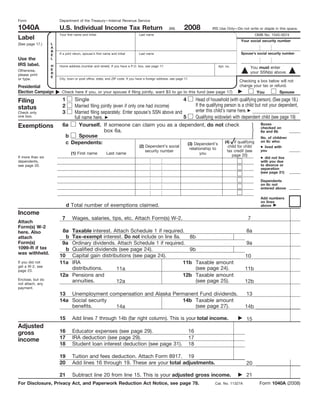

1) This is an IRS Form 1040A for the 2008 tax year, which is used to file an individual US income tax return.

2) The form provides lines to report income such as wages, taxable interest, dividends and retirement distributions, as well as adjustments, deductions, credits, tax amount, payments and refund or amount owed.

3) It includes options to elect tax credits, request a refund by direct deposit, and allow discussion of the tax return with the IRS by a third party designee.

Wayne Lippman presents Tax Filing Status GuideWayne Lippman

Who should file their tax? Wayne Lippman explains.

Determine the most advantageous (and allowable) filing status for the taxpayer.

Overview of all 5 filing statii:

Married Filing Jointly (not legally separated)

Qualifying Widow(er) with Dependent Child

Head of Household

Single

Married Filing Separately (Taxpayer either Itemizes or claims 0 standard deductions, if spouse itemized deductions)

*Confirm marital status on the last day of the tax year

In our latest webinar on e-Invoicing our in-house experts, CA Kunal Gandhi, Finance Controller and Lokesh Malhotra, Lead - Product Manager, explained the concepts and challenges of e-Invoicing. Further, covered how Open simplifies e-Invoicing while keeping your business tax compliant.

Key Insights from the webinar:

1. e-Invoicing under GST - Introduction and Timelines

2. How to create e-Invoices, Standard format, Schema, etc.

3. Debunking common myths around e-Invoicing

4. Advantages of e-Invoicing

5. Demo on Generating e-Invoices using Open

For more information, Visit : https://webinars.open.money/e-invoice/

The GST Council has relaxed filing rules for the first two months post implementation. Here's how to file your returns for these months using form GSTR 3B. To know more about GSTR 3B, visit our page https://cleartax.in/s/gstr-3b

this presentation consists of the information abou TDS ans TCS and their implications under GST. It also includes the differnce between both the terms.

Wayne Lippman presents Tax Filing Status GuideWayne Lippman

Who should file their tax? Wayne Lippman explains.

Determine the most advantageous (and allowable) filing status for the taxpayer.

Overview of all 5 filing statii:

Married Filing Jointly (not legally separated)

Qualifying Widow(er) with Dependent Child

Head of Household

Single

Married Filing Separately (Taxpayer either Itemizes or claims 0 standard deductions, if spouse itemized deductions)

*Confirm marital status on the last day of the tax year

In our latest webinar on e-Invoicing our in-house experts, CA Kunal Gandhi, Finance Controller and Lokesh Malhotra, Lead - Product Manager, explained the concepts and challenges of e-Invoicing. Further, covered how Open simplifies e-Invoicing while keeping your business tax compliant.

Key Insights from the webinar:

1. e-Invoicing under GST - Introduction and Timelines

2. How to create e-Invoices, Standard format, Schema, etc.

3. Debunking common myths around e-Invoicing

4. Advantages of e-Invoicing

5. Demo on Generating e-Invoices using Open

For more information, Visit : https://webinars.open.money/e-invoice/

The GST Council has relaxed filing rules for the first two months post implementation. Here's how to file your returns for these months using form GSTR 3B. To know more about GSTR 3B, visit our page https://cleartax.in/s/gstr-3b

this presentation consists of the information abou TDS ans TCS and their implications under GST. It also includes the differnce between both the terms.

The following Presentation enumerates the various provisions w.r.t. ITC, how it can be used,eligibilty and conditions for claiming ITC along with various case studies and illustrations. further, it elaborates the concept of input service distributor.

Real estate, as an immovable factor, tends to be overtaxed in most countries and Portugal is no exception. Tax structuring and optimizing is crucial to minimize total acquisition costs and maximize investment returns.

RPBA’s updated presentation deals with this challenging topic incorporating the latest developments, including tax incentives on rehabilitation, the OECD Multilateral Instrument rules on “real estate rich” companies and also the brand new SIGI company (the Portuguese equivalent of the REIT – Real Estate Investment Trust).

How to file form-1 (equalization levy) on new income-tax portal?Ankitasahu60

On or before the 30th of June immediately following the financial year, the statement in Form No.1 in respect of all the specified services chargeable to the equalization levy must be given.

