Brief Outline

• Overviewof AIS

• Transaction Cycle and Business Processes

• Developing Accounting Systems

• QuickBooks

• Systems Securities and Risk-control

• Emerging Trends and Ethical Issues

3.

Text books

• BRomney, M., & Steinbart, P. J. (2016). Accounting

information systems. 5th ed. UK: Prentice Hall.

• Bodnar, G. H., & Hopwood, W. S. (2013). Accounting

information systems. Pearson.

TOPIC ONE: OVERVIEWOF AIS

1.1 Introduction

• An accounting information system (AIS) involves the collection,

storage, and processing of financial and accounting data used by

internal users to report information to other stakeholders like

managers, investors, etc.

• It captures and records the financial effects of the firm’s

transactions.

6.

• The studyof accounting information systems analyzes how events

affecting an organization are recorded, summarized, and reported.

• These events are recorded using that organization’s system of human and

computer resources, summarized using accounting methods and

objectives, and reported as information to interested persons both within

and outside of the organization.

• Accounting information systems are used for all different forms of

organizations (Sole proprietor, partnership, corporations, nonprofit

foundations).

7.

• The functionsan of AIS are to:

i) Collect and store data about events, resources, and agents. Input

Device/Input system.

ii) Transform that data into information that management can use to make

decisions about events, resources, and agents.

iii) Provide adequate controls to ensure that the entity’s resources (including

data) are available when needed, accurate and reliable

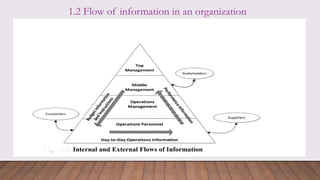

1.2 Flow ofinformation in an organization

• Internally

• External sources

• A good system should to capture info

10.

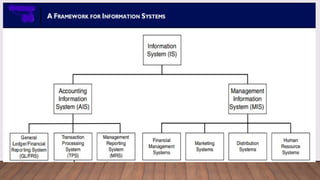

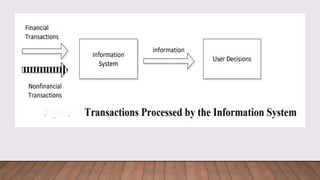

• Information systemsin an organization comprise of AIS and MIS

i) Accounting Information Systems (AIS) process financial transactions;

e.g. sale of goods

ii) Management Information Systems (MIS) process

a) Financial transaction

b) Nonfinancial transactions that are not normally processed by

traditional AIS; e.g., tracking customer complaints.

• The aim of both systems is to provide information to improve decision

making and increase the effectiveness and efficiency in an organization.

• Automation: To improve operations

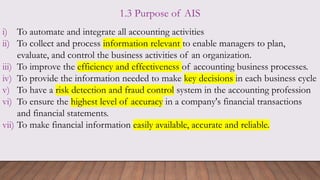

1.3 Purpose ofAIS

i) To automate and integrate all accounting activities

ii) To collect and process information relevant to enable managers to plan,

evaluate, and control the business activities of an organization.

iii) To improve the efficiency and effectiveness of accounting business processes.

iv) To provide the information needed to make key decisions in each business cycle

v) To have a risk detection and fraud control system in the accounting profession

vi) To ensure the highest level of accuracy in a company's financial transactions

and financial statements.

vii) To make financial information easily available, accurate and reliable.

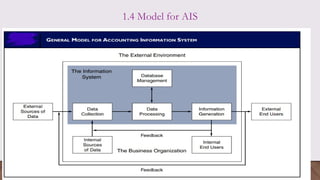

• Activity 1:In groups of six, discuss the general model for AIS

presented above and show the importance of AIS in the business

organization.

17.

1.5 Components ofthe AIS

i) People: Users, the ones operating the system

ii) Data: This the key component for the AIS. Financial data. At the

input (collection), the data processed into useful information.

iii) Software: Enables the people to communicate with the system

iv) Procedure: For every system, there should processes/step

through the user communicates with the other components

v) Information Technology: This supports the whole system

vi) Internal Controls: Needed for data protection and privacy.

Protect against data leakage.

18.

• Planning: Situationanalysis-mention the gap/challenges

that exist. Propose a solution. Gathering data on the

status quo.

