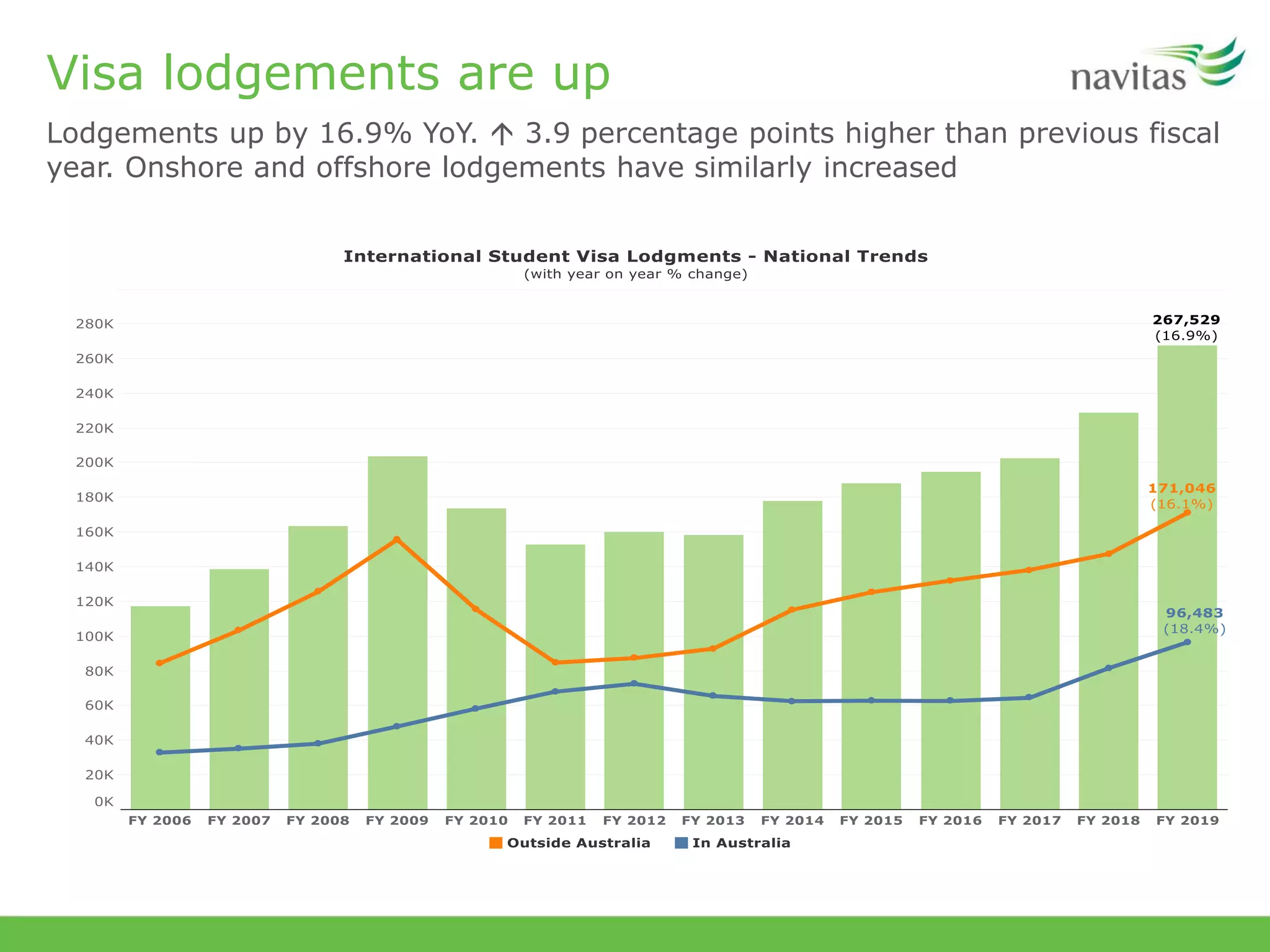

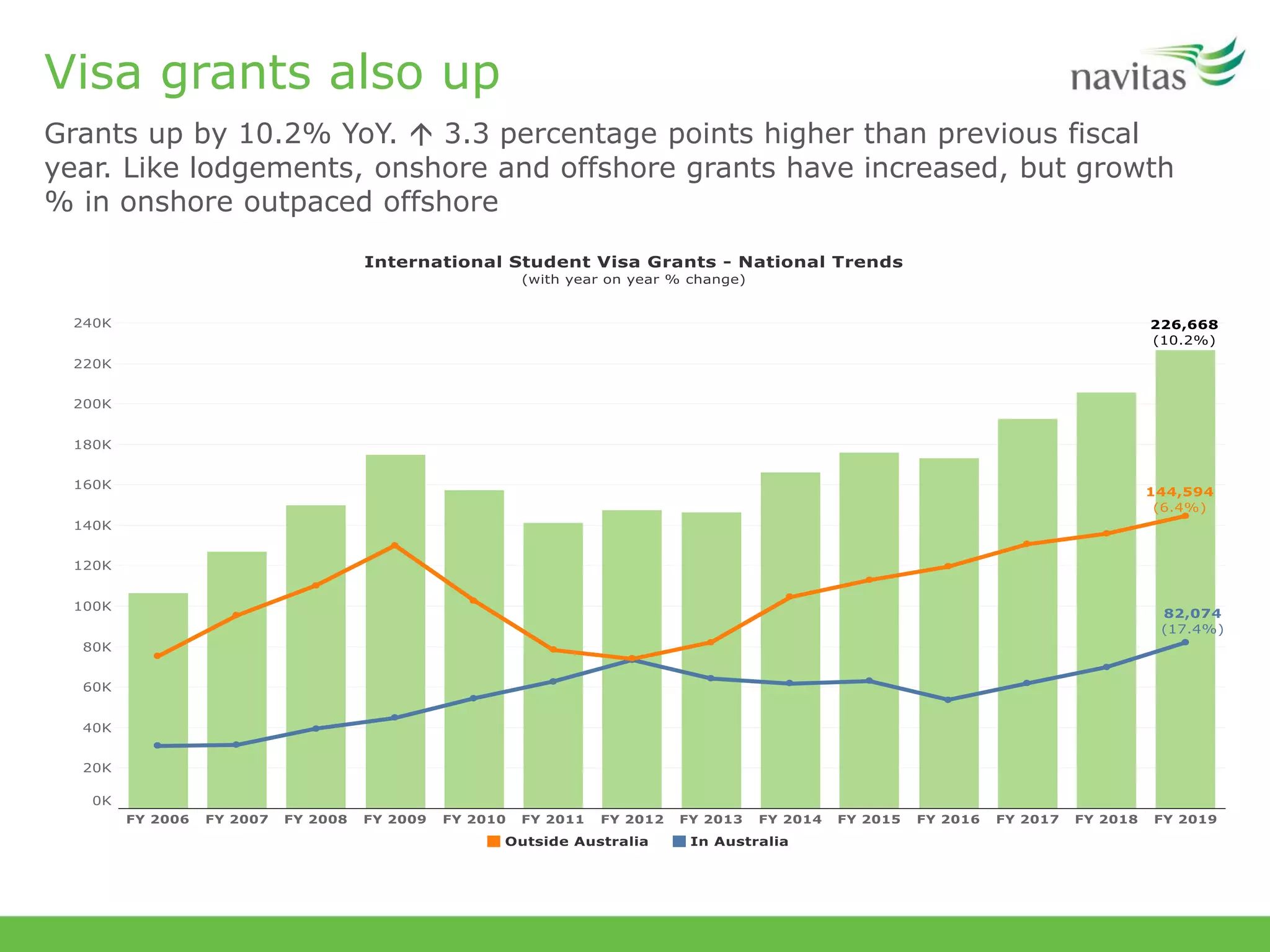

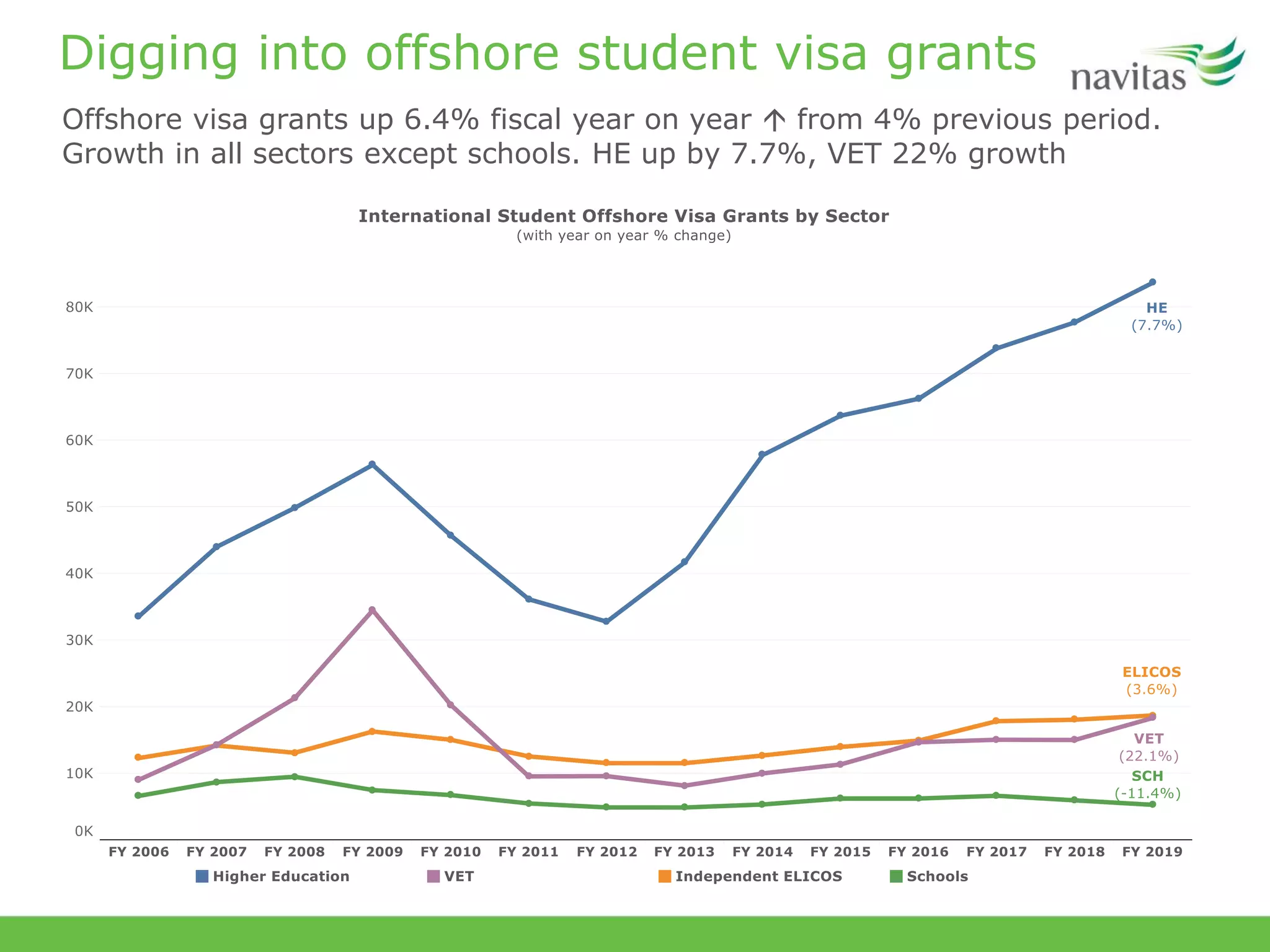

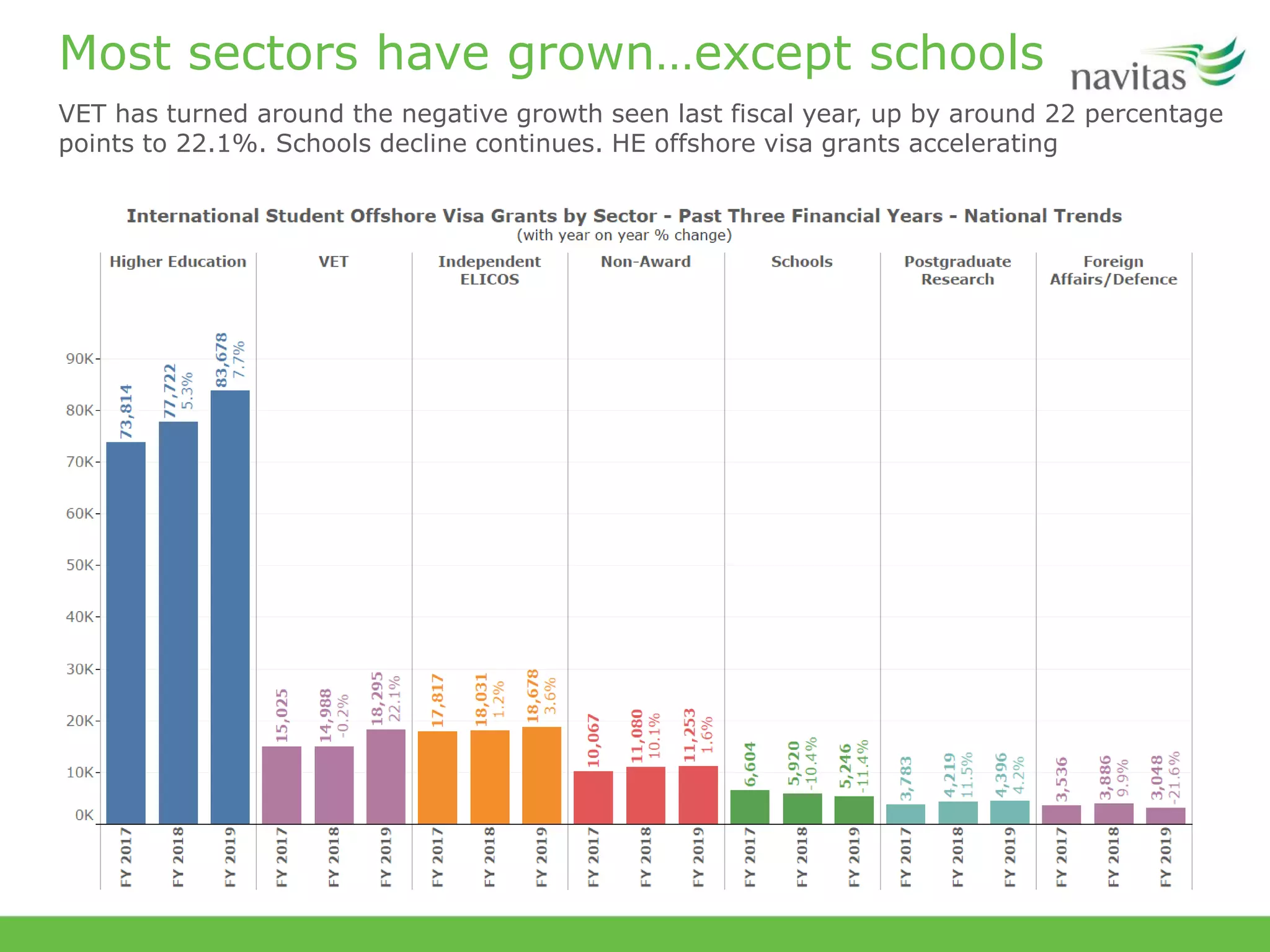

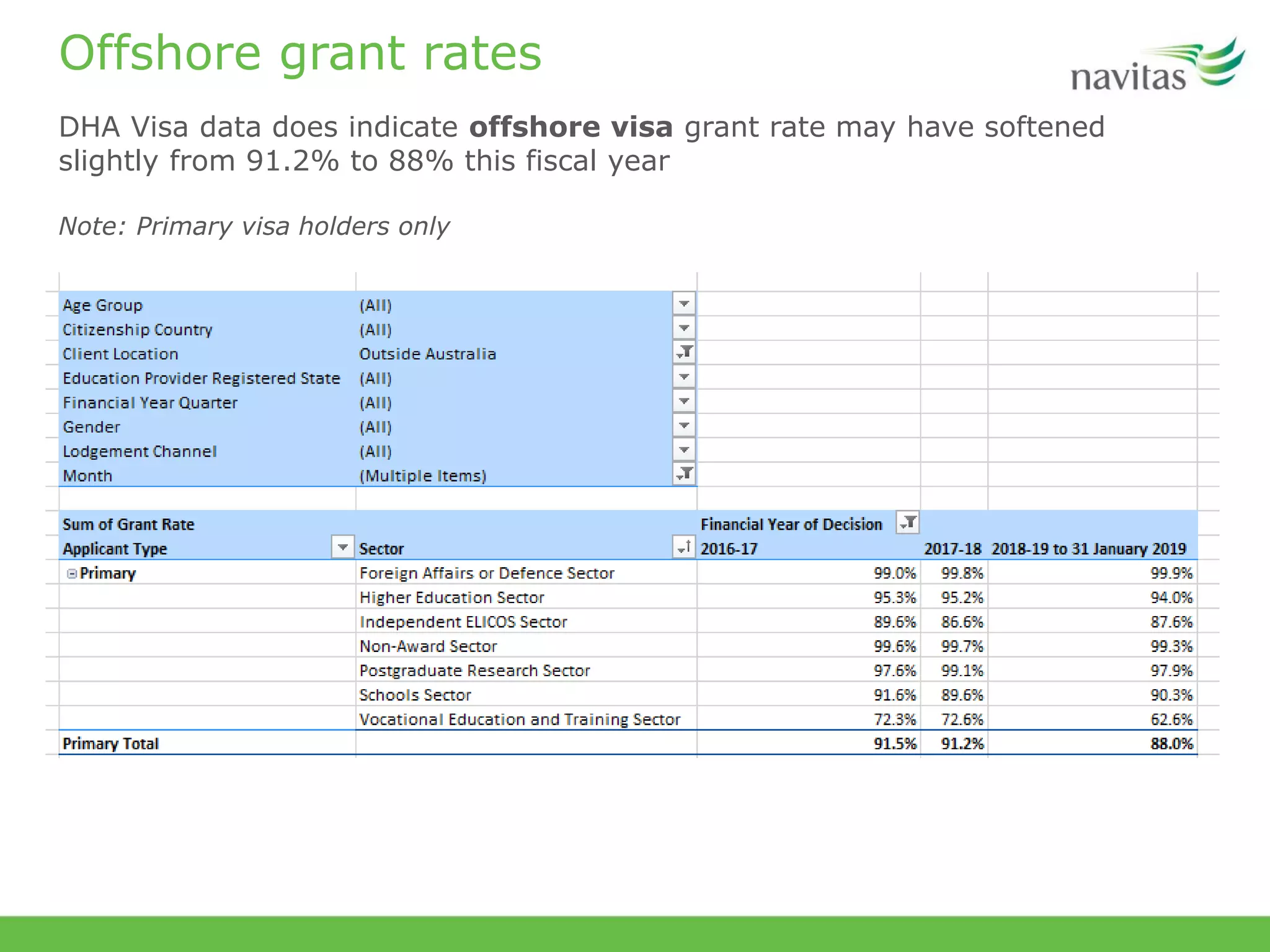

