Download to read offline

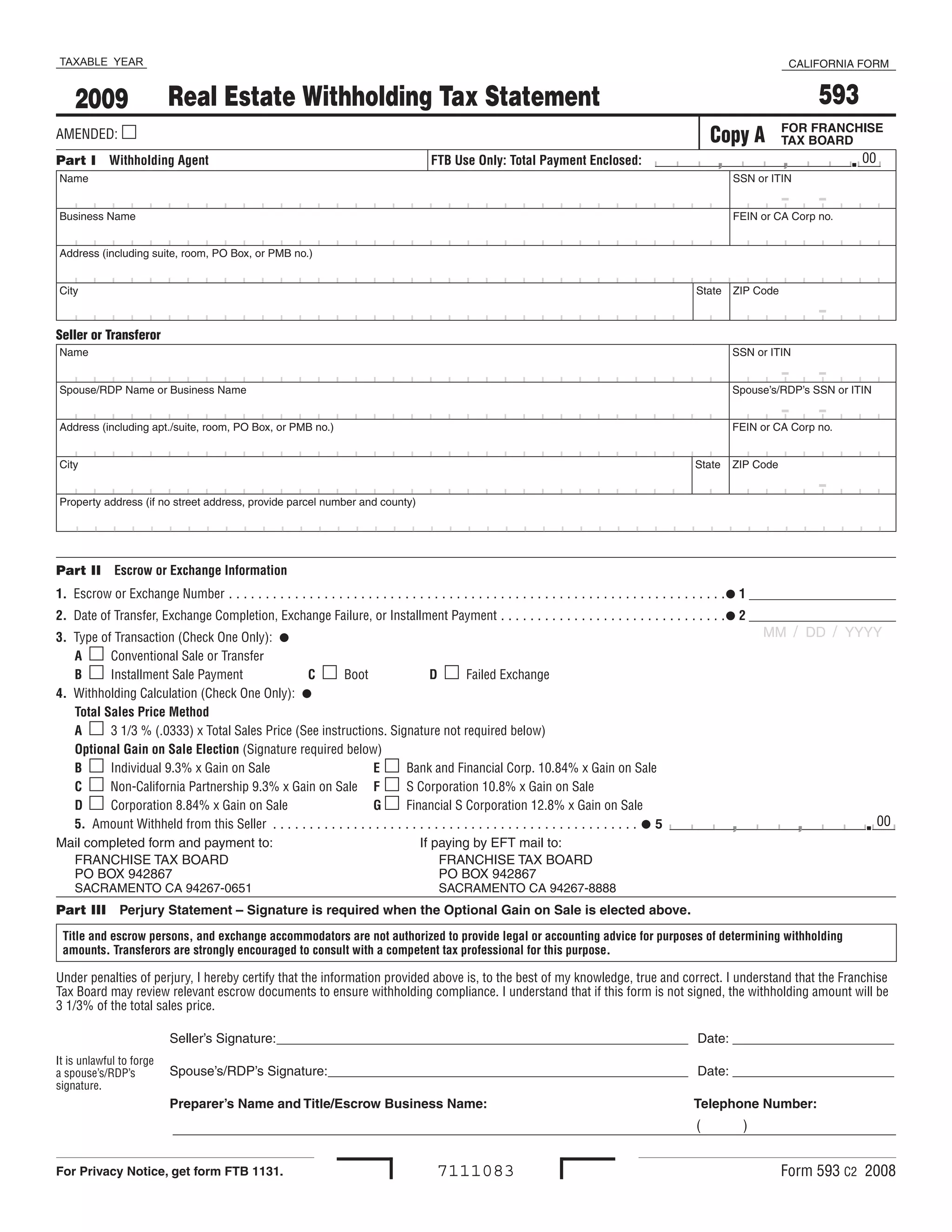

This document is a California Form 593 for real estate withholding tax. It contains information about the withholding agent, seller or transferor, escrow or exchange details, and transaction details. The form requires the seller to sign a perjury statement if electing an optional gain on sale calculation method rather than the default 3 1/3% of total sales price withholding amount.

![Independent Consultant Application & Agreement[1]](https://cdn.slidesharecdn.com/ss_thumbnails/IndependentConsultantApplicationAgreement1-123601947622-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)