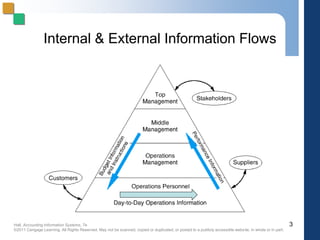

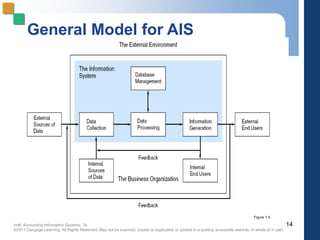

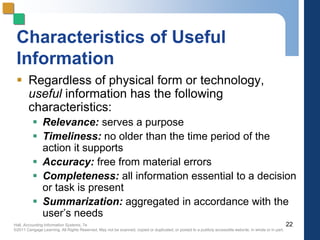

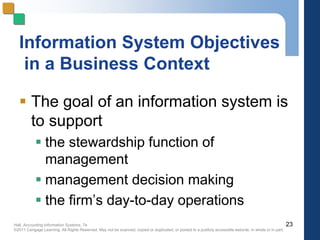

This chapter discusses accounting information systems from an accountant's perspective. It defines key terms like transactions, information systems, accounting information systems, and management information systems. It also outlines the general model for information systems, including data collection, processing, management, and information generation. The chapter describes the objectives of an accounting information system and characteristics of useful information for decision making.

![accounting_information_system[1].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/accountinginformationsystem1-231215144622-b88f4649-thumbnail.jpg?width=640&height=640&fit=bounds)