Seamless flow of credit under gst

•Download as PPSX, PDF•

1 like•935 views

This document discusses key aspects of the Goods and Services Tax (GST) implemented in India, including: 1. GST is levied on intra-state and inter-state supply of goods and services, except for alcoholic liquor, petroleum products, and real estate. 2. Under GST, tax credits can be utilized across state borders to avoid double taxation, ensuring a seamless flow of credits. 3. The document provides examples to illustrate how tax credits flow between suppliers and purchasers within and across states.

Recommended

More Related Content

What's hot

What's hot (20)

Similar to Seamless flow of credit under gst

Similar to Seamless flow of credit under gst (20)

More from CA Dr. Prithvi Ranjan Parhi

More from CA Dr. Prithvi Ranjan Parhi (20)

Recently uploaded

Recently uploaded (20)

Seamless flow of credit under gst

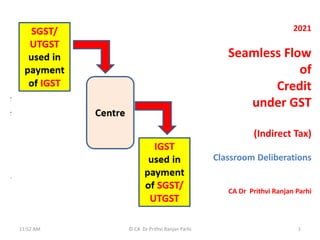

- 1. 2021 Seamless Flow of Credit under GST (Indirect Tax) Classroom Deliberations CA Dr Prithvi Ranjan Parhi 11:52 AM © CA Dr Prithvi Ranjan Parhi 1

- 2. Understanding CGST, SGST, UTGST & IGST 11:52 AM 2 © CA Dr Prithvi Ranjan Parhi Foreign Territory State 1 State 2 Union Territory IGST IGST IGST IGST CGST +SGST CGST +SGST CGST +UTGST

- 3. ITC Utilisation Input Tax Credit Tax Liability 11:52 AM © CA Dr Prithvi Ranjan Parhi 3 IGST CGST SGST IGST CGST SGST

- 4. Input Tax Credit CGST IGST First to pay CGST Second to pay IGST Not allowed to SGST First to pay SGST Second to pay IGST Not allowed to CGST First to pay IGST Second to pay CGST Third to pay SGST SGST 11:52 AM 4 © CA Dr Prithvi Ranjan Parhi To be utilised First Only after exhausting CGST ITC

- 5. Seamless flow of credit Since GST is a destination based consumption tax, revenue of SGST ordinarily accrues to the consuming States. 11:52 AM © CA Dr Prithvi Ranjan Parhi 5 IGST CGST SGST IGST IGST CGST SGST The inter-State supplier in the exporting State is allowed to set off the available credit of IGST, CGST and SGST/UTGST (in that order) against the IGST payable on inter-State supply made by him. The buyer in the importing State is allowed to avail the credit of IGST paid on inter-State purchases made by him. Under GST regime there is a seamless credit flow in case of inter- State supplies too. Interstate Supply Interstate/ Intrastate Supply

- 6. Seamless flow of credit The revenue of inter-State sale does not accrue to the exporting State. The exporting State transfers to the Centre the credit of SGST/UTGST used in payment of IGST. The Centre transfers to the importing State the credit of IGST used in payment of SGST/UTGST. Credit chain does not break. 11:52 AM © CA Dr Prithvi Ranjan Parhi 6 SGST/ UTGST used in payment of IGST IGST used in payment of SGST/ UTGST Centre This ensures seamless flow of credit under GST, in case of intra-State and inter-State supplies .

- 7. I. Illustration :Intra-State Supply • In case of local supply of goods/ services, the supplier would charge dual GST i.e., CGST and SGST at specified rates on the supply. I. Supply of goods/ services by A to B The CGST & SGST charged on B for supply of goods/services will be remitted by A to the appropriate account of the Central and State Government respectively. A is the first stage supplier of goods/services and hence, does not have credit of CGST, SGST or IGST. ©CA.Dr.Prithvi Ranjan Parhi Amount (in Rs.) Value charged for supply of goods/ services 10,000 Add: CGST @ 9% 900 Add: SGST @ 9% 900 Total price charged by A from B for local supply of goods/ services 11,800

- 8. 11:52 AM © CA Dr Prithvi Ranjan Parhi 8

- 9. II. Supply of goods/services by B to C – Value addition @ 20% • B will avail credit of CGST and SGST paid by him on the purchase of goods/ services and will utilize such credit for being set off against the CGST and SGST payable on the supply of goods/services made by him to C. ©CA.Dr.Prithvi Ranjan Parhi Amount (in Rs.) Value charged for supply of goods/ services (Rs. 10,000 x 120%) 12,000 Add: CGST @ 9% 1,080 Add: SGST @ 9% 1,080 Total price charged by B from C for local supply of goods/ services 14,160