• New features within the sytem

19.

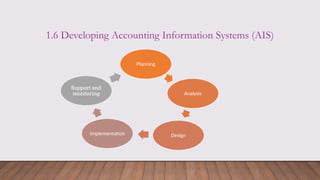

1.6 Developing AccountingInformation Systems (AIS)

Planning

Analysis

Design

Implementation

Support and

monitoring

20.

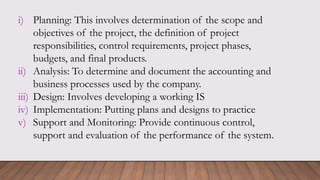

i) Planning: Thisinvolves determination of the scope and

objectives of the project, the definition of project

responsibilities, control requirements, project phases,

budgets, and final products.

ii) Analysis: To determine and document the accounting and

business processes used by the company.

iii) Design: Involves developing a working IS

iv) Implementation: Putting plans and designs to practice

v) Support and Monitoring: Provide continuous control,

support and evaluation of the performance of the system.

21.

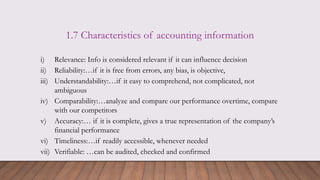

1.7 Characteristics ofaccounting information

i) Relevance: Info is considered relevant if it can influence decision

ii) Reliability:…if it is free from errors, any bias, is objective,

iii) Understandability:…if it easy to comprehend, not complicated, not

ambiguous

iv) Comparability:…analyze and compare our performance overtime, compare

with our competitors

v) Accuracy:… if it is complete, gives a true representation of the company’s

financial performance

vi) Timeliness:…if readily accessible, whenever needed

vii) Verifiable: …can be audited, checked and confirmed

22.

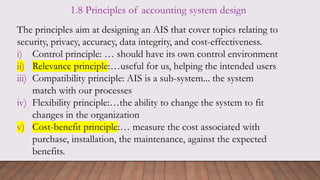

1.8 Principles ofaccounting system design

The principles aim at designing an AIS that cover topics relating to

security, privacy, accuracy, data integrity, and cost-effectiveness.

i) Control principle: … should have its own control environment

ii) Relevance principle:…useful for us, helping the intended users

iii) Compatibility principle: AIS is a sub-system... the system

match with our processes

iv) Flexibility principle:…the ability to change the system to fit

changes in the organization

v) Cost-benefit principle:… measure the cost associated with

purchase, installation, the maintenance, against the expected

benefits.

23.

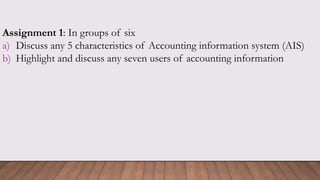

Assignment 1: Ingroups of six

a) Discuss any 5 characteristics of Accounting information system (AIS)

b) Highlight and discuss any seven users of accounting information

TOPIC TWO: TRANSACTIONCYCLE AND

BUSINESS PROCESSES

2.1 Introduction

• A business process is a set of related, coordinated and structured

activities and tasks that are performed by a person, a computer or a

machine, and that help accomplish a specific organizational goal.

• Organizations must organize their business processes into groups of

related transactions.

• Many business activities are pairs of events involved in a give-get

exchange.

26.

• A transactionis an agreement between two entities to exchange goods or

services or any other event that can be measured in economic terms by

the organization.

• Examples include

a) selling goods to customers

b) buying inventory from suppliers

c) paying employees, etc

• A transaction is an event that affects or is of interest to the organization.

• Two types:

i) Financial

ii) Non-Financial

27.

• The transactionprocessing system (TPS) is the system able to collect

data from various input points, i.e. transactions, business activities

• It is central to the overall function of the accounting information

system by

i) Converting economic events into financial transactions

ii) Recording financial transactions in the accounting records (journals

and ledgers)

iii) Distributing essential financial information to operations personnel

to support their daily operations.

• The transaction processing system deals with business events that occur

frequently.

28.

2.2 Classifications ofTPS

i) The Expenditure Cycle: Purchasing to Cash Disbursements.

