Downloaded 10 times

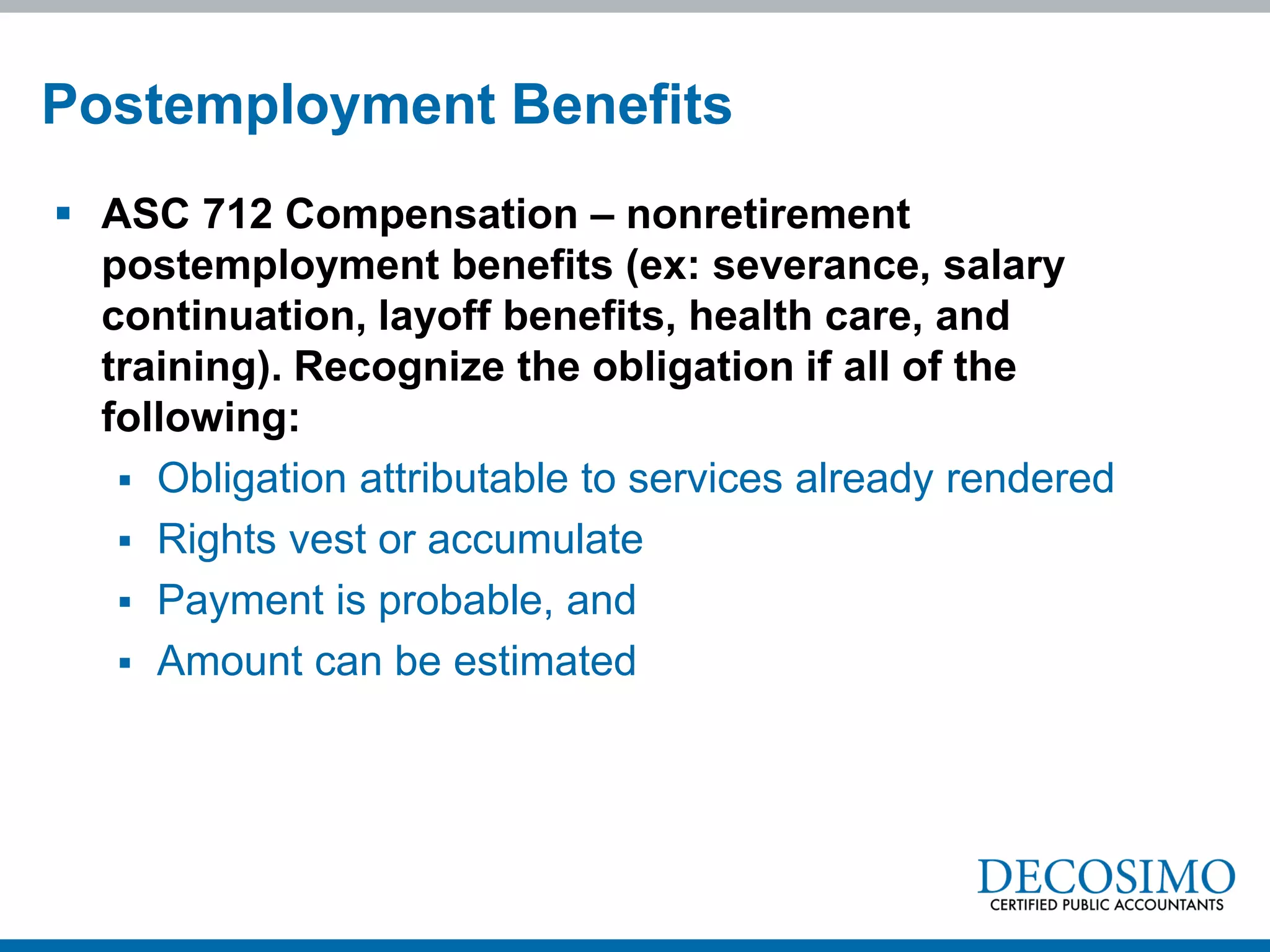

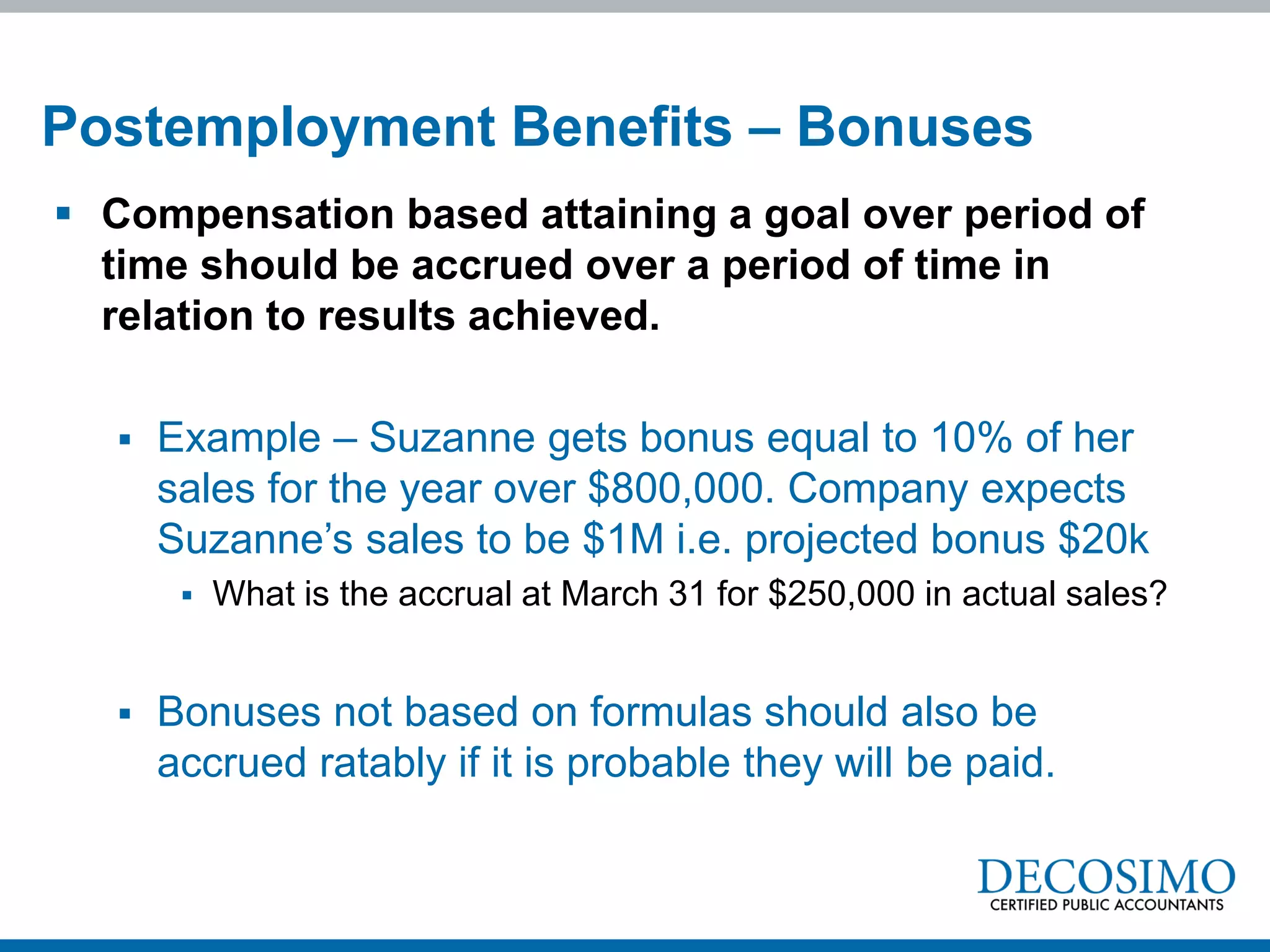

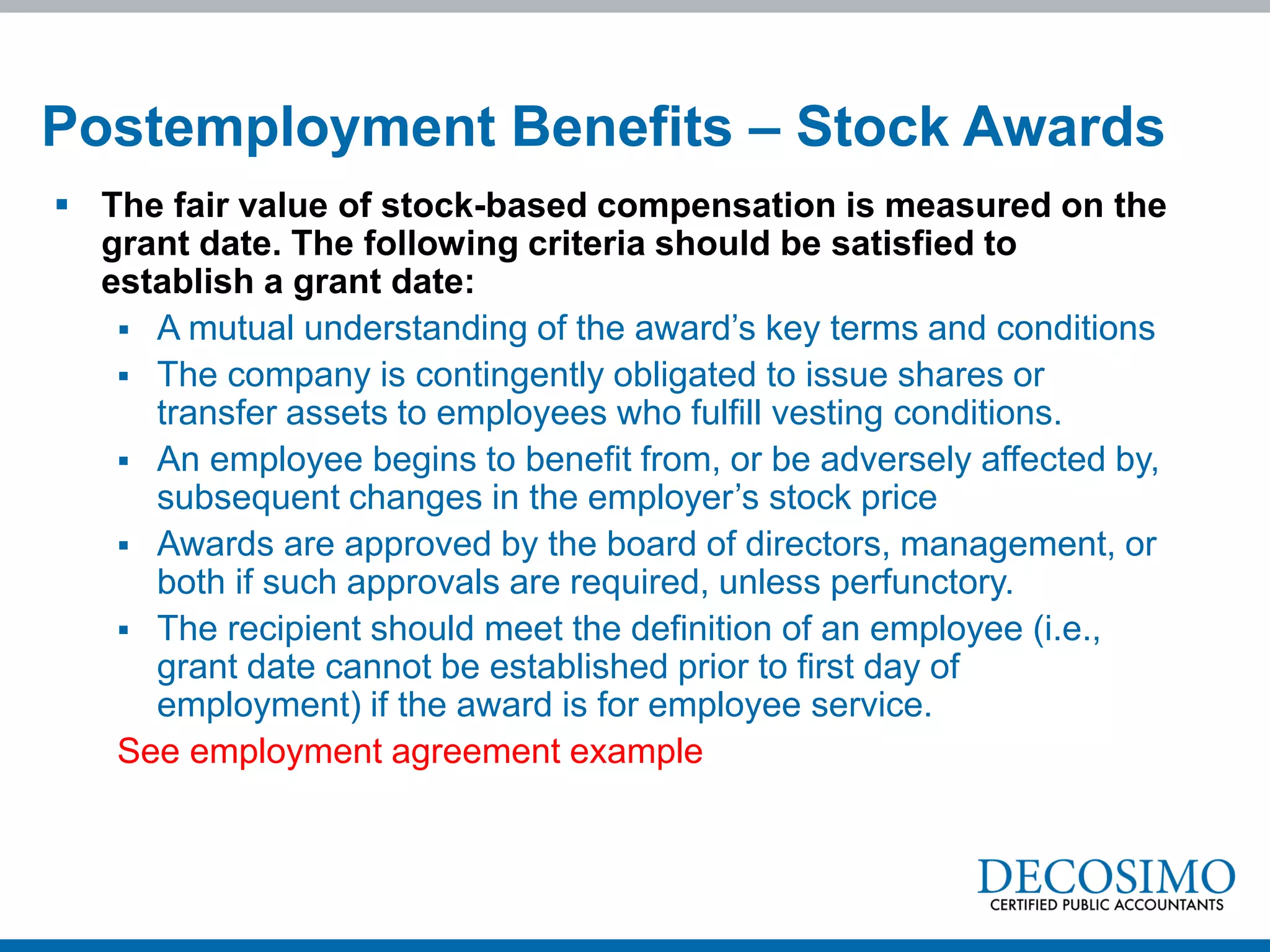

This document discusses common accounting topics that can cause unintended errors, or "oopsies", including life insurance policies, compensated absences, stock compensation, legal fees, accruals, capitalization minimums, FOB shipping terms, and deferred tax calculations. It provides examples and guidance for properly accounting for each topic according to US GAAP. The expert, Jennifer Goodman, is available to answer questions on ensuring compliance and avoiding unintended accounting errors.