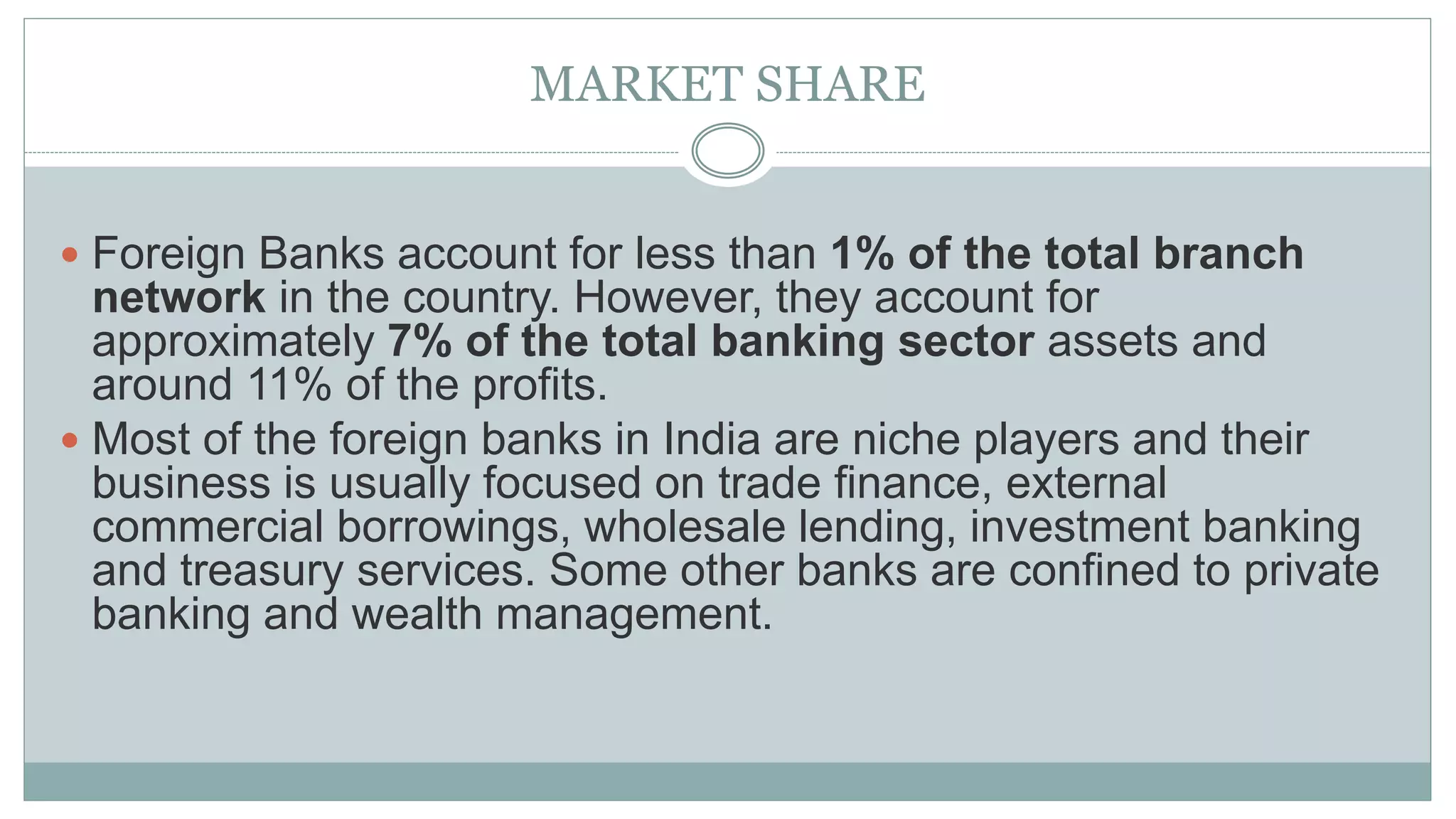

This document discusses foreign banks operating in India. It notes that foreign banks are defined as banks headquartered in another country operating in India through branches. There are currently 45 foreign banks operating 286 branches in India. While foreign banks account for under 1% of branches, they control around 7% of banking sector assets and 11% of profits. The document outlines the advantages of foreign banks like increased competition and innovation, and the disadvantages like domestic banks facing greater competition.