Where companies purchase inventory for resale or raw

materials to use in producing products in exchange for cash or

a future promise to pay cash.

ii) The Production Cycle or Conversion Cycle, where raw

materials are transformed into finished goods.

iii) The Revenue Cycle: Sales to Cash Collections. Where goods

and services are sold for cash or a future promise to receive

cash.

29.

iv) The HumanResources Management or Payroll Cycle: Where

employees are hired, trained, compensated, evaluated, promoted,

and terminated.

v) General Ledger and Reporting System: Where financial reports and

statements are generated to useful information for the end users.

30.

2.3 Identifying Eventsin Business Process

• Most common financial transactions are economic exchanges with external

parties e.g. sales, purchases

• Financial transactions also include certain internal events such as the

depreciation of fixed assets; the use of labor, raw materials, and overhead to

the production process; and the transfer of inventory from one department

to another.

• Every business:

i) Incurs expenditures in exchange for resources (expenditure cycle),

ii) Provides value addition through its products or services (conversion cycle),

iii) Receives revenue (grant) from outside sources (revenue cycle).

31.

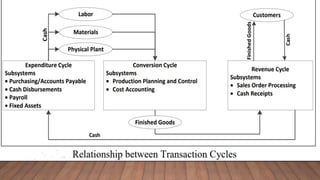

2.3.1 The ExpenditureCycle

• Business activities begin with the acquisition of materials, property, and labor

in exchange for cash in the expenditure cycle.

• Most expenditure transactions are based on a credit relationship between the

trading parties.

• The actual disbursement of cash takes place at some point after the receipt of

the goods or services.

• From a systems perspective, this cycle has two parts:

i) a physical component (the acquisition of the goods/services)

ii) a financial component (the cash disbursement to the supplier).

• Each component of the cycle is processed separately by a different subsystem.

32.

• The expenditurecycle comprises the following main

subsystems:

i) Purchases/accounts payable system

ii) Cash disbursements system

iii) Payroll system

iv) Fixed asset system

33.

2.3.2 The ConversionCycle

• The conversion cycle is composed of two major subsystems

i) The production system: involves the planning, scheduling, and

control of the physical product through the manufacturing process.

• This includes determining raw material requirements, authorizing the

work to be performed and the release of raw materials into

production, and directing the movement of the work-in process

through its various stages of manufacturing.

34.

ii) The costaccounting system: monitors the flow of cost

information related to production.

• The information this system produces is used for inventory

valuation, budgeting, cost control, performance reporting, and

management decisions, such as make-or-buy decisions.

• Note: Manufacturing firms convert raw materials into finished

products through formal conversion cycle operations.

• However, the conversion cycle is not usually formal and observable

in service and retail enterprises

35.

2.3.3 The RevenueCycle

• Firms sell their finished goods to customers through the revenue cycle,

which involves processing cash sales, credit sales, and the receipt of cash

following a credit sale.

• Revenue cycle transactions comprise of

i) a physical component (sale of goods/services)

ii) a financial component (receipt of cash)

36.

• The primarysubsystems of the revenue cycle are:

i) Sales order processing system: involve tasks such as preparing sales

orders, granting credit, shipping products (or rendering of a service)

to the customer, billing customers, and recording the transaction in

the accounts (accounts receivable, inventory, expenses, and sales).

ii) Cash receipts system: includes collecting cash, depositing cash in

the bank, and recording these events in the accounts (accounts

receivable and cash).

38.

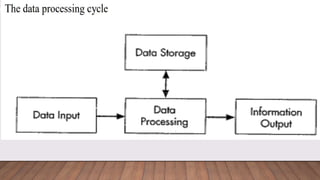

2.4 Transaction Processing:The Data Processing Cycle

• The data processing cycle consists of a series of steps where raw

data (input) is fed into a system to produce actionable insights

(output).

• Each step is taken in a specific order, but the entire process is

repeated in a cyclic manner.

40.

1. Input –The raw data after collection needs to be fed in the cycle for

processing.

2. Processing – Once the input is provided the raw data is processed by a

suitable or selected processing method. This is the most important step

as it provides the processed data in the form of output which will be

used further.

3. Output – This is the outcome and the raw data provided in the first stage

is now “processed” and the data is useful and provides information and

no longer called data. The output should be information useful for the

end users.

