Downloaded 1,192 times

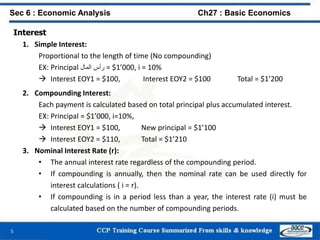

![Section 1 : Cost Chapter 7 : Economic Costs

49

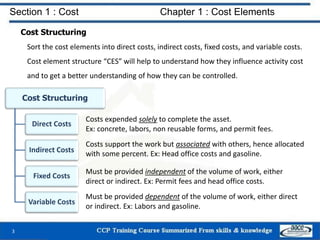

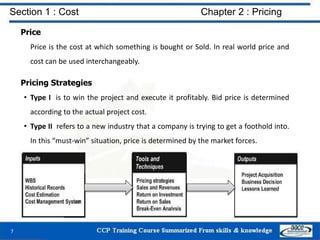

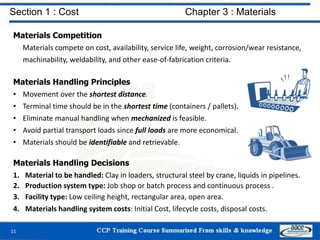

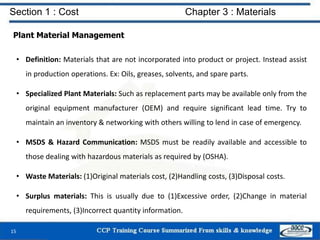

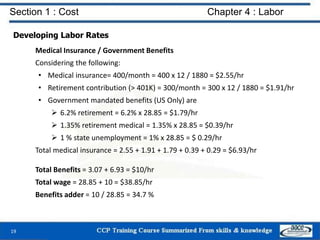

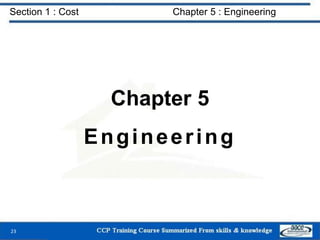

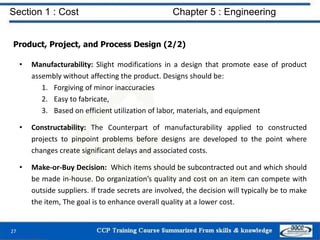

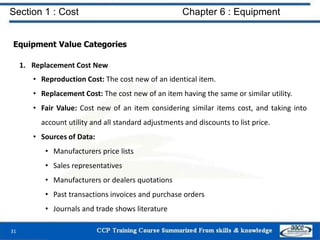

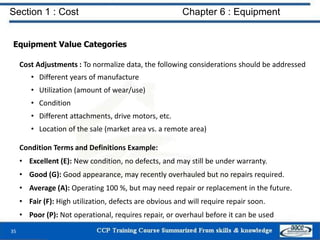

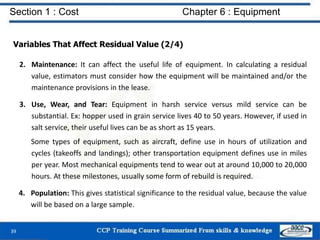

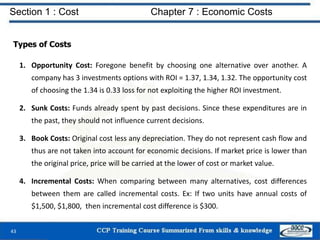

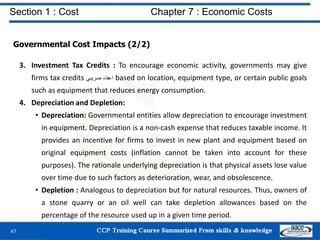

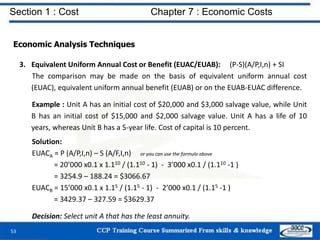

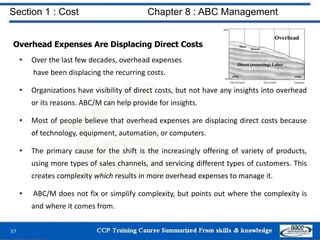

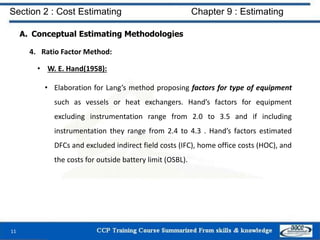

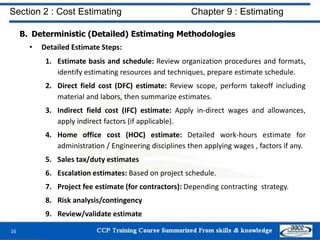

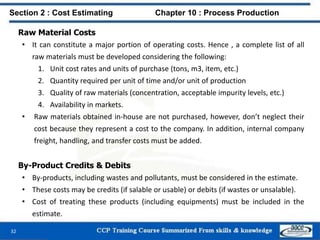

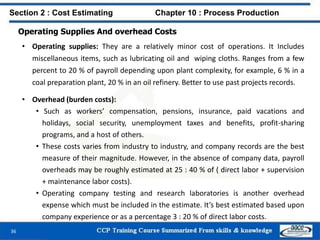

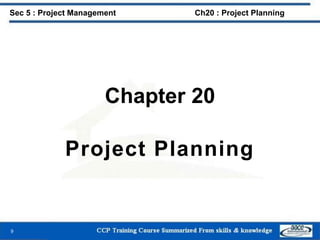

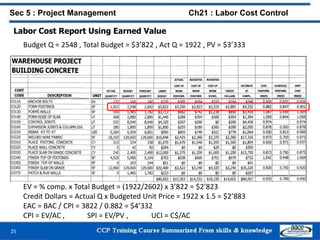

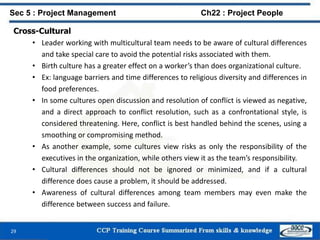

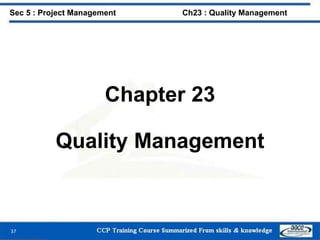

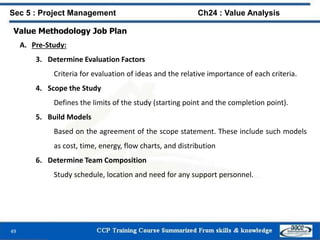

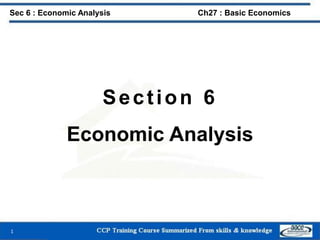

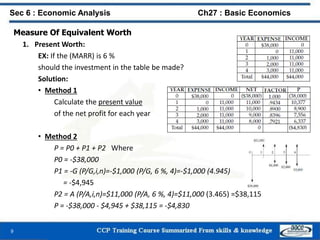

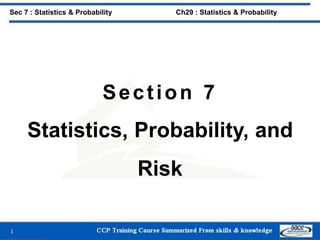

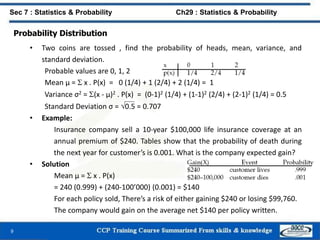

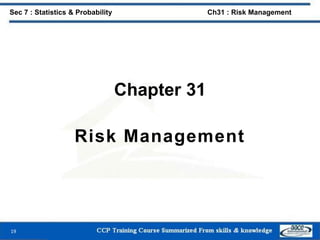

Depreciation Techniques (2/2)

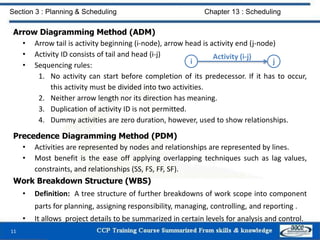

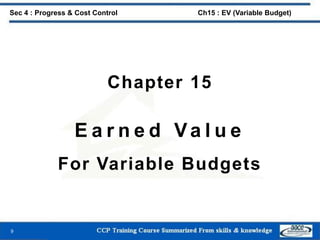

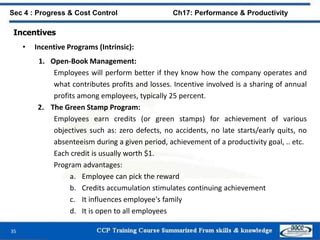

3. Sum-of-Years Digits Depreciation (SOYD): Dr = (C - S) x [ (N-r+1) / ((N(N + 1) /2 )]

Where: Dr = Depreciation charge for the rth year, C = asset original cost, S = salvage

value, N = remaining asset depreciable life (years), r = rthyear.

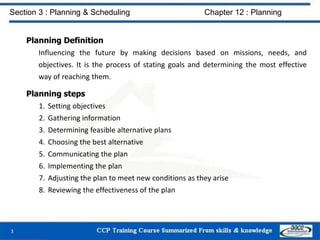

Ex: For the previous example,

4. Modified Accelerated Cost Recovery System Depreciation (MACRS):

• Unique to the United States Tax Code.

• Based on original asset cost, asset type, asset recovery period.

5. Units of Production Depreciation:

• Utilized when depreciation is more accurately based on usage instead of time.

