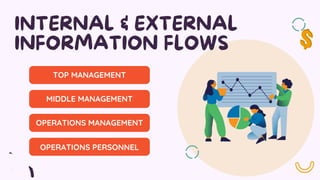

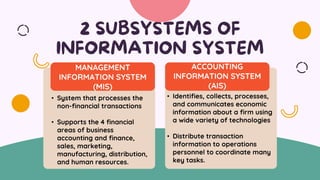

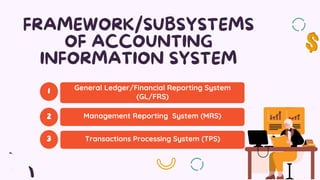

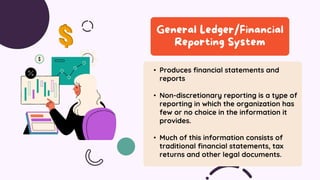

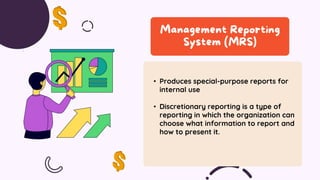

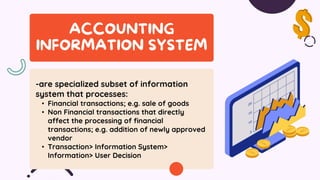

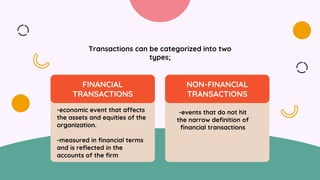

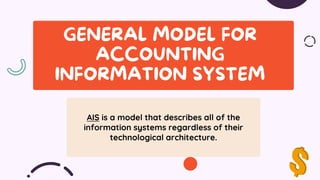

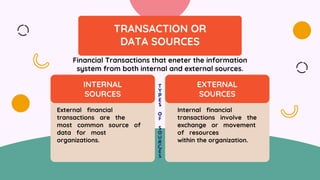

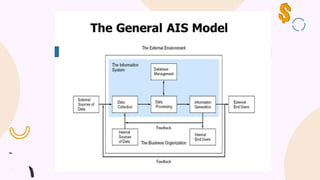

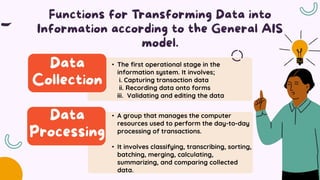

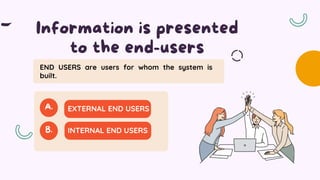

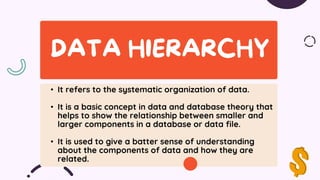

This document provides an overview of information systems from an accountant's perspective. It discusses how information systems support business operations and management decision making. There are two main types of information systems: management information systems (MIS) and accounting information systems (AIS). The AIS processes financial and some non-financial transactions to provide accounting reports. It consists of various subsystems like the general ledger system. Financial transactions come from internal and external sources and are processed through data collection, processing, storage, and distribution stages to produce useful information for end users.

![accounting_information_system[1].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/accountinginformationsystem1-231215144622-b88f4649-thumbnail.jpg?width=640&height=640&fit=bounds)

![How Big Brands are Taking Your Traffic in Alberta [Data Inside].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/howbigbrandsaretakingyourtrafficinalbertadatainside-260123180142-42d276f3-thumbnail.jpg?width=640&height=640&fit=bounds)