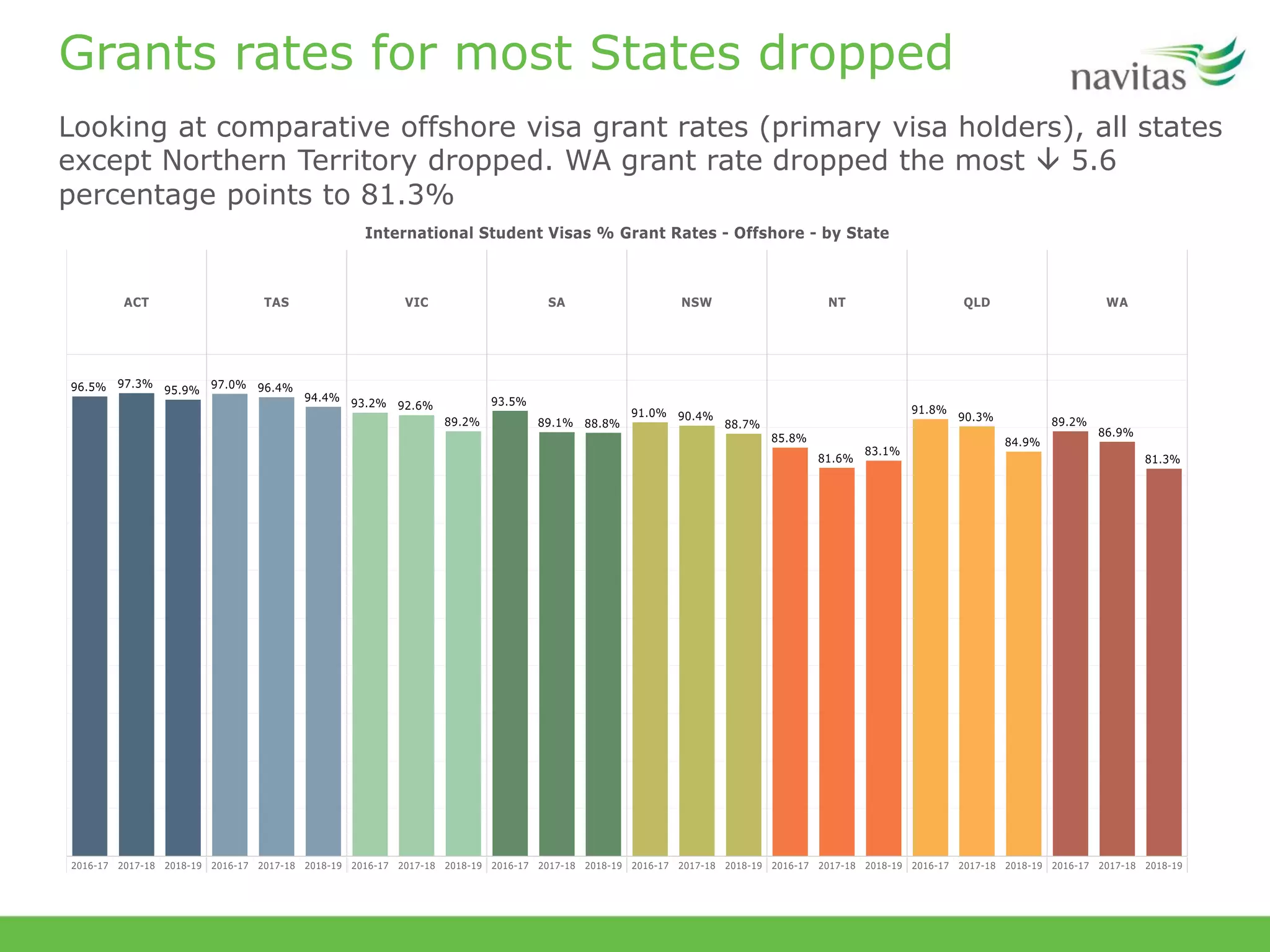

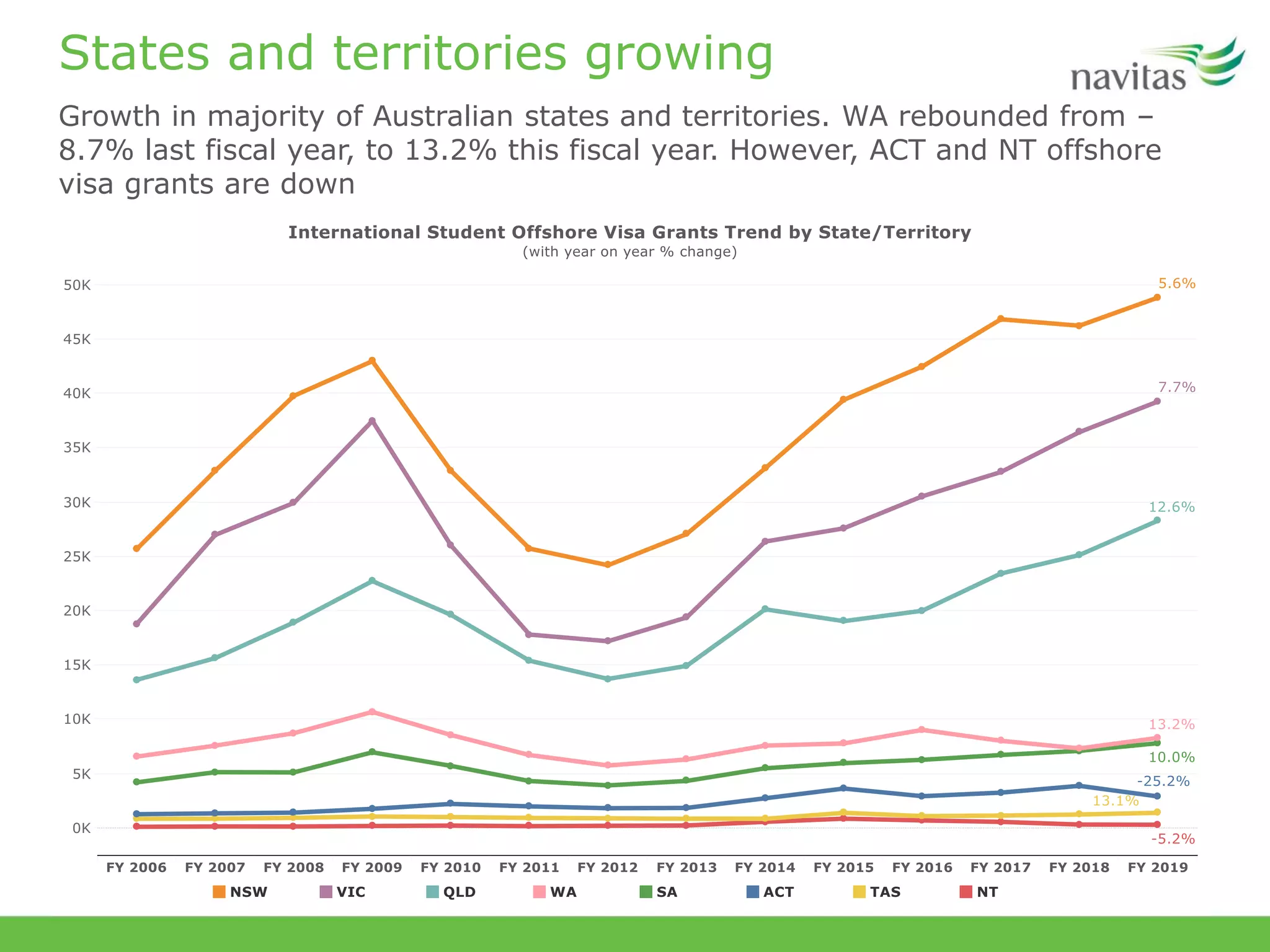

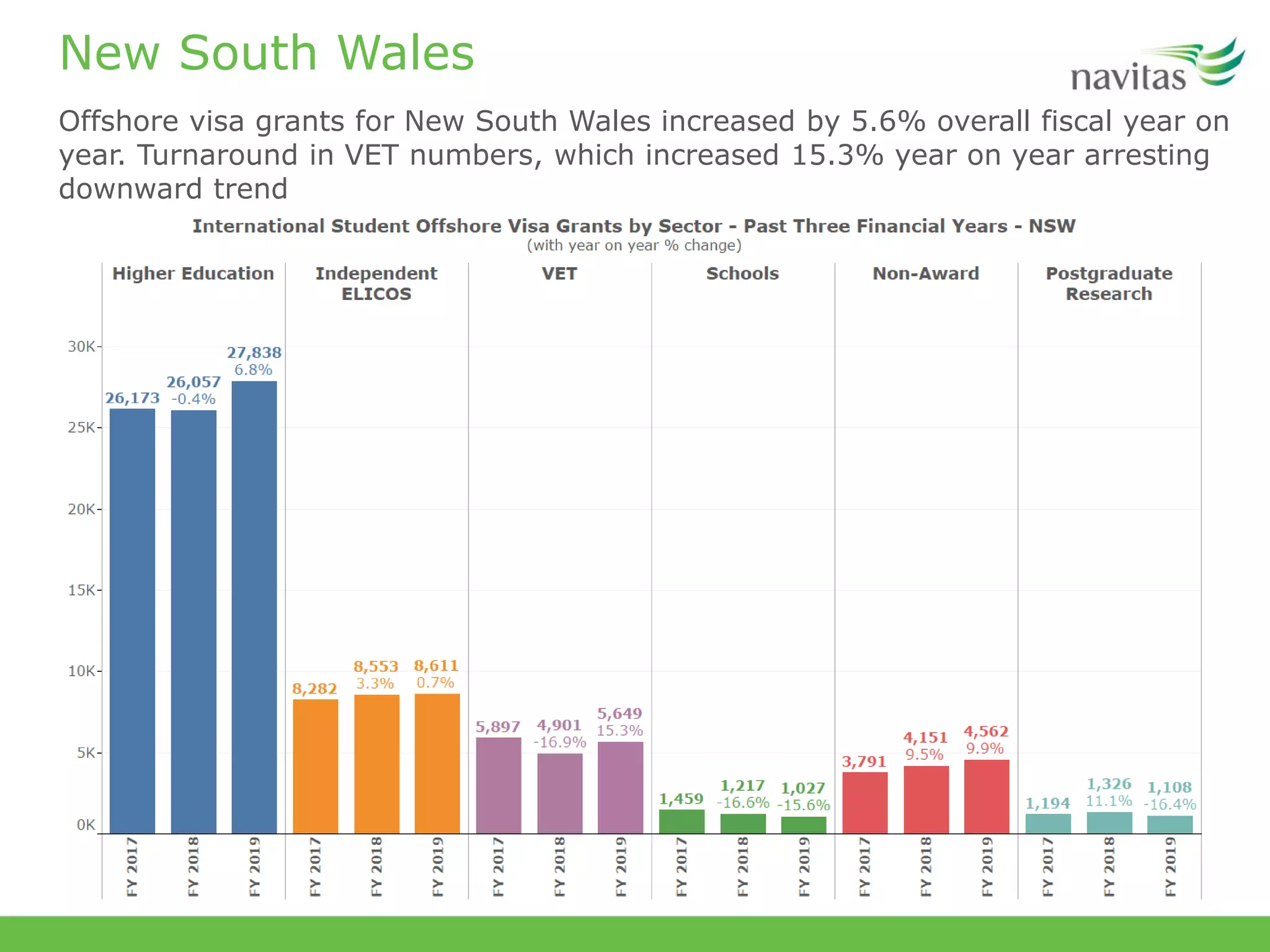

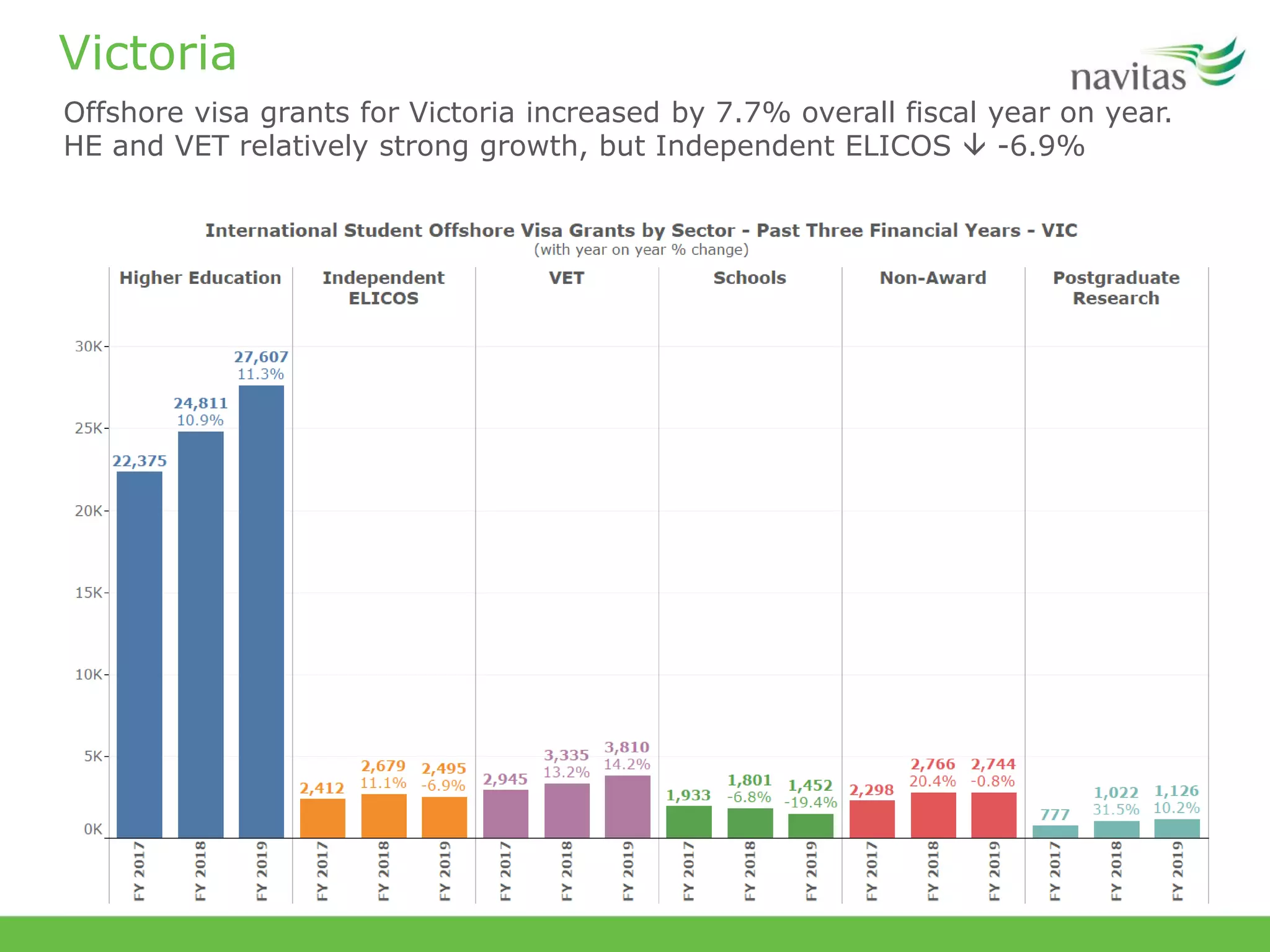

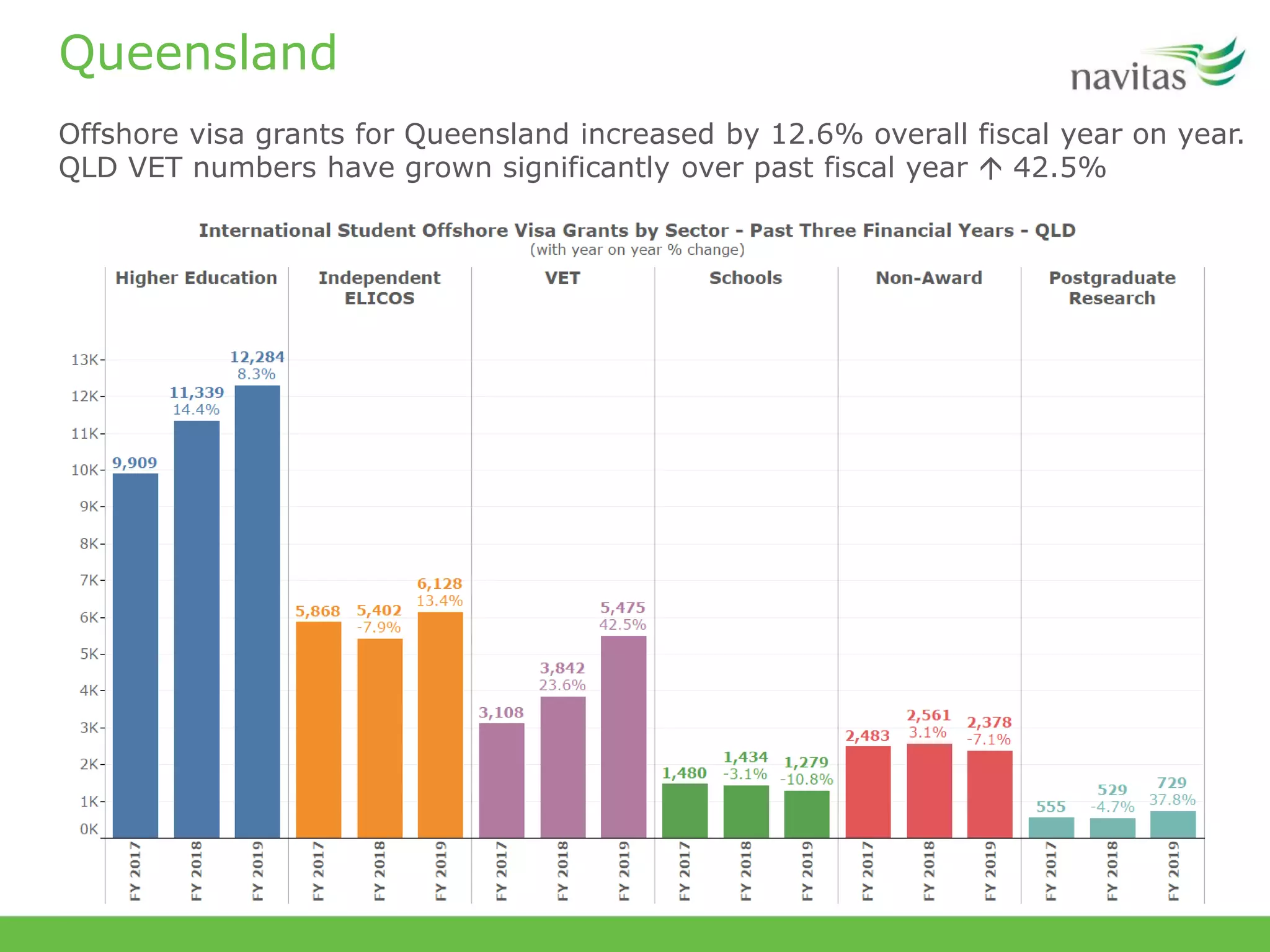

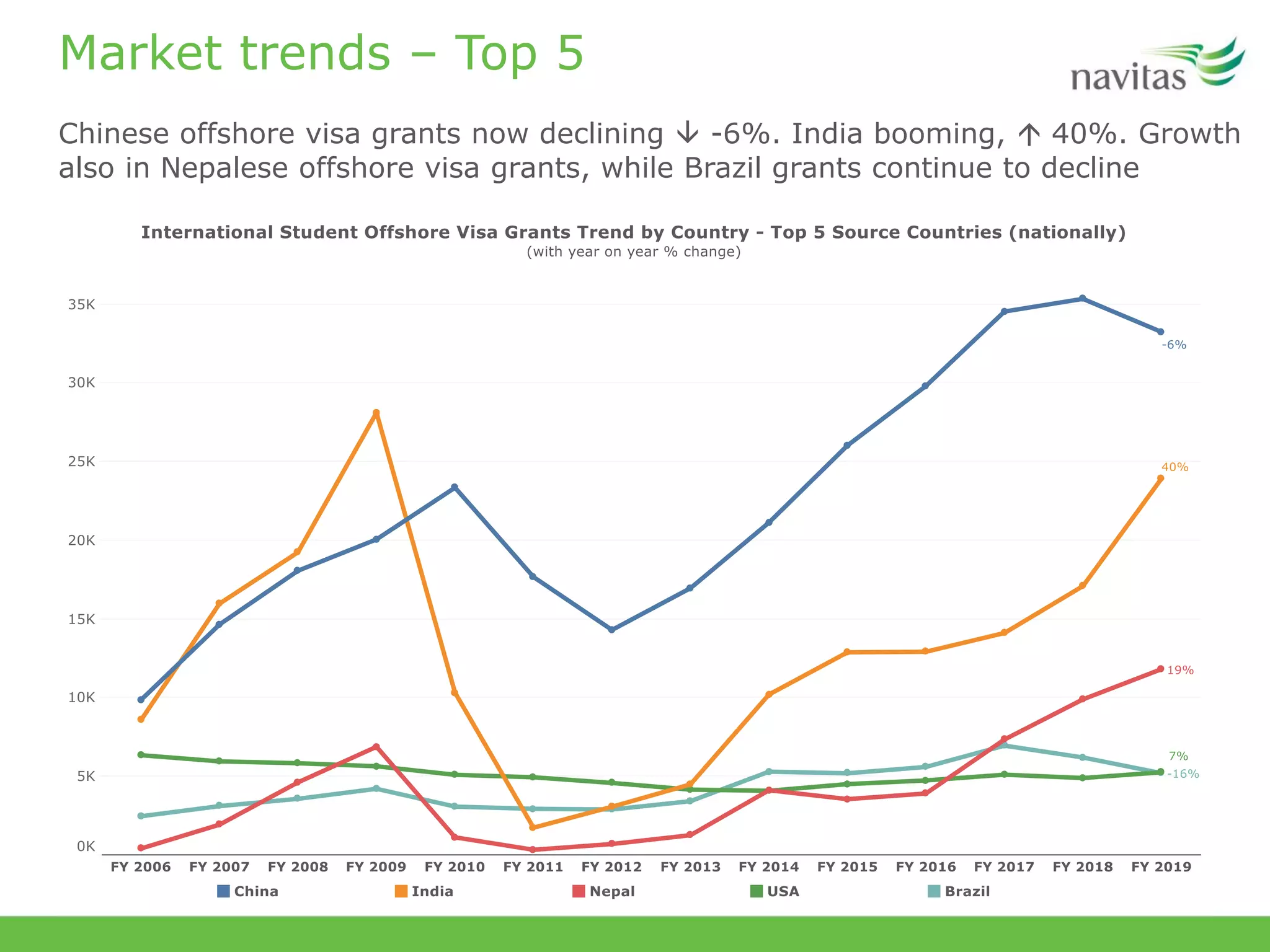