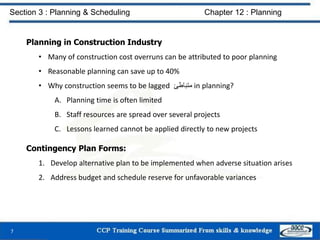

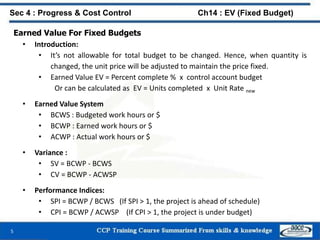

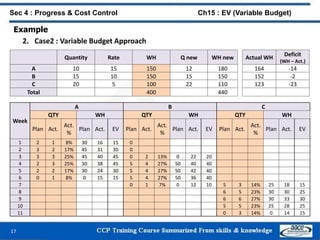

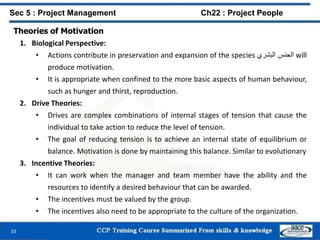

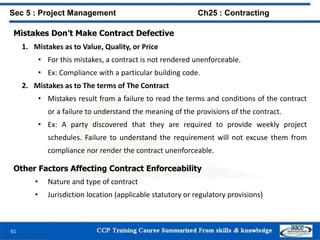

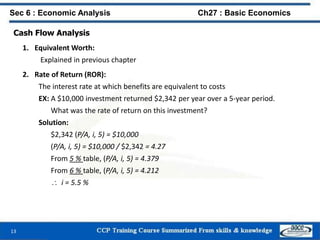

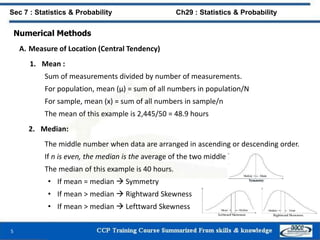

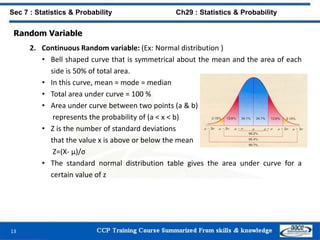

Year Calculation Dep. Amount

1 (8000 – 2000) x (5/15) $2’000

2 (8000 – 2000) x (4/15) $1’600

3 (8000 – 2000) x (3/15) $1200

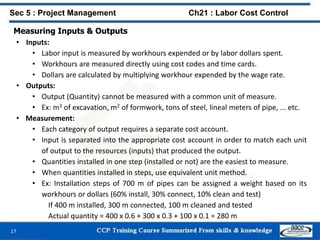

4 (8000 – 2000) x (2/15) $800

5 (8000 – 2000) x (1/15) $400](https://image.slidesharecdn.com/ccpmaterial-160302105905/85/CCP-Material-50-320.jpg)