41.

2.4.1 Data Input

1.Step 1: Capture transaction and enter data into the system

• The data capture process is usually triggered by a business activity.

• Data must be collected about three facets of each business activity:

i) Each activity of interest

ii) The resource(s) affected by each activity

iii) The people who participate in each activity

• With the use of AIS and information technology, Source data automation

devices capture transaction data in machine-readable form at the time and

place of their origin. E.g. ATMs, point of-sale (POS) scanners, bar code

scanners.

42.

• E.g. thefollowing data about a sales transaction may be collected:

Date and time the sale occurred

Employee who made the sale and the checkout clerk who processed the

sale

Checkout register where the sale was processed

Item(s) sold

Quantity of each item sold

List price and actual price of each item sold

Total amount of the sale

Delivery instructions

For credit sales: customer name, customer bill-to and ship-to addresses

43.

2. Step 2:Make sure captured data are accurate and complete

• One way to do this is to use source data automation or well-designed

documents and data entry screens.

• These approaches help improve accuracy and completeness by providing

instructions or prompts about what data to collect, grouping logically

related pieces of information close together, using check off boxes or

pull-down menus to present the available options, and using appropriate

shading and borders to clearly separate data items.

3. Step 3: Make sure company policies and procedures are followed, such

as approving or verifying a transaction.

44.

2.4.2 Data Storage

•A company's data are one of its most important resources.

• However, the mere existence of relevant data does not guarantee that they are

useful.

• To function properly, an organization must have ready and easy access to its

data.

• Therefore, accountants need to understand how data are organized and stored

in an AIS and how they can be accessed. In essence, they need to know how to

manage data for maximum corporate use.

• Transaction data are often recorded in a journal before they are entered into a

ledger. Cumulative accounting information is stored in general and subsidiary

ledgers.

45.

Coding techniques

• Datain ledgers is organized logically using coding techniques.

• Coding is the systematic assignment of numbers or letters to items to

classify and organize them.

i) Sequence codes: items are numbered consecutively to account for all

items. Any missing items cause a gap in the numerical sequence.

Examples include pre-numbered checks, invoices, and purchase orders.

ii) Block code: blocks of numbers are reserved for specific categories of

data.

iii) Group codes: which are two or more subgroups of digits used to code

items, are often used in conjunction with block codes.

iv) Mnemonic codes: letters and numbers are combined to identify an item.

46.

• Guidelines resultin a better coding system. The code should:

i) Be consistent with its intended use, which requires that the code

designer determine desired system outputs prior to selecting the code.

ii) Allow for growth. For example, don't use a three-digit employee code

for a fast-growing company with 950 employees.

iii) Be as simple as possible to minimize costs, facilitate memorization and

interpretation, and ensure employee acceptance.

iv) Be consistent with the company's organizational structure and across

the company's divisions.

• E.g. of coding system is the Chart of Accounts.

47.

• Note: Anaudit trail can be used to assess the accuracy, validity and

completeness of the transactions

• An audit trail is a traceable path of a transaction through a data

processing system from point of origin to final output, or backwards from

final output to point of origin.

48.

2.4.3 Data Processing

•Once business activity data have been entered into the system, they must

be processed to keep the databases current.

• The four different types of data processing activities, referred to as

CRUD, are as follows:

i) Creating new data records, such as adding a newly hired employee to the

payroll database.

ii) Reading, retrieving, or viewing existing data.

iii) Updating previously stored data.

iv) Deleting data, such as removing the vendor master file of all vendors

the company no longer does business with.

49.

Batch vs. Real-TimeProcessing

• Batch Processing system is where data updating and processing is done at regular

intervals of time.

• In a batch processing system, transactions are accumulated over a period of time

and processed as a single unit, or batch.

• Batch processing is cheaper and more efficient.

• The data are current and accurate only immediately after processing.

• Batch processing is used only for applications, such as payroll, that do not need

frequent updating and those naturally occurs or are processed at fixed time

periods.

• There is some time delay between the actual event and the processing of the

transaction to update the records of the organization

50.

• In areal-time processing system, transactions are processed

immediately as they occur without any delay to accumulate transactions.

Real-time processing is also referred to as online transaction processing, or

OLTP.