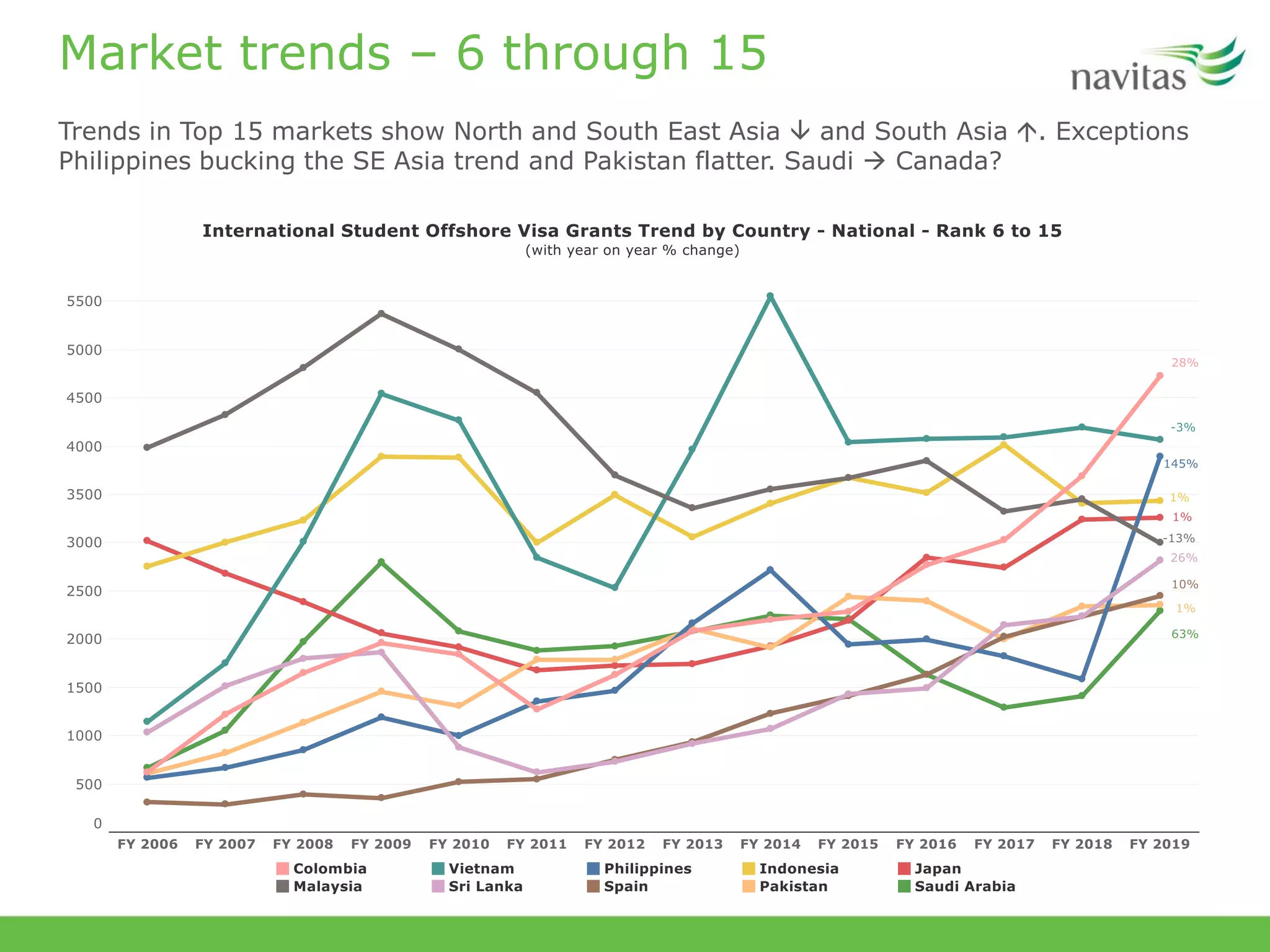

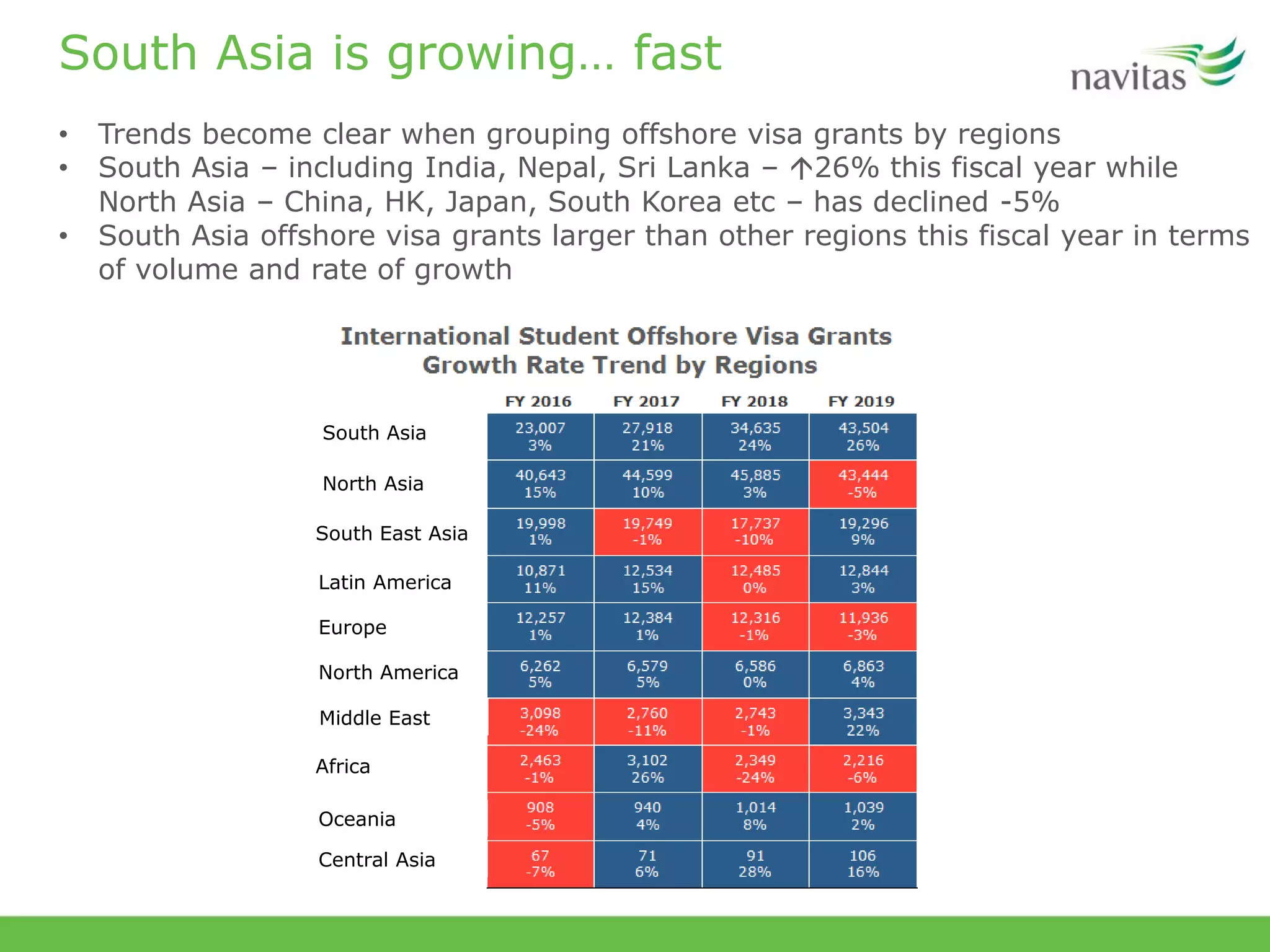

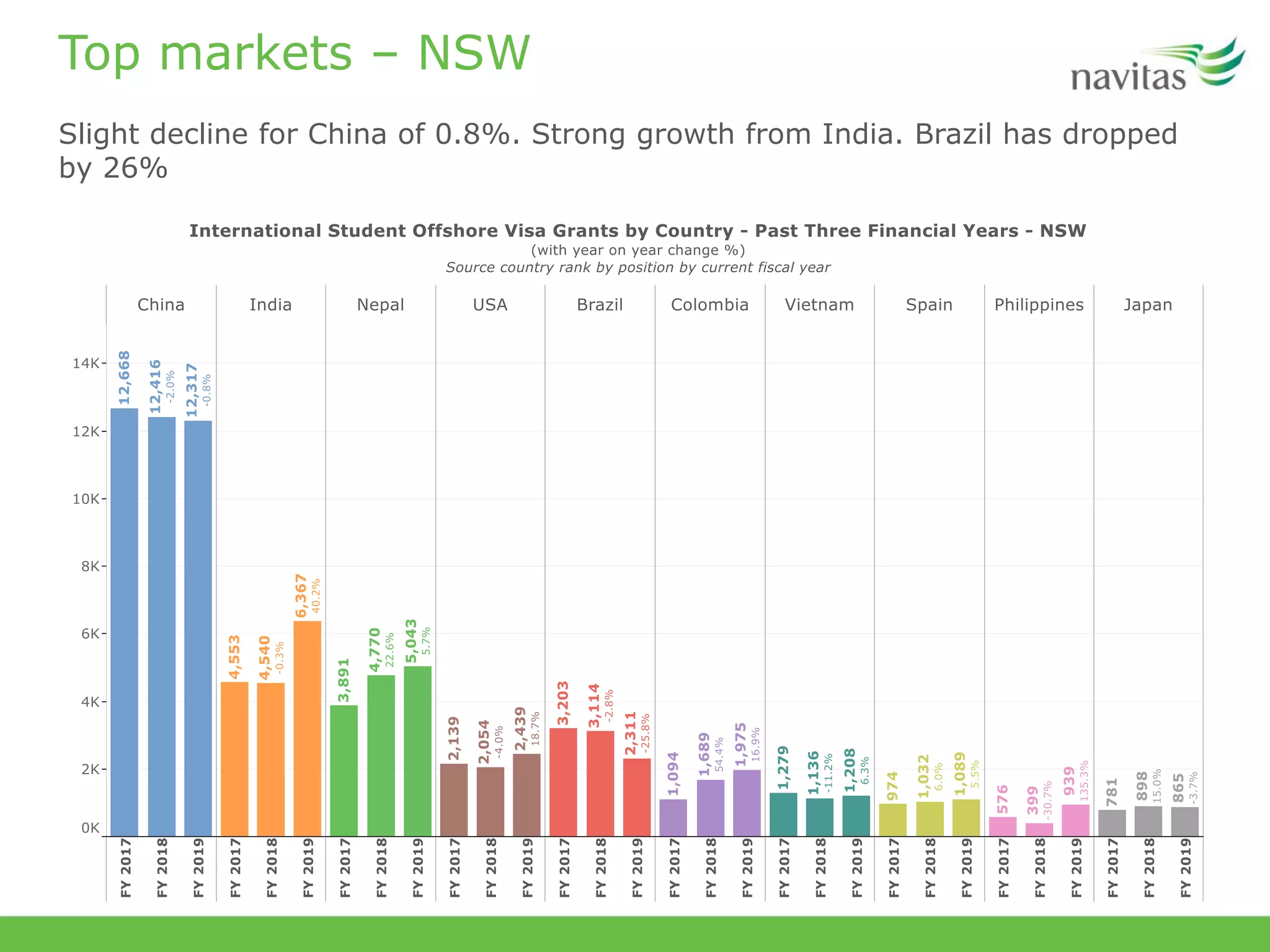

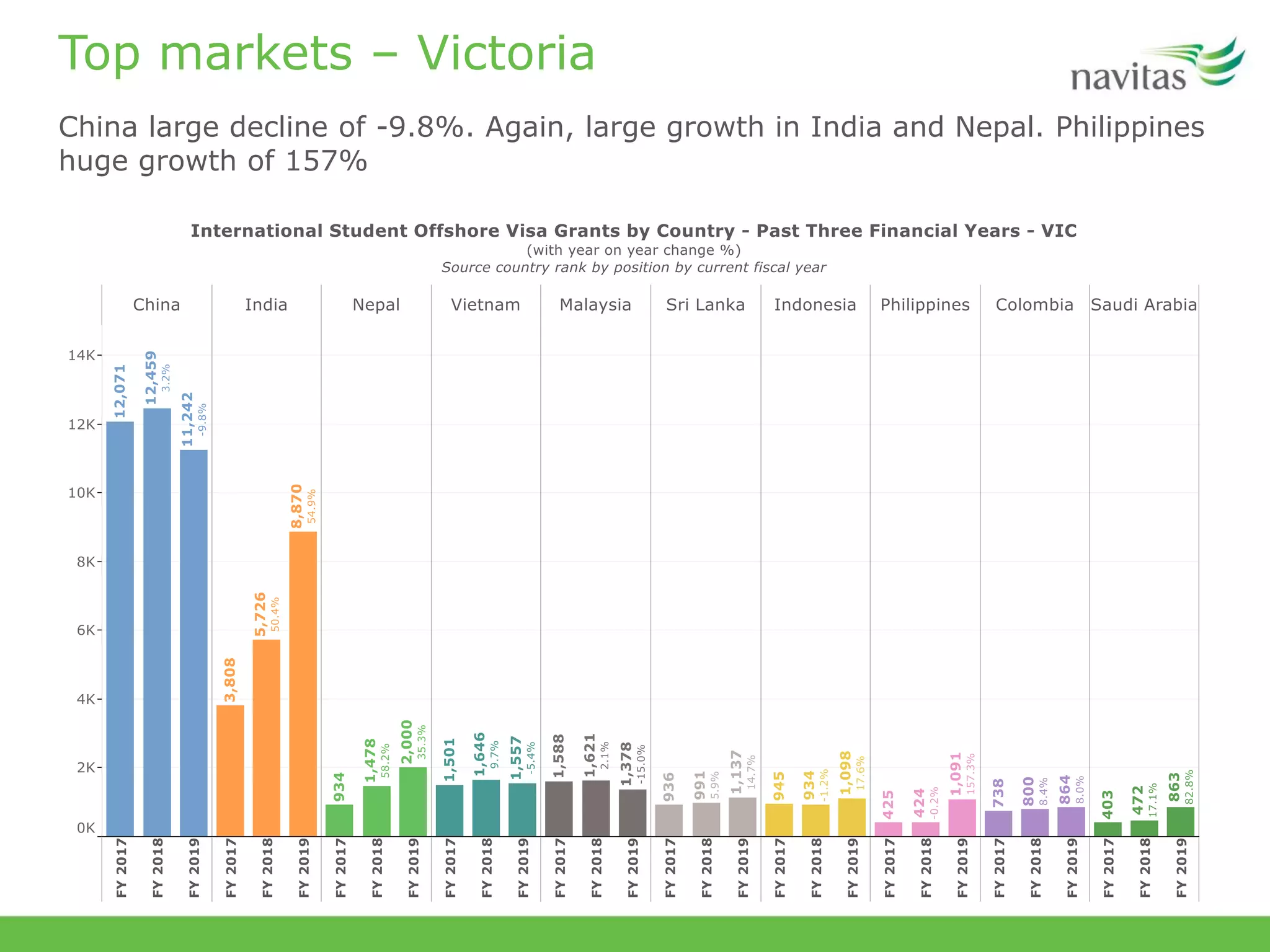

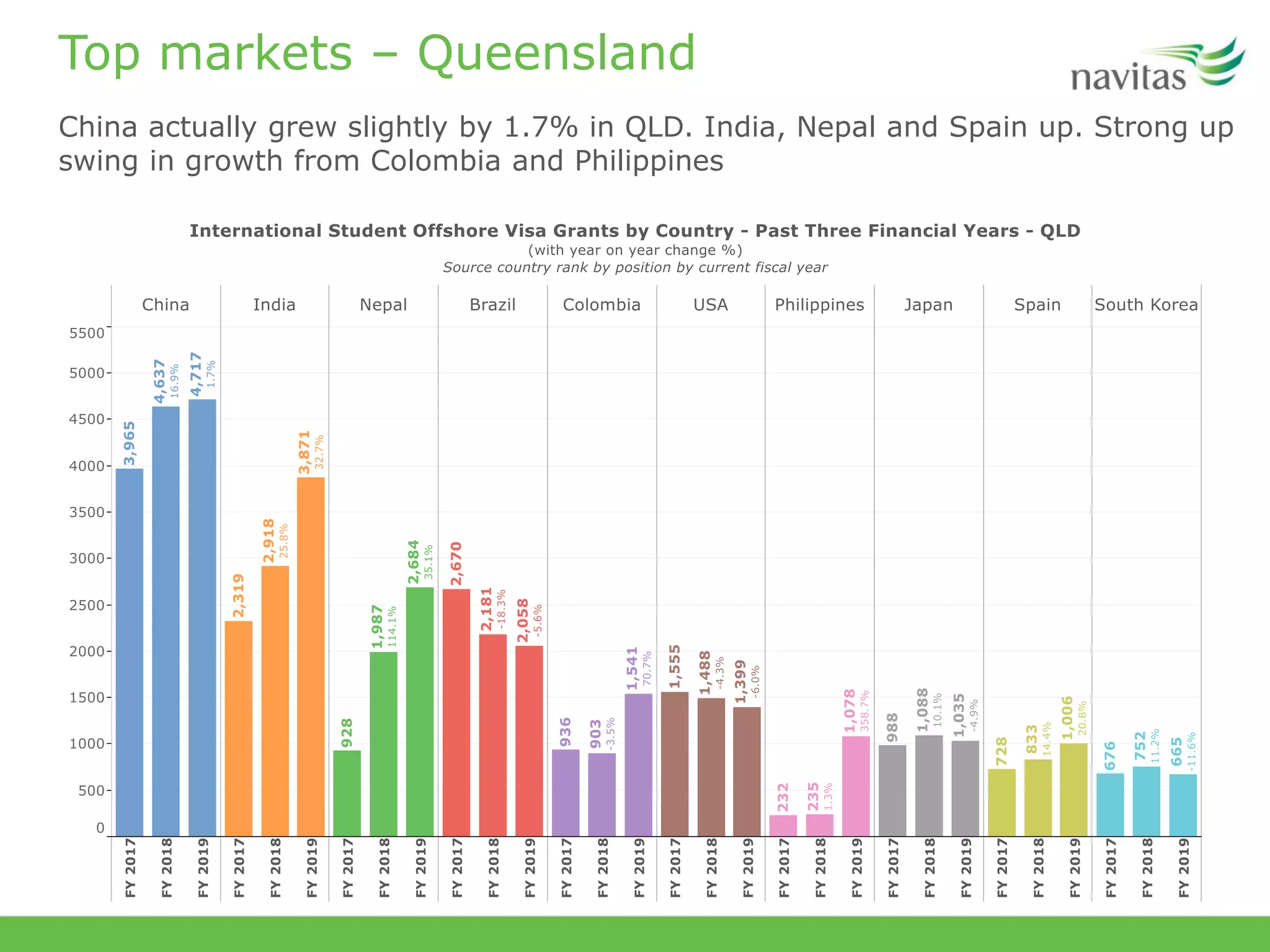

