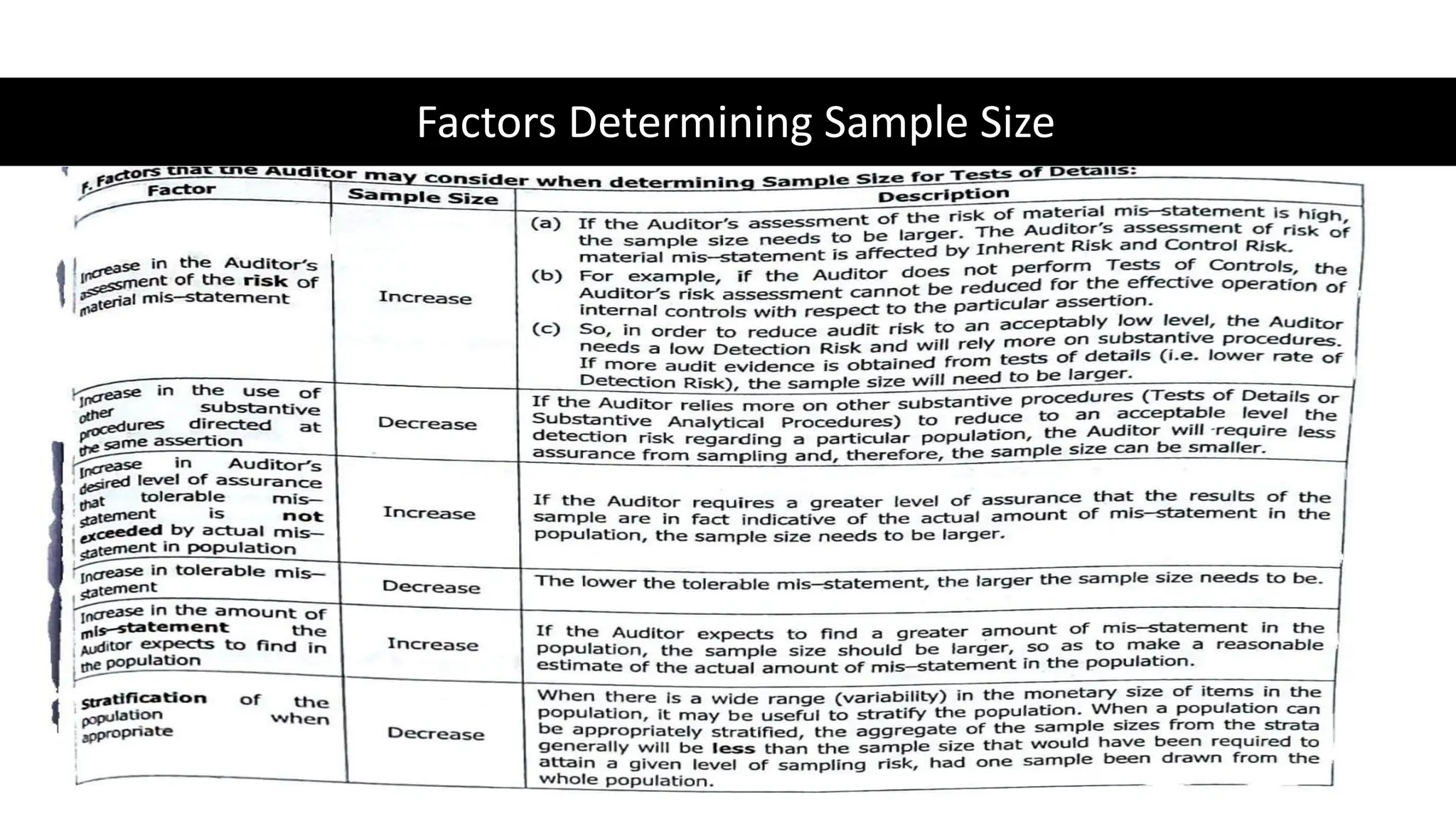

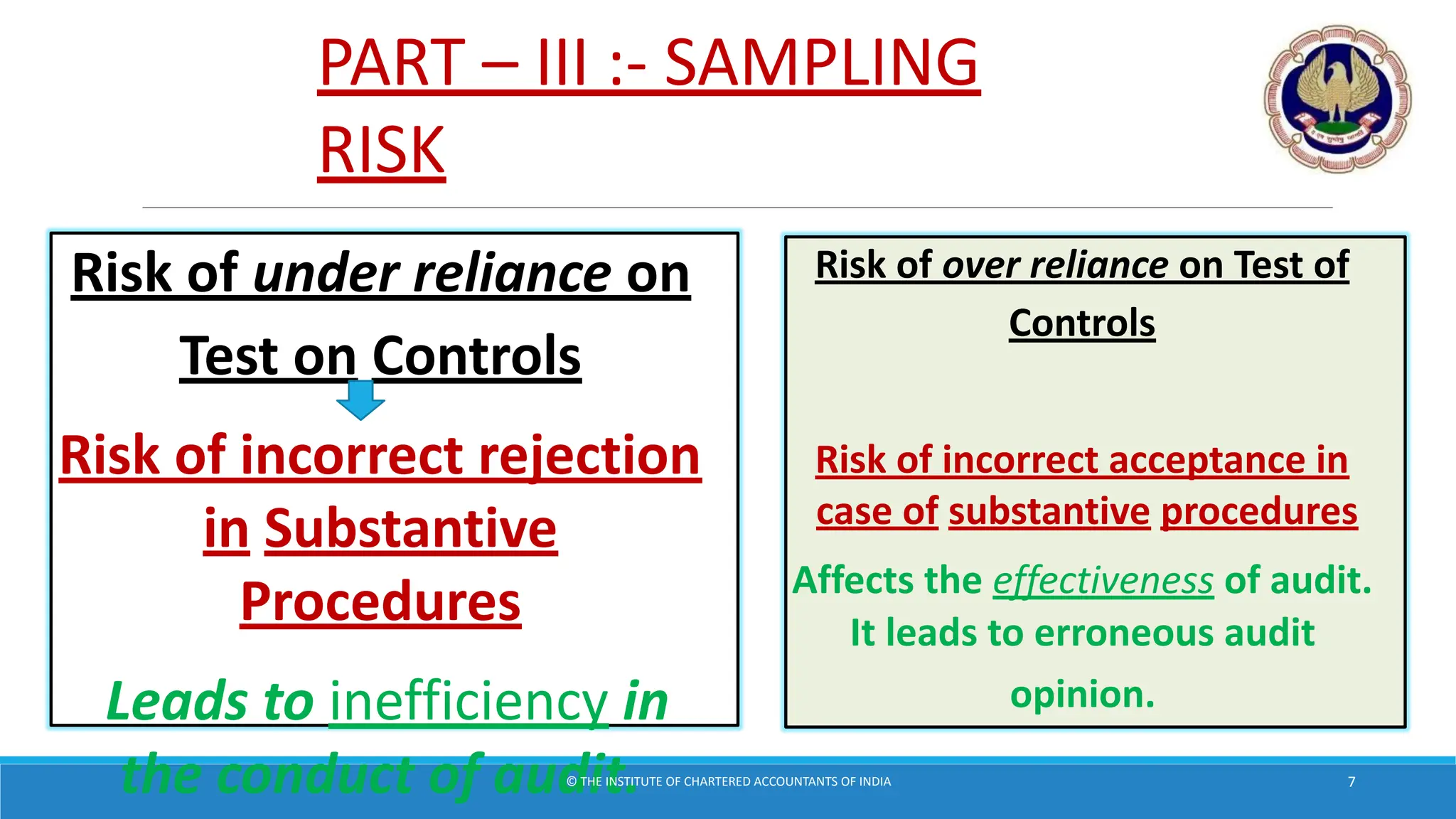

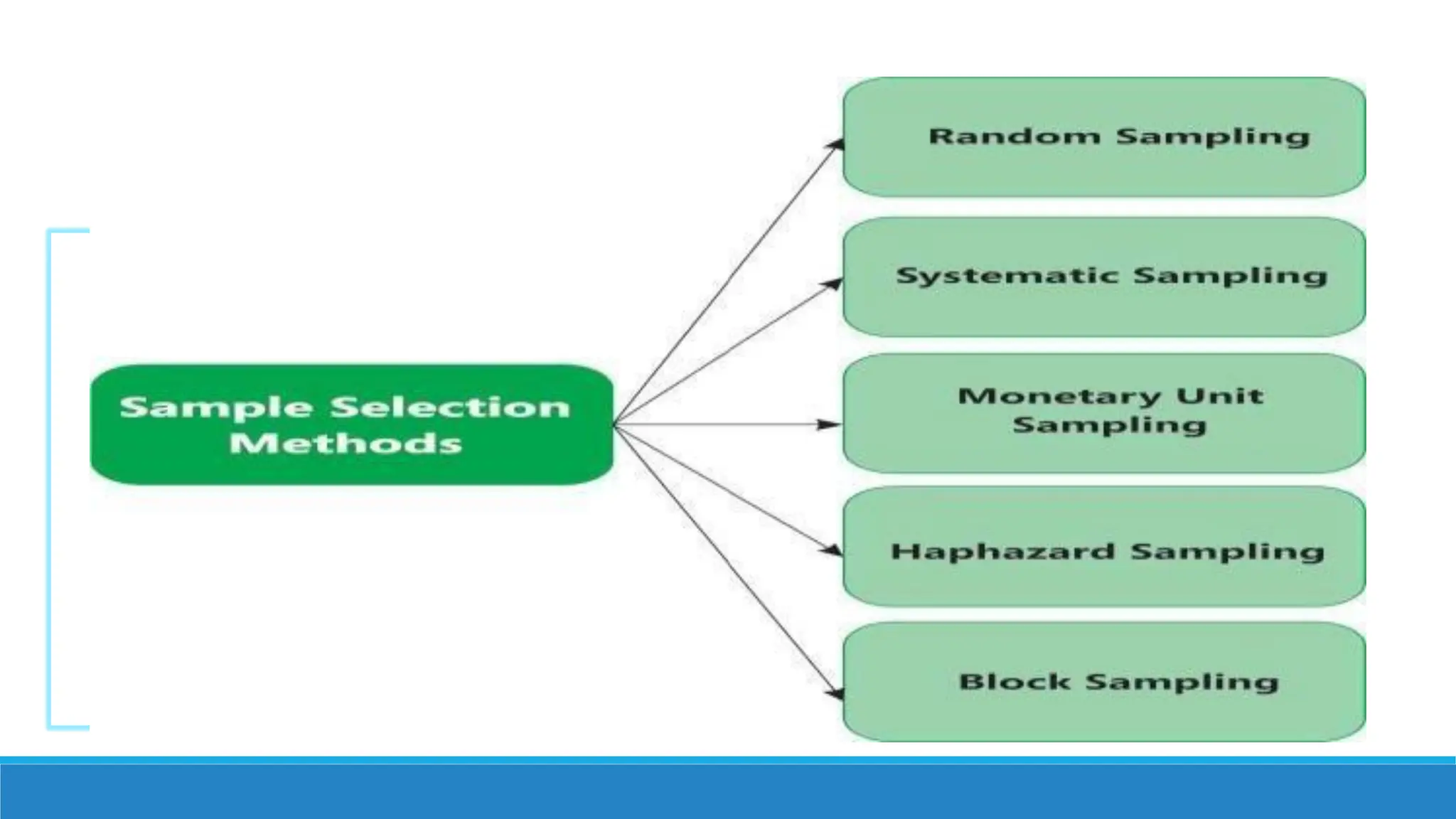

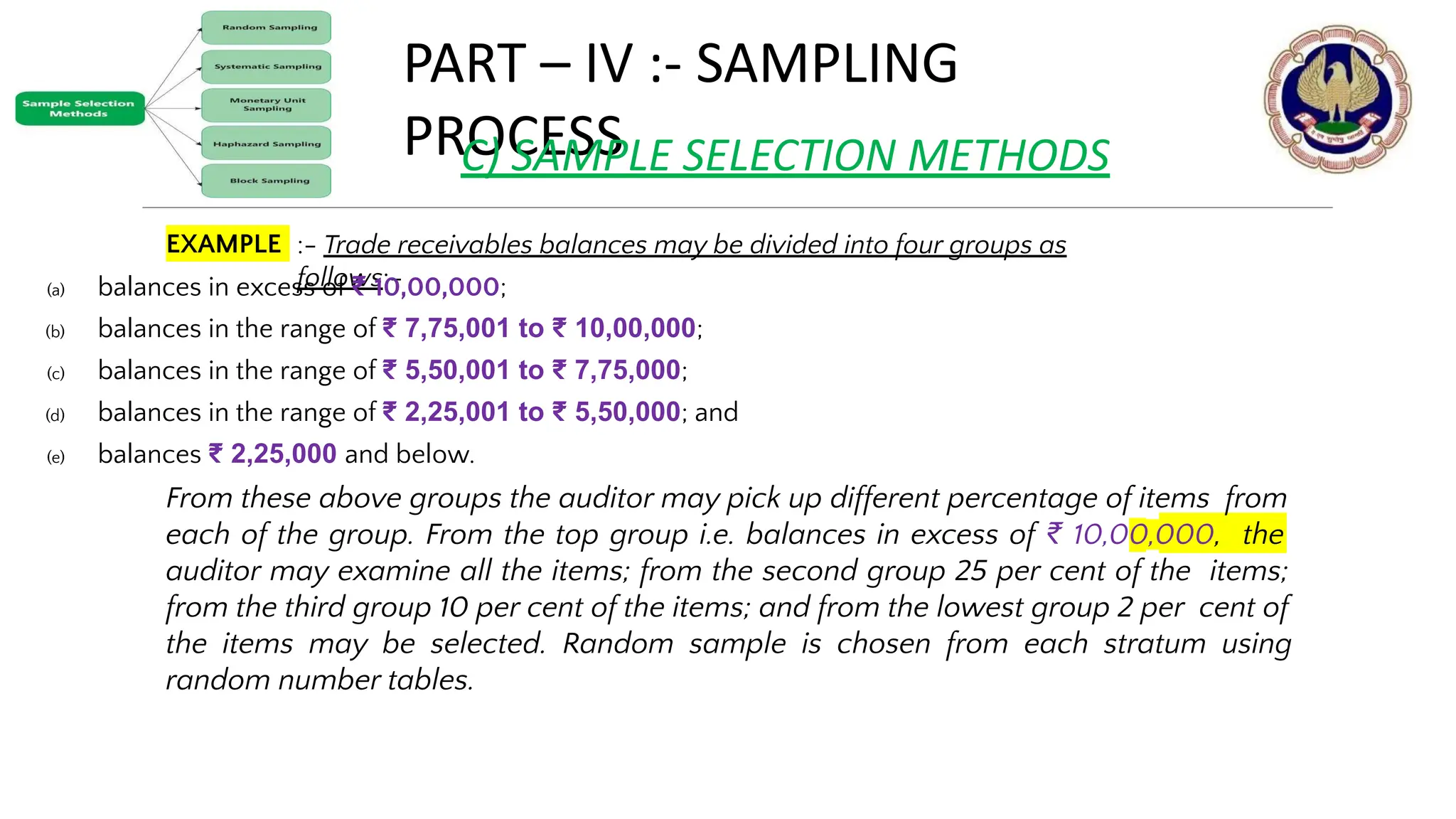

The document provides an overview of audit sampling, detailing its meaning, objectives, and the various methods for selecting samples, including random and stratified sampling. It highlights the risks associated with sampling, such as the potential for erroneous conclusions, and describes how auditors should evaluate the results of sampling methods. The text emphasizes the importance of ensuring that the selected sample accurately represents the entire population to support the auditor's conclusions.