- 10. Computation of CGST, SGST payable by B to Govt Note: Rates of CGST and SGST have been assumed to be 9% each for the sake of simplicity. ©CA.Dr.Prithvi Ranjan Parhi Amount (in Rs.) CGST payable 1,080 Less: Credit of CGST 900 CGST payable to Central Government 180 SGST payable 1,080 Less: Credit of SGST 900 SGST payable to State Government 180

- 11. Statement of revenue earned by Central and State Govt ©CA.Dr.Prithvi Ranjan Parhi Transaction Revenue to Central Government (Rs.) Revenue to State Government (Rs.) Supply of goods/services by A to B 900 900 Supply of goods/services by B to C 180 180 Total 1,080 1,080

- 12. 2. Illustration :Inter-State Supply • In case of inter-State supply of goods/ services, the supplier would charge IGST at specified rates on the supply. I. Supply of goods/services by X of State Odisha to A of State Odisha X is the first stage supplier of goods/services and hence, does not have any credit of CGST, SGST or IGST. ©CA.Dr.Prithvi Ranjan Parhi Amount (in Rs.) Value charged for supply of goods/services 10,000 Add: CGST @ 9% 900 Add: SGST @ 9% 900 Total price charged by X from A for intra- State supply of goods/services 11,800

- 13. II. Supply of goods/services by A of State Odisha to B of State AP – Value addition @ 20% ©CA.Dr.Prithvi Ranjan Parhi Amount (in Rs.) Value charged for supply of goods/services (Rs. 10,000 x 120%) 12,000 Add: IGST @ 18% 2,160 Total price charged by A from B for inter- State supply of goods/services 14,160

- 14. Computation of IGST payable to Government • The IGST charged on B of State AP for supply of goods/services will be remitted by A of State Odisha to the appropriate account of the Central Government. • State Odisha (Exporting State) will transfer SGST credit of Rs. 900 utilised in the payment of IGST to the Central Government. ©CA.Dr.Prithvi Ranjan Parhi Amount (in Rs.) IGST payable 2,160 Less: Credit of CGST 900 Less: Credit of SGST 900 IGST payable to Central Government 360

- 15. III. Supply of goods/services by B of State AP to C of State AP – Value addition @ 20% • B will avail credit of IGST paid by him on the purchase of goods/services and will utilize such credit for being set off against the CGST and SGST payable on the local supply of goods/services made by him to C. ©CA.Dr.Prithvi Ranjan Parhi Amount (in Rs.) Value charged for supply of goods/ services (Rs.12,000 x 120%) 14,400 Add: CGST @ 9% 1,296 Add: SGST @ 9% 1,296 Total price charged by B from C for local supply of goods/services 16,992

- 16. Computation of CGST, SGST payable to Government • Central Government will transfer IGST credit of Rs. 864 utilised in the payment of SGST to State AP (Importing State). Note: Rates of CGST, SGST and IGST have been assumed to be 9%, 9% and 18% respectively for the sake of simplicity. ©CA.Dr.Prithvi Ranjan Parhi Amount (in Rs.) CGST payable 1,296 Less: Credit of IGST 1,296 CGST payable to Central Government Nil SGST payable 1,296 Less: Credit of IGST (Rs.2,160 – Rs.1,296) 864 SGST payable to State Government 432

- 17. Statement of revenue earned by Central and State Governments ©CA.Dr.Prithvi Ranjan Parhi Transaction Revenue to Central Government (Rs.) Revenue to Government of State Odisha (Rs.) Revenue to Government of State AP (Rs.) Supply of goods/services by X to A 900 900 Supply of goods/services by A of Odisha to B of AP 360 Transfer by State Odisha to Centre 900 (900) Supply of goods/services by B to C 432 Transfer by Centre to State AP (864) 864 Total 1,296 Nil 1,296

- 18. Registration – Every supplier of goods and/or services is required to obtain registration in the State/UT from where he makes the taxable supply if his aggregate turnover exceeds the threshold limit during a FY. **persons engaged exclusively in intra-State supply of goods ©CA.Dr.Prithvi Ranjan Parhi States with threshold limit of Rs.10 lakh for both goods and services States with threshold limit of Rs.20 lakh for both goods and services States with threshold limit of Rs.20 lakh for services and Rs.40 lakh for goods** •Manipur •Mizoram •Nagaland •Tripura •Arunachal Pradesh •Meghalaya •Sikkim •Uttarakhand •Puducherry •Telangana •Jammu and Kashmir •Assam •Himachal Pradesh •All other state