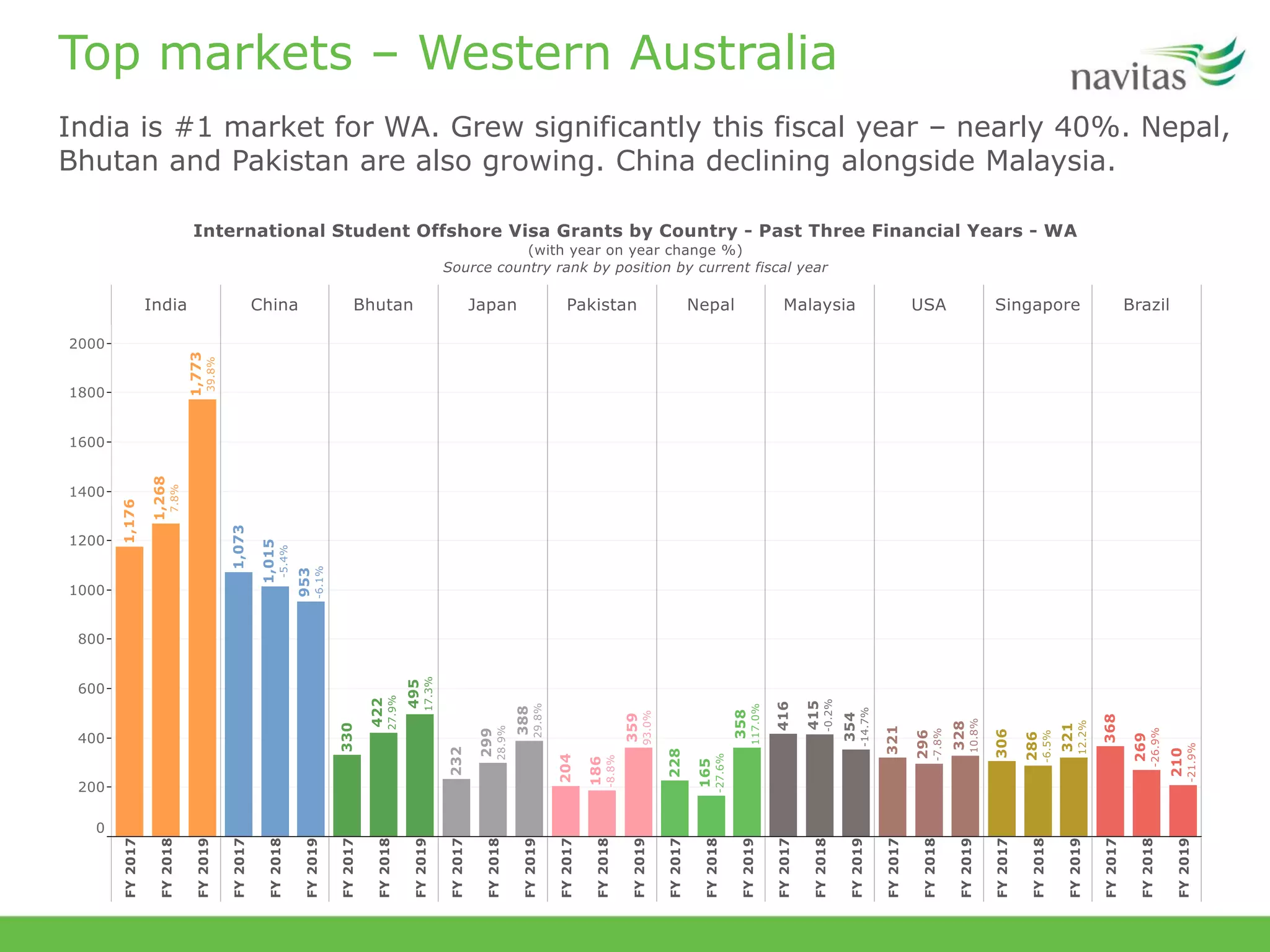

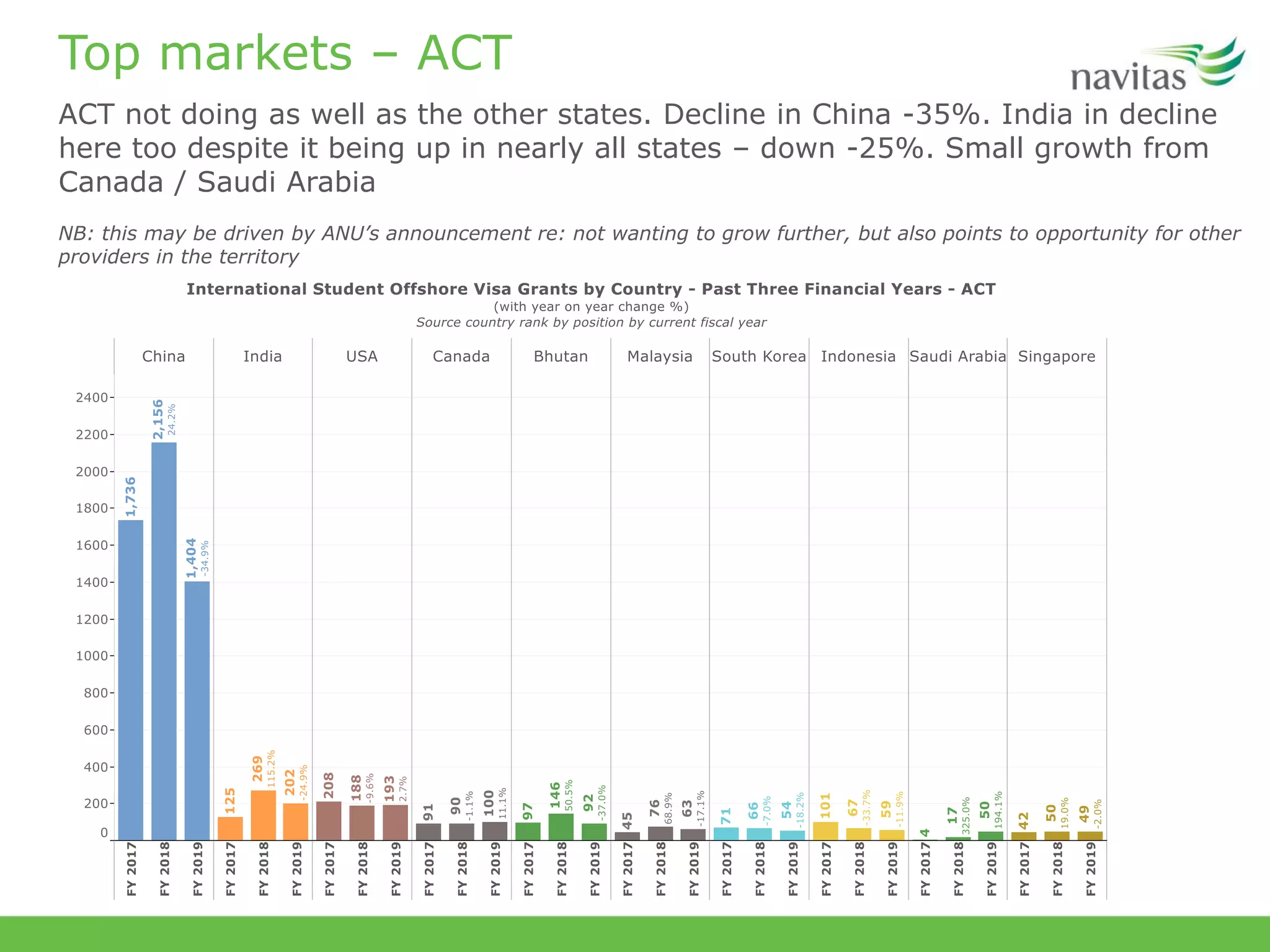

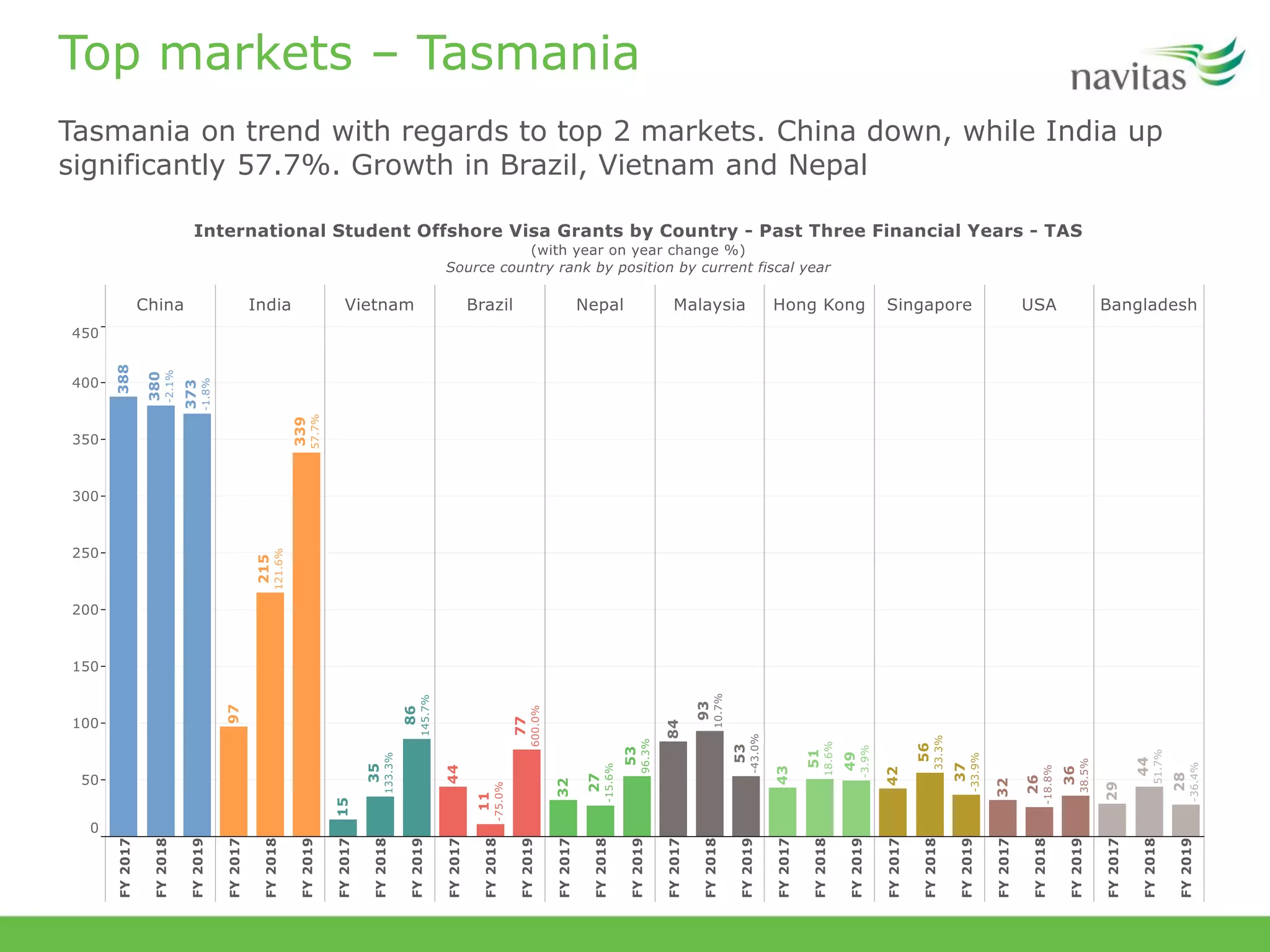

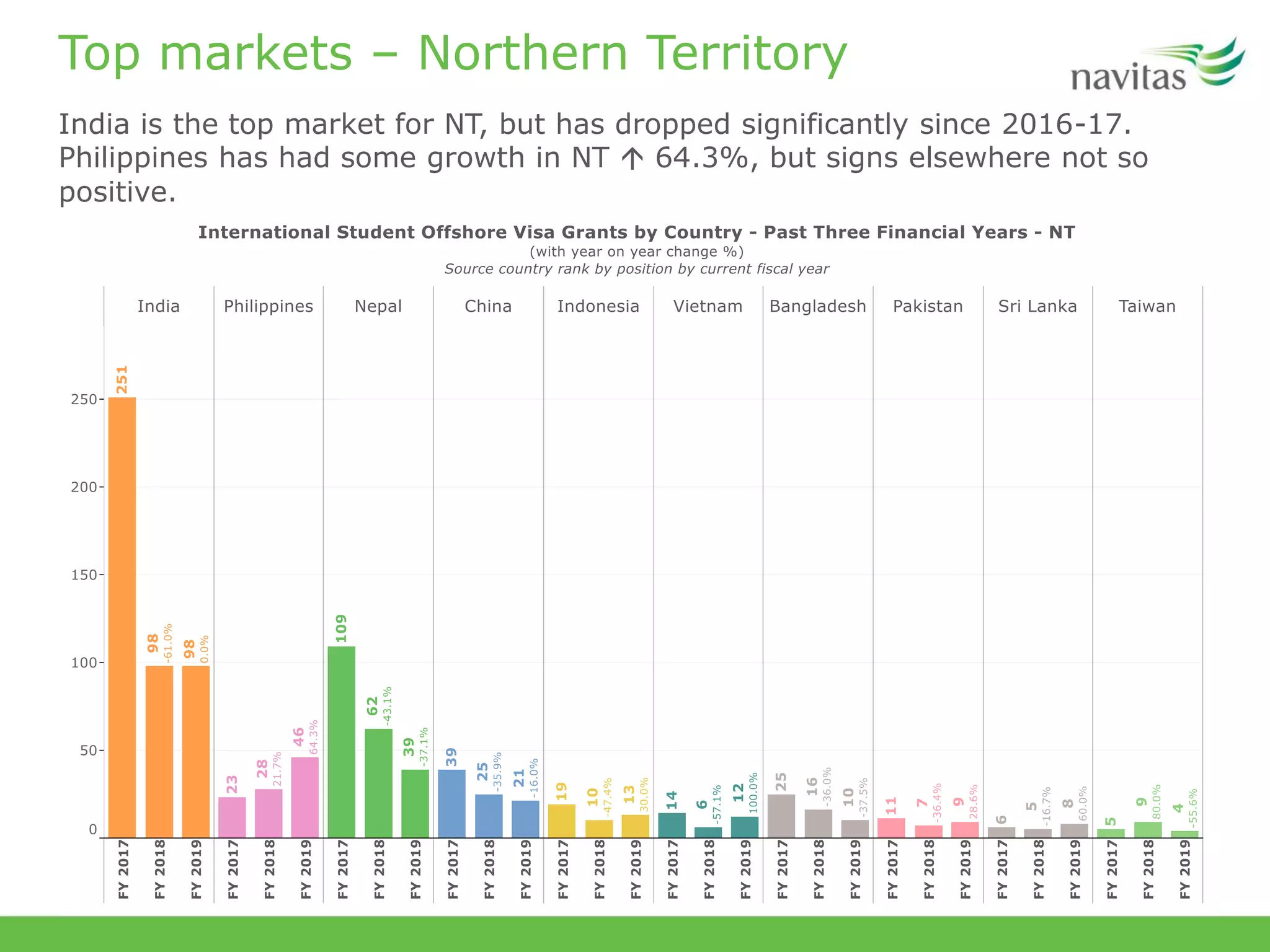

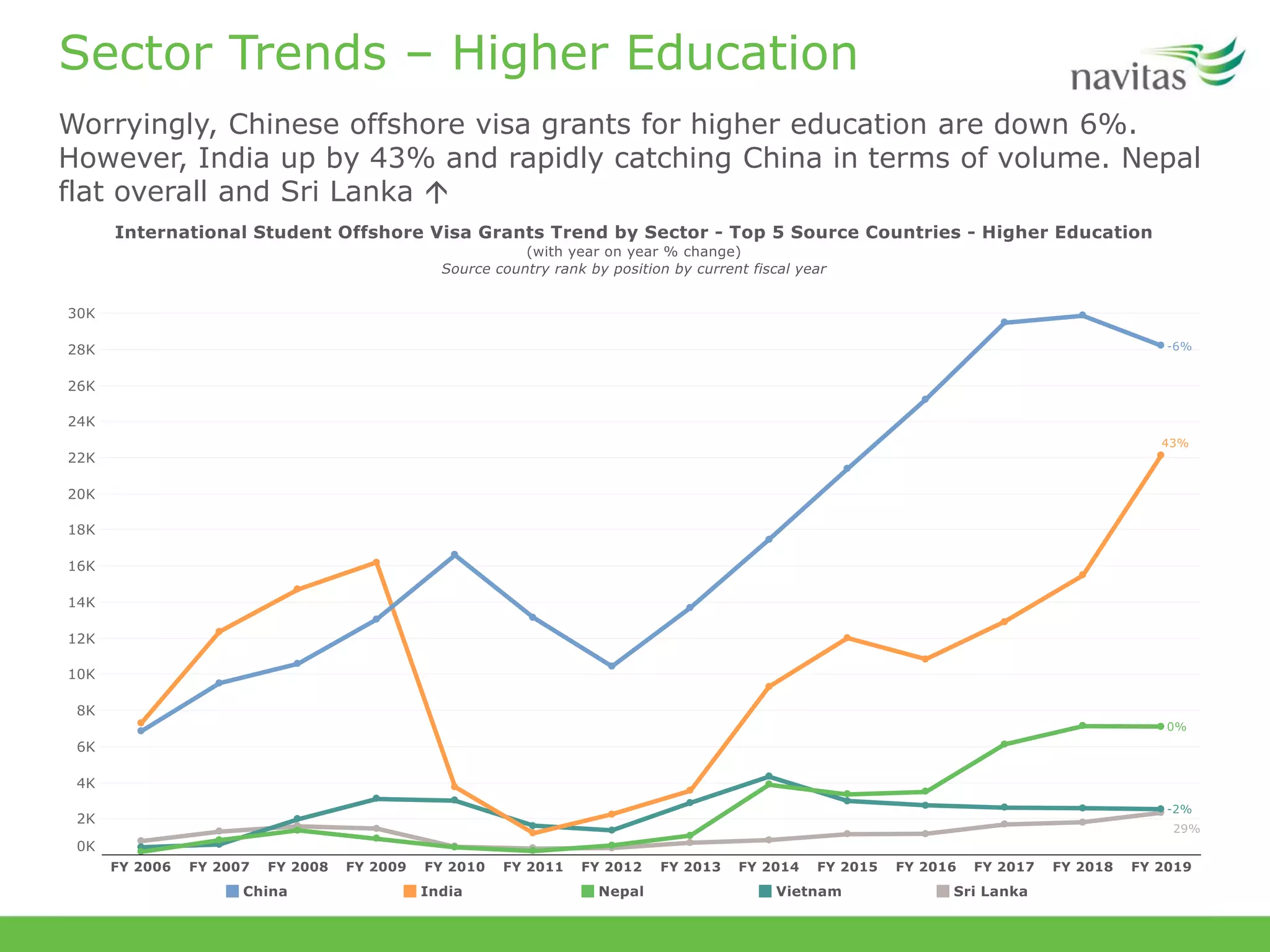

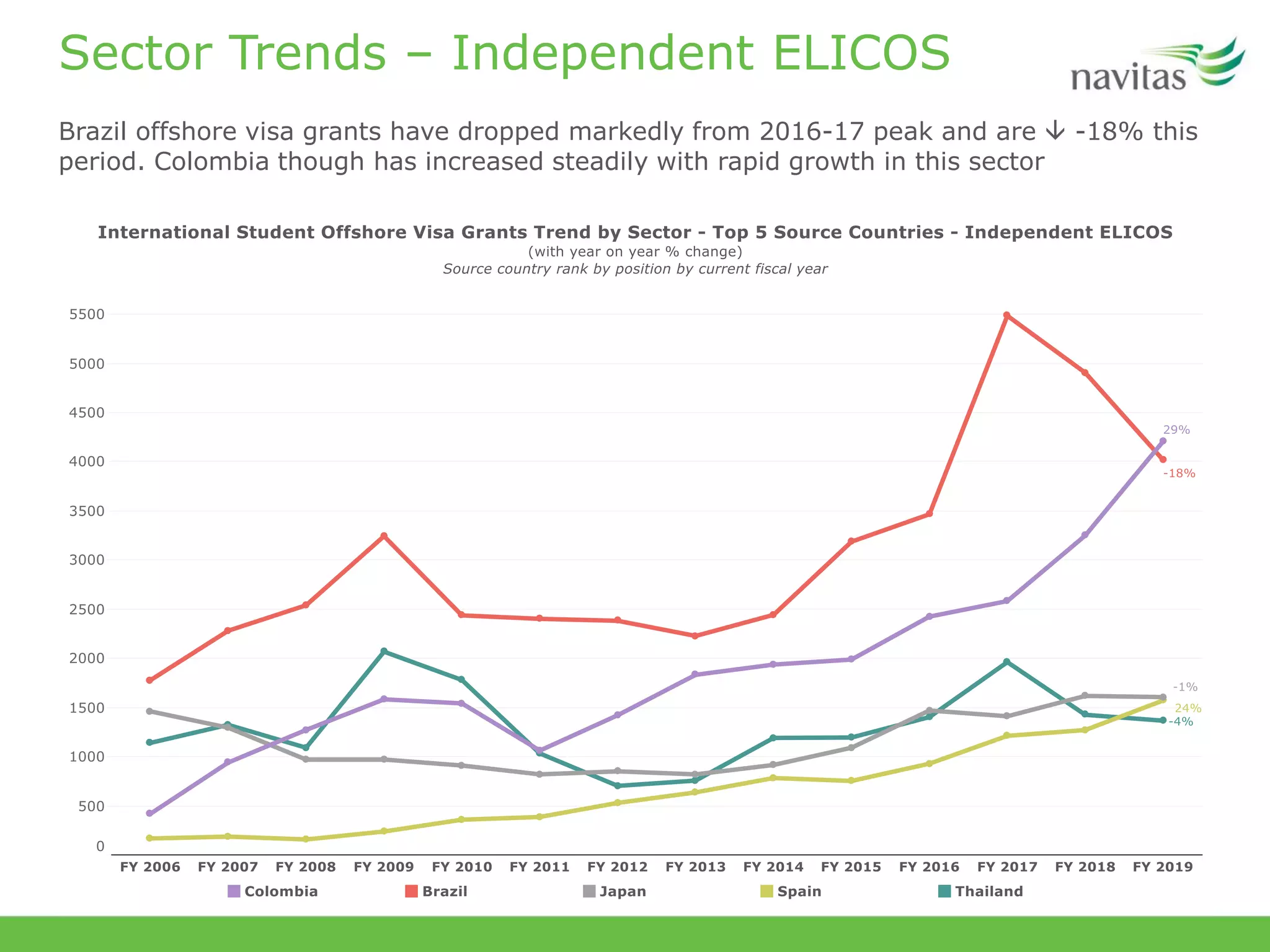

