Downloaded 106 times

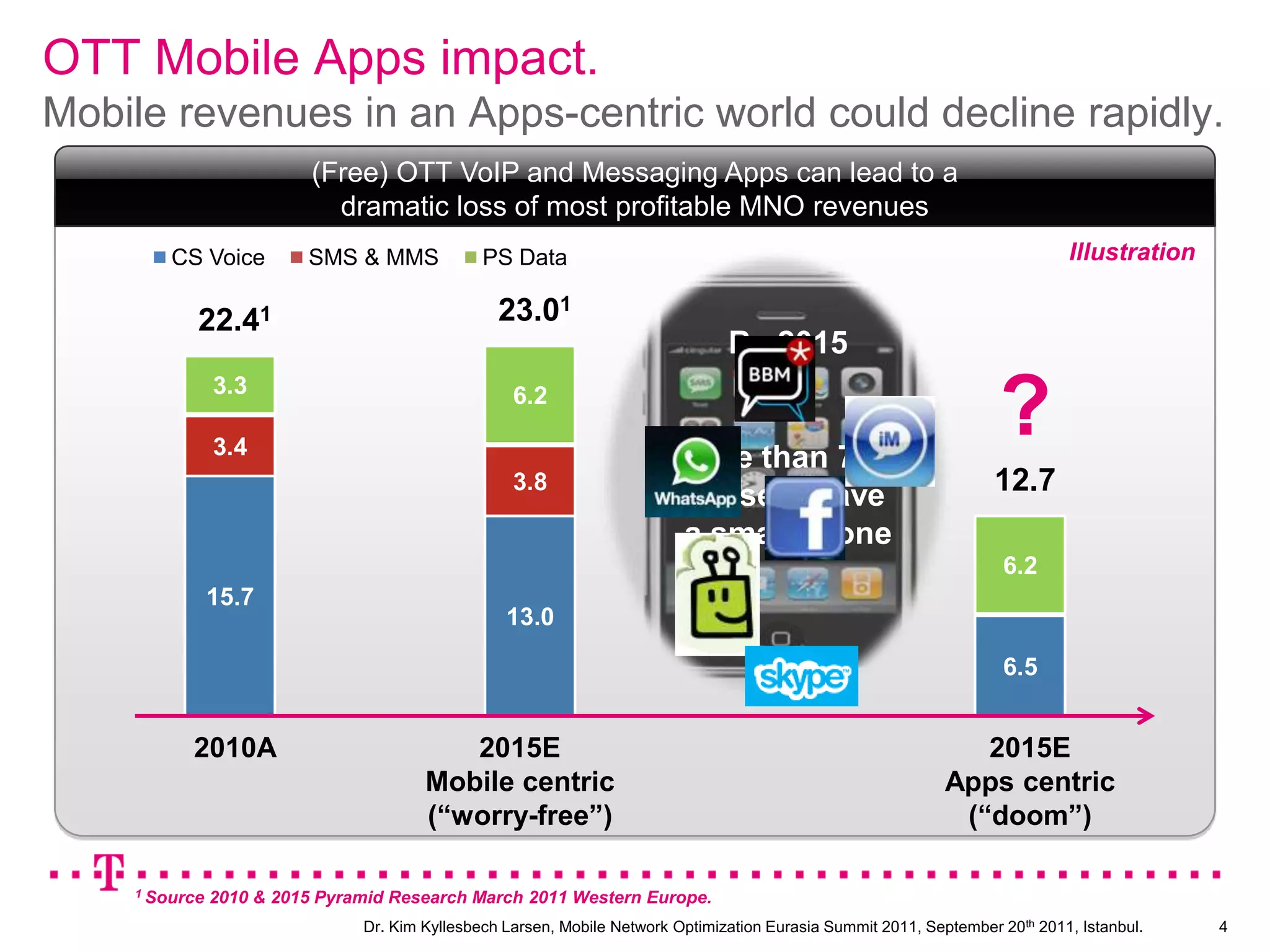

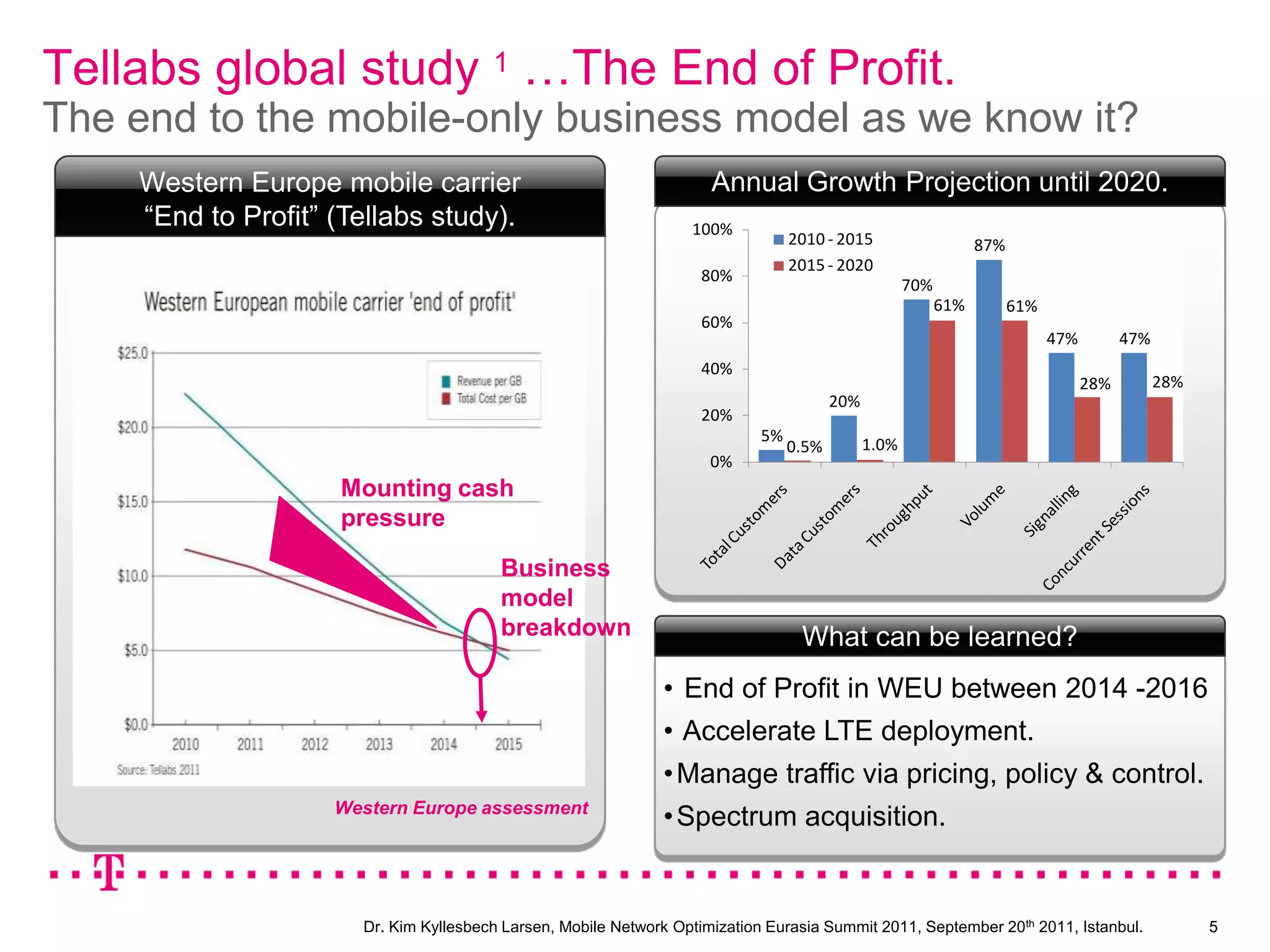

