Downloaded 14 times

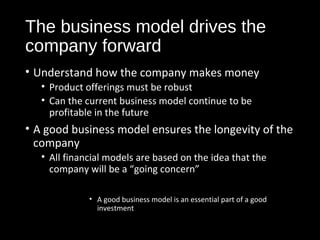

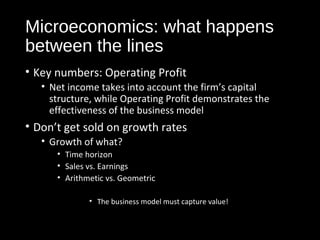

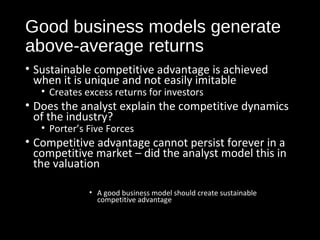

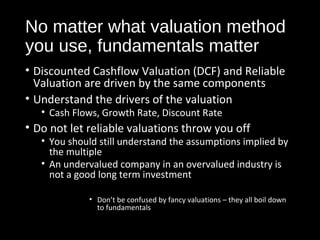

The document discusses important aspects to consider when evaluating a company valuation. It emphasizes the need to consider both qualitative and quantitative factors, including understanding the business model, underlying economics, competitive advantage, and financial assumptions. A good valuation analyzes the company's ability to generate sustainable competitive advantages and profits through a robust business model, supported by realistic financial projections and assumptions.

![Innovation And Creativity 131[1]](https://cdn.slidesharecdn.com/ss_thumbnails/innovationandcreativity1311-091021125330-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)