Download to read offline

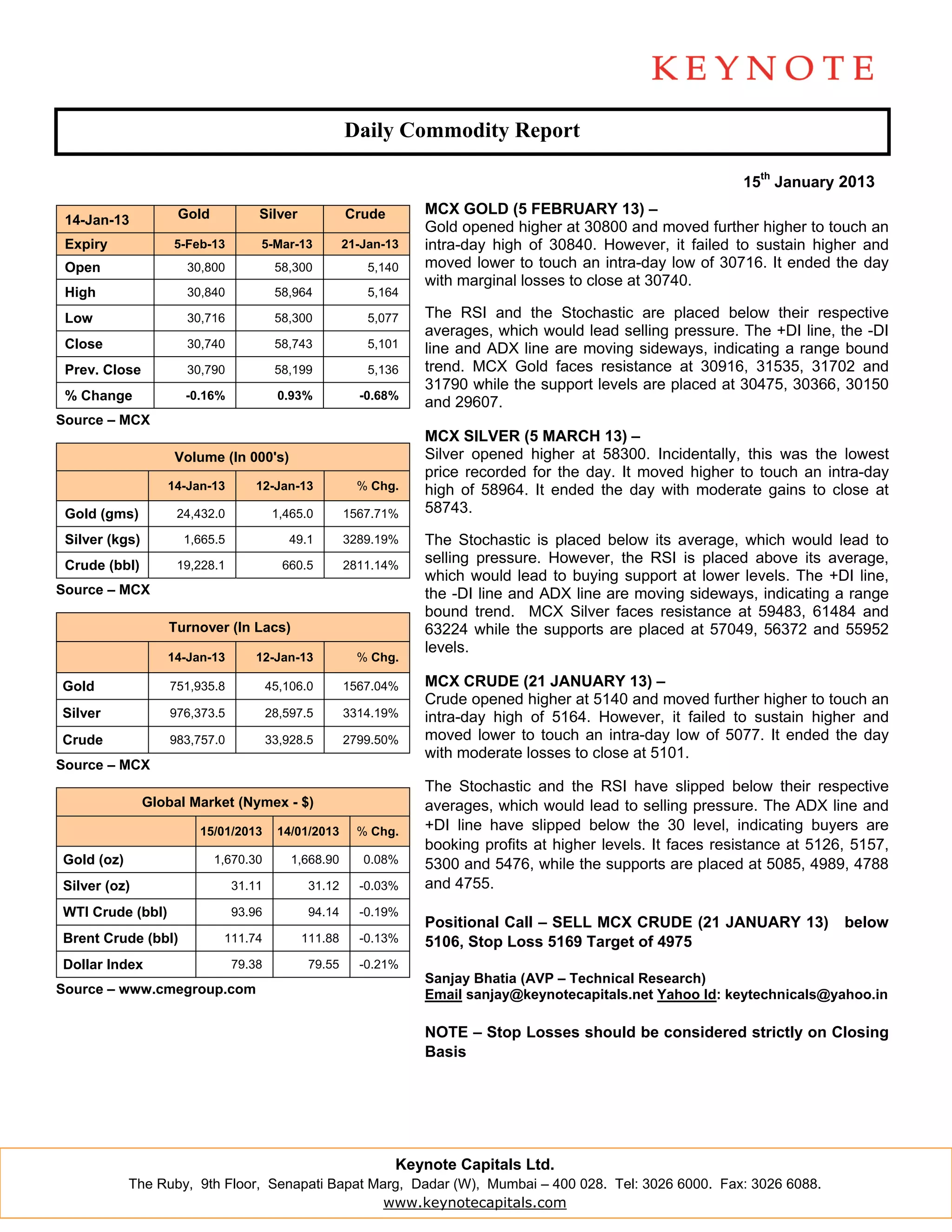

- Gold, silver, and crude oil prices moved higher today before closing with marginal losses or gains. - The technical indicators show most commodities are in a range-bound trend. Resistance and support levels are provided. - A sell recommendation is given for MCX crude oil based on technical analysis. - Economic data releases are listed for the coming days from India, US, UK, Eurozone, and China that may impact commodity prices.