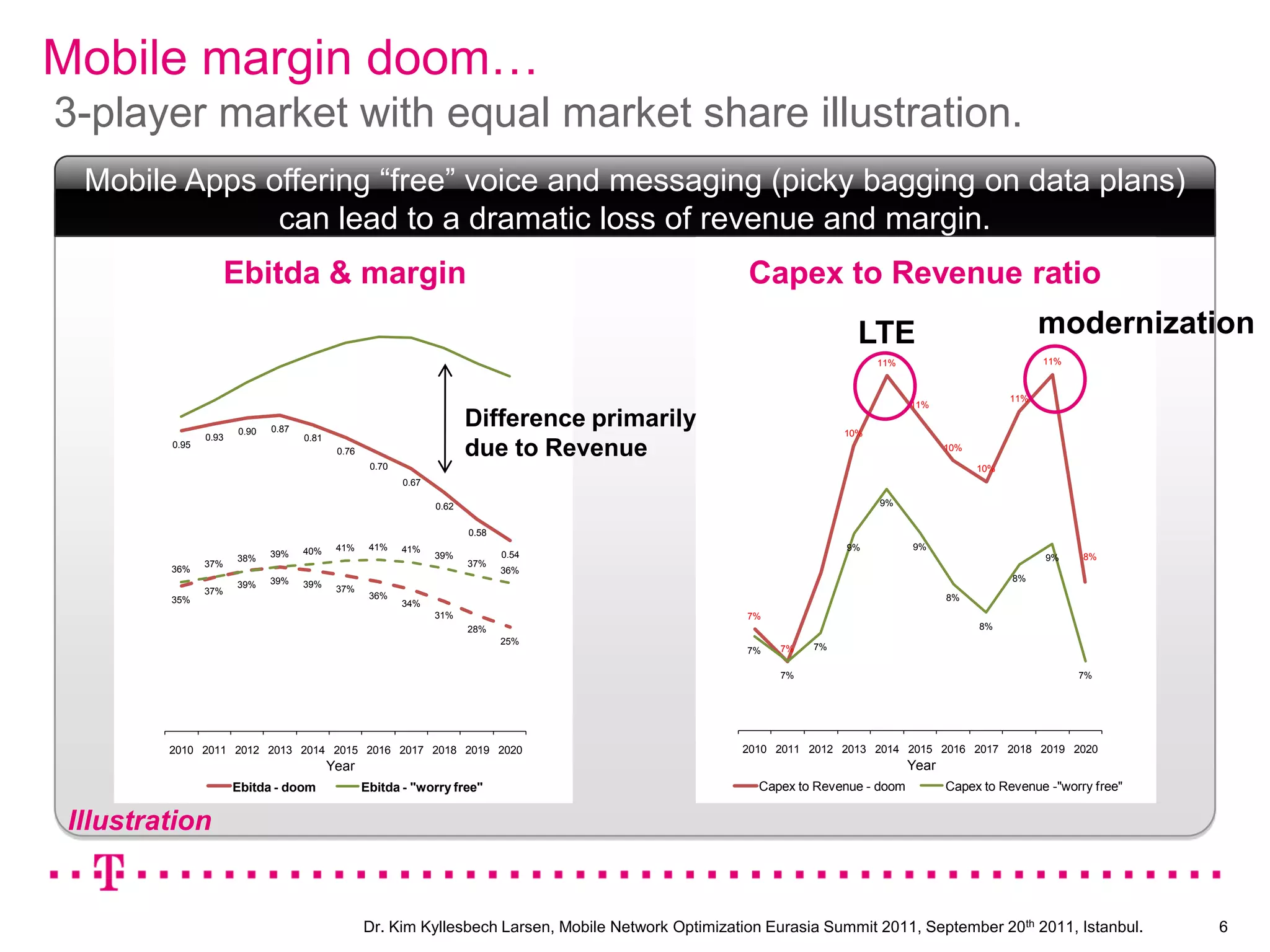

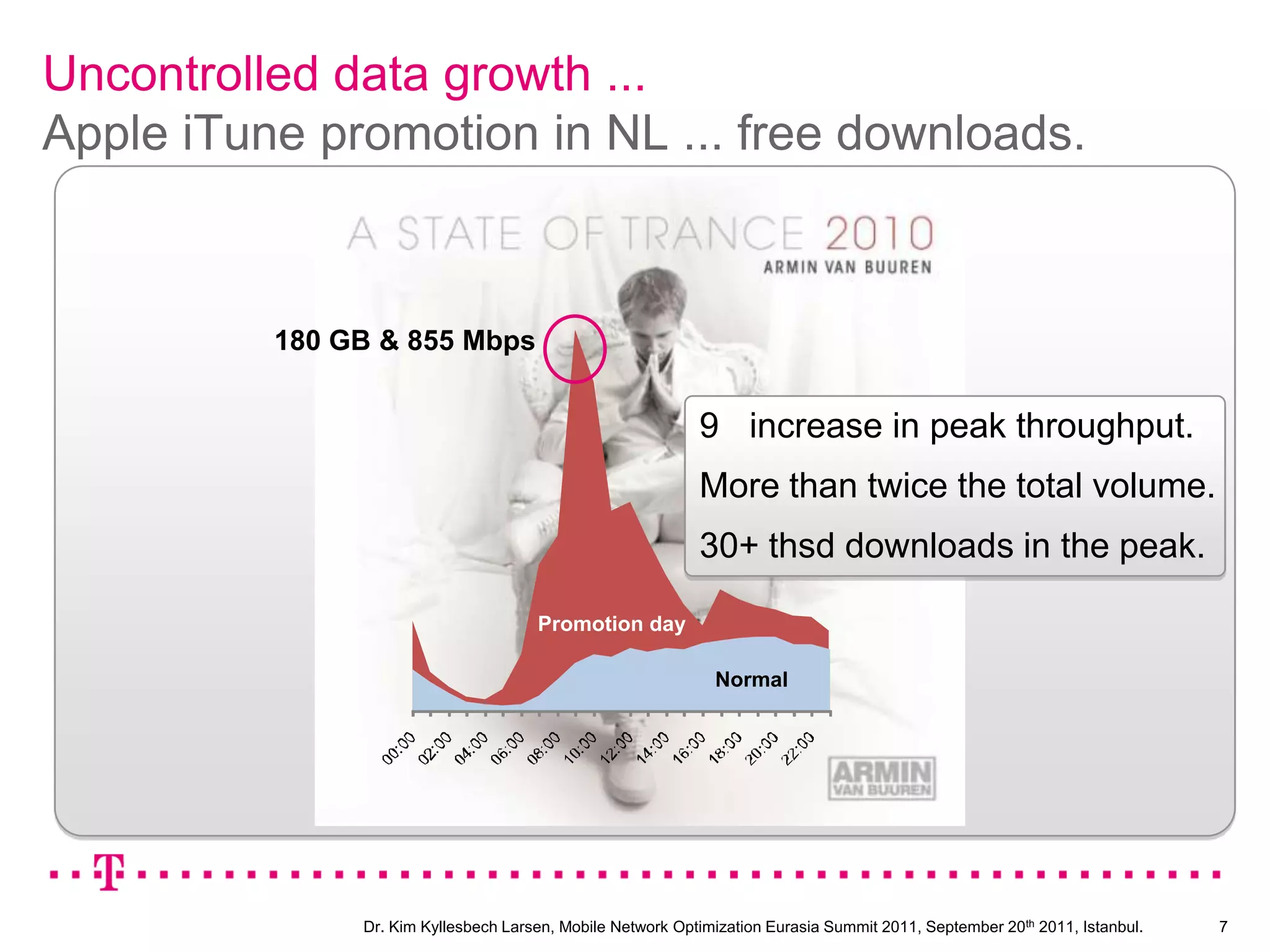

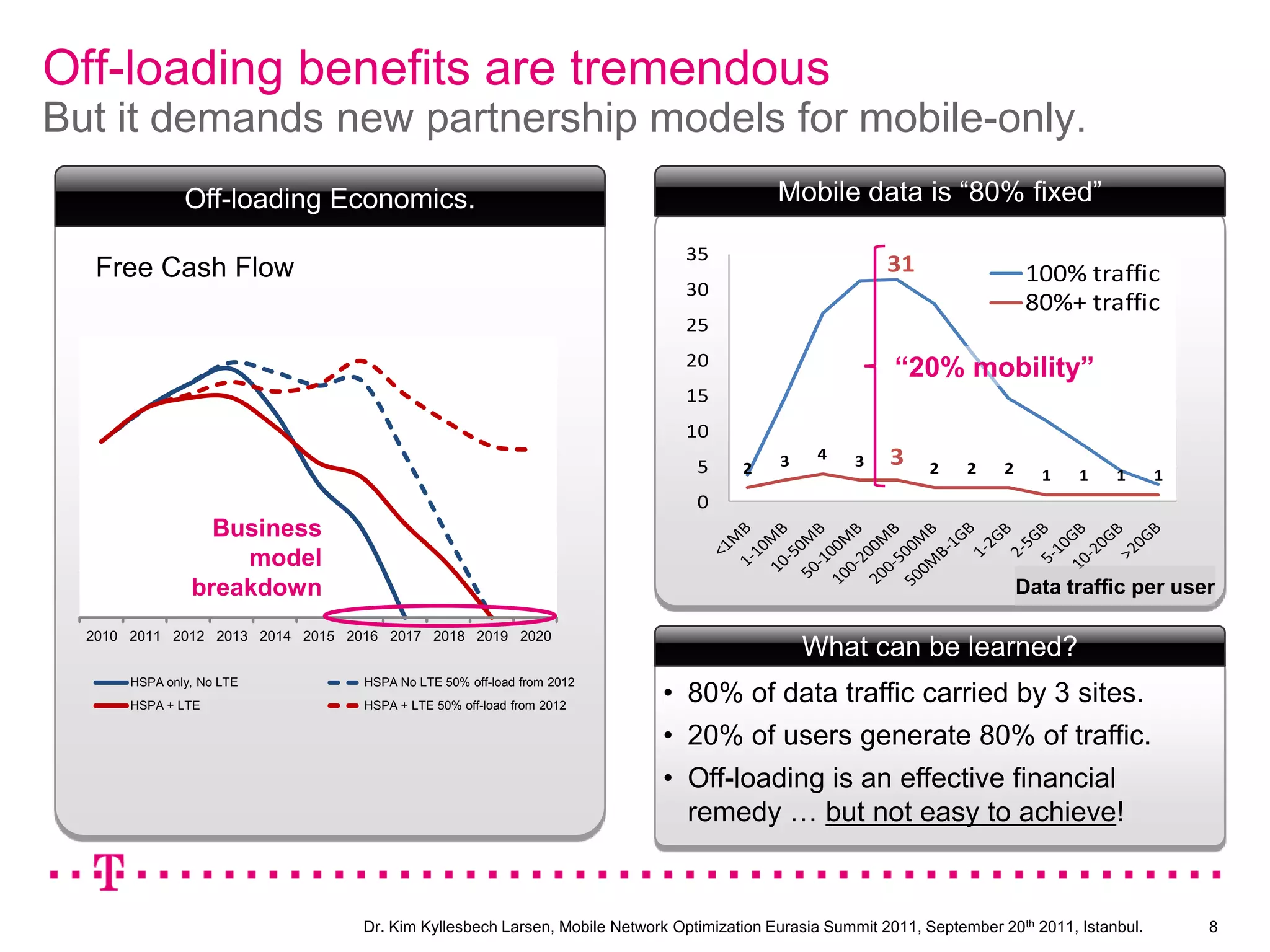

