This document provides an overview of Accounting Information Systems by discussing key topics such as:

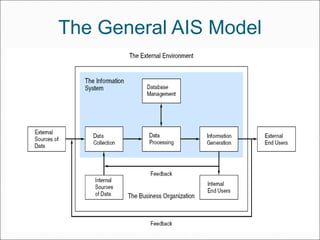

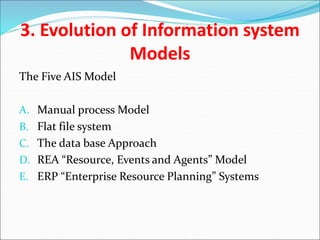

- The evolution of AIS models from manual to database to ERP systems.

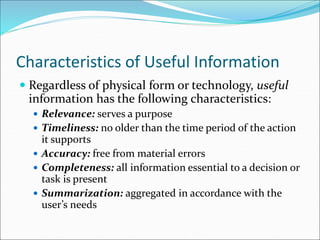

- The objectives and characteristics of useful information in a business context.

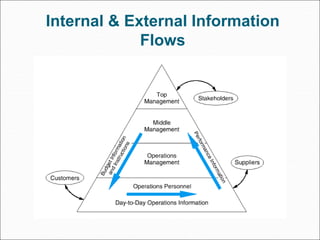

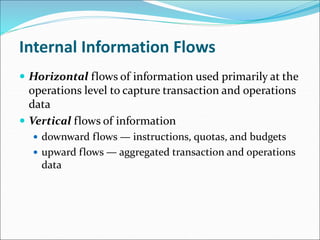

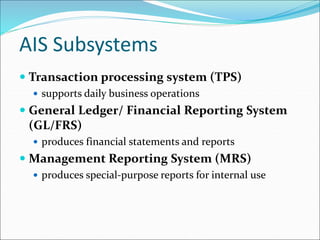

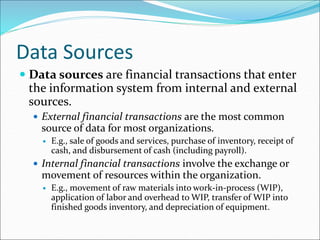

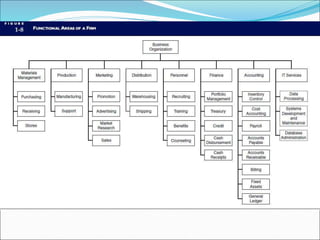

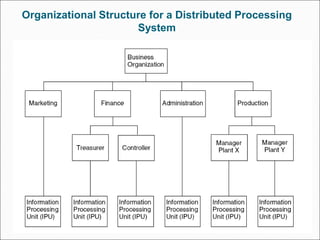

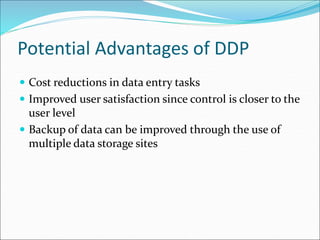

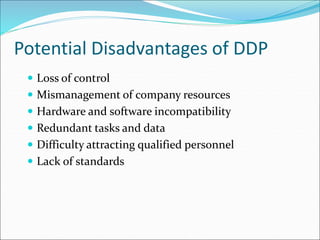

- How internal and external information flows within an organization and the roles of various AIS subsystems.

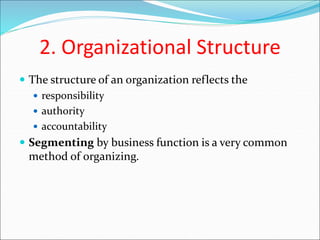

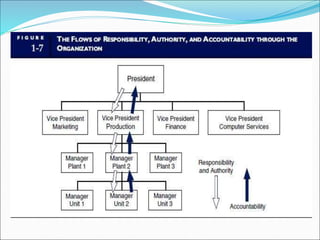

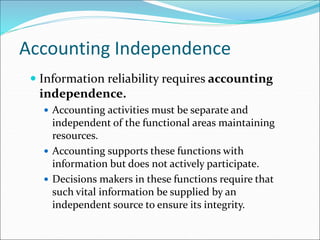

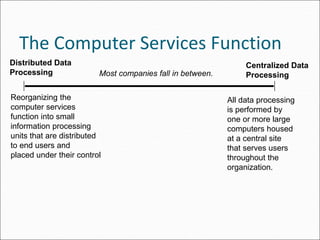

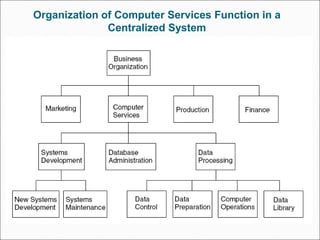

- The importance of accounting independence and how the computer services function can be organized.

- The role of accountants in designing information systems that meet the needs of the accounting function.

![[Webinar] Invoice Processing in Accounts Payable: Start the Year Strong](https://cdn.slidesharecdn.com/ss_thumbnails/anybillinvoiceprocessinginaccountspayable-130128133129-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![accounting_information_system[1].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/accountinginformationsystem1-231215144622-b88f4649-thumbnail.jpg?width=640&height=640&fit=bounds)