The equalization levy would be 6% of the amount of consideration for specified services received or receivable by a non-resident not having a permanent establishment ('PE') in India, from an Indian resident carrying on business or profession, or from a non-resident having a permanent establishment in India.

OBJECTIVES:

Definition

Job work Procedure u/s 143 of CGST Act, 2017.

Input tax credit as per Section 16 and 19 of the CGST Act, 2017.

Other clarifications relating to Job work as per Circular No. 38/12/2017 – Central Tax dated 26th of March 2018.

The Portuguese non-habitual tax resident (NHR) regime is granted to individuals who become resident for tax purposes in Portugal. This regime may grant an exemption on certain foreign source income as well as a 20% tax rate on employment and self-employment income deriving from high value-added activities during 10 years. Entrants into the NHR regime that became Portuguese tax residents after April 1st 2020 are subject to a flat tax rate of 10% on foreign-sourced pensions (instead of the previous exemption), as well as on other payments, such as pre-retirement benefits and "lump-sum" payments from pension funds and similar retirement schemes. It targets non-resident individuals who are likely to establish residence in Portugal. View a few standard case studies on this RPBA’s infographic.

EWAY Bill a complete guide by GSTSEVA.COM

This slides specifically prepared for logistics, transport, registered users under gst and students to understand eway bill concept in GST with examples.

Thanks

Team www.gstseva.com

With the help of this presentation one can learn e filing of Income Tax Return and can start his/her own practice as agent for filing of income tax returns

Deferred Tax,

By: Mahima Pahwa (IBS Gurgaon)

Differences between Accounting Income and Taxable Income

TYPES OF DEFERRED TAX

DEFERRED TAX LIABILITY

FINANCIAL STATEMENTS PRESENTATION

The following Presentation enumerates the various provisions w.r.t. ITC, how it can be used,eligibilty and conditions for claiming ITC along with various case studies and illustrations. further, it elaborates the concept of input service distributor.

Real estate, as an immovable factor, tends to be overtaxed in most countries and Portugal is no exception. Tax structuring and optimizing is crucial to minimize total acquisition costs and maximize investment returns.

RPBA’s updated presentation deals with this challenging topic incorporating the latest developments, including tax incentives on rehabilitation, the OECD Multilateral Instrument rules on “real estate rich” companies and also the brand new SIGI company (the Portuguese equivalent of the REIT – Real Estate Investment Trust).

How to file form-1 (equalization levy) on new income-tax portal?Ankitasahu60

On or before the 30th of June immediately following the financial year, the statement in Form No.1 in respect of all the specified services chargeable to the equalization levy must be given.

The equalization levy would be 6% of the amount of consideration for specified services received or receivable by a non-resident not having a permanent establishment ('PE') in India, from an Indian resident carrying on business or profession, or from a non-resident having a permanent establishment in India.

OBJECTIVES:

Definition

Job work Procedure u/s 143 of CGST Act, 2017.

Input tax credit as per Section 16 and 19 of the CGST Act, 2017.

Other clarifications relating to Job work as per Circular No. 38/12/2017 – Central Tax dated 26th of March 2018.

The Portuguese non-habitual tax resident (NHR) regime is granted to individuals who become resident for tax purposes in Portugal. This regime may grant an exemption on certain foreign source income as well as a 20% tax rate on employment and self-employment income deriving from high value-added activities during 10 years. Entrants into the NHR regime that became Portuguese tax residents after April 1st 2020 are subject to a flat tax rate of 10% on foreign-sourced pensions (instead of the previous exemption), as well as on other payments, such as pre-retirement benefits and "lump-sum" payments from pension funds and similar retirement schemes. It targets non-resident individuals who are likely to establish residence in Portugal. View a few standard case studies on this RPBA’s infographic.

EWAY Bill a complete guide by GSTSEVA.COM

This slides specifically prepared for logistics, transport, registered users under gst and students to understand eway bill concept in GST with examples.

Thanks

Team www.gstseva.com

With the help of this presentation one can learn e filing of Income Tax Return and can start his/her own practice as agent for filing of income tax returns

Deferred Tax,

By: Mahima Pahwa (IBS Gurgaon)

Differences between Accounting Income and Taxable Income

TYPES OF DEFERRED TAX

DEFERRED TAX LIABILITY

FINANCIAL STATEMENTS PRESENTATION

BYD SWOT Analysis and In-Depth Insights 2024.pptxmikemetalprod

Indepth analysis of the BYD 2024

BYD (Build Your Dreams) is a Chinese automaker and battery manufacturer that has snowballed over the past two decades to become a significant player in electric vehicles and global clean energy technology.

