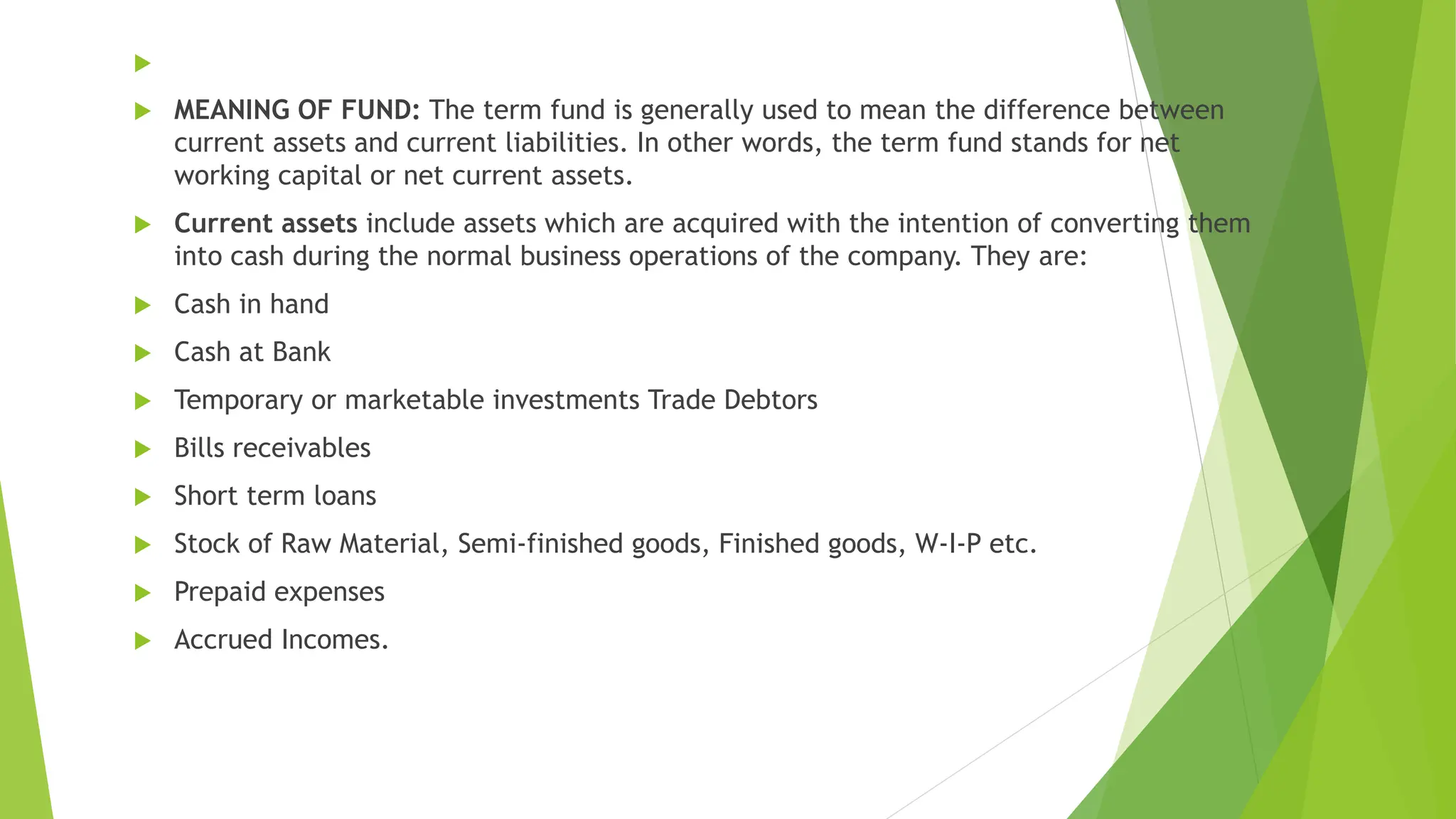

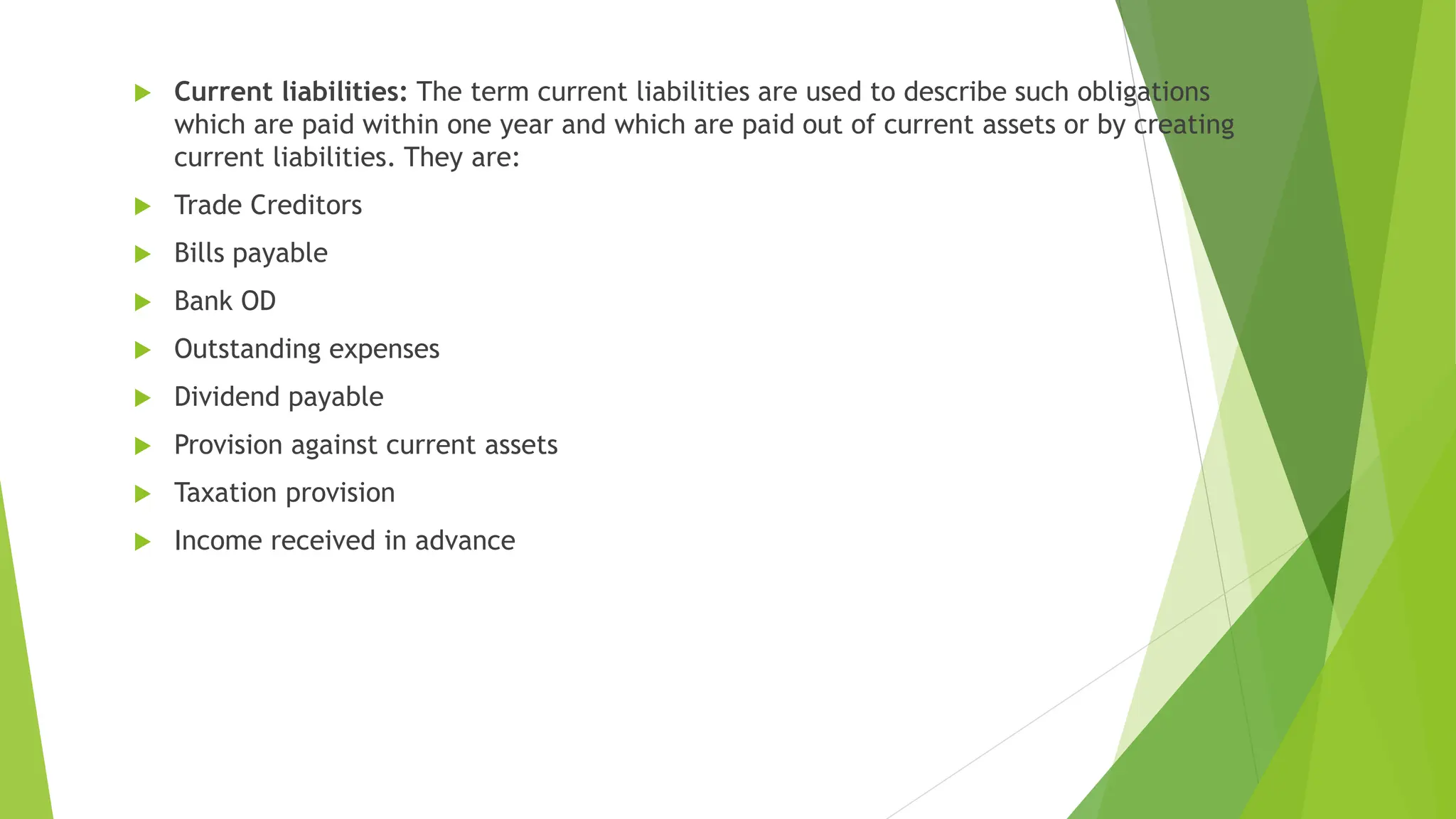

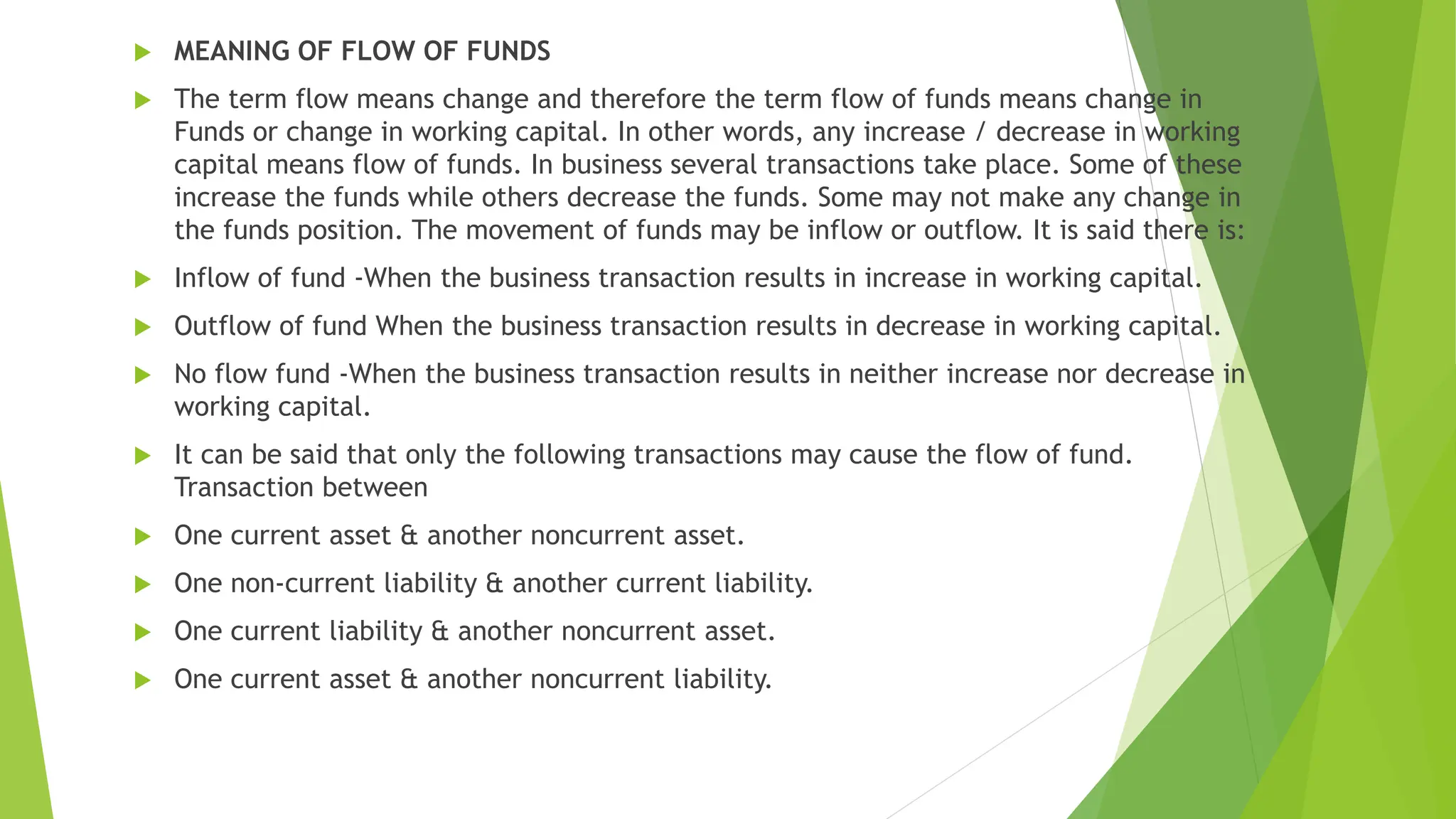

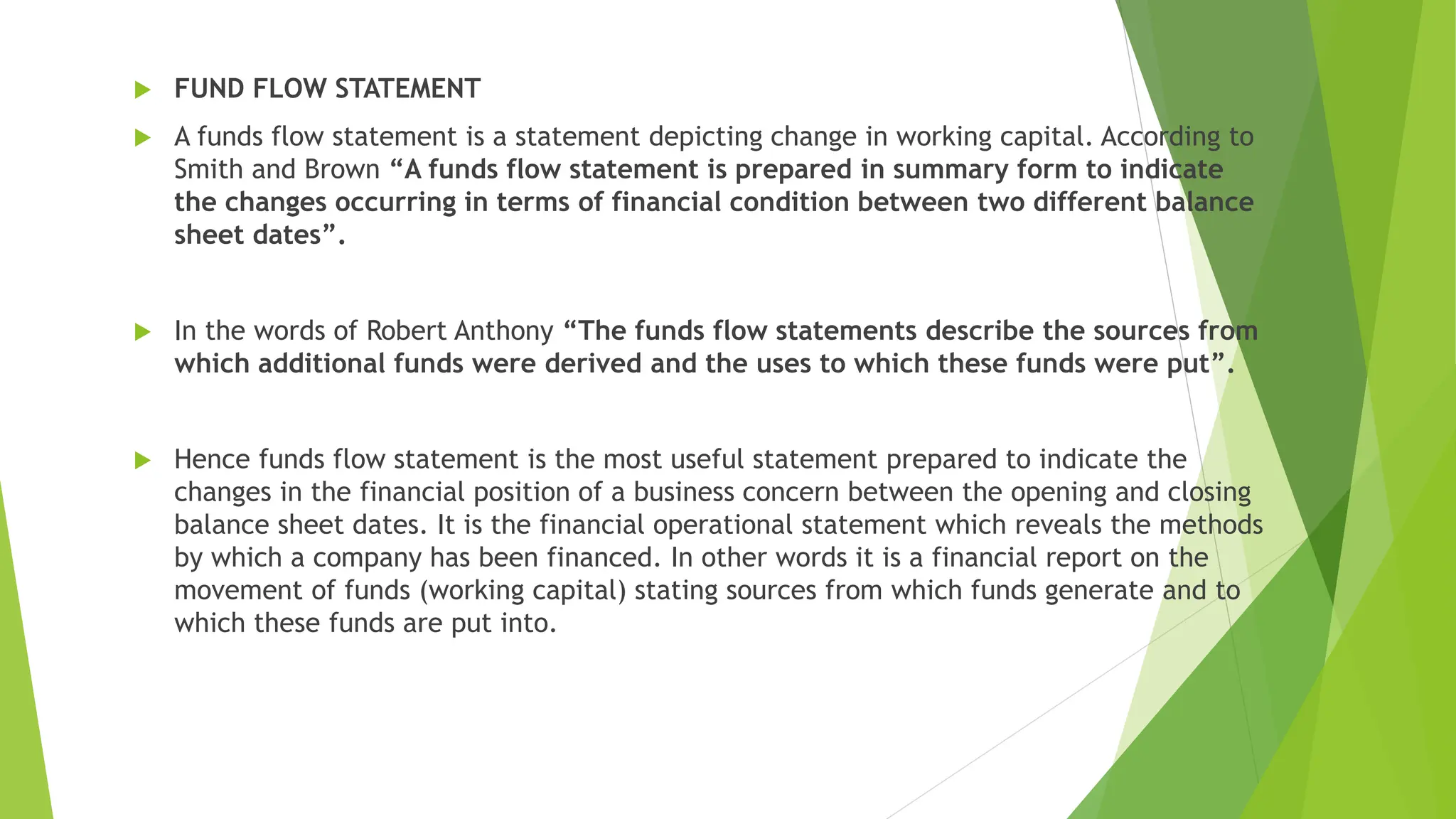

The document discusses fund flow analysis, including definitions of funds, current assets and liabilities, and the meaning of fund flows. It states that a fund flow statement depicts changes in working capital between two balance sheet dates, showing how funds were obtained and used. The statement is useful for analysis, working capital management, decision making, forecasting, and measuring creditworthiness. Some limitations are that it relies on historical data and does not include non-fund items. Sources of funds include issues of shares/debentures, loans, asset sales, and profits. Uses include losses, debt repayments, investments, and non-operating expenses.