Downloaded 11 times

![Legislative Framework

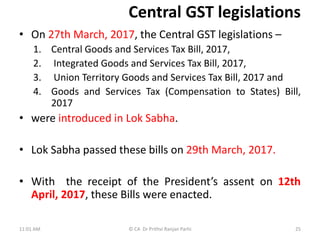

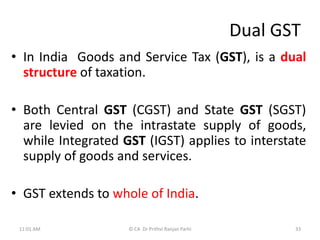

• There is single legislation – CGST Act, 2017 - for levying

CGST.

•

• Union Territories without State legislatures are governed by

UTGST Act, 2017 for levying UTGST.

• States and Union territories with their own legislatures [Delhi

and Puducherry] have their own GST legislation for levying

SGST.

• Though there are multiple SGST legislations, the basic features

of law, such as chargeability, definition of taxable event and

taxable person, classification and valuation of goods and

services, procedure for collection and levy of tax and the like

are uniform in all the SGST legislations, as far as feasible.

• This is necessary to preserve the essence of dual GST.

11:01 AM 35

© CA Dr Prithvi Ranjan Parhi](https://image.slidesharecdn.com/introductiontogst-210928110141/85/Introduction-to-GST-35-320.jpg)

This document provides an introduction to Goods and Services Tax (GST) in India. It begins with definitions of direct and indirect taxes, explaining that GST is an indirect tax that is destination-based and replaces existing indirect taxes. It then discusses the genesis of GST in India and the framework of the dual GST model consisting of CGST, SGST, IGST and cess. Key features of GST like tax credit set-off, value-added taxation, and it being a destination-based tax are also highlighted.