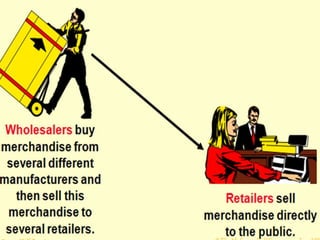

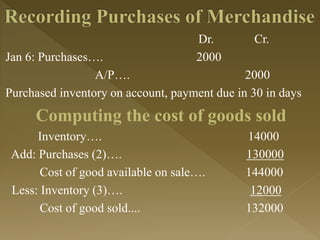

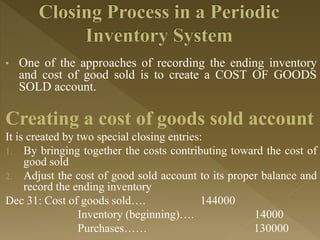

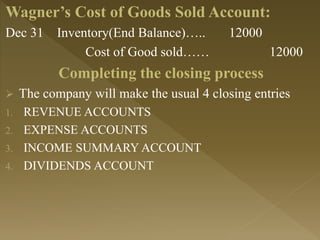

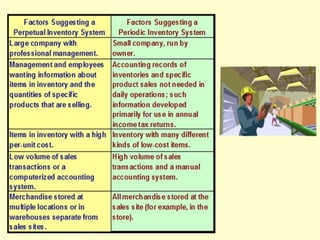

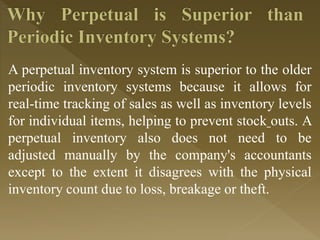

The document provides an overview of merchandising companies, detailing the distinctions between retailers and wholesalers, as well as their purchasing practices. It explains the perpetual and periodic inventory systems, outlining how inventory transactions are recorded and how cost of goods sold is calculated. Additionally, it discusses the impact of sales returns, allowances, and discounts on revenue and presents the importance of proper inventory management for effective business operations.