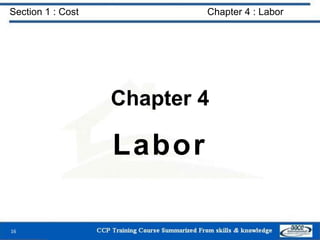

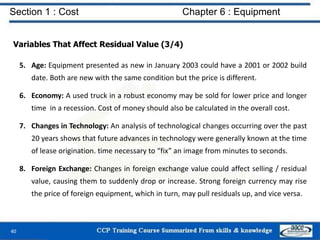

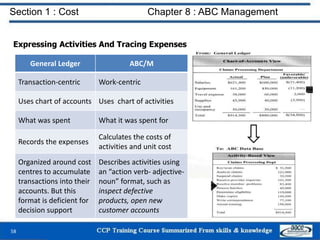

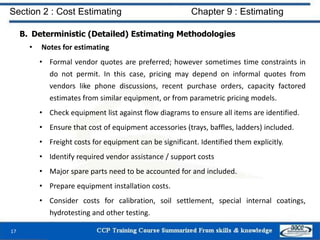

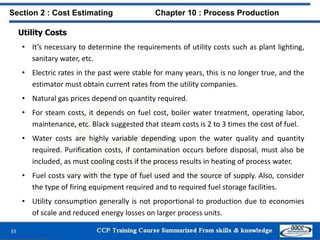

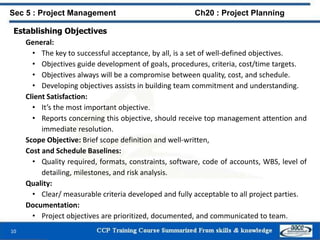

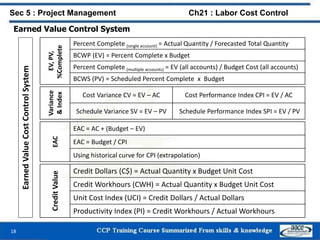

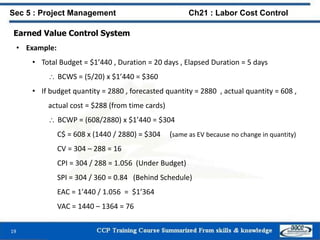

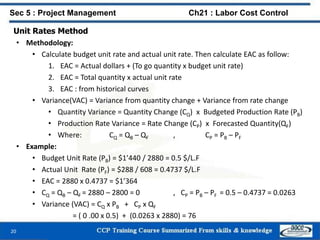

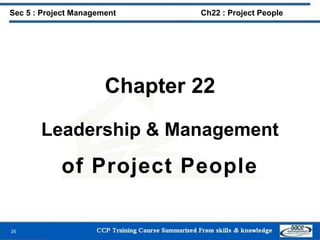

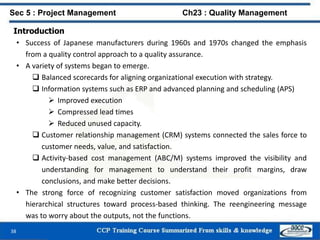

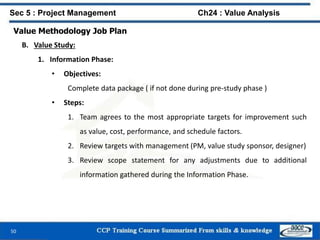

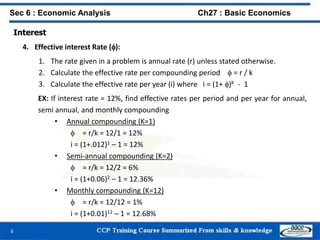

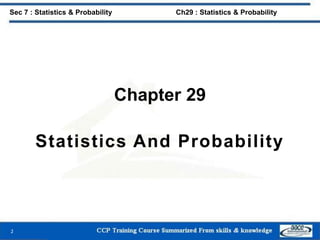

![Section 1 : Cost Chapter 7 : Economic Costs

51

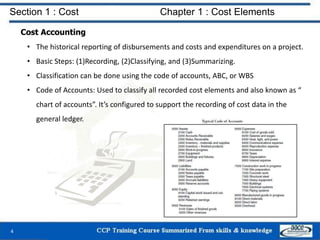

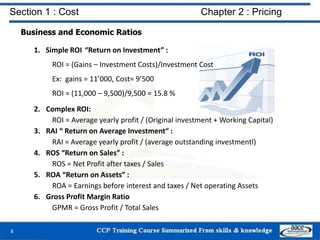

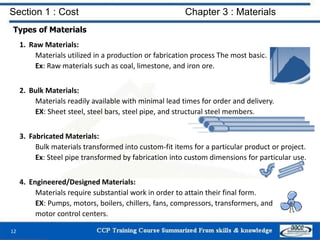

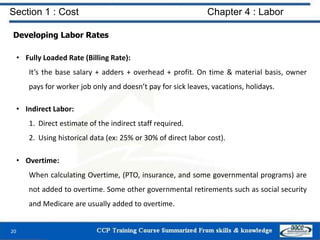

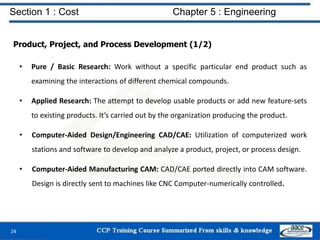

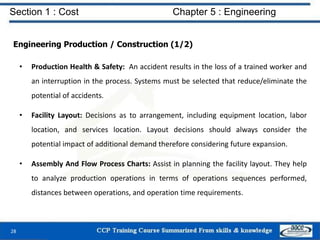

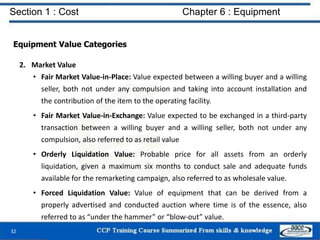

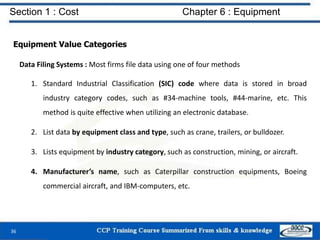

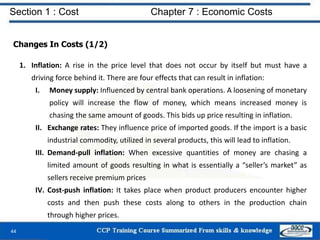

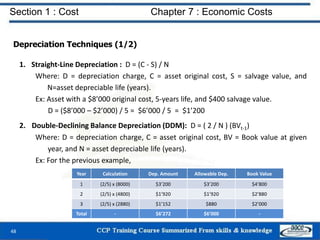

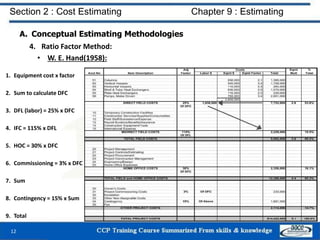

