Downloaded 66 times

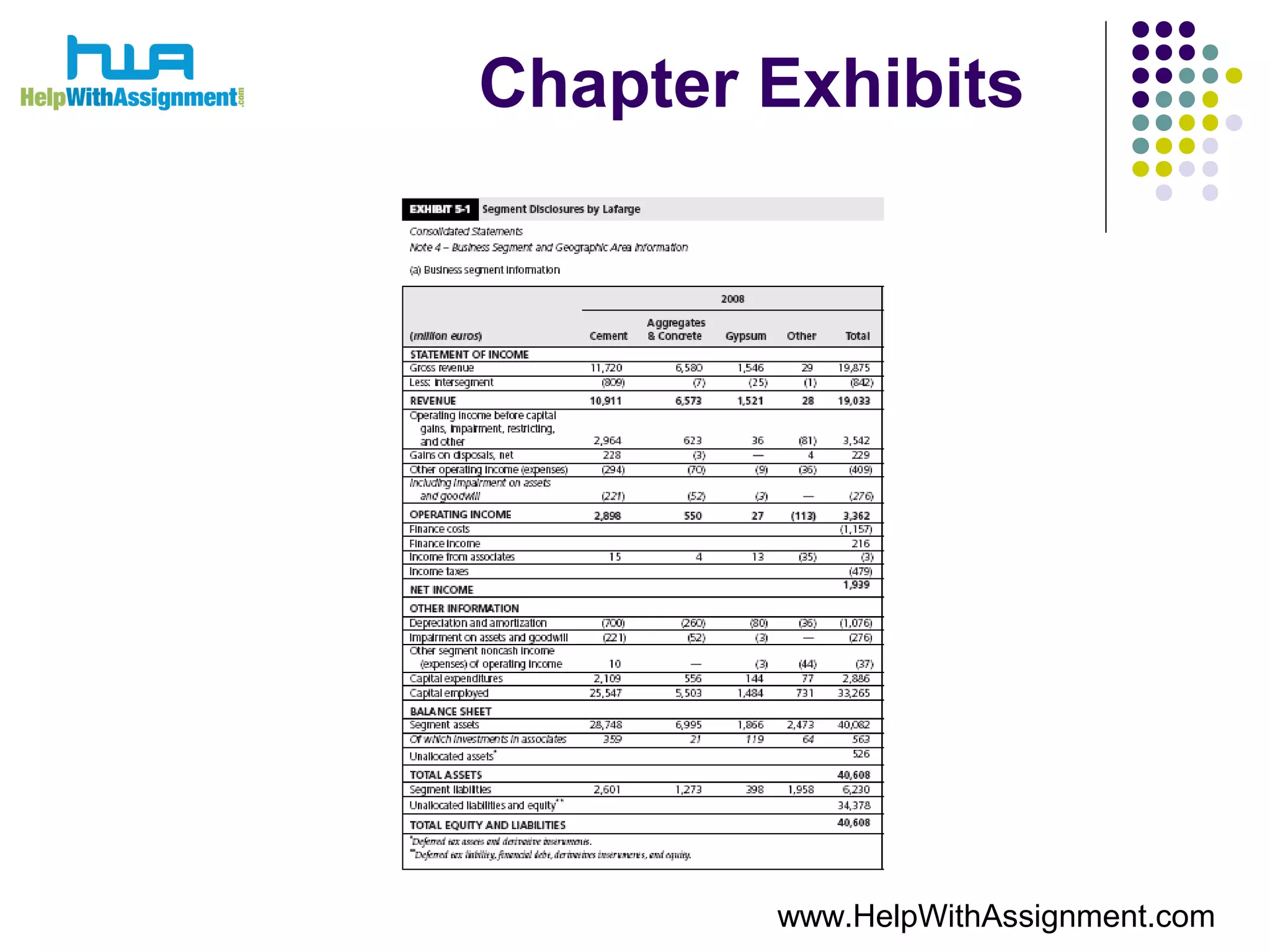

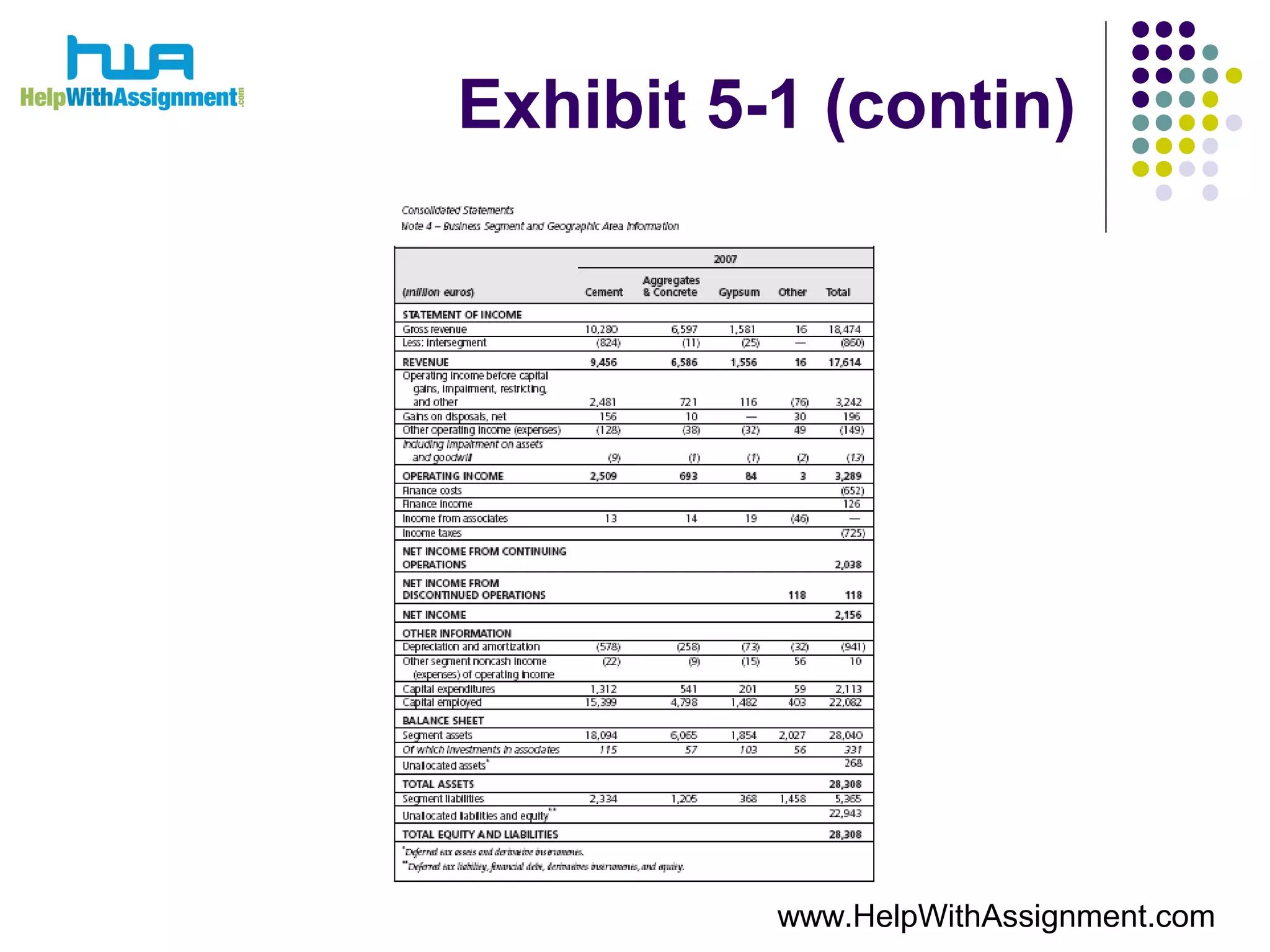

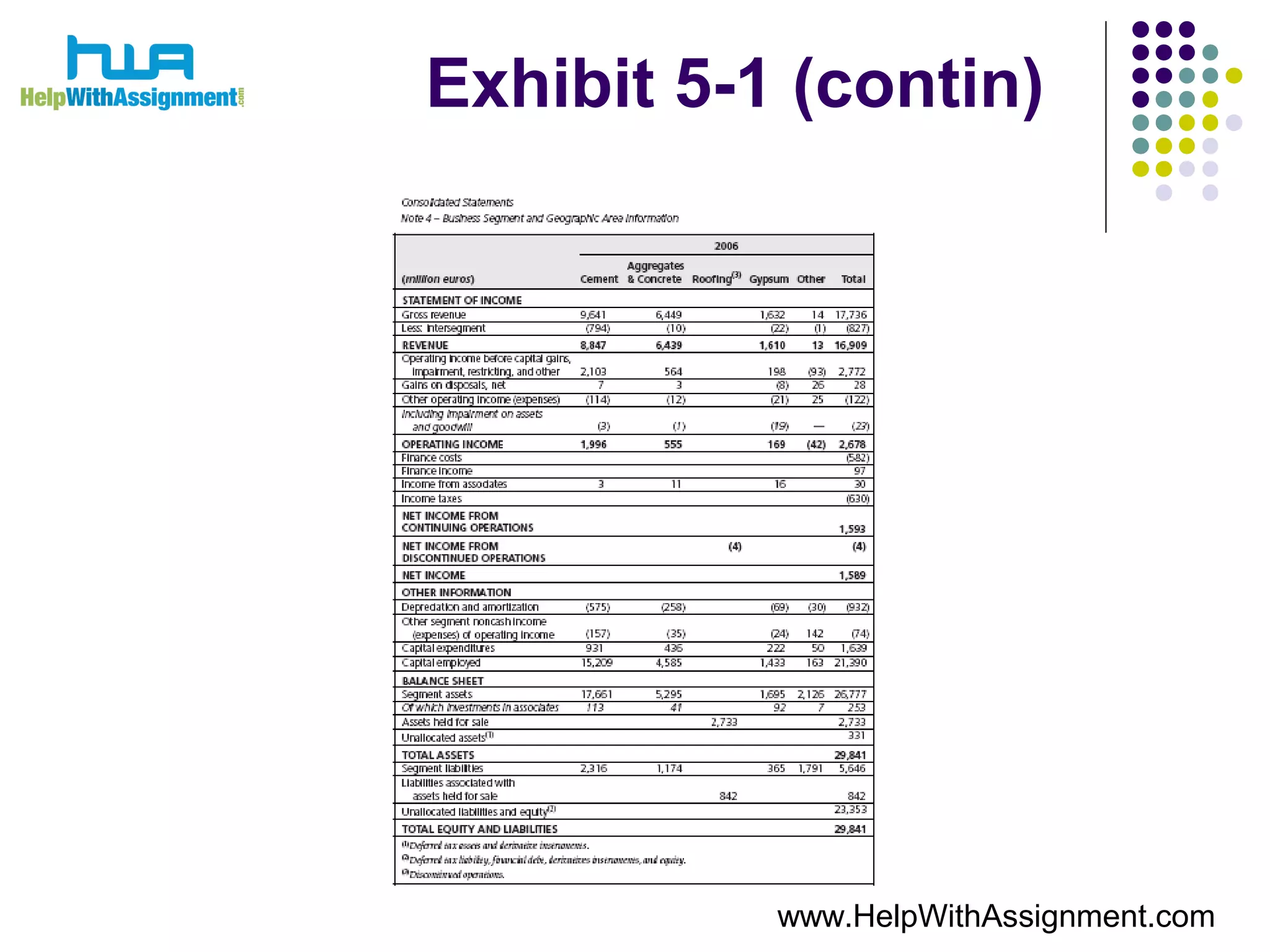

This document outlines key aspects of reporting and disclosure in international accounting, focusing on the distinction between voluntary and mandatory disclosures, and their regulatory measures. It discusses various practices including forward-looking information, segment disclosures, social responsibility reporting, and corporate governance disclosures aimed at enhancing transparency for investors. Furthermore, it highlights the challenges faced by developing countries in terms of disclosure practices compared to developed nations.