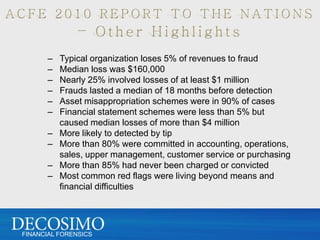

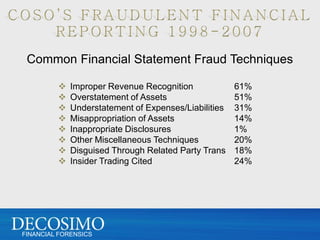

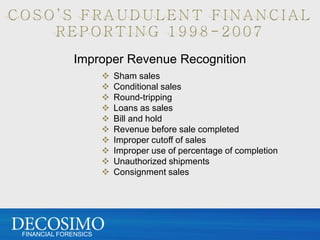

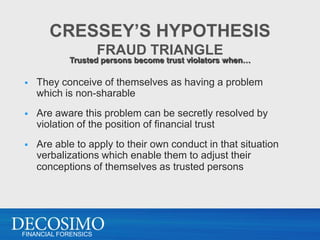

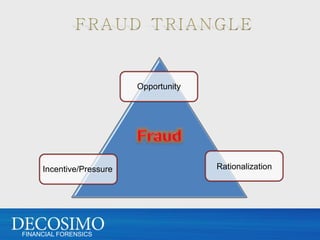

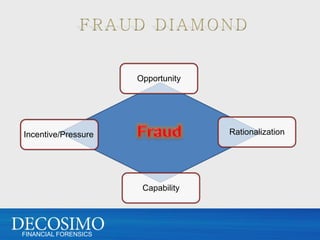

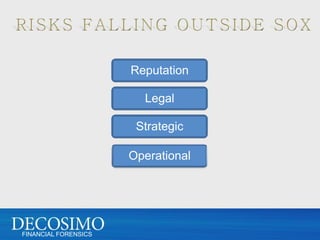

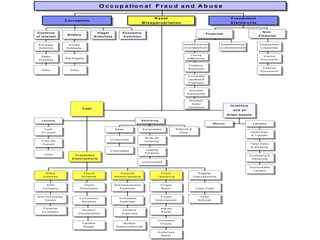

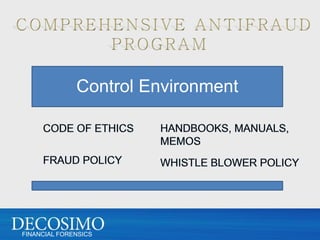

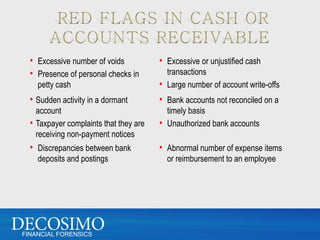

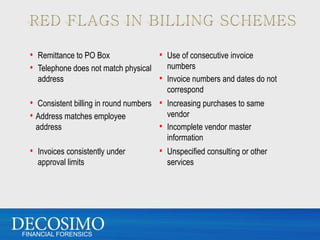

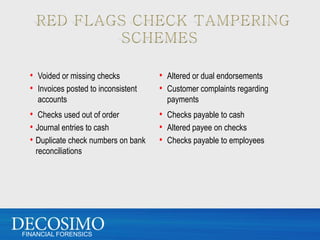

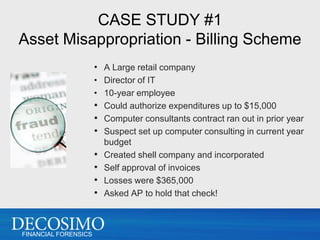

The document discusses internal controls to prevent and detect fraud from a forensic accountant's perspective. It provides definitions of fraud, outlines common fraud techniques like improper revenue recognition, and describes fraud risk factors such as an employee living beyond their means. The document also discusses establishing strong control environments, implementing antifraud controls and activities, ensuring proper information and communication, and monitoring for fraud through analytical reviews and fraud detection procedures. Strong internal controls, following up on red flags, and creating an ethical organizational culture can help prevent and detect occupational fraud.