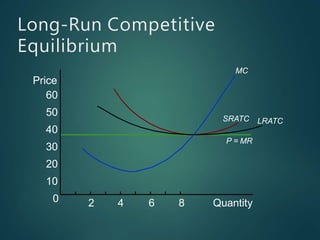

This document defines the characteristics of perfect competition and outlines the necessary conditions for a perfectly competitive market. It explains that in perfect competition, there are many small firms and buyers/sellers that are price takers, homogeneous products, free entry and exit, and perfect information. Firms produce at the quantity where price equals marginal cost to maximize profits. In the long run, perfect competition leads to zero economic profits and constant costs as firms enter and exit the market.