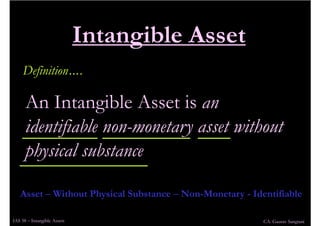

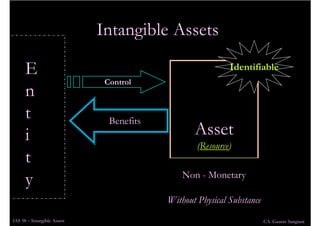

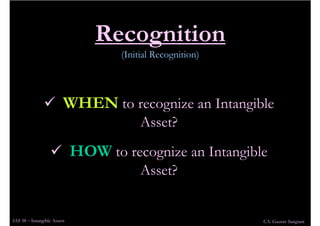

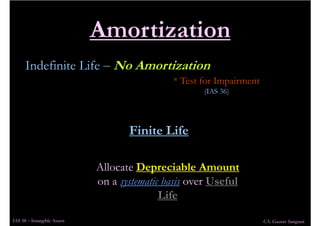

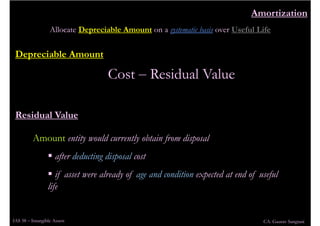

The document discusses the key aspects of IAS 38 - Intangible Assets including the scope, definition of an intangible asset, recognition, measurement, amortization, and disclosure requirements. It covers the initial recognition of intangible assets at cost and the subsequent measurement using either the cost or revaluation model. Internally generated intangible assets are recognized if certain criteria are met. Intangible assets with finite useful lives are amortized on a systematic basis over their useful lives while those with indefinite lives are tested annually for impairment.

![Brennan, Niamh and Connell, Brenda [2000] Intellectual Capital: Current Issue...](https://cdn.slidesharecdn.com/ss_thumbnails/0410brennanconnellintellectualcapitalcurrentissuesandpolicyimplications-121116102513-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)