• In this case, the records in the system always reflect the current status.

• Most companies update each transaction as it occurs.

• This increases decision making usefulness.

• It is also more accurate because data input errors can be corrected in real

time or refused.

• It also provides significant competitive advantages

51.

2.4.4 Information Output

•The final step in the data processing cycle is information output which may be in soft

copy or hard copy.

• It may be given in three main forms:

i) Documents: Records of transaction or other company data eg invoices, receipts,

checks, purchase orders

ii) Reports: Used by employees to control operational activities and by managers to make

decisions and to formulate business strategies. External users need reports to evaluate

company profitability, judge creditworthiness, or comply with regulatory requirements.

E.g. Income statement, sales reports, balance sheet, etc.

iii) Query response: A database query is used to provide the information needed to deal

with problems and questions that need rapid action or answers. A user enters a request

for a specific piece of information; it is retrieved, displayed, or analyzed as requested.

52.

2.5 Types ofFiles

2.5.1 Manual Process Model

• Manual systems constitute the physical events, resources, and personnel that

characterize many business processes.

• This includes such tasks as order-taking, warehousing materials, manufacturing

goods for sale, shipping goods to customers, and placing orders with vendors.

• Traditionally, this model also includes the physical task of record keeping.

• The files kept include

i) Documents: Source documents, product documents and Turnaround

Documents

ii) Journal: Enters transactions in chronological order.

iii) Ledgers: Accounts for various transactions

53.

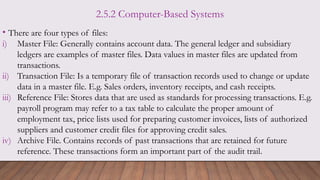

2.5.2 Computer-Based Systems

•There are four types of files:

i) Master File: Generally contains account data. The general ledger and subsidiary

ledgers are examples of master files. Data values in master files are updated from

transactions.

ii) Transaction File: Is a temporary file of transaction records used to change or update

data in a master file. E.g. Sales orders, inventory receipts, and cash receipts.

iii) Reference File: Stores data that are used as standards for processing transactions. E.g.

payroll program may refer to a tax table to calculate the proper amount of

employment tax, price lists used for preparing customer invoices, lists of authorized

suppliers and customer credit files for approving credit sales.

iv) Archive File. Contains records of past transactions that are retained for future

reference. These transactions form an important part of the audit trail.

54.

2.6 Disadvantages ofAIS

i) Stand alone information system (transaction processing system)

ii) Its only concern is financial data and accounting transactions.

Hence, it requires support from other subsystems that capture

non-financial information.

Note: Add other disadvantages

55.

2.7 Enterprise ResourcePlanning (ERP) Systems

• A system that integrates all aspects of an organization’s activities into one

system.

• An ERP integrate all aspects of a company’s operations with a traditional

AIS.

• Most large and many medium-sized organizations use ERP systems to

coordinate and manage their data, business processes, and resources.

• The ERP system collects, processes, and stores data and provides the

information managers and external parties need to assess the company.

• An ERP facilitates information flow among the company’s various business

functions and manages communications with outside stakeholders.

56.

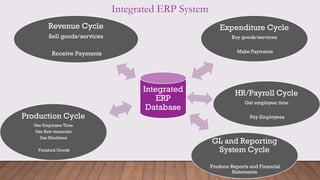

Integrated ERP System

Integrated

ERP

Database

RevenueCycle

Sell goods/services

Receive Payments

Expenditure Cycle

Buy goods/services

Make Payments

HR/Payroll Cycle

Get employee time

Pay Employees

GL and Reporting

System Cycle

Produce Reports and Financial

Statements

Production Cycle

Use Employee Time

Use Raw materials

Use Machines

Finished Goods

57.

• Assignment 2:Select a company of your choice and propose or

design an Accounting Information Systems.

a) The AIS designed should be complete and able to process the

business transactions from start to the preparation of final

accounts.

b) Discuss factors to consider when designing the AIS

c) Present the process of TPS in the AIS tracking the company’s

transactions from start to the preparation of Final Accounts.

d) Discuss the challenges that AIS designing may encounter and

propose strategies mitigating these challenges.

58.