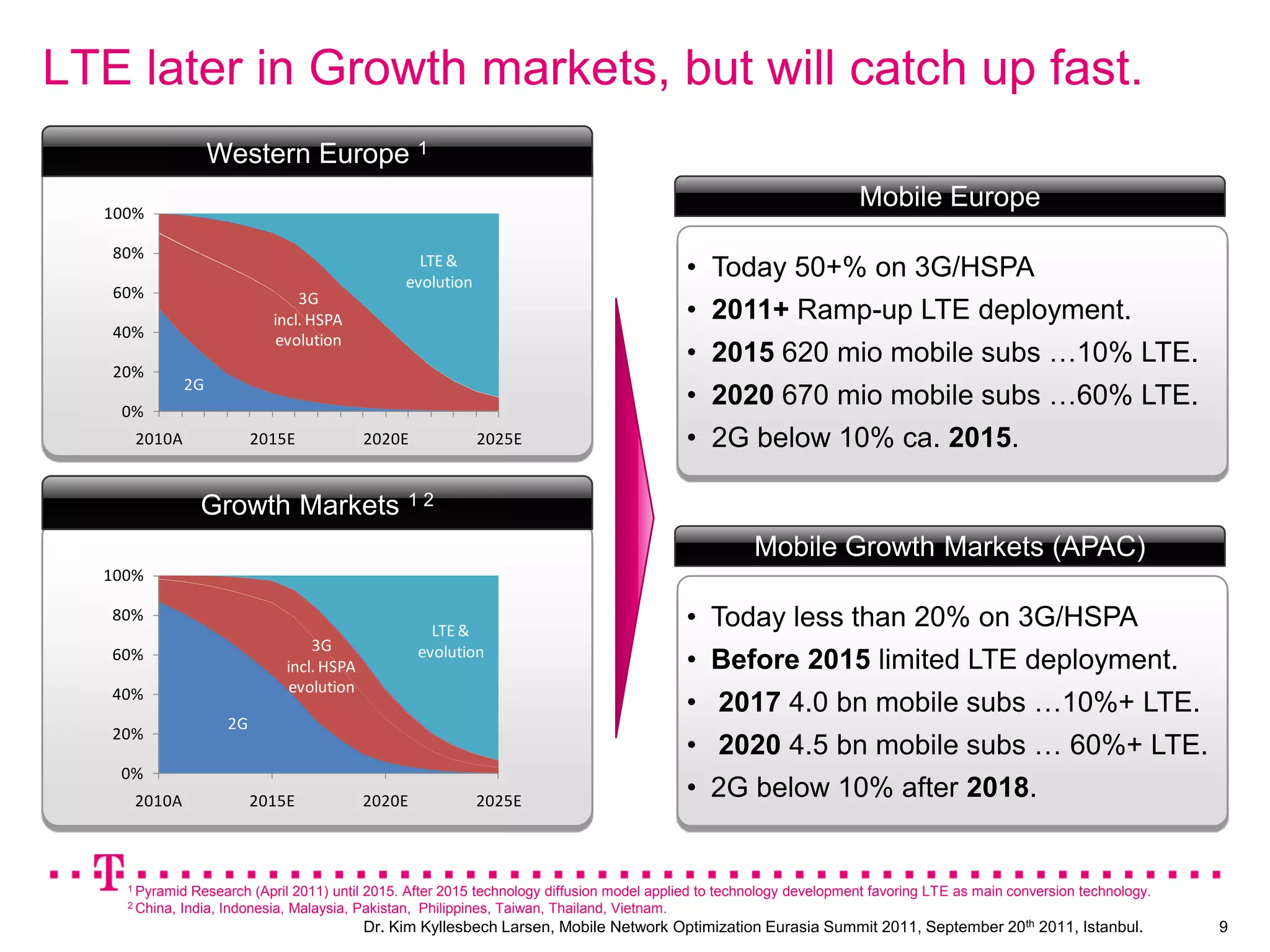

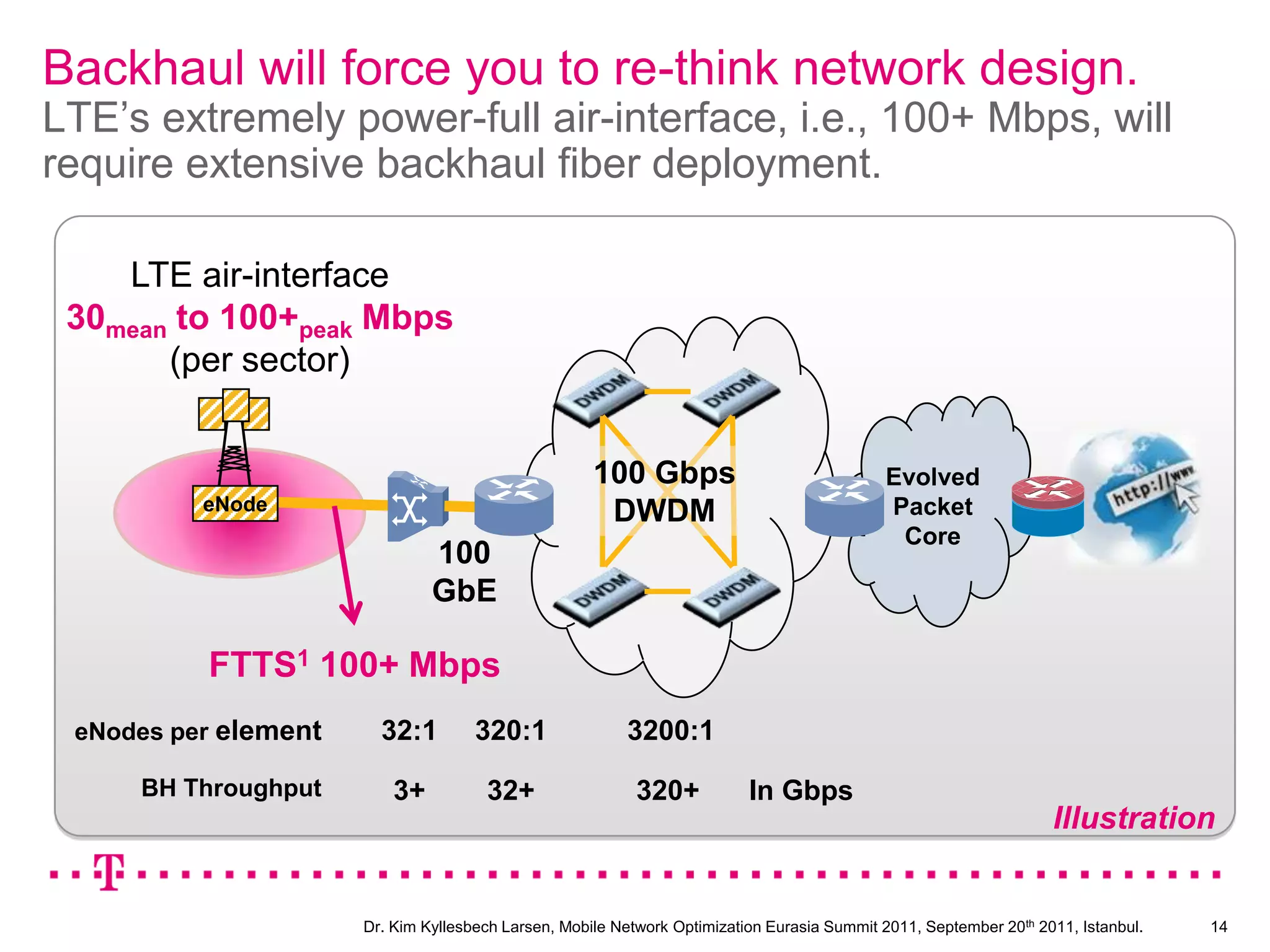

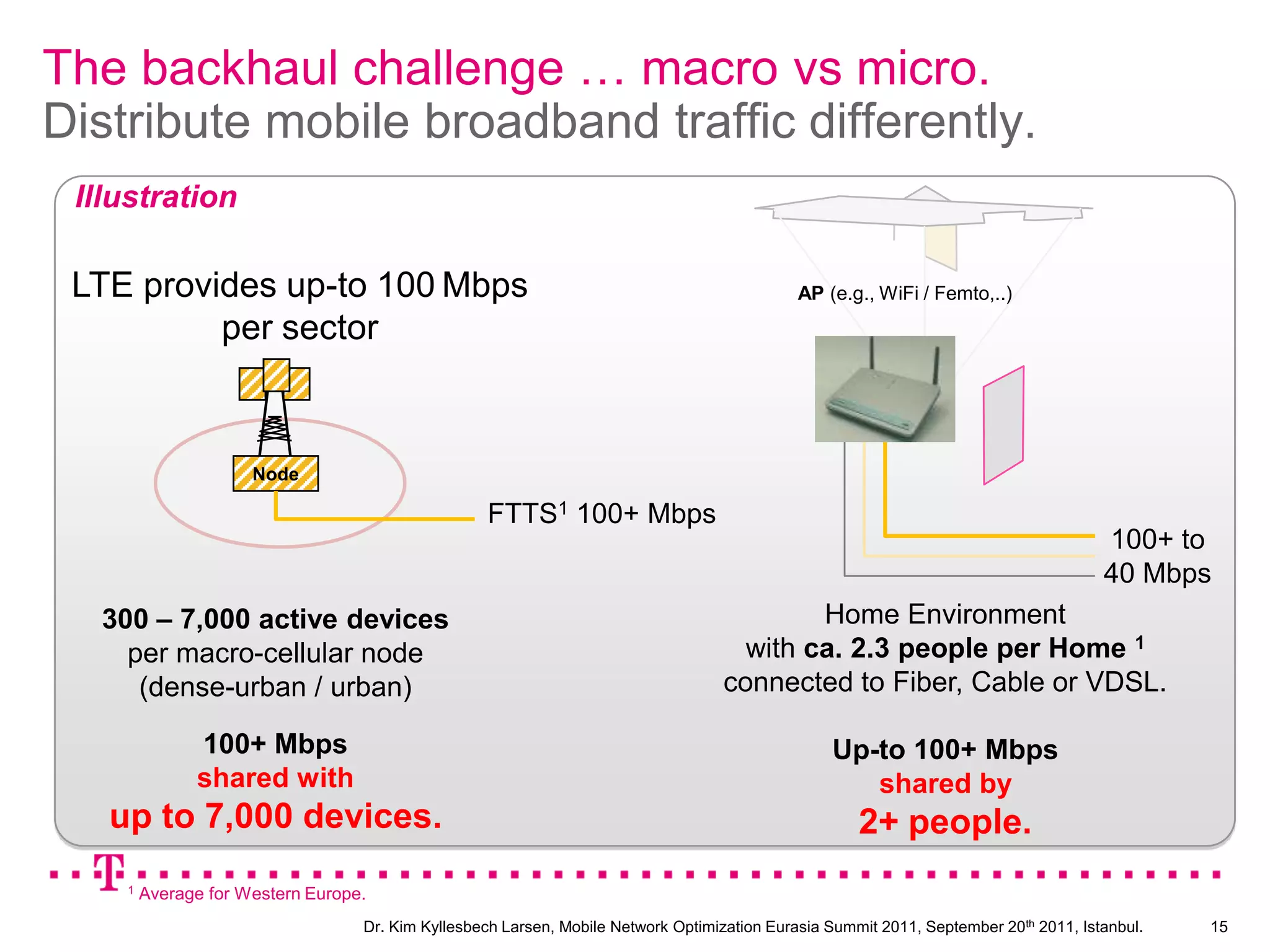

