Downloaded 167 times

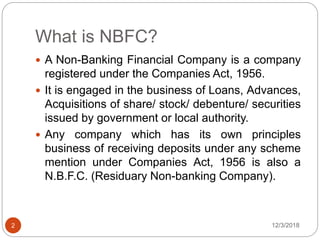

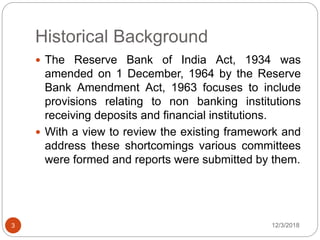

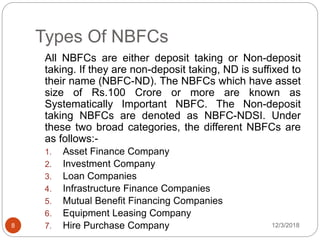

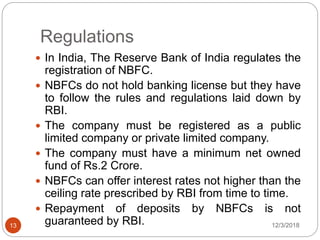

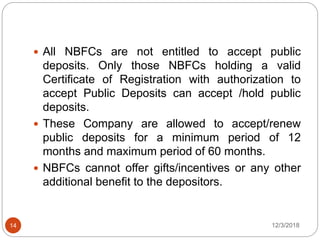

Non-banking financial companies (NBFCs) are financial institutions registered under the Companies Act and engaged in lending and investment activities. The document discusses the history and regulation of NBFCs in India. It outlines the various types of NBFCs and their roles in providing credit to sectors underserved by banks. While NBFCs cannot accept demand deposits like banks, they play an important role in developing industries and financing first-time buyers. The Reserve Bank of India regulates NBFC registration and prudential norms in India.