Downloaded 92 times

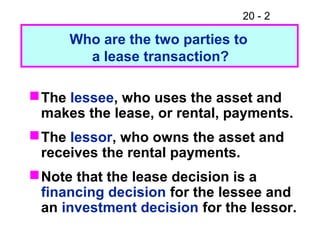

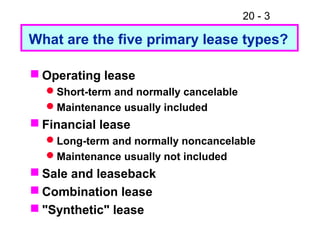

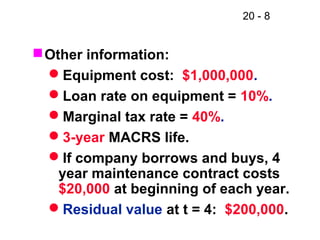

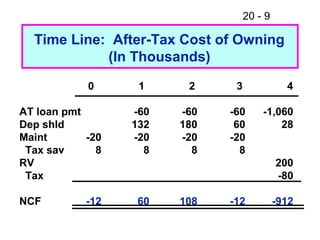

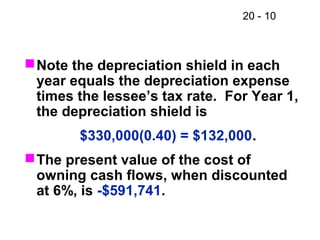

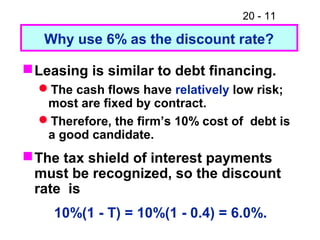

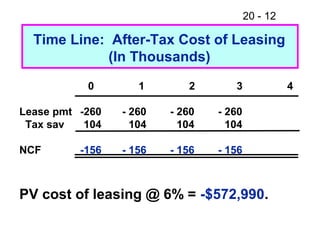

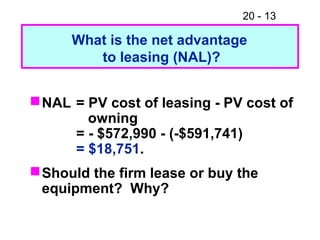

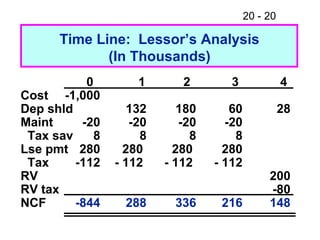

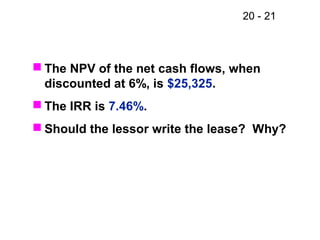

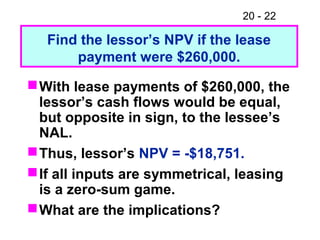

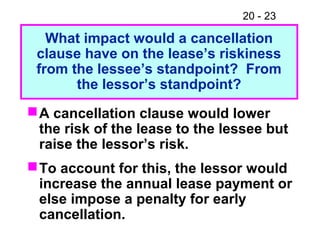

This document discusses key aspects of lease financing including: - The two parties to a lease are the lessee who uses the asset and makes payments, and the lessor who owns the asset and receives payments. - There are five primary lease types: operating, financial, sale and leaseback, combination, and synthetic. - Leases are classified for tax and accounting purposes, which affects the financial analysis. - The analysis compares the net present value of costs for the lessee to lease versus own an asset, considering factors like depreciation, interest, and residual value.