Downloaded 393 times

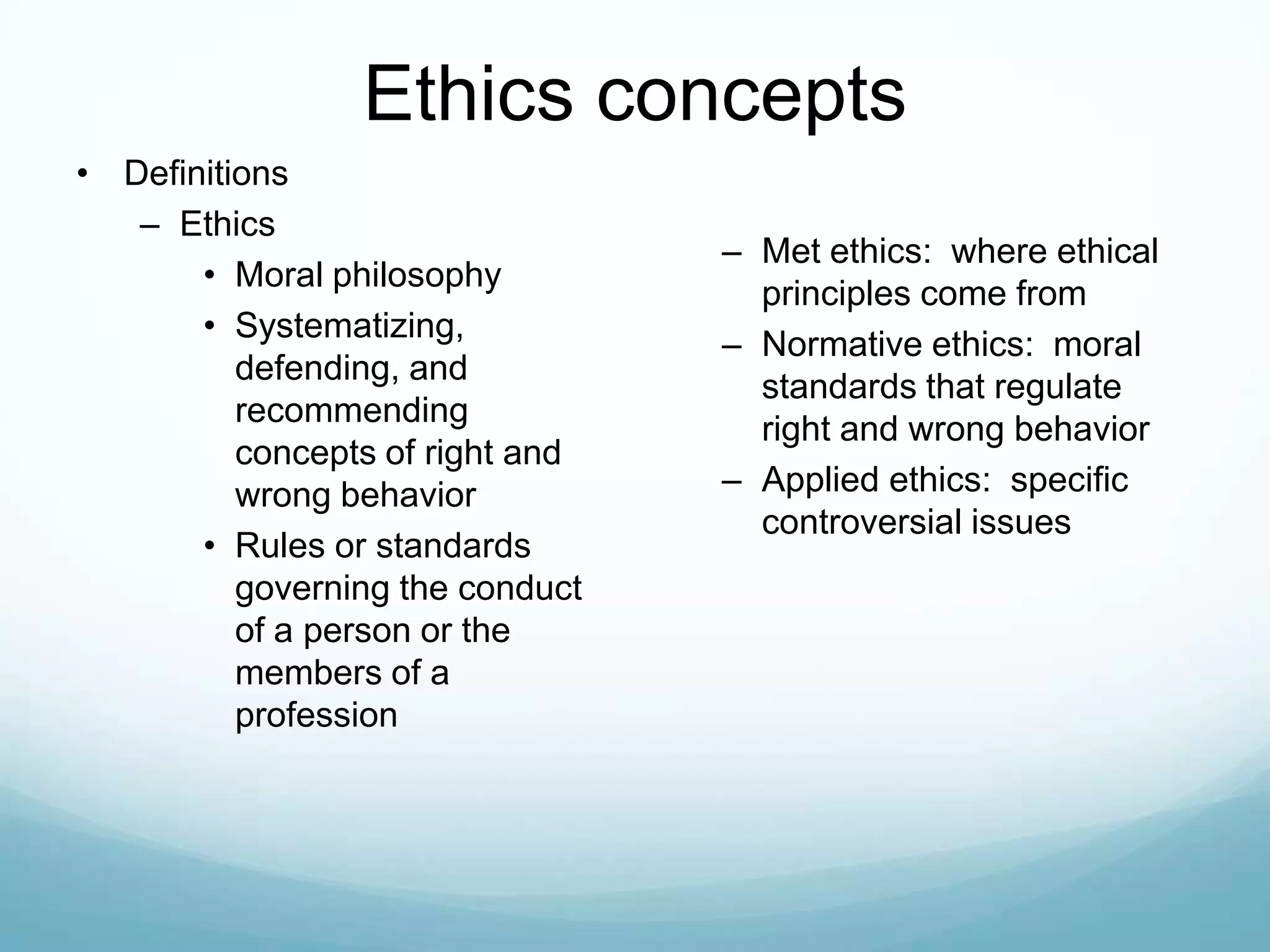

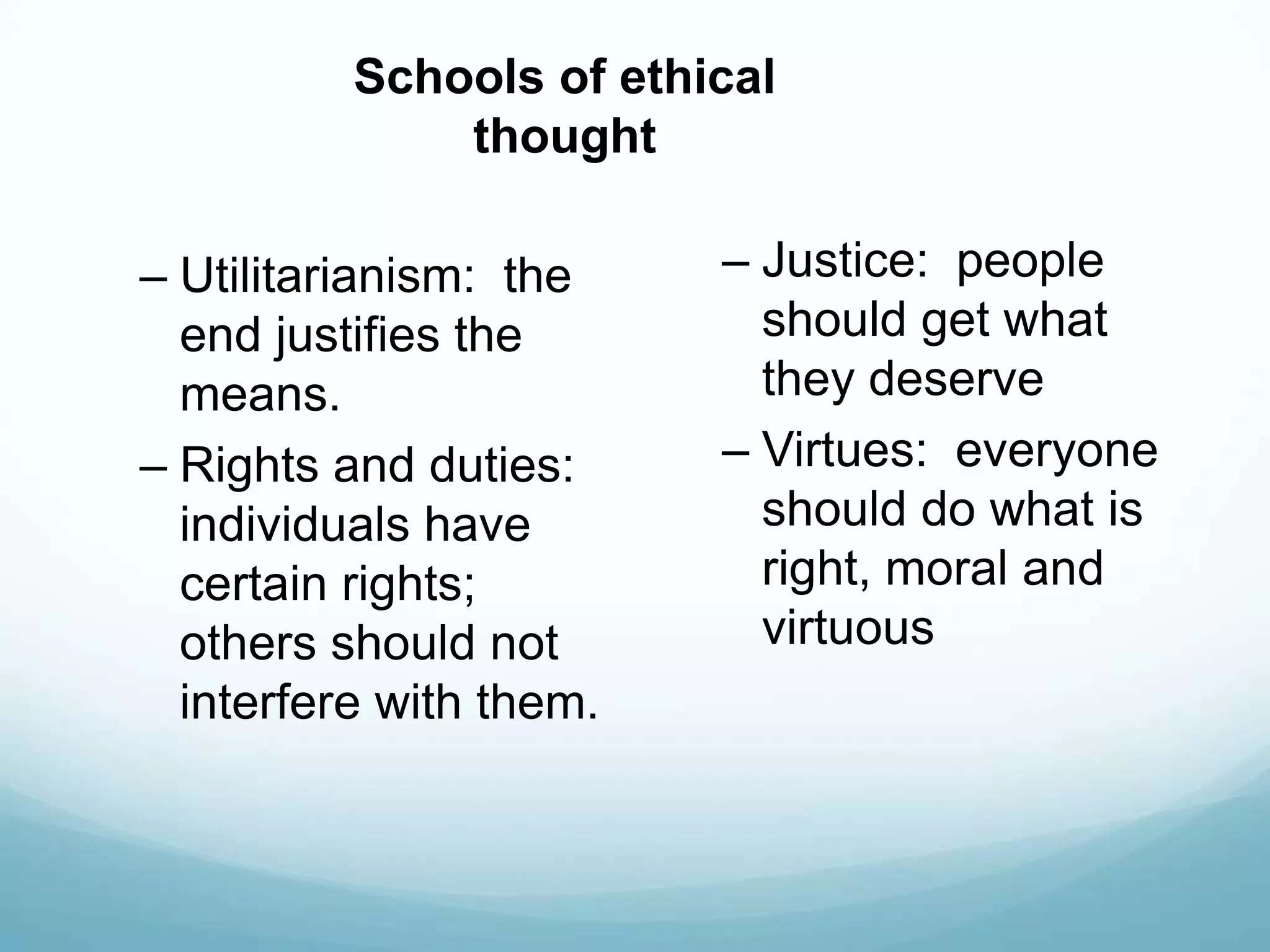

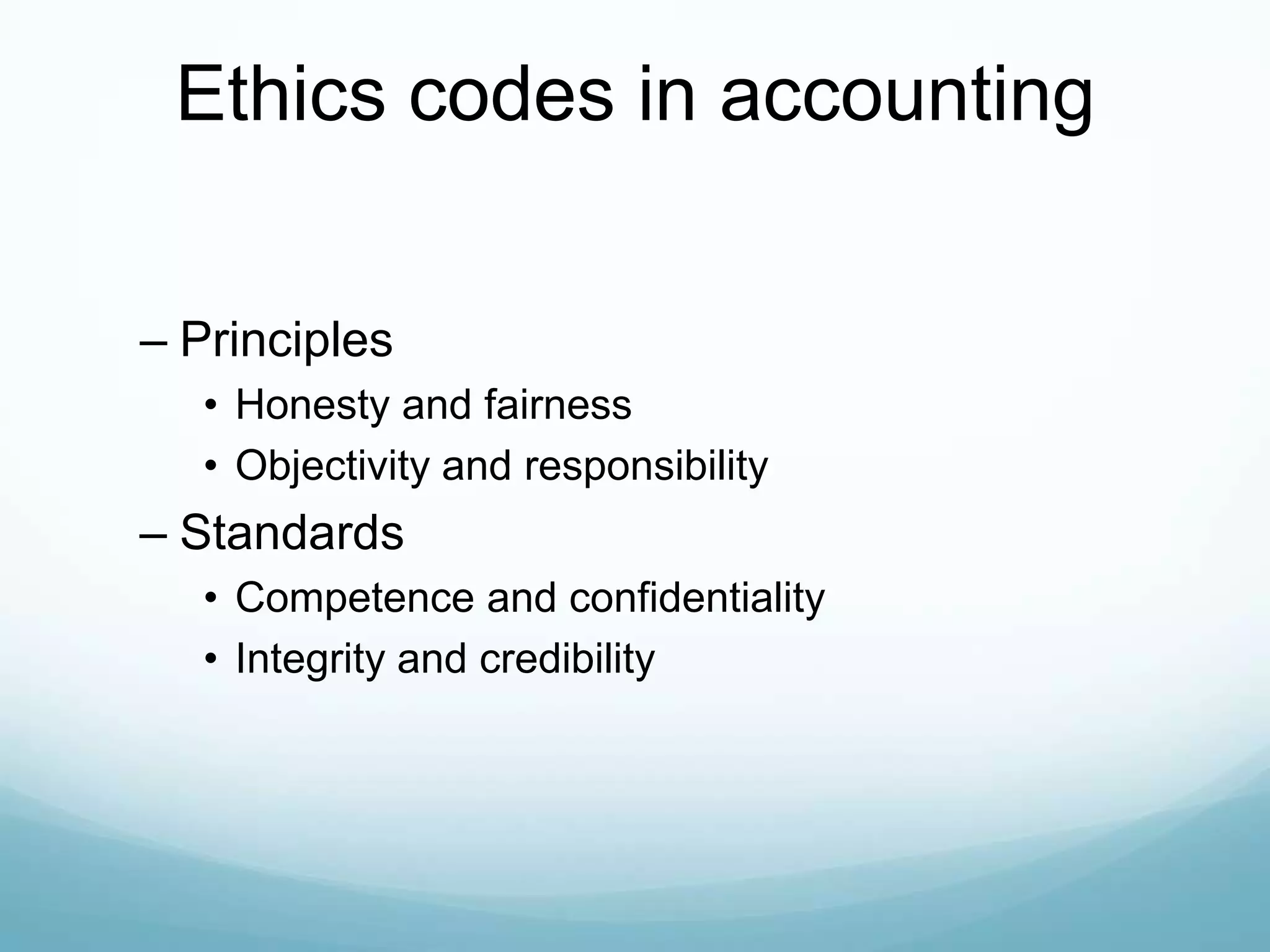