This SWOT analysis examines BYD's strengths, weaknesses, opportunities, and threats as it competes in the fast-changing automotive and energy storage industries.

Founded in 1995 and headquartered in Shenzhen, BYD started as a battery company before expanding into automobiles in the early 2000s.

Initially manufacturing gasoline-powered vehicles, BYD focused on plug-in hybrid and fully electric vehicles, leveraging its expertise in battery technology.

Today, BYD is the world’s largest electric vehicle manufacturer, delivering over 1.2 million electric cars globally. The company also produces electric buses, trucks, forklifts, and rail transit.

On the energy side, BYD is a major supplier of rechargeable batteries for cell phones, laptops, electric vehicles, and energy storage systems.

The secret way to sell pi coins effortlessly.DOT TECH

Well as we all know pi isn't launched yet. But you can still sell your pi coins effortlessly because some whales in China are interested in holding massive pi coins. And they are willing to pay good money for it. If you are interested in selling I will leave a contact for you. Just telegram this number below. I sold about 3000 pi coins to him and he paid me immediately.

Telegram: @Pi_vendor_247

where can I find a legit pi merchant onlineDOT TECH

Yes. This is very easy what you need is a recommendation from someone who has successfully traded pi coins before with a merchant.

Who is a pi merchant?

A pi merchant is someone who buys pi network coins and resell them to Investors looking forward to hold thousands of pi coins before the open mainnet.

I will leave the telegram contact of my personal pi merchant to trade with

@Pi_vendor_247

how to sell pi coins effectively (from 50 - 100k pi)DOT TECH

Anywhere in the world, including Africa, America, and Europe, you can sell Pi Network Coins online and receive cash through online payment options.

Pi has not yet been launched on any exchange because we are currently using the confined Mainnet. The planned launch date for Pi is June 28, 2026.

Reselling to investors who want to hold until the mainnet launch in 2026 is currently the sole way to sell.

Consequently, right now. All you need to do is select the right pi network provider.

Who is a pi merchant?

An individual who buys coins from miners on the pi network and resells them to investors hoping to hang onto them until the mainnet is launched is known as a pi merchant.

debuts.

I'll provide you the Telegram username

@Pi_vendor_247

Exploring Abhay Bhutada’s Views After Poonawalla Fincorp’s Collaboration With...beulahfernandes8

The financial landscape in India has witnessed a significant development with the recent collaboration between Poonawalla Fincorp and IndusInd Bank.

The launch of the co-branded credit card, the IndusInd Bank Poonawalla Fincorp eLITE RuPay Platinum Credit Card, marks a major milestone for both entities.

This strategic move aims to redefine and elevate the banking experience for customers.

If you are looking for a pi coin investor. Then look no further because I have the right one he is a pi vendor (he buy and resell to whales in China). I met him on a crypto conference and ever since I and my friends have sold more than 10k pi coins to him And he bought all and still want more. I will drop his telegram handle below just send him a message.

@Pi_vendor_247

What website can I sell pi coins securely.DOT TECH

Currently there are no website or exchange that allow buying or selling of pi coins..

But you can still easily sell pi coins, by reselling it to exchanges/crypto whales interested in holding thousands of pi coins before the mainnet launch.

Who is a pi merchant?

A pi merchant is someone who buys pi coins from miners and resell to these crypto whales and holders of pi..

This is because pi network is not doing any pre-sale. The only way exchanges can get pi is by buying from miners and pi merchants stands in between the miners and the exchanges.

How can I sell my pi coins?

Selling pi coins is really easy, but first you need to migrate to mainnet wallet before you can do that. I will leave the telegram contact of my personal pi merchant to trade with.

Tele-gram.

@Pi_vendor_247

Empowering the Unbanked: The Vital Role of NBFCs in Promoting Financial Inclu...Vighnesh Shashtri

In India, financial inclusion remains a critical challenge, with a significant portion of the population still unbanked. Non-Banking Financial Companies (NBFCs) have emerged as key players in bridging this gap by providing financial services to those often overlooked by traditional banking institutions. This article delves into how NBFCs are fostering financial inclusion and empowering the unbanked.

Even tho Pi network is not listed on any exchange yet.

Buying/Selling or investing in pi network coins is highly possible through the help of vendors. You can buy from vendors[ buy directly from the pi network miners and resell it]. I will leave the telegram contact of my personal vendor.

@Pi_vendor_247

how can i use my minded pi coins I need some funds.DOT TECH

If you are interested in selling your pi coins, i have a verified pi merchant, who buys pi coins and resell them to exchanges looking forward to hold till mainnet launch.