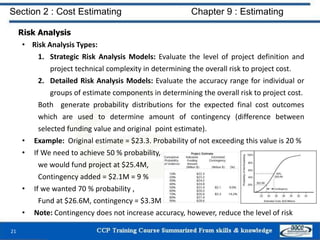

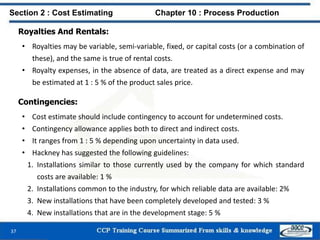

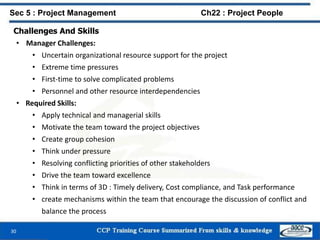

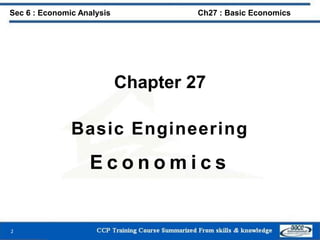

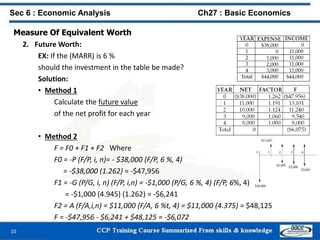

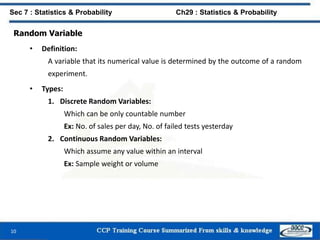

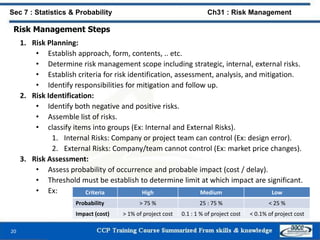

Economic Analysis Techniques

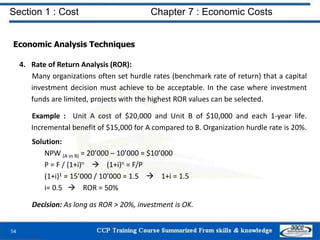

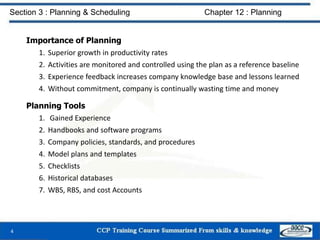

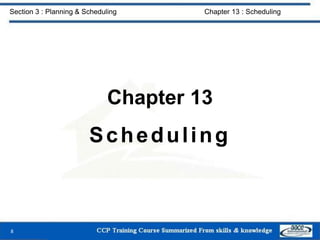

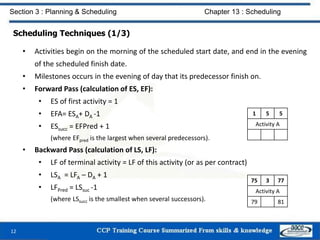

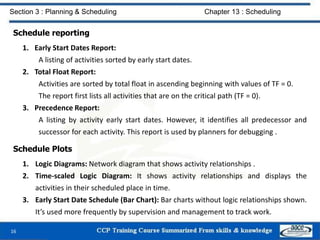

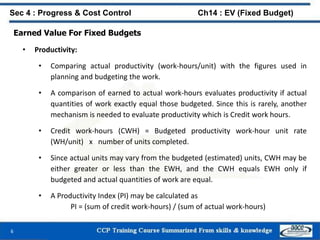

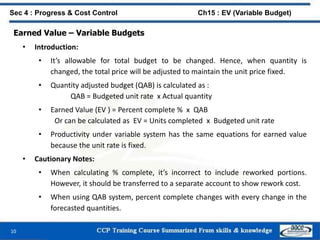

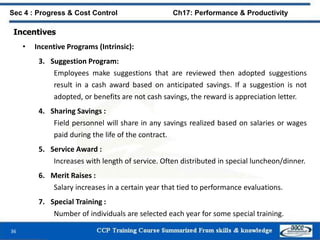

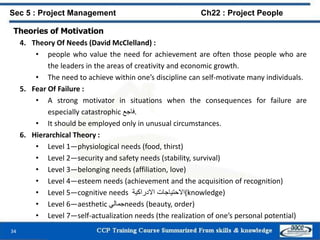

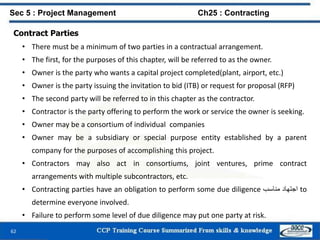

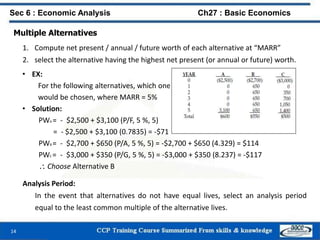

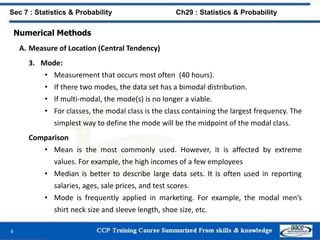

1. Net Present Worth Method (NPW):

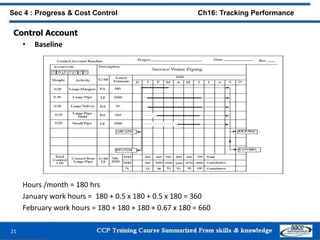

Ex: Unit A price=$10’000, life=4years, salvage=0, Annual maintenance = $500/year.

Unit B price=$20’000, life=12year, salvage=$5’000, maintenance costs are Year1=0,

Year2=$100 and increase by $100/year. The firm’s cost of capital is 8 percent.