TOPIC THREE: DEVELOPINGACCOUNTING

SYSTEMS

3.1 Introduction

• System Development Life Cycle (SDLC): Is a formal process used by

organization to develop, introduce and implement an information system

• Accountants commonly apply the systems approach in the development of

new information systems.

• The recent adoption of computer technology in accounting has forced

accountants to be more attentive to the methods used in developing

accounting systems.

• It has initiated the debate of using information technology within the

accounting profession.

59.

3.2 The qualitiesof a successful system

• A system is successful if it achieves most of the goals set.

i) It should produce correct and timely information.

ii) It should be developed within a reasonable amount of time.

iii) The system should meet the organization’s needs for information.

iv) The users should be satisfied with it

60.

3.3 AIS DevelopmentApproaches

• Some of the main approaches in system development include:

i) Systems Development Life Cycle (SDLC)

ii) Rapid Application Development (RAD)

iii) Object-Oriented Approach (OOA)

3.3.1 The Systems Life Cycle (SLC) is a type of methodology used to

describe the process for building information systems, intended to develop

information systems in a very deliberate, structured and methodical way,

reiterating each stage of the life cycle.

61.

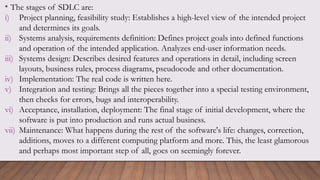

• The stagesof SDLC are:

i) Project planning, feasibility study: Establishes a high-level view of the intended project

and determines its goals.

ii) Systems analysis, requirements definition: Defines project goals into defined functions

and operation of the intended application. Analyzes end-user information needs.

iii) Systems design: Describes desired features and operations in detail, including screen

layouts, business rules, process diagrams, pseudocode and other documentation.

iv) Implementation: The real code is written here.

v) Integration and testing: Brings all the pieces together into a special testing environment,

then checks for errors, bugs and interoperability.

vi) Acceptance, installation, deployment: The final stage of initial development, where the

software is put into production and runs actual business.

vii) Maintenance: What happens during the rest of the software's life: changes, correction,

additions, moves to a different computing platform and more. This, the least glamorous

and perhaps most important step of all, goes on seemingly forever.

62.

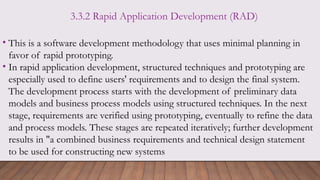

3.3.2 Rapid ApplicationDevelopment (RAD)

• This is a software development methodology that uses minimal planning in

favor of rapid prototyping.

• In rapid application development, structured techniques and prototyping are

especially used to define users' requirements and to design the final system.

The development process starts with the development of preliminary data

models and business process models using structured techniques. In the next

stage, requirements are verified using prototyping, eventually to refine the data

and process models. These stages are repeated iteratively; further development

results in "a combined business requirements and technical design statement

to be used for constructing new systems

63.

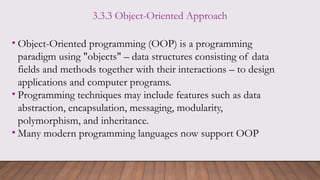

3.3.3 Object-Oriented Approach

•Object-Oriented programming (OOP) is a programming

paradigm using "objects" – data structures consisting of data

fields and methods together with their interactions – to design

applications and computer programs.

• Programming techniques may include features such as data

abstraction, encapsulation, messaging, modularity,

polymorphism, and inheritance.

• Many modern programming languages now support OOP

64.

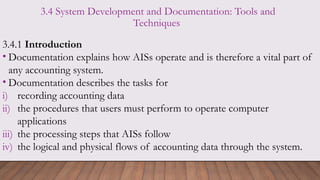

3.4 System Developmentand Documentation: Tools and

Techniques

3.4.1 Introduction

• Documentation explains how AISs operate and is therefore a vital part of

any accounting system.

• Documentation describes the tasks for

i) recording accounting data

ii) the procedures that users must perform to operate computer

applications

iii) the processing steps that AISs follow

iv) the logical and physical flows of accounting data through the system.

65.

• Document flowchartsdescribe the physical flow of order forms,

requisition slips, and similar hardcopy documents through an AIS.

