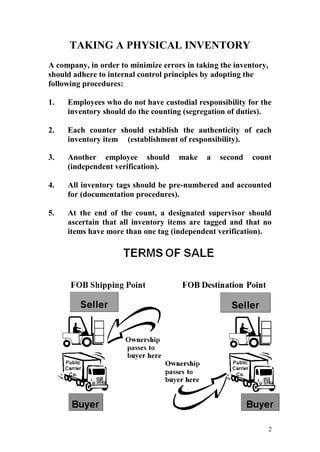

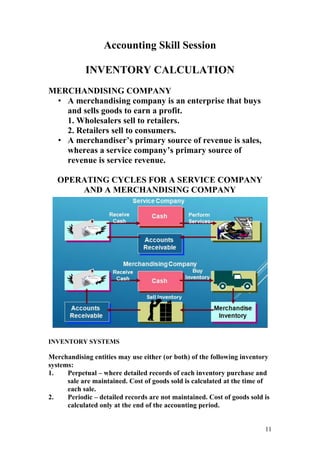

The document discusses inventory costing methods for merchandising companies. It covers topics such as taking a physical inventory, determining inventory quantities, cost flow assumptions under FIFO and average costing, and the effects of inventory errors on financial statements. Proper internal controls over physical inventory counts include segregating inventory custody and counting duties and verifying counts through independent verification.