Solution:

• Life is different and the common multiple is 12 years

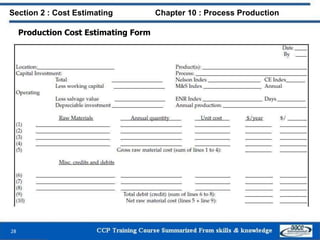

• NPW(A)= 10’000 + 10’000/1.084 + 10’000/1.088 + 500 x [(1.0812-1)/(0.08x1.0812)]

= 10’000 + 7350.3 + 5402.7 + 3768 = 26’521

• NPW(B)=20’000+ 100 x [ (1.0812 -0.08x12-1)/(0.0812 x 1.0812)] – 5000/1.0812

= 20’000 + 3463 - 1985.6 = 21’277.82

Decision: Select unit B that has the least cost.](https://image.slidesharecdn.com/ccpmaterial-160302105905/85/CCP-Material-52-320.jpg)

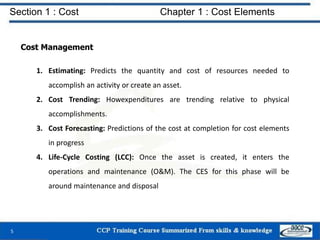

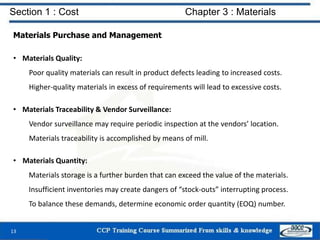

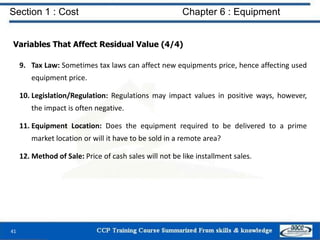

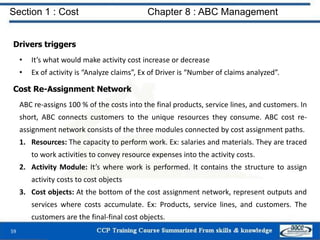

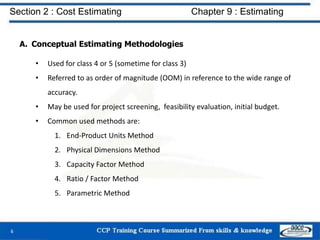

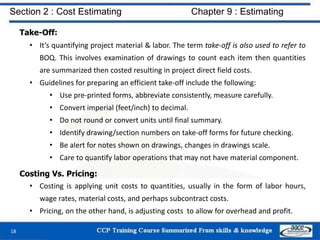

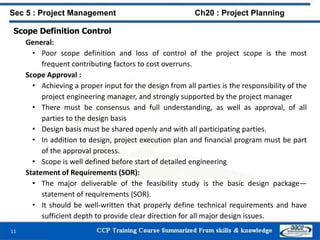

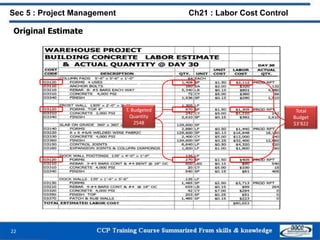

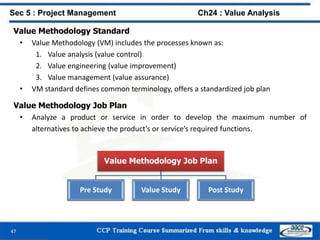

![A. Conceptual Estimating Methodologies

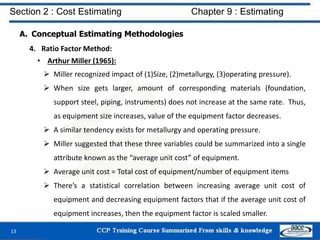

4. Parametric Method

• A correlation between physical or functional characteristics of a plant (or

process system) and its resultant cost [NASA].