- 19. UIN • Unique Identification Number, UIN, is a special class of GST registration for foreign diplomatic missions and embassies which are not liable to taxes in the Indian territory. • Any amount of tax (direct or indirect) collected from such bodies is refunded back to them. Who can apply for UIN under GST? 1. A specialized agency of the United Nations Organization 2. A Multilateral Financial Institution and Organization notified under the United Nations (Privileges and Immunities) Act, 1947, 3. Consulate or Embassy of foreign countries 4. Any other person or class of persons as notified by the Commissioner 11:52 AM 19 © CA Dr Prithvi Ranjan Parhi

- 20. Alcoholic liquor for human consumption: GST is levied on all goods and services, except – alcoholic liquor for human consumption and – petroleum crude, diesel, petrol, ATF and natural gas. Alcoholic liquor for human consumption: is outside the realm of GST. The manufacture/production of alcoholic liquor continues to be subjected to State excise duty and inter-State/intra-State sale of the same is subject to CST/VAT respectively. ©CA.Dr.Prithvi Ranjan Parhi

- 21. Petroleum crude, diesel, petrol, ATF and natural gas: As regards petroleum crude, diesel, petrol, ATF and natural gas are concerned, they are not presently leviable to GST. GST will be levied on these products from a date to be notified on the recommendations of the GST Council. Till such date, central excise duty continues to be levied on manufacture/production of petroleum crude, diesel, petrol, ATF and natural gas and inter-State/intra-State sale of the same is subject to CST/ VAT respectively. ©CA.Dr.Prithvi Ranjan Parhi Petroleu m crude High speed diesel Motor spirit(co mmonly known as petrol) Natural gas Aviation Turbine fuel

- 22. Tobacco: Tobacco is within the purview of GST, i.e. GST is leviable on tobacco. Union Government has also retained the power to levy excise duties on tobacco and tobacco products manufactured in India. Resultantly, tobacco is subject to GST as well as central excise duty. ©CA.Dr.Prithvi Ranjan Parhi

- 23. Real estate sector • GST is not applicable on ready-to-move (RTM) properties for which completion certificates are issued. • Because Sale of building is treated as activity or transaction which shall be treated neither as a supply of good nor a supply of service as per SCHEDULE III of CGST Act,2017 • GST is also not applicable on resale of properties, on Land purchase and sale. • GST applies to residential apartments in Real Estate Project (REP) and Residential Real Estate Project (RREP) and commercial apartments in RREP which are covered under RERA [Real Estate (Regulation and Development) Act, 2016]. • However GST is applicable on supply of Under Construction Properties , works contracts etc. 11:52 AM © CA Dr Prithvi Ranjan Parhi 23

- 24. PAN Alphabet ‘Z’ by default Check digit State Code 11:52 AM 24 © CA Dr Prithvi Ranjan Parhi

- 25. Exemption from tax : Sec 11 (1) (1)Where the Government is satisfied that it is necessary in the public interest so to do, it may, on the recommendations of the Council, by notification, exempt generally, – either absolutely or – subject to such conditions as may be specified therein, • goods or services or both of any specified description from the whole or any part of the tax leviable thereon with effect from such date as may be specified in such notification. 11:52 AM 25 © CA Dr Prithvi Ranjan Parhi

- 26. GST Common Portal • Managed by GSTN which is a Section 8 Company. • Accessible over internet • Services provided – Registration – Payment & Refund – Return 11:52 AM 26 © CA Dr Prithvi Ranjan Parhi

- 27. 11:52 AM 27 © CA Dr Prithvi Ranjan Parhi

- 28. E- waybill Portal 11:52 AM 28 © CA Dr Prithvi Ranjan Parhi

- 29. www.ewaybillgst.gov.in • However, it is important to note that the Common GST Electronic Portal for furnishing electronic way bill is www.ewaybillgst.gov.in . • Managed by the National Informatics Centre, Ministry of Electronics & Information Technology, Government of India. • E-way bill is an electronic document generated on the GST portal evidencing movement of goods. 11:52 AM 29 © CA Dr Prithvi Ranjan Parhi