Because the core team has announced that pi network will not be doing any pre-sale. The only way exchanges like huobi, bitmart and hotbit can get pi is by buying from miners.

Now a merchant stands in between these exchanges and the miners. As a link to make transactions smooth. Because right now in the enclosed mainnet you can't sell pi coins your self. You need the help of a merchant,

i will leave the telegram contact of my personal pi merchant below. 👇 I and my friends has traded more than 3000pi coins with him successfully.

@Pi_vendor_247

how to swap pi coins to foreign currency withdrawable.DOT TECH

As of my last update, Pi is still in the testing phase and is not tradable on any exchanges.

However, Pi Network has announced plans to launch its Testnet and Mainnet in the future, which may include listing Pi on exchanges.

The current method for selling pi coins involves exchanging them with a pi vendor who purchases pi coins for investment reasons.

If you want to sell your pi coins, reach out to a pi vendor and sell them to anyone looking to sell pi coins from any country around the globe.

Below is the contact information for my personal pi vendor.

Telegram: @Pi_vendor_247

Turin Startup Ecosystem 2024 - Ricerca sulle Startup e il Sistema dell'Innov...Quotidiano Piemontese

Turin Startup Ecosystem 2024

Una ricerca de il Club degli Investitori, in collaborazione con ToTeM Torino Tech Map e con il supporto della ESCP Business School e di Growth Capital

Poonawalla Fincorp and IndusInd Bank Introduce New Co-Branded Credit Cardnickysharmasucks

The unveiling of the IndusInd Bank Poonawalla Fincorp eLITE RuPay Platinum Credit Card marks a notable milestone in the Indian financial landscape, showcasing a successful partnership between two leading institutions, Poonawalla Fincorp and IndusInd Bank. This co-branded credit card not only offers users a plethora of benefits but also reflects a commitment to innovation and adaptation. With a focus on providing value-driven and customer-centric solutions, this launch represents more than just a new product—it signifies a step towards redefining the banking experience for millions. Promising convenience, rewards, and a touch of luxury in everyday financial transactions, this collaboration aims to cater to the evolving needs of customers and set new standards in the industry.

Poonawalla Fincorp and IndusInd Bank Introduce New Co-Branded Credit Card

Form 1040A-Individual Income Tax Return - Short Form

1. Form Department of the Treasury—Internal Revenue Service

1040A 2008

U.S. Individual Income Tax Return IRS Use Only—Do not write or staple in this space.

(99)

OMB No. 1545-0074

Your first name and initial Last name

Label Your social security number

L

(See page 17.)

A

B

Spouse’s social security number

If a joint return, spouse’s first name and initial Last name

E

Use the L

IRS label. H Home address (number and street). If you have a P.O. box, see page 17. Apt. no. You must enter

E

Otherwise, your SSN(s) above.

R

please print

E

or type. City, town or post office, state, and ZIP code. If you have a foreign address, see page 17.

Checking a box below will not

change your tax or refund.

Presidential

Election Campaign Check here if you, or your spouse if filing jointly, want $3 to go to this fund (see page 17) Spouse

You

1 Single 4 Head of household (with qualifying person). (See page 18.)

Filing

If the qualifying person is a child but not your dependent,

2 Married filing jointly (even if only one had income)

status enter this child’s name here.

Married filing separately. Enter spouse’s SSN above and

3

Check only

one box. 5 Qualifying widow(er) with dependent child (see page 19)

full name here.

Boxes

6a Yourself. If someone can claim you as a dependent, do not check

Exemptions checked on

box 6a. 6a and 6b

b Spouse No. of children

on 6c who:

(4) if qualifying

c Dependents: (3) Dependent’s

(2) Dependent’s social ● lived with

child for child

relationship to you

tax credit (see

security number

(1) First name Last name you page 20)

● did not live

If more than six

dependents, with you due

to divorce or

see page 20.

separation

(see page 21)

Dependents

on 6c not

entered above

Add numbers

on lines

d Total number of exemptions claimed. above

Income

7 Wages, salaries, tips, etc. Attach Form(s) W-2. 7

Attach

Form(s) W-2

8a Taxable interest. Attach Schedule 1 if required. 8a

here. Also

bTax-exempt interest. Do not include on line 8a. 8b

attach

Form(s) 9a Ordinary dividends. Attach Schedule 1 if required. 9a

1099-R if tax bQualified dividends (see page 24). 9b

was withheld.

10 Capital gain distributions (see page 24). 10

11a IRA 11b Taxable amount

If you did not

get a W-2, see

distributions. (see page 24).

11a 11b

page 23.

12a Pensions and 12b Taxable amount

Enclose, but do annuities. (see page 25).