• Capacity factor & equipment factor are simple examples of parametric

estimates; however sophisticated parametric models involve several variables .

• Developing a parametric model involves the following steps :

1. Cost model scope determination: End use, physical characteristics.

2. Data collection: Quality of model can be no better than quality of data.

3. Data normalization: Escalation, location, site conditions.

4. Data analysis: Series of linear and non-linear regression analysis will be

run to determine the best algorithm (model).

5. Data application: User interface that accept user inputs then calculate

costs and display results. Spread sheets is an excellent tool.

6. Testing: Test the result validity and accuracy.

7. Documentation: User manual.

14

Section 2 : Cost Estimating Chapter 9 : Estimating](https://image.slidesharecdn.com/ccpmaterial-160302105905/85/CCP-Material-77-320.jpg)

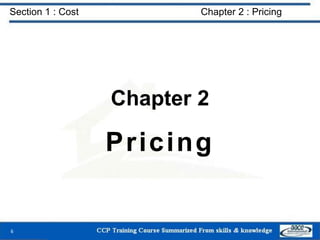

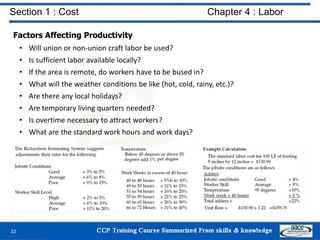

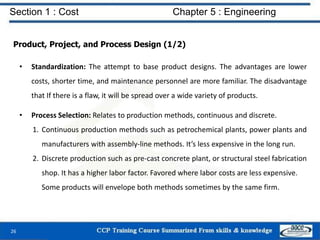

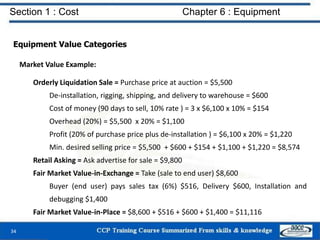

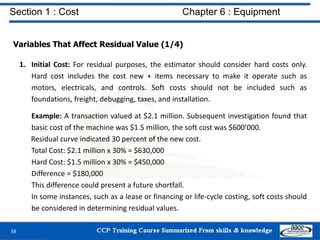

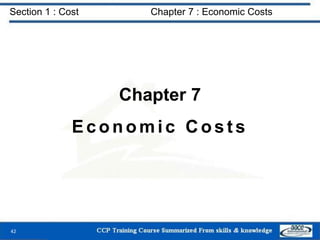

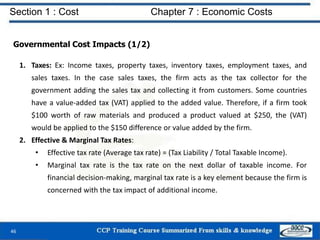

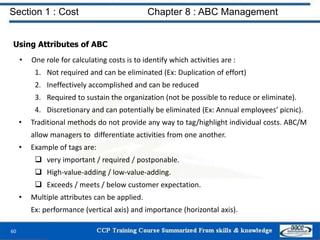

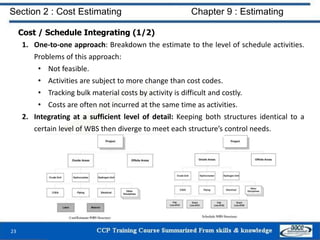

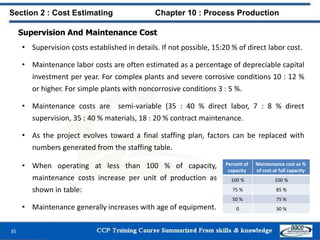

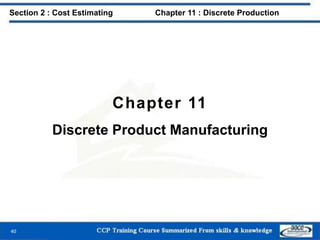

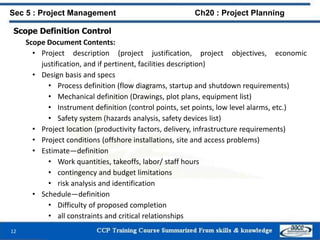

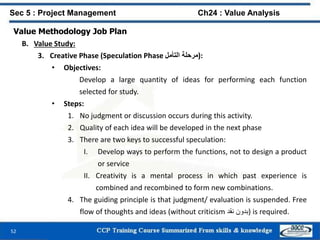

![Depreciation

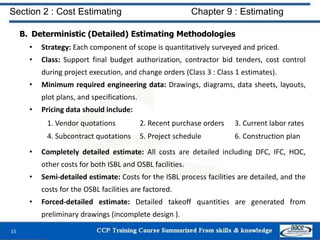

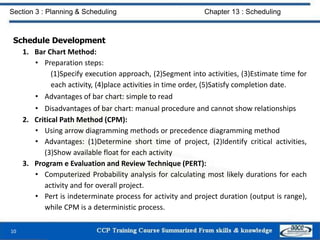

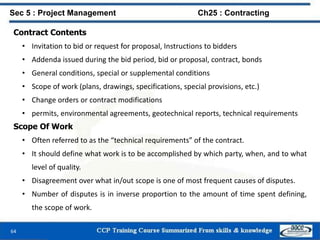

• Not a true operating cost, but considered to be an operating cost for tax purposes.