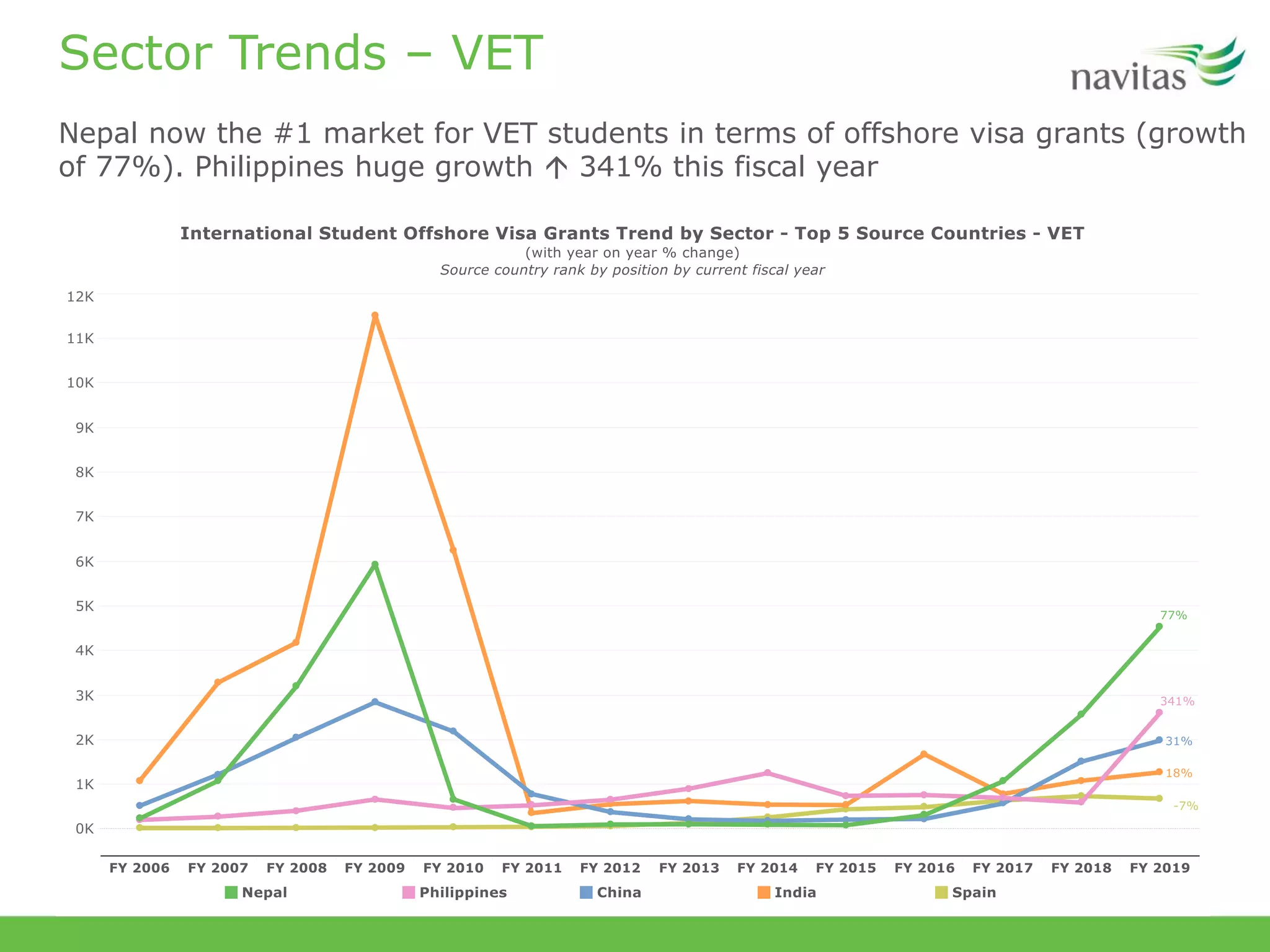

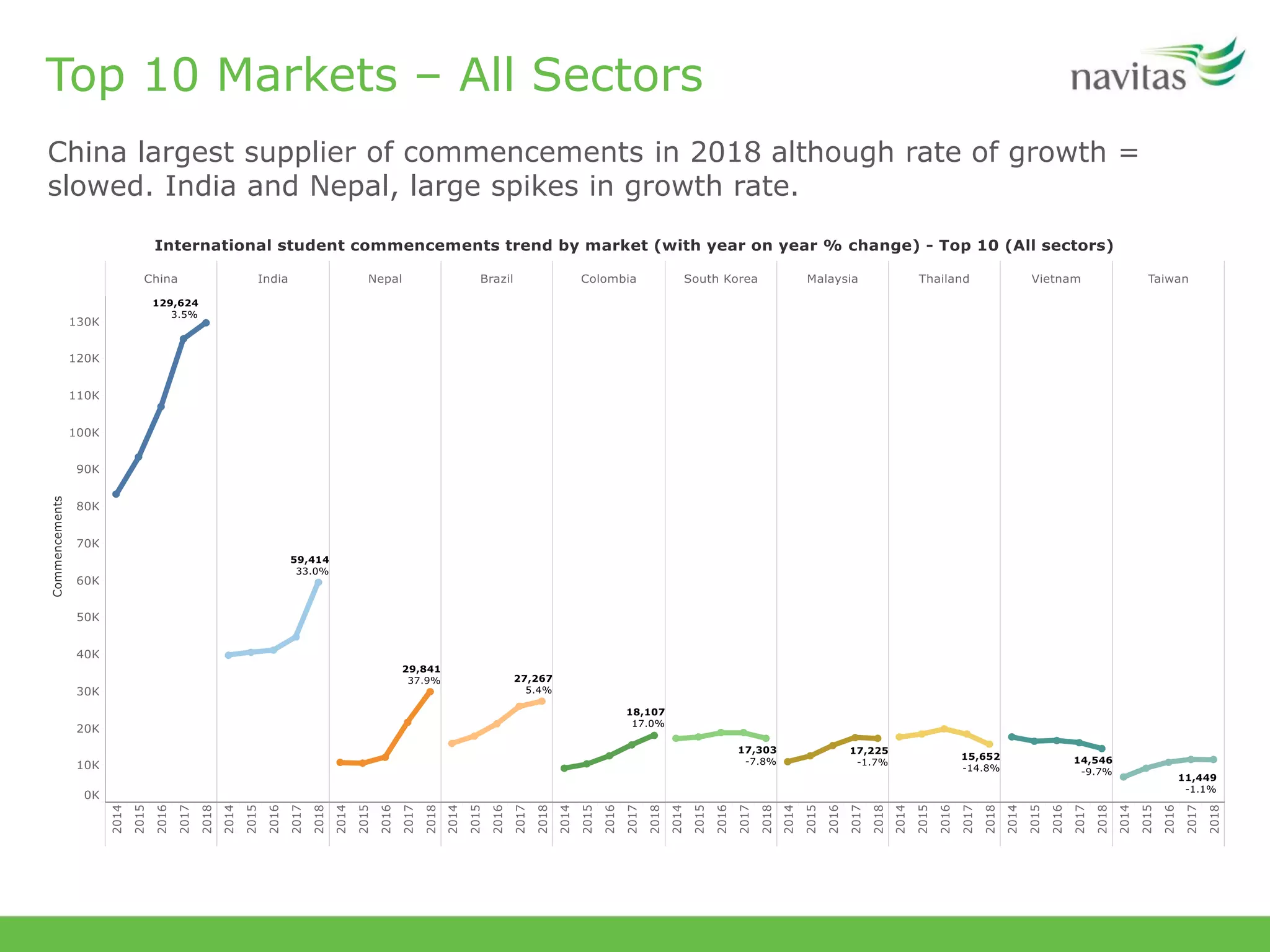

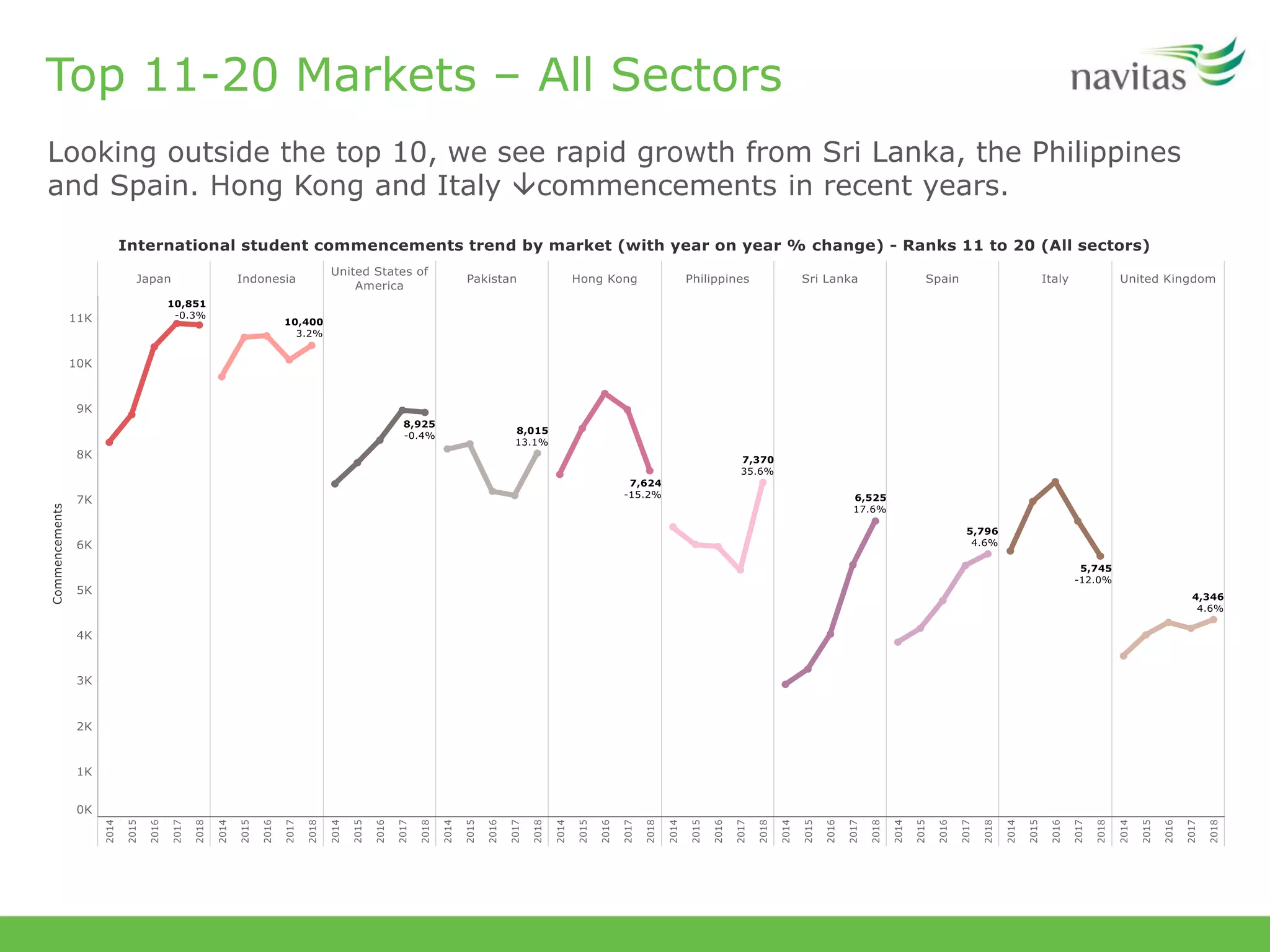

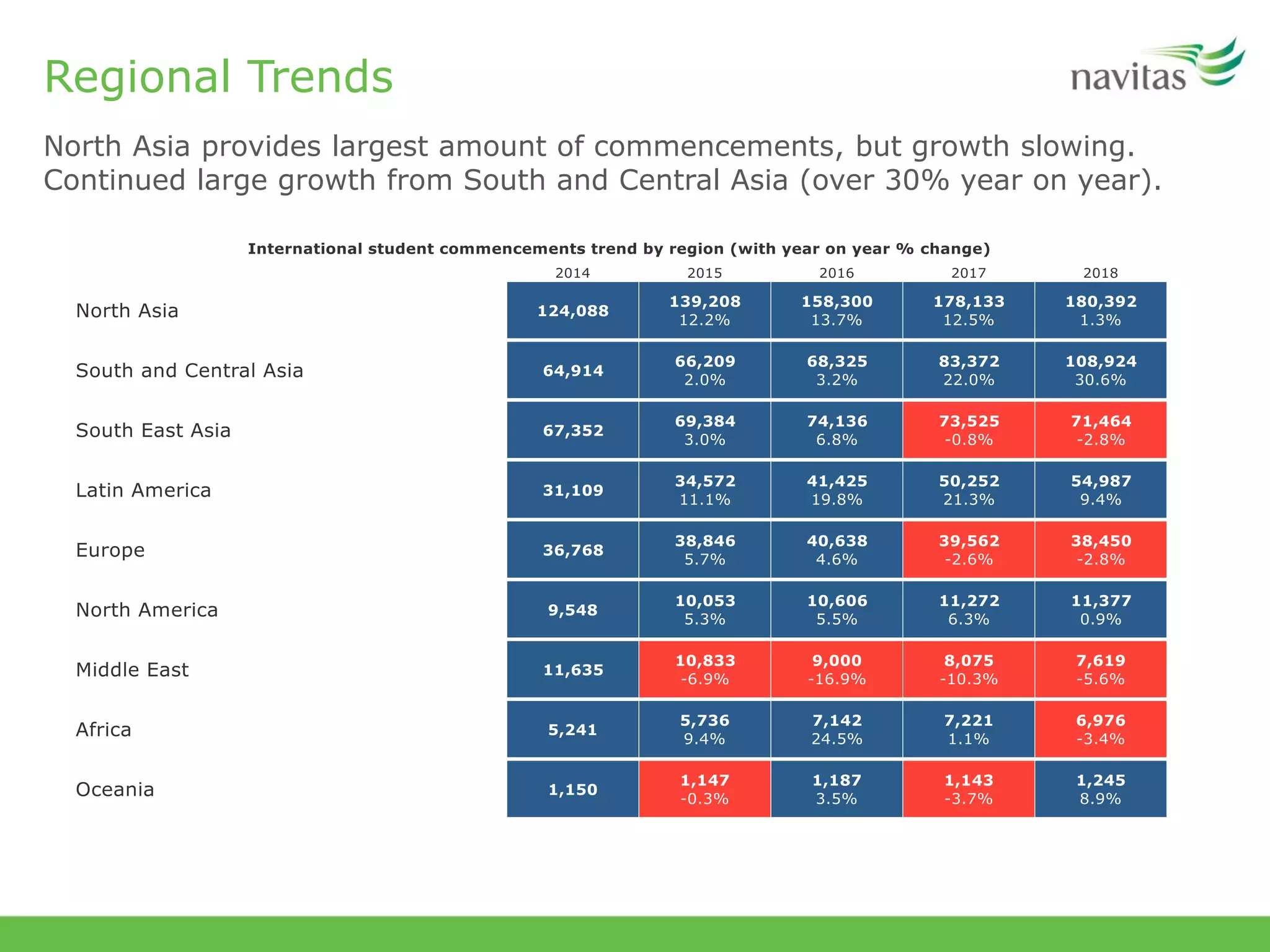

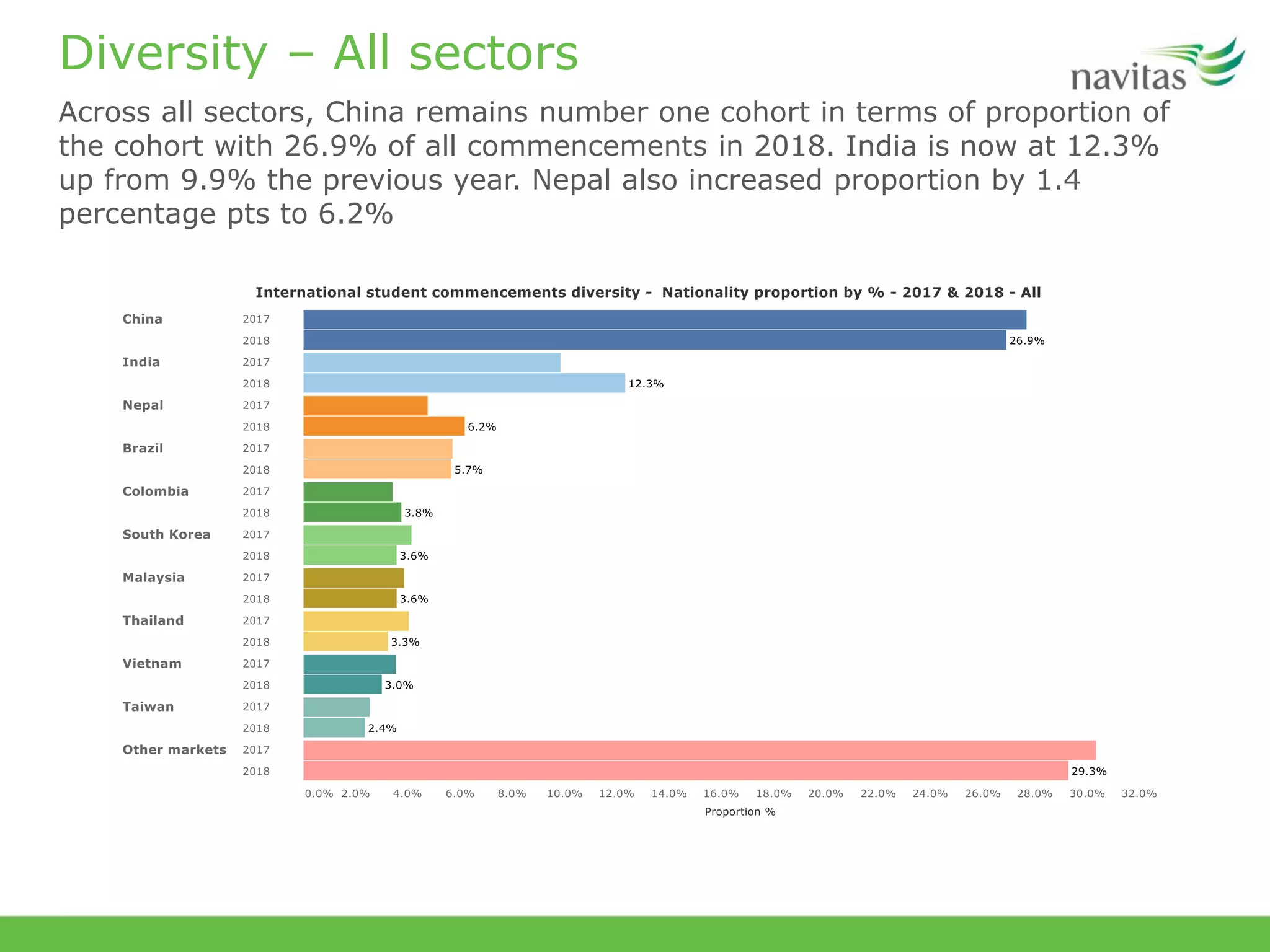

