Downloaded 89 times

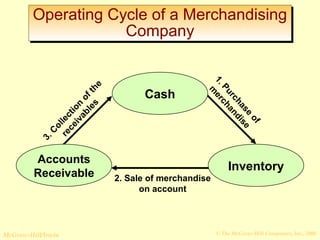

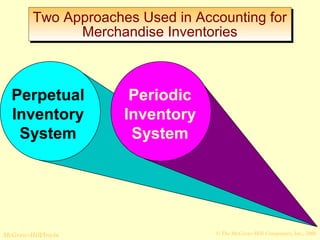

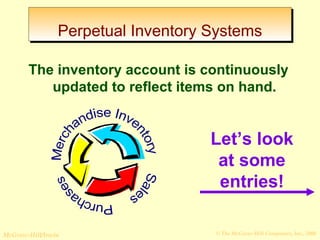

This document discusses accounting for merchandising companies. It describes the operating cycle of merchandising companies, which involves purchasing inventory, selling inventory on credit, and collecting accounts receivable. The document also discusses the income statement and accounting systems used by merchandising companies, including perpetual and periodic inventory systems. It provides examples of journal entries under each system.