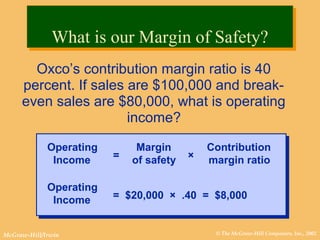

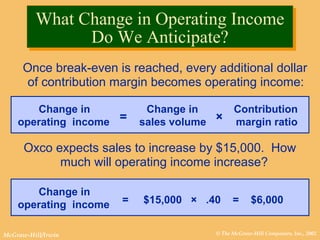

Operating income = $8,000 Oxco’s contribution margin ratio is 40 percent. If sales are $100,000 and break- even sales are $80,000, what is operating income? What is our Margin of Safety?