• These flowcharts pictorially represent data paths in compact formats and

therefore save pages of narrative description.

• System flowcharts usually focus on the electronic flows of data in

computerized AISs.

66.

3.4.2 Importance ofdocumentation in System

Development

• Depicting how the system works

• Training users

• Designing new systems

• Controlling system development and maintenance costs

• Standardizing communications with others

• Auditing AISs

• Documenting business processes

• Establishing accountability

67.

3.4.3 Documentation Tools

i)Data Flow Diagrams (DFD)

ii) Flow Charts: Include

a) Document Flow Chart: a graphical description of the flow of documents and

information between departments or areas of responsibility within an

organization. It traces the physical flow of documents through an organization.

b) System Flowchart: a graphical description of the relationship among the input,

processing, and output in an information system. It shows the electronic flow

of data and processing steps in an AIS.

c) Program Flowchart: a graphical description of the sequence of logical

operations that a computer performs as it executes a program.

68.

Assignment

• An accountinginformation system (AIS) involves the

collection, storage, and processing of financial and

accounting data used by different decision makers. For the

AIS to be effective, it needs to have in place an appropriate

and effective internal control environment as well as system

maintenance.

• In groups of 4,

a) Discuss the role of internal control environment in AIS

b) Discuss system maintenance and its function in AIS

c) What is system audit? What significance does it have in AIS

TOPIC FIVE: ACCOUNTINGSYSTEMS

SECURITIES AND RISK CONTROL

5.1 Accounting System Environment

5.2 Accounting System Analysis and Audit

5.3 Accounting System Security

5.4 Accounting System Maintenance

71.

5.1 Accounting SystemEnvironment

• The accounting system environment includes the factors influencing the running

of the accounting using modern technology.

• Accounting functions in a dynamic environment. Changes in technology as well as

economic and political factors can significantly influence accounting practice.

• The environment includes

i) System environment: The overall operation, components, system, principles,

procedure

ii) Hardware components

iii) Control Environment: various measures put in place to protect the system

iv) Accounting processes: step by step procedure in accounting transaction

v) Accounting principles and standards: international guidelines on accounting

vi) Ethical principles: morals to be adhered

72.

• The internationalnature of business requires organization to be able to

make their financial statements understandable to users all over the

world.

• Ethics are the basic moral principles that govern an individual’s

behavior, including how an individual conducts himself or herself in a

business-related activity.

• Personal ethics and morals should be intertwined with the accounting

profession.

• Control environment is necessary to ensure and promote AIS security

and protection.

73.

5.2 Accounting SystemAnalysis and Audit

• Every business firm follows a particular accounting system that is set up to keep

the records of all the transactions of the business.

• Is system meeting the intended goals, in line with the organization goals

• Accounting system analysis is the evaluation and analysis of the present accounting

system which a firm follows.

• Accounting system analysis evaluates the performance of the system from time to

time to ensure that the system meets the expectations of the business.

• An accounting system audit is an examination of the financial and accounting system

of an organization to determine compliance with the applicable accounting

requirements.

• The system audit checks the applicability of the accounting system to comply with the

accounting standards.

74.

• It helpsthe firms to identify the prevailing drawbacks (form

feedback on the challenges) of the accounting system, and how

the firm can achieve the expected profits by tackling such

drawbacks.

• By conducting an accounting system analysis, the firms can

make required changes in the accounting system so that they

can effectively achieve the expected results.

• Overall performance of the system

75.

• Core partsof accounting system analysis

• An accounting system analysis includes three main parts which are as follows:

i) Analysis: It is very important for the firms to analyze the accounting system

from time to time in order to identify the changes required to be made with the

change in the nature and type of the business and the transactions. After

analysis of the changes, the firms start to modify the accounting system as per

the new requirements.

ii) Design: After the analysis process, the designing of the accounting system gets

started. The new accounting system must fulfill the requirements of the

company as well as the requirements of the individuals who play an important

role in the accounting business. It must contain revised and updated accounting

laws and principles and other important updates. We want to make system to

be more and more relevant to the organization. Upgrading the existing

76.

iii) Implementation: Afterthe analysis and designing of the required

accounting system, the next part is implementation. This involves

putting the plans and design into effect. It is a time-consuming

process. The accounting team of the business must also be provided

with adequate training regarding the new accounting system. The

complexity of the accounting system is also a factor that decides the

time for implementation of the system. Even after the

implementation of the new system there may be many things that

may require changes.