• Depreciable portion = Initial investment – (working capital + salvage value). In

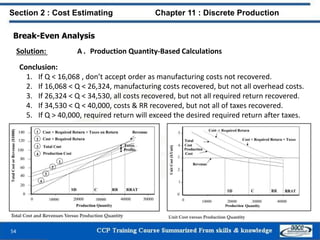

theory, working capital, salvage value can be recovered after plant shut down.

• Taxing authorities permit the use of any generally accepted method of depreciation

calculation provided that it is applied in a consistent manner to all investments

• In 1981 in the U.S., accelerated cost recovery system (ACRS) was mandated by law.

• In 1986, ACRS was replaced by modified accelerated cost recovery system (MACRS).

• Most industrial firms utilize accelerated depreciation. This deferring يؤجل taxes to

the latest possible date. However, for preliminary estimates, straight-line is used.

• Straight-line depreciation: D = C / Y , where D is annual depreciation, C is

depreciable portion, Y is asset life in years.

• Double-declining balance method: D = 2 (F-CD) / n , where F is initial asset value,

CD is cumulative depreciation charged in prior years, n is asset life in years.

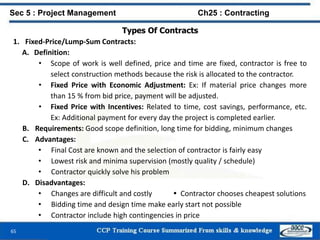

• Sum-Of-Years-Digits Depreciation: D = C x [ 2(n-Y+1) ] / [ n(n+1) ] , where C is

depreciable portion, n is asset life in years.

Section 2 : Cost Estimating Chapter 10 : Process Production

39](https://image.slidesharecdn.com/ccpmaterial-160302105905/85/CCP-Material-102-320.jpg)

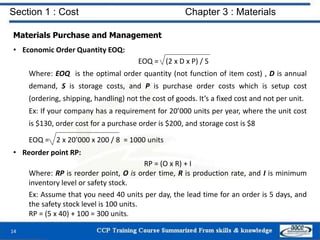

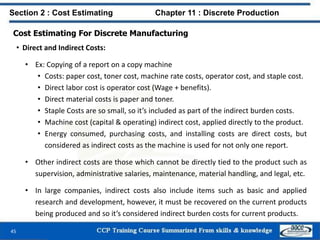

![Cost Estimating For Discrete Manufacturing

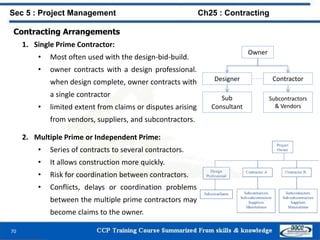

• Cost Estimating Example: (2/2)

47

Section 2 : Cost Estimating Chapter 11 : Discrete Production

Note that 20% of selling price = [20/(100-20)] % of Total Cost = 25% of Total Cost.](https://image.slidesharecdn.com/ccpmaterial-160302105905/85/CCP-Material-110-320.jpg)

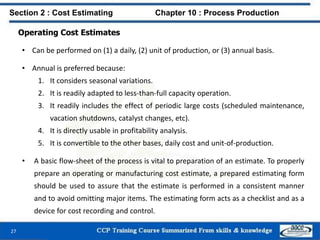

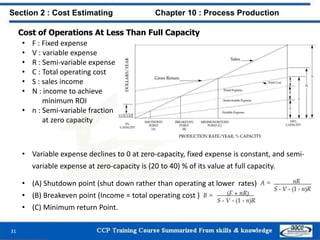

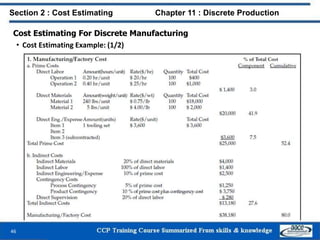

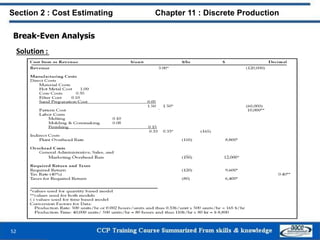

![Break-Even Analysis

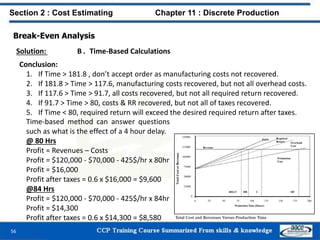

Solution: B . Time-Based Calculations

1. Shutdown Point

Revenues = Production Costs

120,000 = Material Costs + Labor Costs + Tooling Costs + Plant Overhead Costs

120,000 = 60,000+165Y+10,000+110Y 120,000 = 70,000 + 275Y Y = 181.8 hrs

2. Cost Point

Revenues = Total Costs

120,000 = Production Costs + Overhead Costs

120,000 = 70,000 + 275Y + 150Y 120,000 = 70,000 + 425Y Y = 117.6 hrs

3. Required Return Point

Revenues = Total Costs + Required Return

120,000 = 70,000 + 425Y + 120Y 120,000 = 70,000 + 545Y Y = 91.7 hrs

4. Required Return After Taxes

Revenues = Total Costs + Required Return + Taxes for Required Return

120,000 = 70,000 + 545Y + 120Y + [ 120Y x (TR/(1-TR)) ]

120,000 = 70,000 + 425Y + 120Y + 80Y Y = 80.0 hrs

55

Section 2 : Cost Estimating Chapter 11 : Discrete Production](https://image.slidesharecdn.com/ccpmaterial-160302105905/85/CCP-Material-118-320.jpg)

