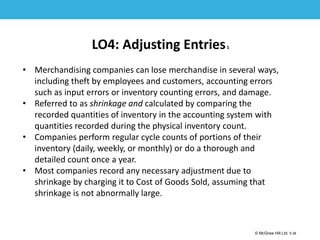

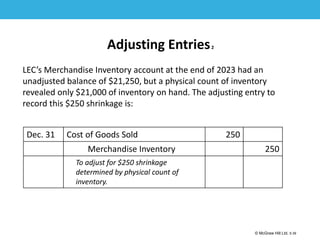

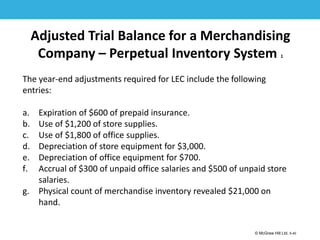

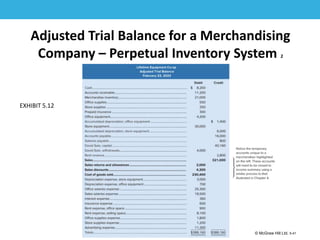

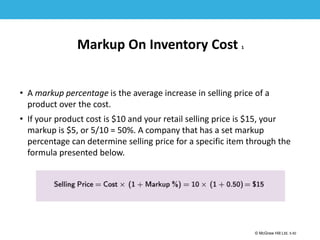

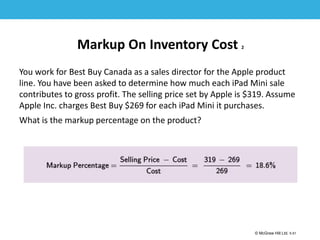

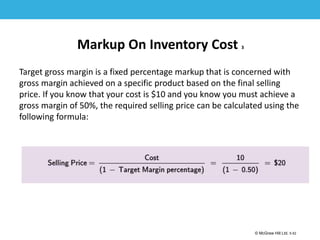

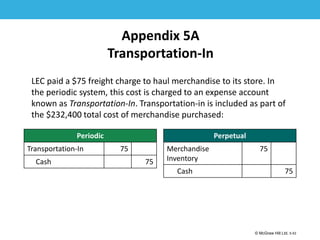

This document outlines accounting concepts and procedures related to merchandising activities, including perpetual and periodic inventory systems. It discusses key income statement and balance sheet components for merchandising companies and how to record purchases and sales of merchandise under the perpetual inventory system. The document contains learning objectives, definitions, journal entries, exhibits, and tips for areas like inventory valuation, purchase discounts, sales returns and allowances, and cost of goods sold.

![1-21

© McGraw Hill Ltd. 5-21

© McGraw-Hill Education. All rights reserved. Authorized only for instructor use in the classroom. No

reproduction or further distribution permitted without the prior written consent of McGraw-Hill

Education.

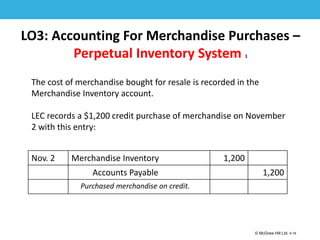

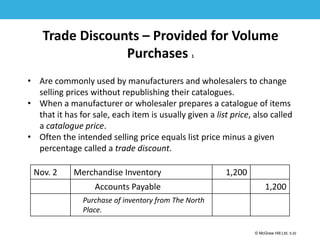

Trade Discounts – Provided for Volume

Purchases 2

On November 2, LEC purchased clothing for resale from The North

Place that was listed at $2,000 in the catalogue. Since LEC receives a

40% trade discount, the company records the transaction at $1,200 [=

$2,000 – (40% × $2,000)].

Nov. 2 Merchandise Inventory 1,200

Accounts Payable 1,200

Purchase of inventory from The North

Place.](https://image.slidesharecdn.com/larson17cepptv1ch052-240111231233-fade93d6/85/Aaccounting-for-merchandising-activities-21-320.jpg)