Downloaded 11 times

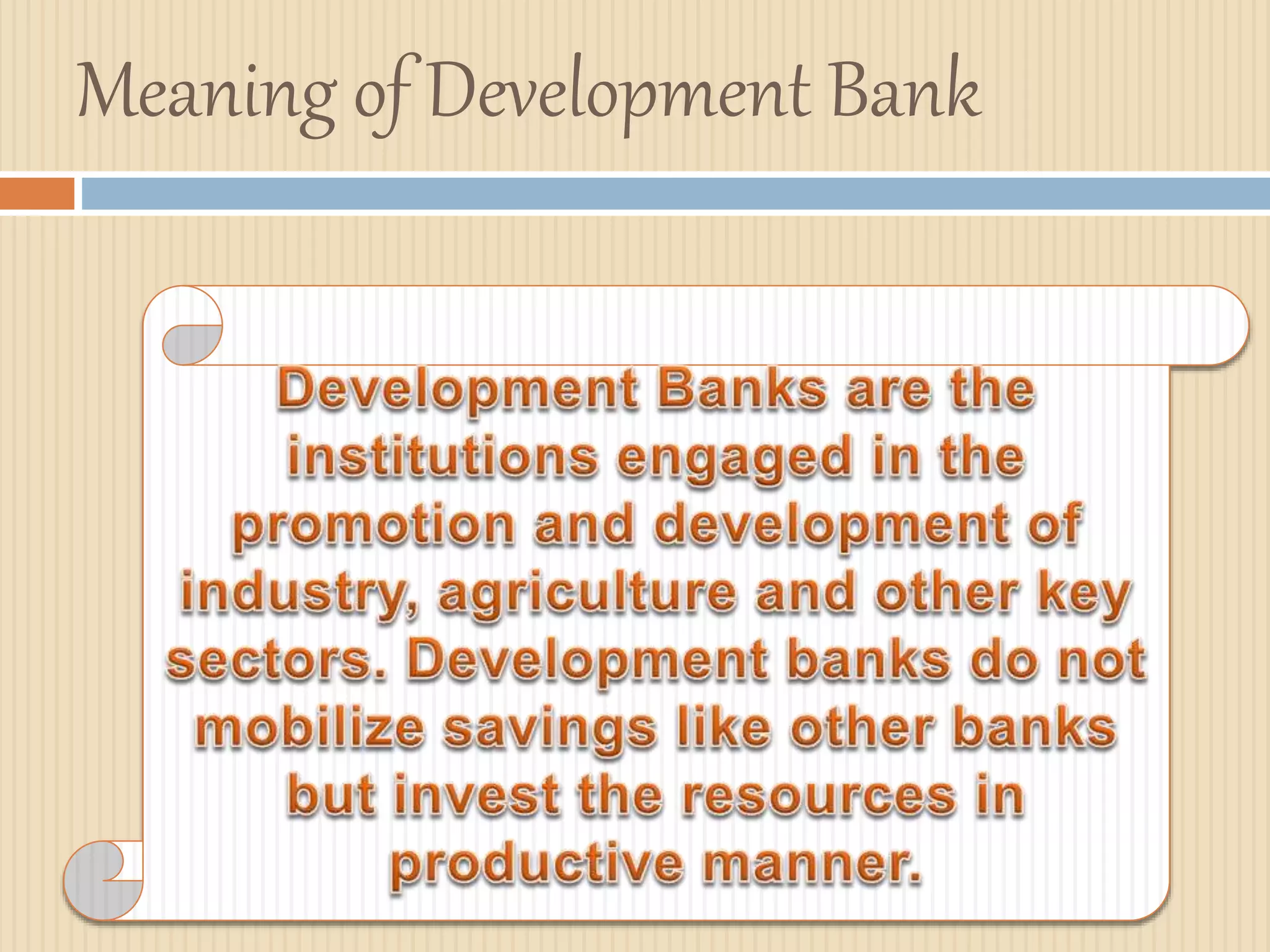

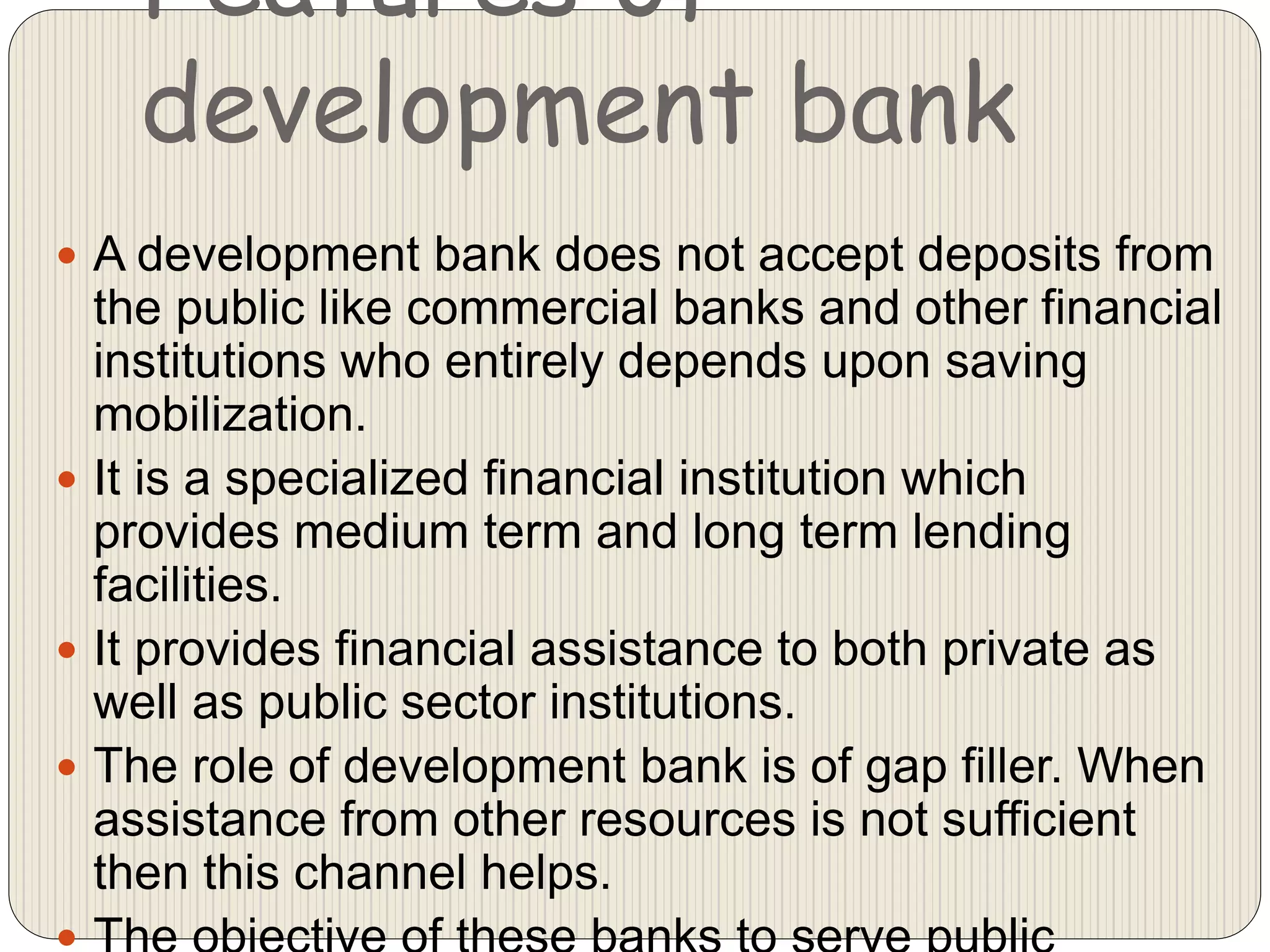

This document outlines the key aspects of development banks, including their definition, features, and lending procedures. It defines a development bank as a financial institution that provides both medium and long-term financing to businesses through loans, underwriting, investments, and other means to promote economic and industrial development. Development banks differ from commercial banks in that they do not accept deposits from the public. Their lending procedures involve thorough technical, economic, commercial, and financial appraisals of projects as well as assessments of managerial competence and national contribution before sanctioning and disbursing loans. Development banks play an important role in a country's economic development.