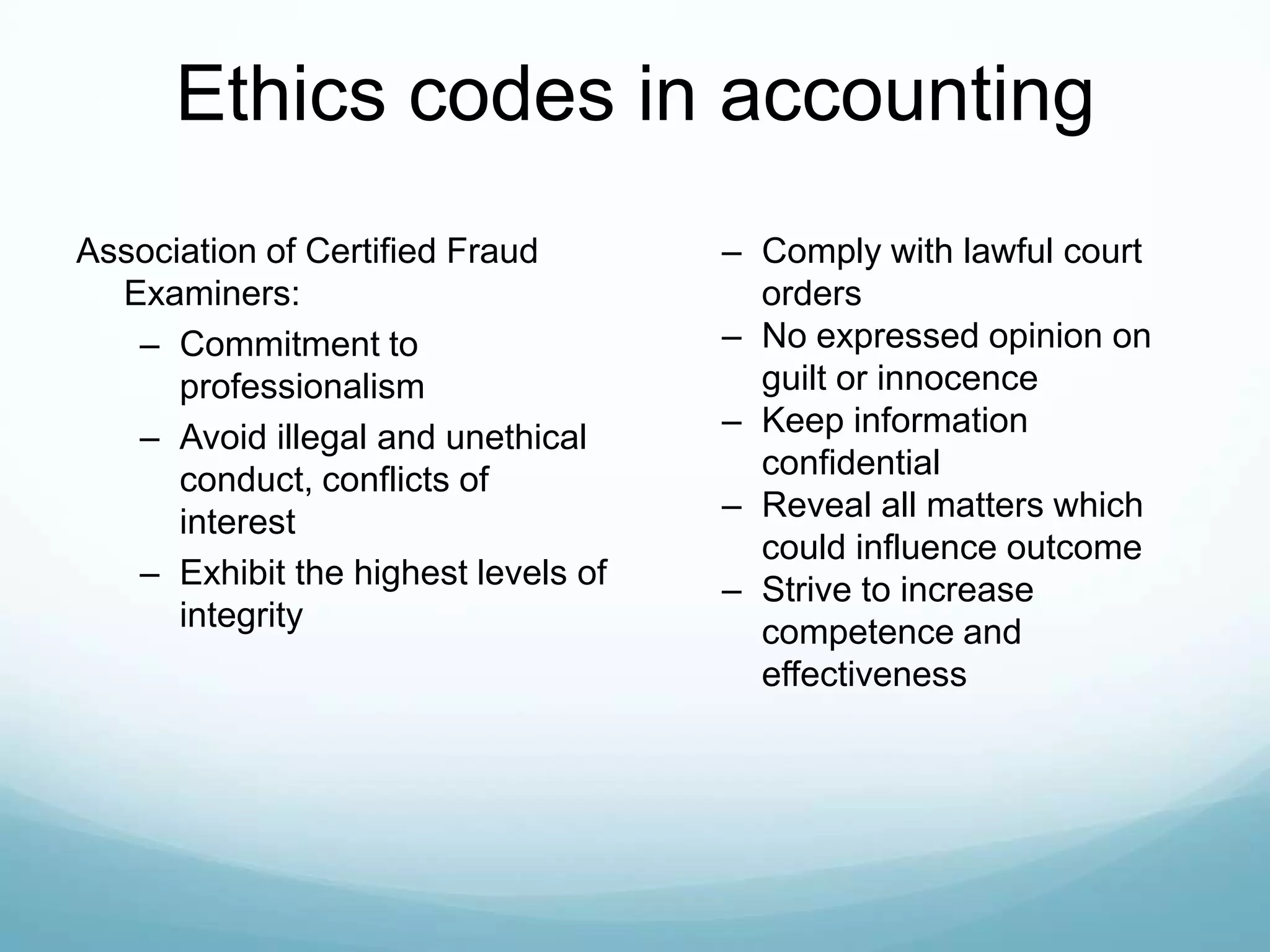

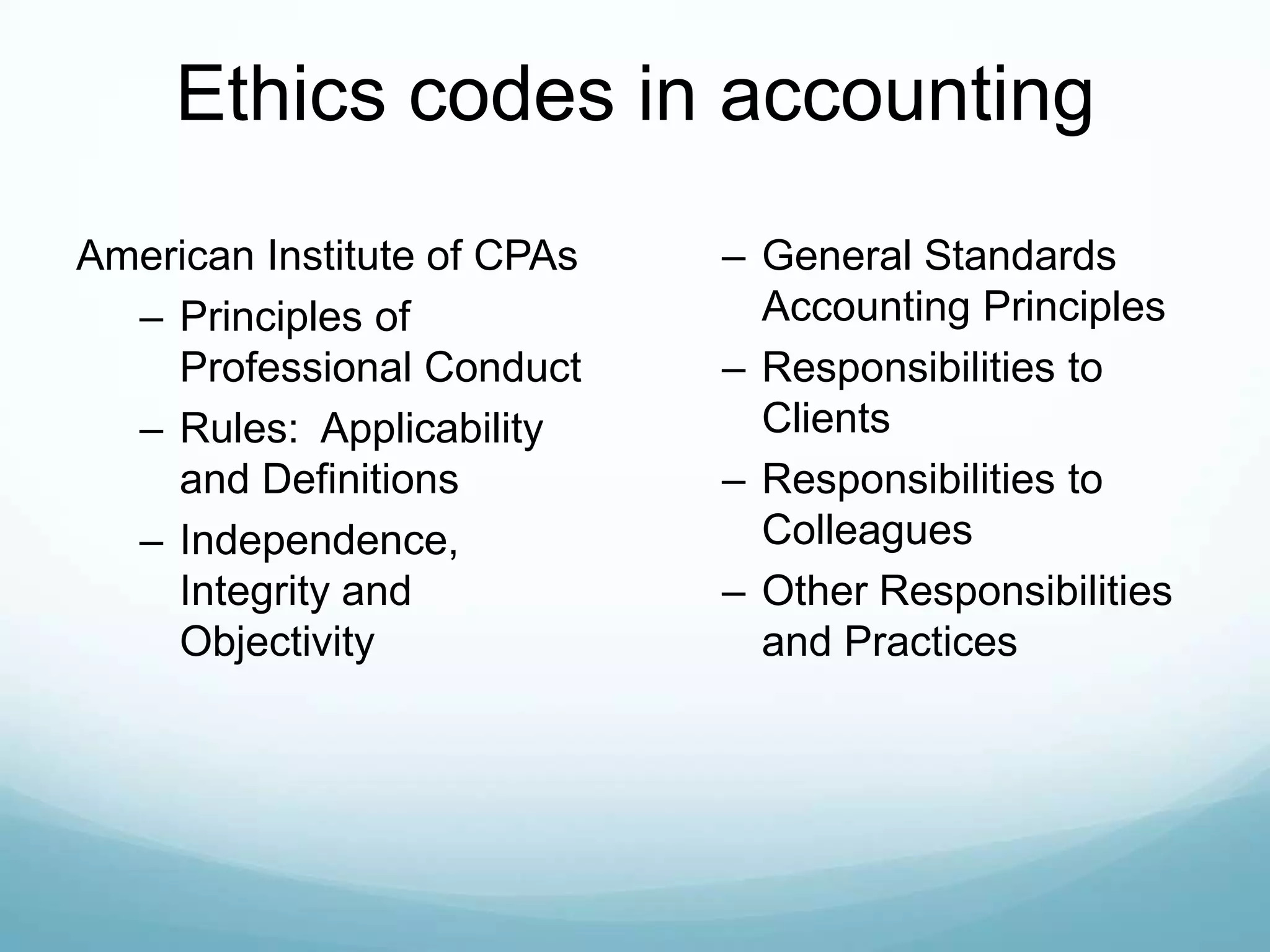

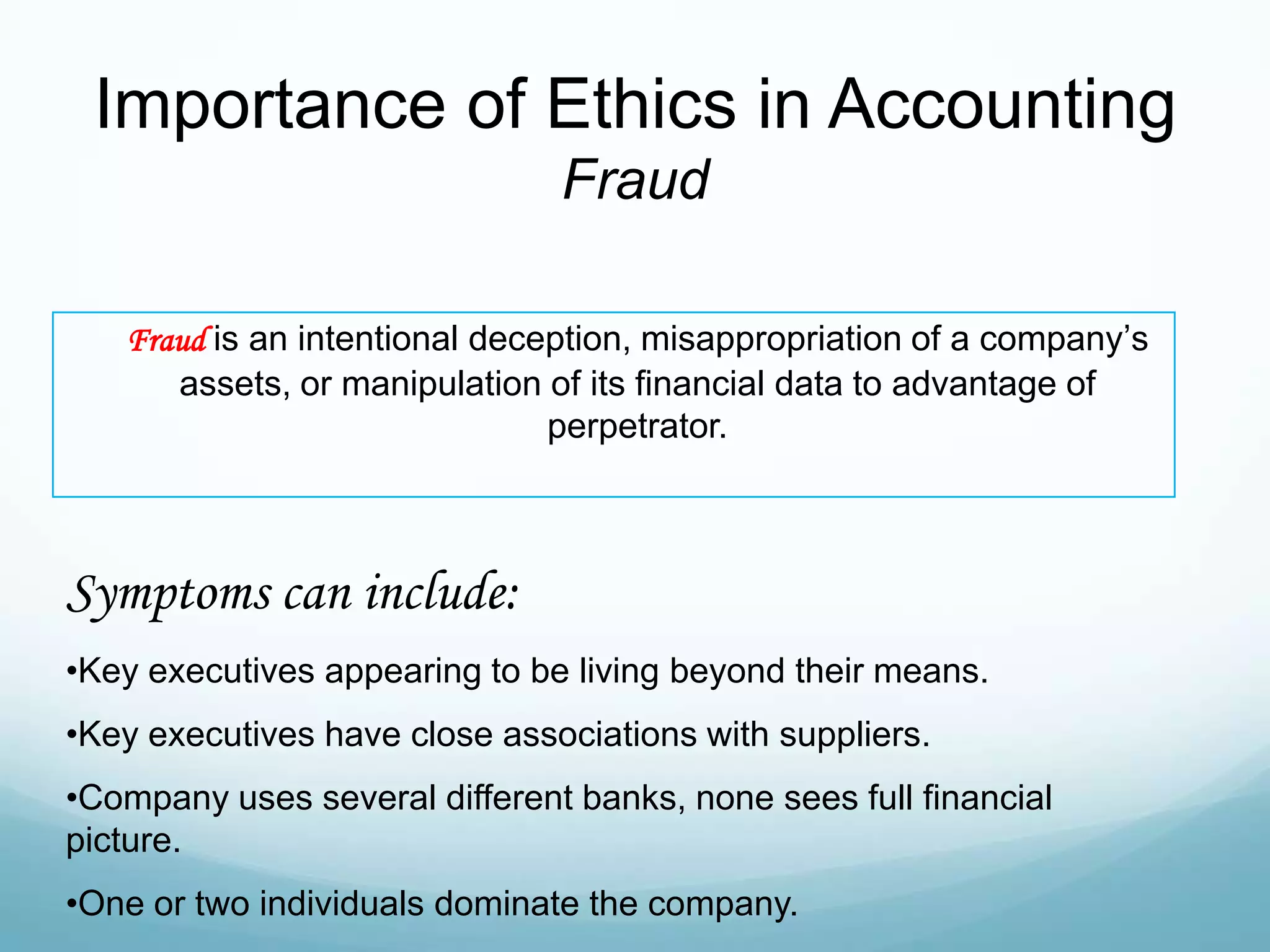

This document discusses ethics in accounting. It begins by listing characteristics of professionals, such as effective communication and exhibiting ethical behavior. It then defines ethics and discusses various models of ethical decision making. It explains ethics codes from accounting organizations like principles of honesty, objectivity, and integrity. The document discusses the importance of ethics in accounting to prevent fraud and losses. It suggests implementing effective ethical controls like a code of conduct and internal control systems to investigate motives for unethical practices and ensure accurate record keeping.