- 30. 11:52 AM © CA Dr Prithvi Ranjan Parhi 30

- 31. e-Way Bill • e-Way Bill is mandatory for Inter-State movement of goods of consignment value exceeding Rs.50,000/- in motorized conveyance. • Registered GST Taxpayers can register in the e-Way Bill Portal using GSTIN. • Unregistered Persons/ Transporters can enroll in the e- Way Bill System by providing their PAN and Aadhaar. • Supplier/ Recipient/ Transporter can generate the e-Way Bill. 11:52 AM © CA Dr Prithvi Ranjan Parhi 31

- 32. 11:52 AM © CA Dr Prithvi Ranjan Parhi 32

- 33. Goods • In terms of Section 2 (52) of the CGST Act “Goods” means every kind of movable property other than money and securities • but includes actionable claims, growing crops, grass and other things attached to or forming part of land which are agreed to be severed before supply or under a contract of supply. • Article 366(12) in The Constitution Of India • Goods includes all materials, commodities, and articles; 11:52 AM © CA Dr Prithvi Ranjan Parhi 33

- 34. Services • In terms of Section 2(102) of the CGST Act “Services” means anything other than goods, money and securities but • includes activity relating to the use of money or its conversion by cash or by any other mode, from one form, currency or denomination, to another form, currency or denomination for which a separate consideration is charged. • Article 366(26A): • Services means anything other than goods. 11:52 AM © CA Dr Prithvi Ranjan Parhi 34

- 35. All Supply • Thus, all supply of goods or services or both would attract CGST (to be levied by Centre) and SGST (to be levied by State) unless kept out of the purview of GST. 11:52 AM © CA Dr Prithvi Ranjan Parhi 35

- 36. Supply • There is no requirement of actual sale of goods under GST. • The alternative methods of supply of goods could be in the form of: • stock transfer; • captive consumption in another location; • supply on consignment basis or any other basis by the principal to his agent; • supply on job work basis (if working under returnable basis- no tax need be paid); • any other supply such as donation, sample etc. 11:52 AM © CA Dr Prithvi Ranjan Parhi 36

- 37. GSTC • (2) The Goods and Services Tax Council (GSTC) shall consist of the following members, namely:— – (a) Chairperson- Union Finance Minister; – (b) Member From Central Govt- Union Minister of State in charge of Revenue or Finance; – (c) Members from State Govt – Minister in charge of Finance or Taxation or any other Minister nominated by each State Government. • (3) The Members of the Goods and Services Tax Council (GSTC) referred to in sub-clause (c) of clause (2) shall, as soon as may be, choose one amongst themselves to be the Vice-Chairperson of the Council for such period as they may decide. (ie Vice Chairperson will be from Member from State Govt) 11:52 AM 37 © CA Dr Prithvi Ranjan Parhi

- 38. GSTC • (4) The Goods and Services Tax Council (GSTC) shall make Recommendations to the Union and the States on— – (a) the taxes, cesses and surcharges levied by the Union, the States and the local bodies which may be subsumed in the goods and services tax; – (b) the goods and services that may be subjected to, or exempted from the goods and services tax; – (c) model Goods and Services Tax Laws, principles of levy, apportionment of Integrated Goods and Services Tax and the principles that govern the place of supply; – (d) the threshold limit of turnover below which goods and services may be exempted from goods and services tax; – (e) the rates including floor rates with bands of goods and services tax; – (f) any special rate or rates for a specified period, to raise additional resources during any natural calamity or disaster; – (g) Special provision with respect to the States of Arunachal Pradesh, Assam, Jammu and Kashmir, Manipur, Meghalaya, Mizoram, Nagaland, Sikkim, Tripura, Himachal Pradesh and Uttarakhand; and – (h) any other matter relating to the goods and services tax, as the Council may decide. 11:52 AM 38 © CA Dr Prithvi Ranjan Parhi

- 39. GSTC • (5) The Goods and Services Tax Council (GSTC) shall recommend the date on which the goods and services tax be levied on petroleum crude, high speed diesel, motor spirit (commonly known as petrol), natural gas and aviation turbine fuel. 11:52 AM 39 © CA Dr Prithvi Ranjan Parhi

- 40. Thank you prithvi.baps@gmail.com 11:52 AM © CA. Dr. Prithvi R Parhi 40

Editor's Notes

- Actionable claim is a claim to any debt, other than a debt secured by mortgage of immovable property or by hypothecation or pledge of moveable property, or to any beneficial interest in moveable property not in possession either actual or constructive, of the claimant, which the civil courts recognize as affording ...