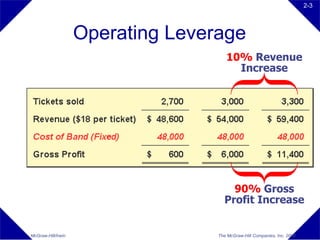

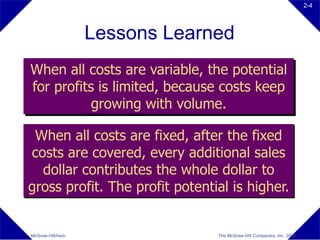

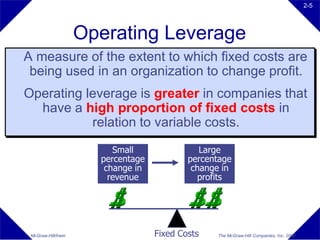

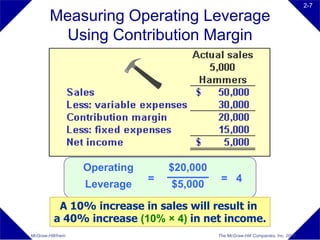

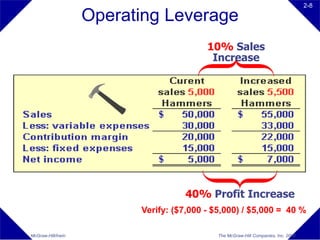

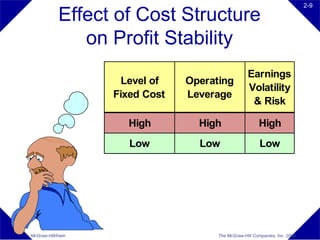

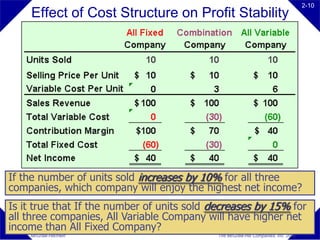

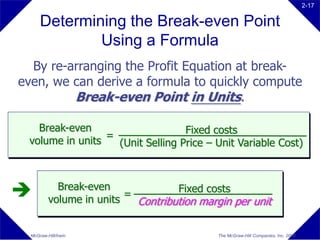

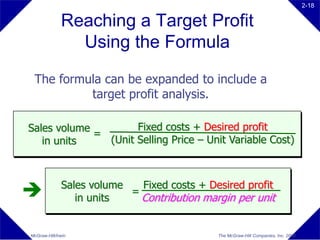

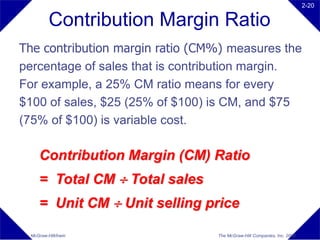

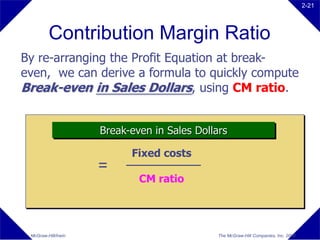

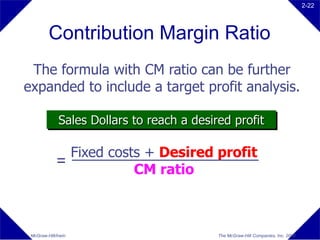

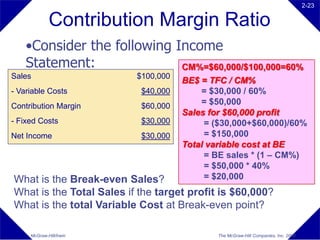

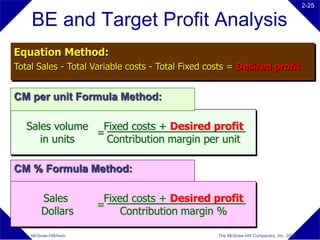

This document discusses cost-volume-profit (CVP) analysis and operating leverage. It defines key terms like contribution margin, break-even point, target profit, and operating leverage. It presents examples of how to calculate break-even point and sales required to meet a target profit using the equation method, contribution margin per unit formula, and contribution margin percentage formula. The document emphasizes that CVP analysis can be used to examine the profit impact of changes in costs, prices, and product mix.