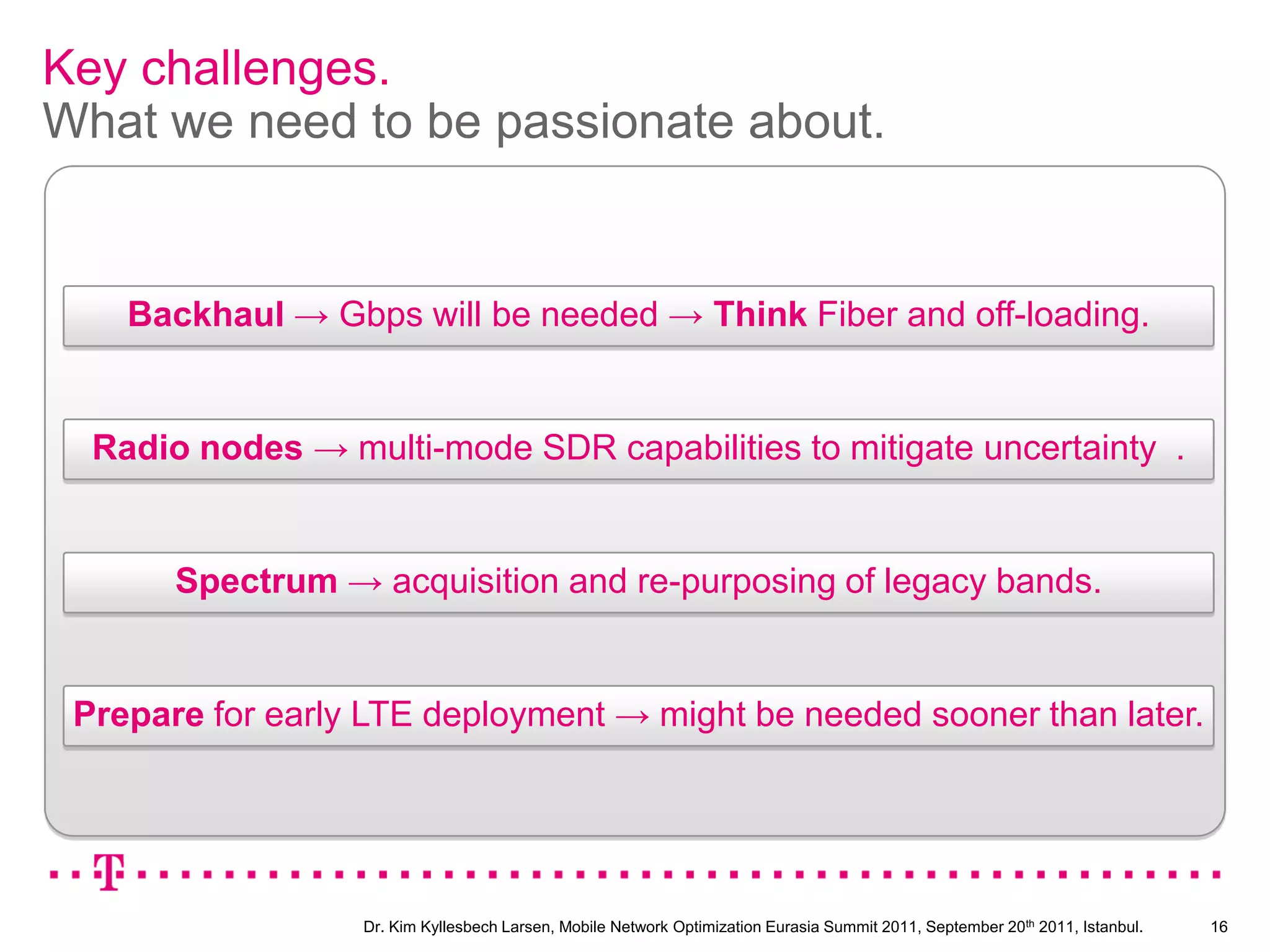

This document discusses the challenges facing mobile networks from increasing data usage and new applications. Smartphones and apps are driving more data consumption, which could reduce mobile revenues if voice and messaging apps allow free use of these services. Deploying 4G LTE networks requires additional spectrum, fiber backhaul to support high speeds, and new infrastructure like small cells. Offloading data to fixed networks can help financially but requires cooperation. Preparing for early LTE deployment may be needed to manage these challenges to the mobile business model.