System analysis is continuous process

77.

• Factors toConsider When conducting System Analysis

i) The User: User friendly interface

ii) User requirements and system functionality

iii) Operating Environment

iv) Organizational goals: improve the efficiency in operation===Profitability

v) Performance evaluation: analyze the system, audited

vi) External Factors: competition, new changes in technologies, political, new rules

regulation, changes in customer preference, suppliers

• Advantages of accounting system analysis

i) It provides a better understanding of the business.

ii) It ensures the prosperity of the business in the best possible manner.

iii) Helps in the assessment of business competition and assists in its preparation.

iv) Optimum utilization of all the business resources. Efficient use of the resources

v) Allows compatibility of the system with the business

78.

5.3 Accounting SystemSecurity

• AIS deals with financial data for the company, data on the customers,

suppliers, employees

• All of the data in an AIS should be encrypted, and access to the system

should be logged and monitored.

• System activity should be traceable. This increase transparency and

accountability.

• An AIS also needs internal controls that protect it from computer viruses,

hackers, and other internal and external threats to network security.

79.

• An AISmust have internal controls to limit access to authorized users

and to protect against unauthorized access.

• The internal controls of an AIS are the security measures it maintains to

protect sensitive data.

• Authorized users will include individuals inside and outside the company.

• Internal controls must also prevent unauthorized file access by individuals

who are allowed to access certain select parts of the system.

• An AIS contains confidential information about the company, employees,

suppliers and customers. These information must be safeguarded.

80.

• Accounting securityplays a significant role in safeguarding sensitive

financial data.

• Security Framework: This is a set of policies, guidelines, and best

practices designed to manage an organization's information security

risks.

i) Advanced encryption

ii) Access controls: Physical control, logical control

iii) Regular audits: Assess the system performance/security

iv) Backup systems: Help us to retrieve info/data incase of data loss.

81.

• In thecontemporary digital era, data security has become a paramount

concern for businesses across all industries, and accounting firms are no

exception.

• Importance of financial data security include:

i) Protecting Confidential Information

ii) Regulatory Compliance

iii) Building Trust

iv) Preventing Financial Fraud

v) Ensure Business Continuity

82.

5.4 Accounting SystemMaintenance

• System maintenance is the process of keeping a company's technology

infrastructure, equipment and software running smoothly and

efficiently.

• It is a crucial aspect of running a business as it ensures the smooth

functioning of all the systems that the company depends on to carry out

its operations.

• Accounting system analysis is the process of closely examining the

financial systems, processes, and data to ensure they are running at their

best.

•

83.

• Types ofsystem maintenance strategies

i) Corrective maintenance: Maintenance is carried out following detection of

an anomaly and aimed at restoring normal operating conditions. Reactive

ii) Preventive maintenance: Maintenance carried out at predetermined

intervals or according to prescribed criteria, aimed at reducing the failure risk

or performance degradation of the equipment. Proactive

iii) Risk-based maintenance: Maintenance carried out by integrating analysis,

measurement and periodic test activities to standard preventive maintenance.

The aim is to perform risk assessment and define the appropriate

maintenance program.

iv) Condition-based maintenance: Maintenance based on the equipment

performance monitoring and the control of the corrective actions taken as a

result.

84.

TOPIC SIX: EMERGINGTRENDS AND ETHICAL

ISSUES

• These are challenges and issues of concern in the modern business in the use of

Accounting Information Systems

i) Increased consumer awareness

ii) Consumer protection

iii) Advanced technology

iv) Cybercrime

v) System integration

vi) Protection of intellectual property such as copyrights and trade secrets

vii) Regional integration and globalization

viii)Fraud prevention and protection

ix) Accountability, transparency and integrity

• Assignment 2:Within a company set-up, select a

transaction of your choice and present a flow chart

showing the business process.

• Discuss the significant of AIS in capturing the business

process.

![accounting_information_system[1].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/accountinginformationsystem1-231215144622-b88f4649-thumbnail.jpg?width=640&height=640&fit=bounds)