Module 5.2

Fund FlowAnalysis

Session Objectives

•Purpose of Funds Flow Statement

•Meaning of Funds Flow

•Funds Flow Statement on Total Resource Basis

•Funds Flow Statement on Cash Basis

•Funds Flow Statement on Working Capital Basis

•Uses Funds Flow Statement

•Limitation of Fund Flow Statement

2.

Purpose of FundsFlow Statement

• The two basic financial statements of a firm are;

– The Balance Sheet

– The Profit and Loss

• Balance sheet gives a static view of the sources and uses of funds

and does not indicate the movement of funds.

• The profit and loss account does not indicate any change in

owner’s equity due to factors like additional investments or

withdrawal of profits.

• Therefore, an additional statement is needed to show the changes

in the assets, liabilities and owner’s equity between dates of two

balance sheets.

• This requirement is fulfilled by a funds flow statement.

3.

Concepts of FundsFlow Statement

• Meaning of :

Fund means “Working Capital”

Flow means transfer of economic values from one asset or equity to another

• Flow of fund refers to movement of funds which cause a change in working

capital of the organization.

• In other words, increase or decrease in working capital reflects flow of funds.

• When a transaction increases working capital it is a known as ‘Source of Fund’

and when it decreases the working capital, it is termed as ‘ Use of fund’.

• When a business transaction does not affect working capital, no flow of fund

take place.

4.

Meaning of FundFlow Statement

• Funds Flow statement is

“a statement that summarizes the sources from which

funds were obtained by the firm and the specific uses to

which the sources were applied.”

5.

Questions answered byFFS

• What is the amount of funds generated from operations?

• How were the Fixed Assets of the organizations financed?

• What is the extent of dependence on external sources of finance?

• Whether the liquidity position of the organization increased?

6.

Identification of Flowof Funds

• Transaction which involve

– only current accounts (CA & CL)

– only non current accounts (FA & FL)

do not result into change in working capital

• Transaction which involve

one current account and one non current account

result into change in working capital.

7.

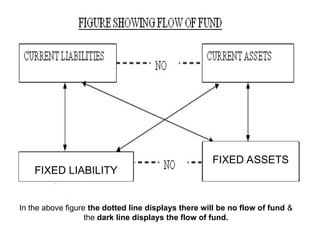

In the abovefigure the dotted line displays there will be no flow of fund &

the dark line displays the flow of fund.

FIXED ASSETS

FIXED LIABILITY

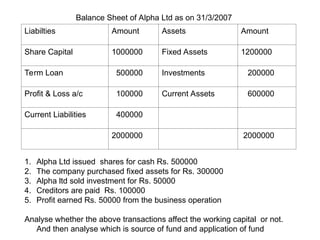

Liabilties Amount AssetsAmount

Share Capital 1000000 Fixed Assets 1200000

Term Loan 500000 Investments 200000

Profit & Loss a/c 100000 Current Assets 600000

Current Liabilities 400000

2000000 2000000

Balance Sheet of Alpha Ltd as on 31/3/2007

1. Alpha Ltd issued shares for cash Rs. 500000

2. The company purchased fixed assets for Rs. 300000

3. Alpha ltd sold investment for Rs. 50000

4. Creditors are paid Rs. 100000

5. Profit earned Rs. 50000 from the business operation

Analyse whether the above transactions affect the working capital or not.

And then analyse which is source of fund and application of fund

10.

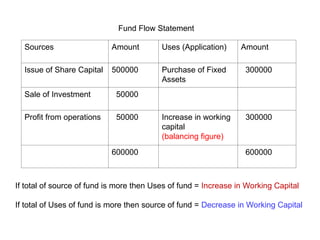

Sources Amount Uses(Application) Amount

Issue of Share Capital 500000 Purchase of Fixed

Assets

300000

Sale of Investment 50000

Profit from operations 50000 Increase in working

capital

(balancing figure)

300000

600000 600000

Fund Flow Statement

If total of source of fund is more then Uses of fund = Increase in Working Capital

If total of Uses of fund is more then source of fund = Decrease in Working Capital

11.

Approaches

• Funds FlowStatement can be prepared in three ways:

On Total Resource Basis

On Cash Basis

On Working Capital Basis

12.

Fund Flow Statementon Total Resource Basis

• While preparing a funds flow statement on total resource

basis, the balance sheets covering a certain time period,

should be compared for which the statement is being

prepared.

• The increase or decrease in different assets and liabilities

are noted and categorized accordingly as sources or uses

of funds.

• Since changes in all the items are considered, the sources

of funds will always be equal to the uses of funds.

• In addition we need to compute funds from operations with

the help of the profit and loss statement.

13.

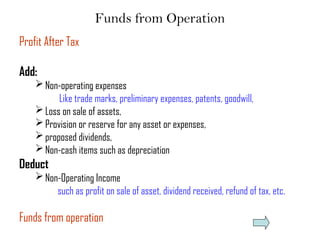

Funds from Operation

ProfitAfter Tax

Add:

Non-operating expenses

Like trade marks, preliminary expenses, patents, goodwill,

Loss on sale of assets,

Provision or reserve for any asset or expenses,

proposed dividends,

Non-cash items such as depreciation

Deduct

Non-Operating Income

such as profit on sale of asset, dividend received, refund of tax, etc.

Funds from operation

14.