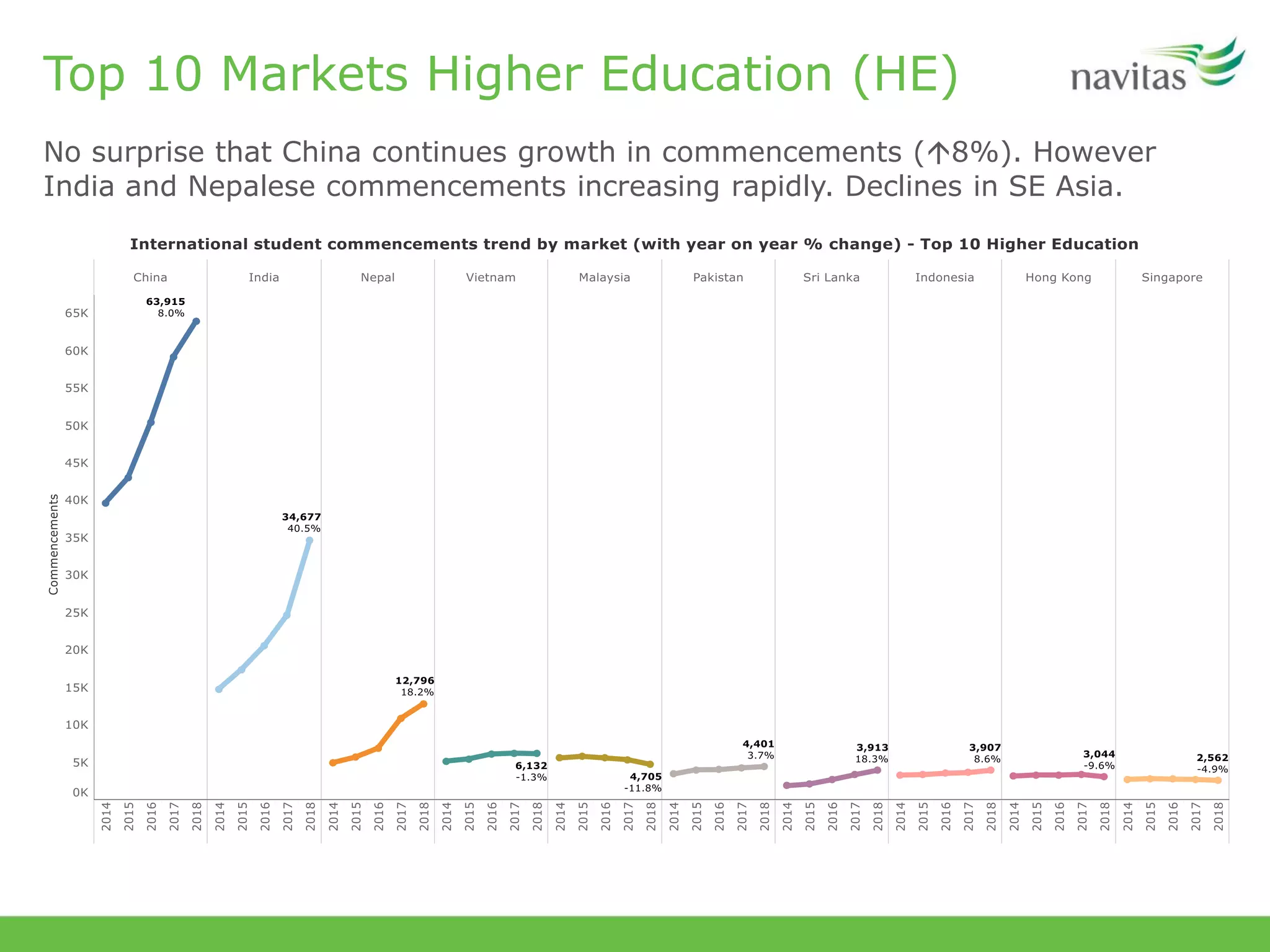

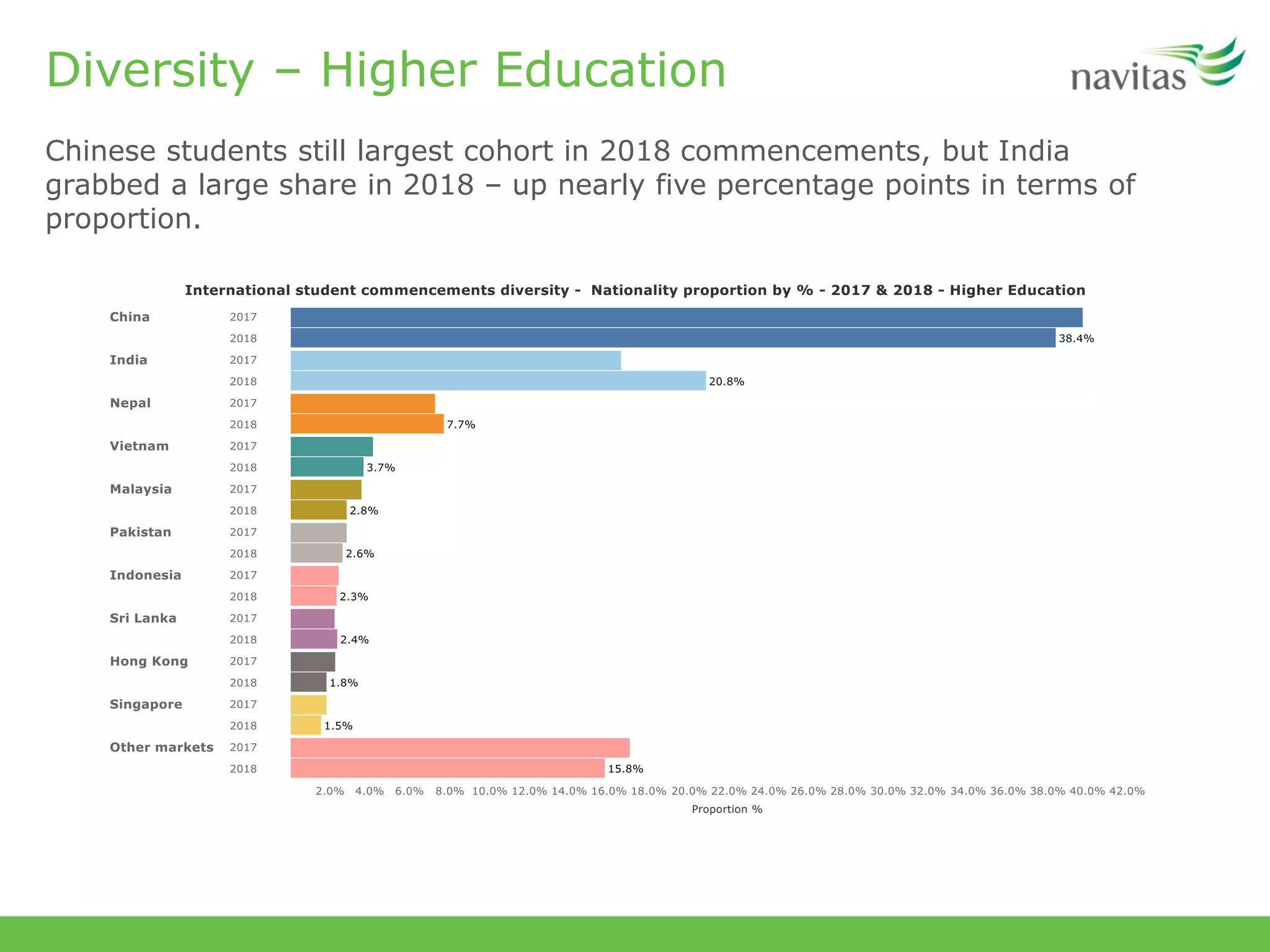

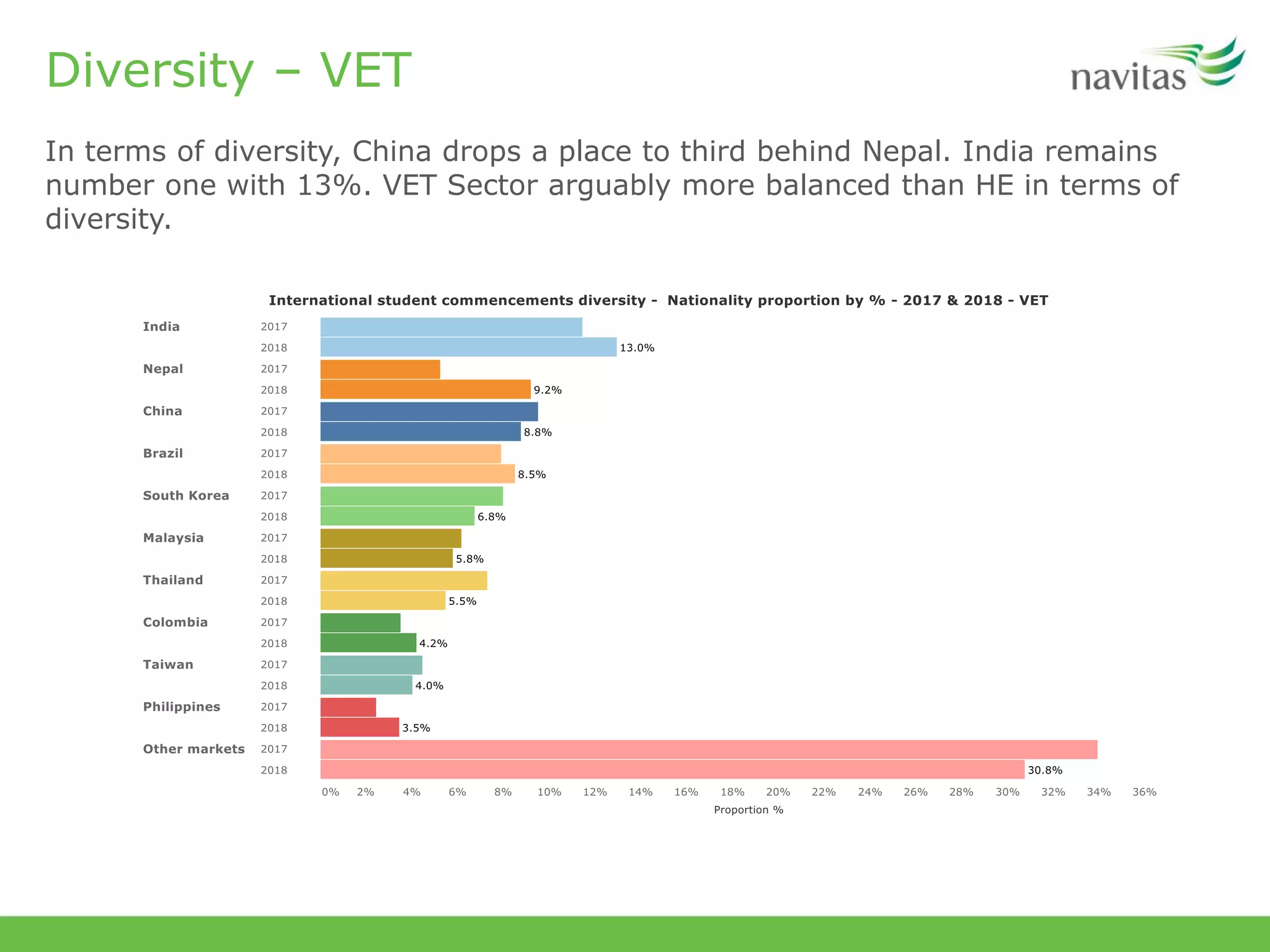

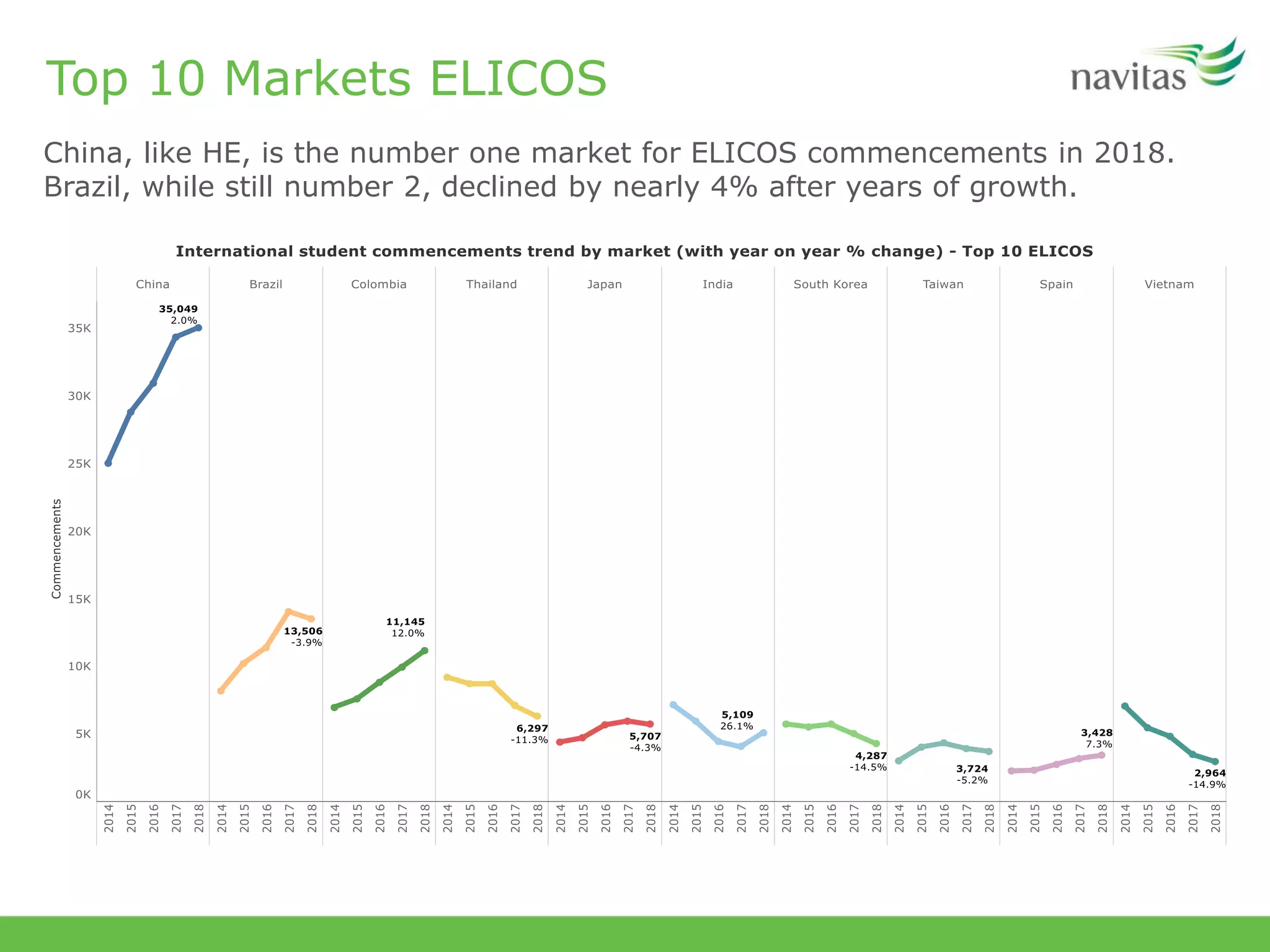

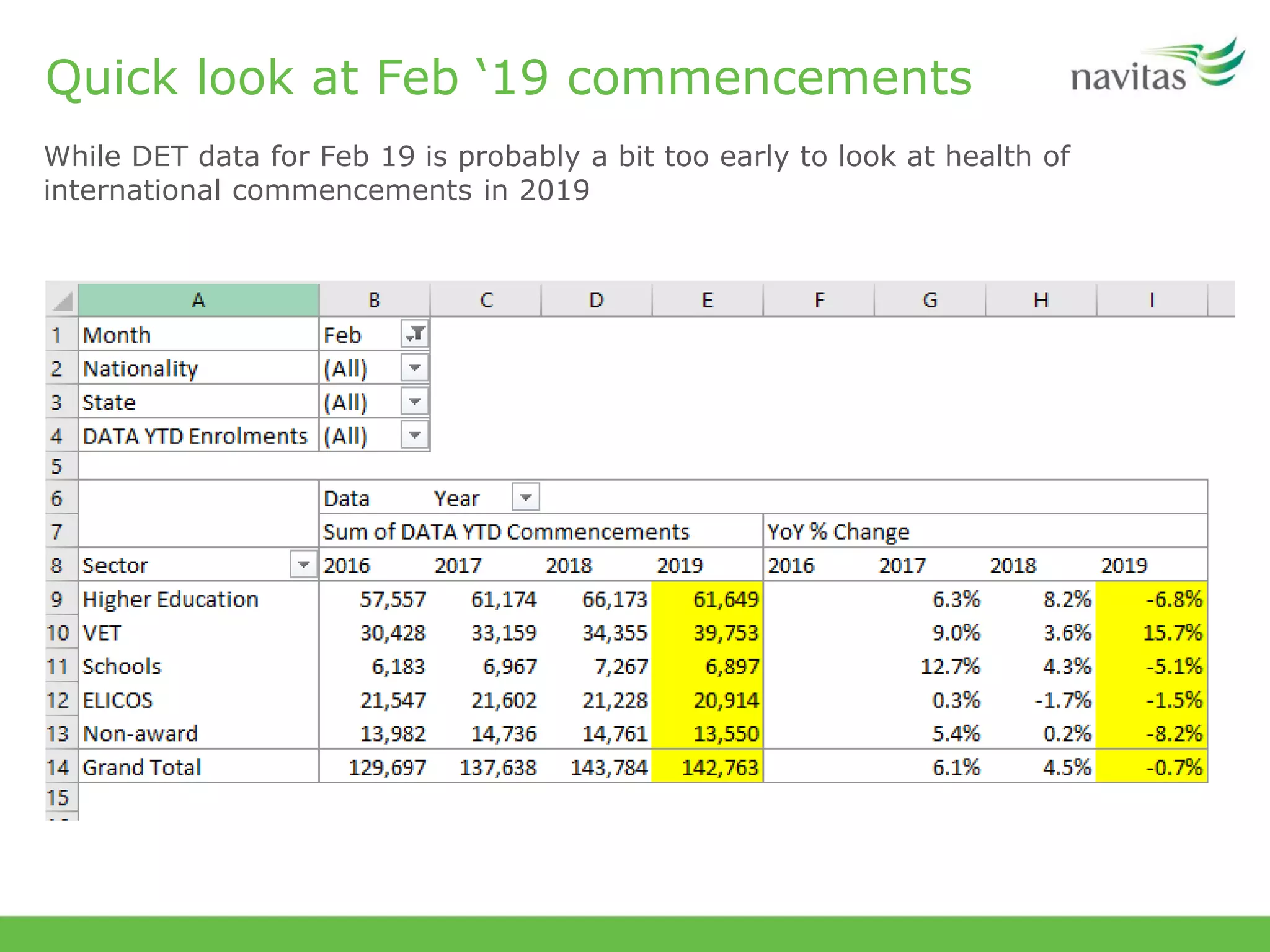

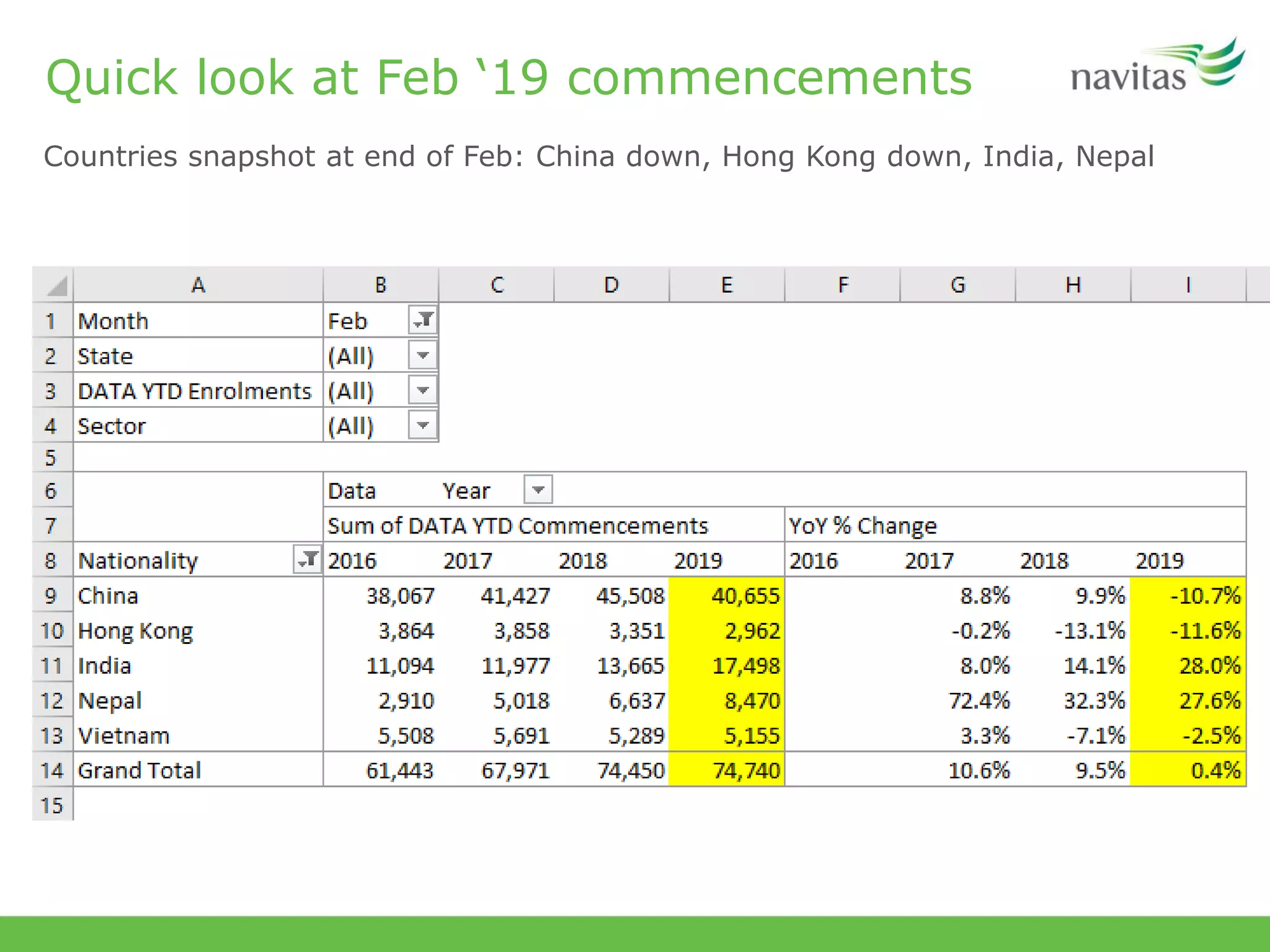

The document analyzes lead indicators in visa lodgement and grant data for international students, noting a year-on-year growth in visa lodgements by 16.9% and grants by 10.2%. While the higher education and vocational education and training sectors showed significant growth, the schools sector continued to decline. Market trends indicate a shift in origin countries, with a decline in Chinese grants but significant increases from India and Nepal.