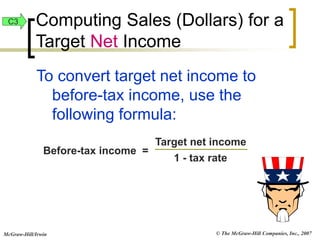

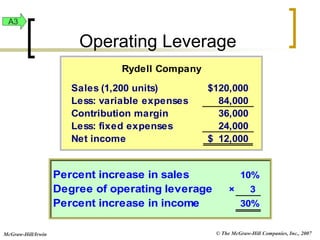

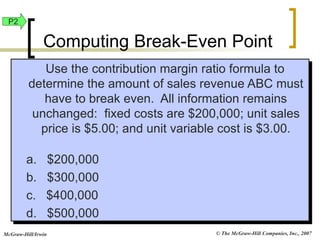

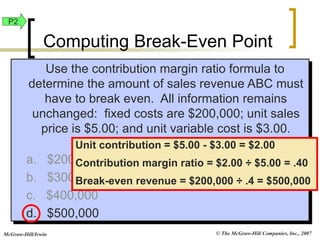

* Unit contribution margin is $5 - $3 = $2

* Contribution margin ratio is $2/$5 = 40%

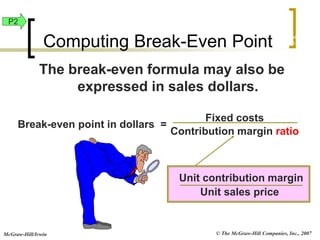

* Break-even point in sales dollars = Fixed costs / Contribution margin ratio

* = $200,000 / 40%

* = $200,000 / 0.4

* = $500,000

Therefore, the amount of sales revenue ABC must have to break even is $500,000.

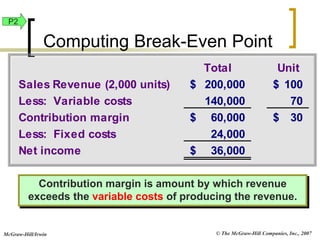

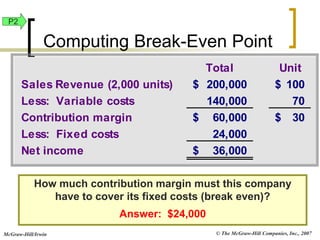

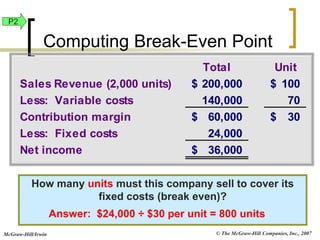

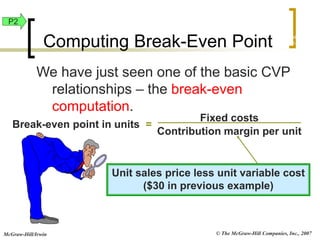

P2

Computing Break-Even Point

�© The McGraw-Hill Companies, Inc., 2007

McGraw-Hill/Irwin

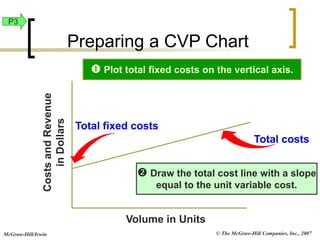

Break-even analysis is useful for:

- Determining the sales volume needed to earn a target profit

![© The McGraw-Hill Companies, Inc., 2007

McGraw-Hill/Irwin

Rydell expects to sell 1,500 units at $100

each next month. Fixed costs are $24,000

per month and the unit variable cost is

$70. What amount of income should

Rydell expect?

Income (pretax) = Sales – Variable costs – Fixed costs

= [1,500 units × $100] – [1,500 units × $70] – $24,000

= $21,000

Computing Income

from Expected Sales

Exh.

22-13

C3](https://image.slidesharecdn.com/mach05-230321094348-12390ca2/85/yrtyt-41-320.jpg)