Downloaded 61 times

![Additional Conditions

Stayed in India

At least 2 out of

10 PPYs

730 days (or) more

in the 7 PPYs

Resident in India AND

(This means that the assessee must have satisfied at least one

of the basic condition for 2 years out of 10 PPYs)

Additional conditions [Sec. 6(6)(a)]

To test as to when a resident individual is

ordinary resident in India (or) not

7PPYs = 2016-17 to 2010-11](https://image.slidesharecdn.com/residentialstatus-181003043532/75/Residential-status-7-2048.jpg)

![Ordinary Resident [OR] = Indian income +

Foreign income

Not Ordinary Resident [NOR]= Indian income

+ One particular type of foreign income

(i.e., business in foreign but controlled from India).

Non-Resident [NR]= Indian income only

Scope of income to Residents](https://image.slidesharecdn.com/residentialstatus-181003043532/75/Residential-status-15-2048.jpg)

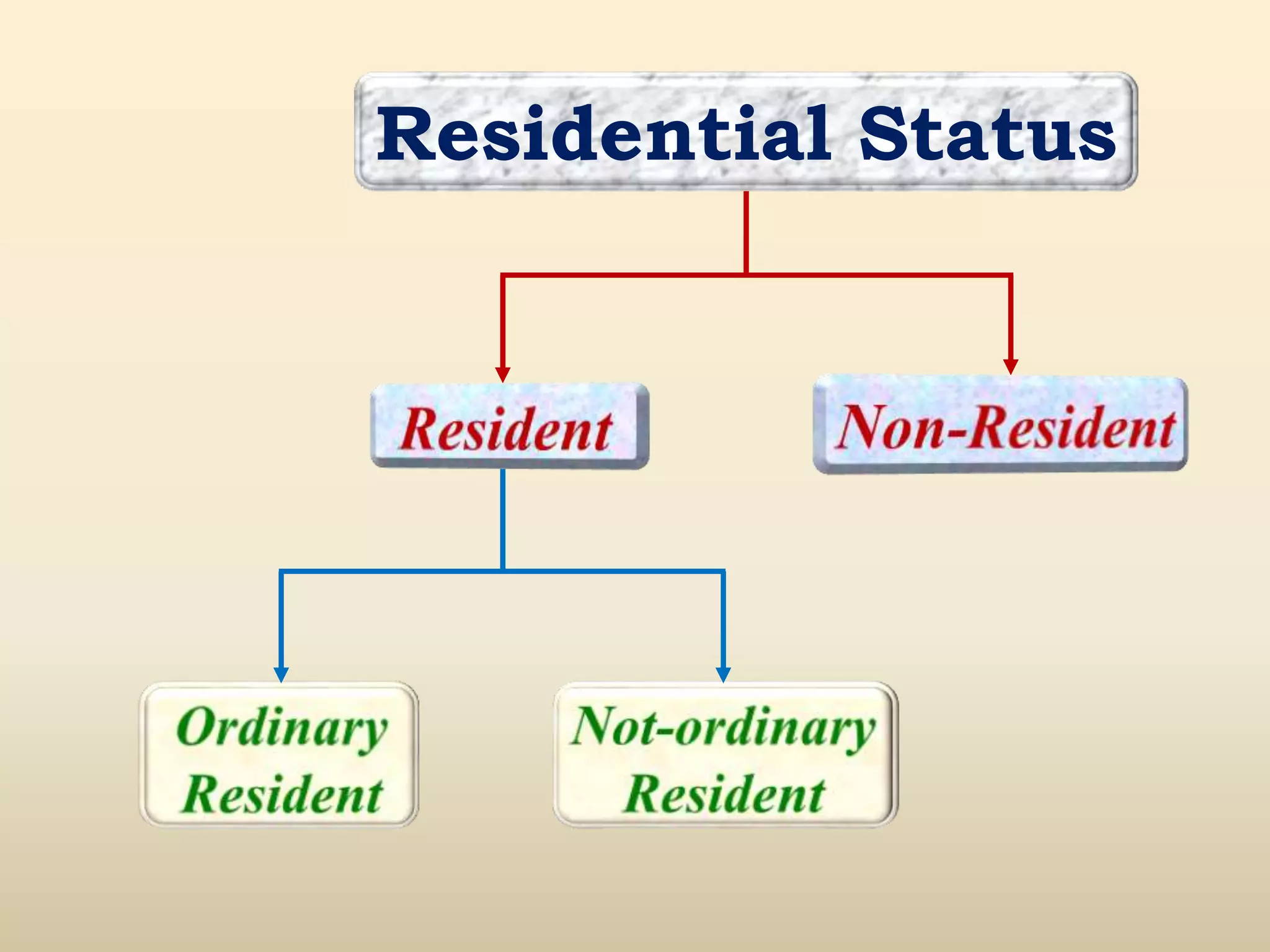

The document discusses the residential status and tax liability of individuals and entities in India. It defines the basic conditions to determine if a person is a resident, ordinary resident, or non-resident based on the number of days spent in India. An ordinary resident's total income and tax liability is the highest, including both Indian and foreign income. A non-resident's total income and tax liability is based only on Indian income. The residential status of entities like HUF, companies, firms, and AOP is also determined based on the control and management of their affairs being within or outside of India.