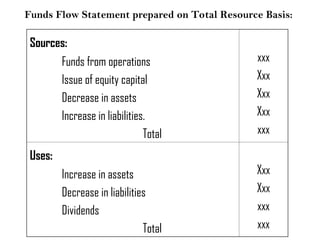

Funds Flow Statementprepared on Total Resource Basis:

Sources:

Funds from operations

Issue of equity capital

Decrease in assets

Increase in liabilities.

Total

xxx

Xxx

Xxx

Xxx

xxx

Uses:

Increase in assets

Decrease in liabilities

Dividends

Total

Xxx

Xxx

xxx

xxx

15.

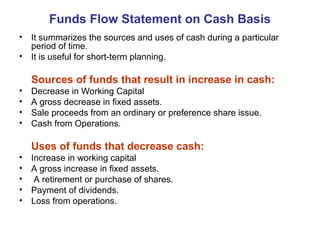

Funds Flow Statementon Cash Basis

• It summarizes the sources and uses of cash during a particular

period of time.

• It is useful for short-term planning.

Sources of funds that result in increase in cash:

• Decrease in Working Capital

• A gross decrease in fixed assets.

• Sale proceeds from an ordinary or preference share issue.

• Cash from Operations.

Uses of funds that decrease cash:

• Increase in working capital

• A gross increase in fixed assets.

• A retirement or purchase of shares.

• Payment of dividends.

• Loss from operations.

16.

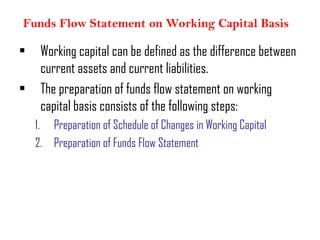

Funds Flow Statementon Working Capital Basis

• Working capital can be defined as the difference between

current assets and current liabilities.

• The preparation of funds flow statement on working

capital basis consists of the following steps:

1. Preparation of Schedule of Changes in Working Capital

2. Preparation of Funds Flow Statement

17.

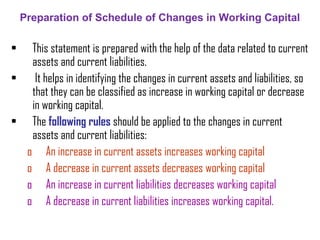

Preparation of Scheduleof Changes in Working Capital

• This statement is prepared with the help of the data related to current

assets and current liabilities.

• It helps in identifying the changes in current assets and liabilities, so

that they can be classified as increase in working capital or decrease

in working capital.

• The following rules should be applied to the changes in current

assets and current liabilities:

o An increase in current assets increases working capital

o A decrease in current assets decreases working capital

o An increase in current liabilities decreases working capital

o A decrease in current liabilities increases working capital.

18.

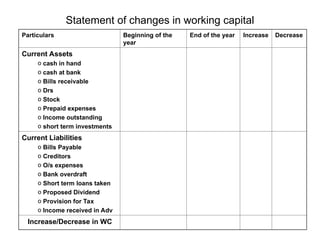

Statement of changesin working capital

Particulars Beginning of the

year

End of the year Increase Decrease

Current Assets

o cash in hand

o cash at bank

o Bills receivable

o Drs

o Stock

o Prepaid expenses

o Income outstanding

o short term investments

Current Liabilities

o Bills Payable

o Creditors

o O/s expenses

o Bank overdraft

o Short term loans taken

o Proposed Dividend

o Provision for Tax

o Income received in Adv

Increase/Decrease in WC

19.

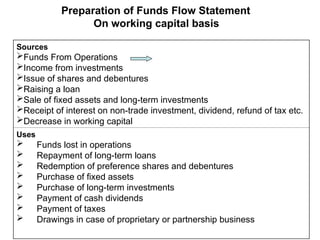

Preparation of FundsFlow Statement

On working capital basis

Sources

Funds From Operations

Income from investments

Issue of shares and debentures

Raising a loan

Sale of fixed assets and long-term investments

Receipt of interest on non-trade investment, dividend, refund of tax etc.

Decrease in working capital

Uses

Funds lost in operations

Repayment of long-term loans

Redemption of preference shares and debentures

Purchase of fixed assets

Purchase of long-term investments

Payment of cash dividends

Payment of taxes

Drawings in case of proprietary or partnership business

20.

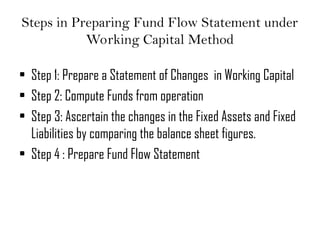

Steps in PreparingFund Flow Statement under

Working Capital Method

• Step 1: Prepare a Statement of Changes in Working Capital

• Step 2: Compute Funds from operation

• Step 3: Ascertain the changes in the Fixed Assets and Fixed

Liabilities by comparing the balance sheet figures.

• Step 4 : Prepare Fund Flow Statement

21.

Uses of FundFlow Statement

– It helps in detecting the imbalances existing in the management

of the assets and liabilities of the firm, so that the appropriate

action is taken.

– Individual funds flow statements prepared for different divisions

of a company help in evaluating their performance.

– It helps in reviewing the financing mix i.e. the mix of the short-

term and long-term sources of funds.

– It helps in predicting the future needs for funds.

22.

Limitation

• Funds flowstatement can be interpreted only in conjunction

with the other financial statements.

• By itself, it cannot provide a complete analysis of the

financial position and changes therein.