Download as PDF, PPTX

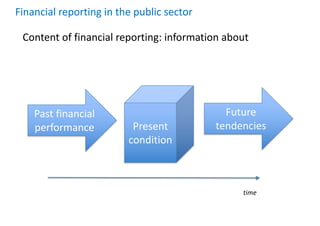

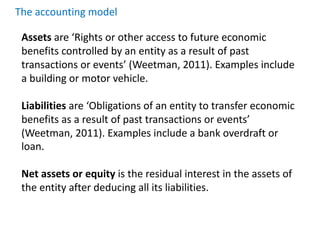

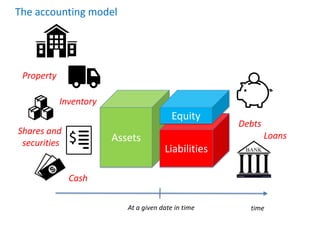

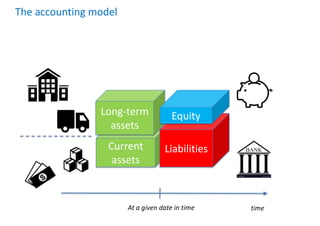

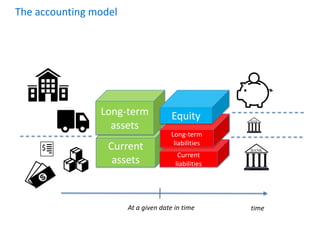

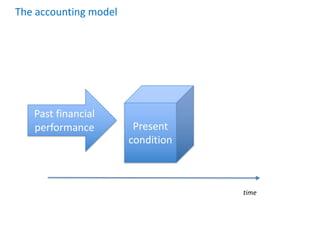

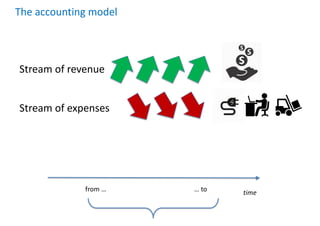

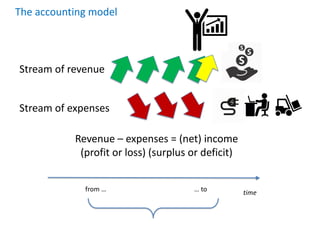

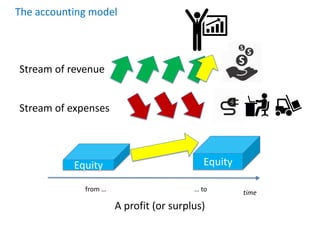

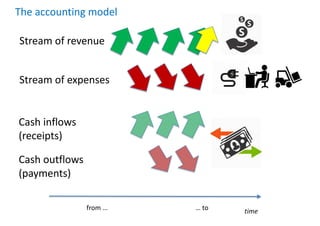

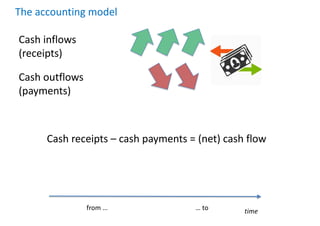

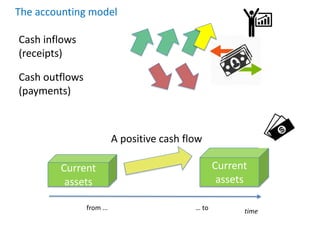

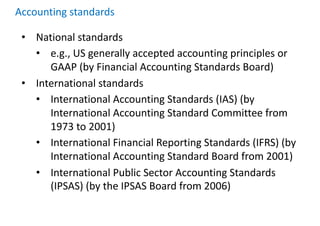

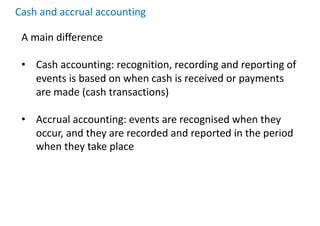

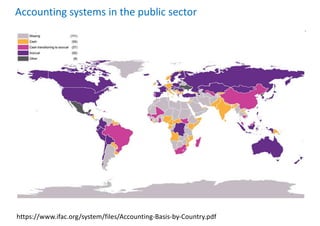

This document discusses accounting in the public sector. It covers topics such as financial reporting, managing revenue and expenditures, accounting standards, and accounting systems. Specifically, it discusses: - The content of financial reporting in the public sector, which provides information about the present condition, past financial performance, and future tendencies. - The accounting model, which shows assets, liabilities, and equity over time and how revenue, expenses, and cash flows impact these categories. - The main accounting standards used in public sector accounting, including national standards like GAAP and international standards like IPSAS. - The key difference between cash accounting, which recognizes events based on cash transactions, and accrual accounting, which recognizes events