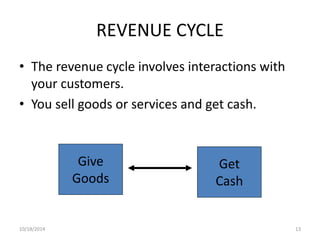

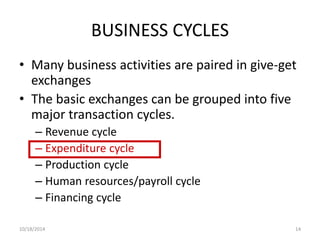

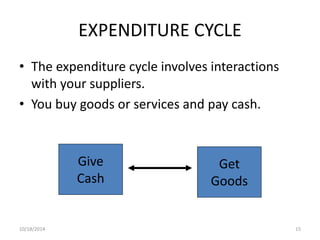

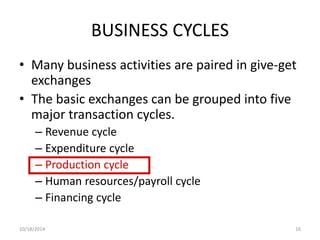

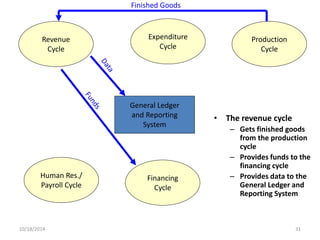

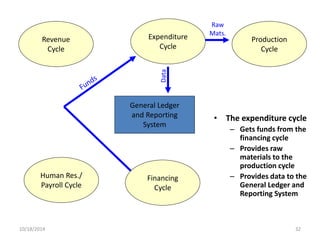

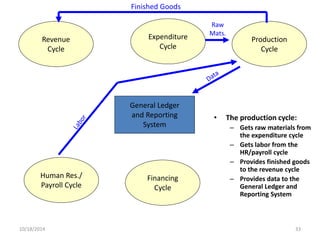

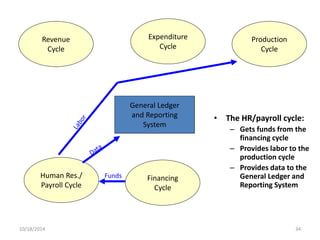

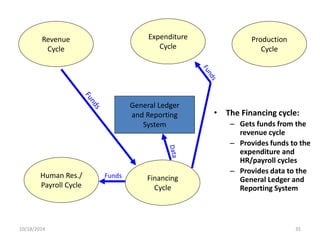

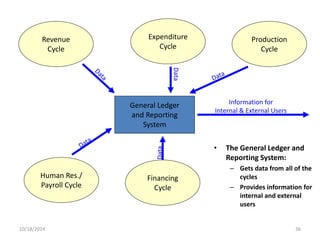

Chapter 2 outlines the essential business processes and activities of organizations, covering areas such as capital acquisition, employee management, and transaction cycles like revenue, expenditure, and production cycles. It highlights the need for information systems and data processing cycles in decision-making and efficiency, emphasizing the integration of financial and non-financial data. The chapter also discusses the interaction of accounting information systems with both internal and external parties, detailing the role of various transaction cycles and information outputs.