12a 12b

not attach, any

payment.

13 Unemployment compensation and Alaska Permanent Fund dividends. 13

14a Social security 14b Taxable amount

benefits. (see page 27).

14a 14b

15 Add lines 7 through 14b (far right column). This is your total income. 15

Adjusted

16 Educator expenses (see page 29). 16

gross

17 IRA deduction (see page 29). 17

income

18 Student loan interest deduction (see page 31). 18

19 Tuition and fees deduction. Attach Form 8917. 19

20 Add lines 16 through 19. These are your total adjustments. 20

21

21 Subtract line 20 from line 15. This is your adjusted gross income.

For Disclosure, Privacy Act, and Paperwork Reduction Act Notice, see page 78. Form 1040A (2008)

Cat. No. 11327A

2. Form 1040A (2008) Page 2

22 Enter the amount from line 21 (adjusted gross income). 22

Tax,

23a Check You were born before January 2, 1944, Blind Total boxes

credits, if: Spouse was born before January 2, 1944, Blind checked 23a

and

b If you are married filing separately and your spouse itemizes

payments deductions, see page 32 and check here 23b

Standard c Check if standard deduction includes real estate taxes (see page 32) 23c

Deduction

24 Enter your standard deduction (see left margin). 24

for—

● People who 25 Subtract line 24 from line 22. If line 24 is more than line 22, enter -0-. 25

checked any 26 If line 22 is over $119,975, or you provided housing to a Midwestern

box on line

displaced individual, see page 32. Otherwise, multiply $3,500 by the total

23a, 23b, or

number of exemptions claimed on line 6d.

23c or who 26

can be

27 Subtract line 26 from line 25. If line 26 is more than line 25, enter -0-.

claimed as a

This is your taxable income. 27

dependent,

see page 32.

28 Tax, including any alternative minimum tax (see page 33). 28

● All others:

29 Credit for child and dependent care expenses.

Single or

Attach Schedule 2. 29

Married filing

30 Credit for the elderly or the disabled. Attach

separately,

$5,450

Schedule 3. 30

Married filing

31 Education credits. Attach Form 8863. 31

jointly or

32 Retirement savings contributions credit. Attach Form 8880. 32

Qualifying

widow(er),

33 Child tax credit (see page 37). Attach

$10,900

33

Form 8901 if required.

Head of

34 Add lines 29 through 33. These are your total credits. 34

household,

$8,000 35 Subtract line 34 from line 28. If line 34 is more than line 28, enter -0-. 35

36 Advance earned income credit payments from Form(s) W-2, box 9. 36

37 Add lines 35 and 36. This is your total tax. 37

38 Federal income tax withheld from Forms W-2 and 1099. 38

39 2008 estimated tax payments and amount

applied from 2007 return. 39

If you have

a qualifying

child, attach 40a Earned income credit (EIC). 40a

b Nontaxable combat pay election. 40b

Schedule

EIC. 41

41 Additional child tax credit. Attach Form 8812.

42 Recovery rebate credit (see worksheet on pages 53 and 54). 42

43 Add lines 38, 39, 40a, 41, and 42. These are your total payments. 43

44 If line 43 is more than line 37, subtract line 37 from line 43.

Refund

44

This is the amount you overpaid.

Direct 45a Amount of line 44 you want refunded to you. If Form 8888 is attached, check here 45a

deposit?

b Routing

See page 55

c Type: Checking Savings

number

and fill in

45b, 45c,

d Account

and 45d or

number

Form 8888.

46 Amount of line 44 you want applied to your

2009 estimated tax. 46

47 Amount you owe. Subtract line 43 from line 37. For details on how

Amount

to pay, see page 56. 47

you owe

48 Estimated tax penalty (see page 57). 48

Do you want to allow another person to discuss this return with the IRS (see page 57)? Yes. Complete the following. No

Third party

Designee’s Phone Personal identification

designee ( )

name no. number (PIN)

Under penalties of perjury, I declare that I have examined this return and accompanying schedules and statements, and to the best of my

Sign knowledge and belief, they are true, correct, and accurately list all amounts and sources of income I received during the tax year. Declaration

here of preparer (other than the taxpayer) is based on all information of which the preparer has any knowledge.

Your occupation Daytime phone number

Your signature Date

Joint return?

See page 17. ( )

Keep a copy Spouse’s signature. If a joint return, both must sign. Date Spouse’s occupation

for your

records.

Date Preparer’s SSN or PTIN

Paid Preparer’s Check if

signature self-employed

preparer’s Firm’s name (or EIN

use only yours if self-employed),

( )

address, and ZIP code Phone no.

Form 1040A (2008)