Downloaded 252 times

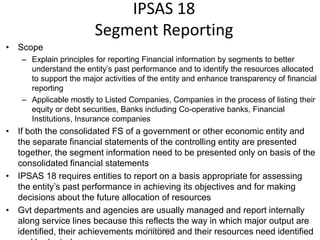

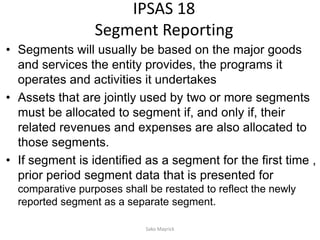

This document provides a summary of IPSAS 18 on segment reporting. Some key points: - IPSAS 18 requires entities to report financial information by segments to improve understanding of past performance and resources allocated to major activities. - Segments will usually be based on major goods/services, programs, and activities. Commonly used segments include departments, agencies, and service lines. - Assets jointly used by segments must be allocated if related revenues and expenses are also allocated. Comparative segment data must be restated if a new segment is identified. - The summary also briefly outlines IPSAS 19 on provisions, contingent liabilities, and contingent assets and the criteria for recognition of each.