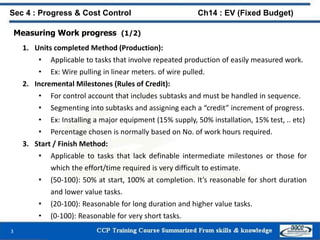

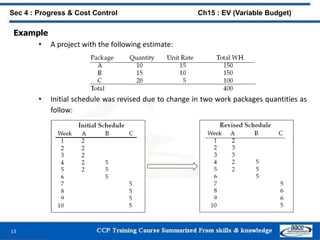

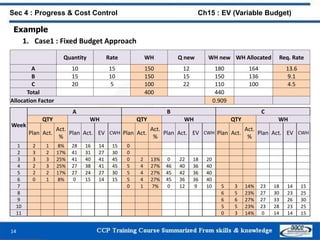

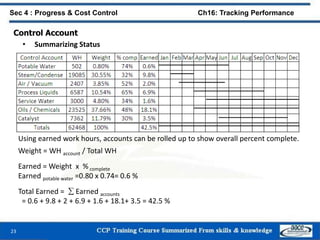

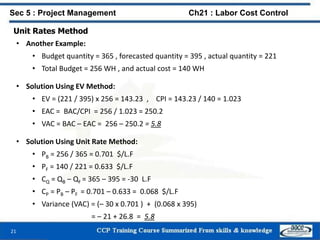

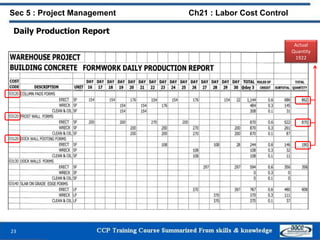

![22

Sec 4 : Progress & Cost Control Ch16: Tracking Performance

• Status will be done using the “units completed” method

• Use main item to be the control item (Large Pipes) then calculate actual quantity

• Actual Quantity (1/3 ) = (5/100) x 2000 x 0.25 = 25 % comp = 25 / 2000 = 1.25%

• Actual Quantity (1/10 ) = (15/100) x 2000 x 0.25 = 75 % comp = 100 / 2000= 5 %

• Actual Quantity (1/24 ) = [ (15/100) x 2000 x 0.25 ] + [ (50/2000) x 2000 x 0.30 ]

= 75 + 15 = 90 % complete = 265 / 2000 = 13.25

Control Account

• Statusing](https://image.slidesharecdn.com/ccpmaterial-160302105905/85/CCP-Material-159-320.jpg)

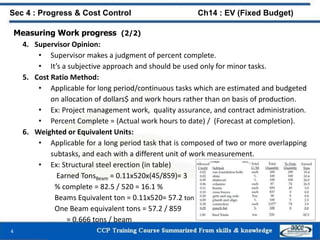

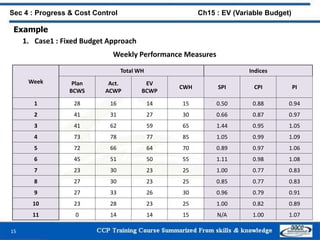

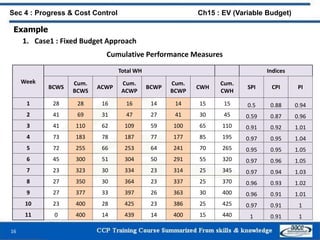

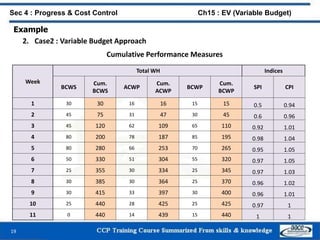

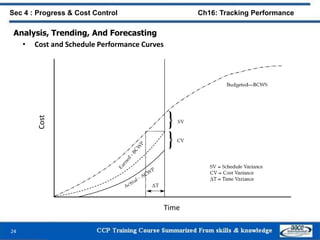

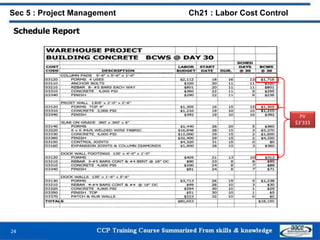

![26

Sec 4 : Progress & Cost Control Ch16: Tracking Performance

Analysis And Forecasting

• Forecasting

1. Using the same rate of planning

EAC = ACWP + ( BAC – BCWP )

Where EAC: Estimate at completion, BAC: Budget at completion

2. Adjusting the same rate to consider cost variance

EAC = ACWP + [ ( BAC – BCWP) / CPI ]

= ACWP + BAC/CPI - BCWP/CPI

= BCWP/CPI + BAC/CPI - BCWP/CPI

= BAC / CPI

3. Extrapolation using the curves](https://image.slidesharecdn.com/ccpmaterial-160302105905/85/CCP-Material-163-320.jpg)

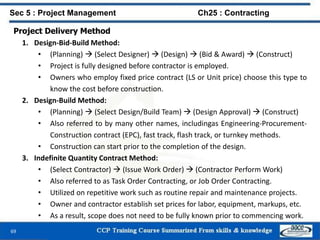

![68

Types Of Contracts

4. Target Contract:

A. Definition:

• Contractor perform early work (planning and design) on reimbursable basis.

• At some point, contractor will prepare and negotiate with the owner, a

detailed estimate with not-to-exceed cost and time of performance.

• It’s also referred to as guaranteed maximum price [GMP] contracts.

• At the end of work costs are compared to target and underruns, if any, are

shared. Overruns, unless caused by owner, are assessed to the contractor.

• Similarly, early completion bonuses are often paid to the contractor.

B. Requirements:

• Competent and trustworthy contractor.

• Quality / financial supervision by the owner.

C. Advantages:

• Early start can be made. Flexibility in dealing with changes.

• encourages economic and speedy completion

D. Disadvantages:

• Final cost initially unknown

• No opportunity to competitively bid the targets.

• Variations are difficult and costly once the target has been established

Sec 5 : Project Management Ch25 : Contracting](https://image.slidesharecdn.com/ccpmaterial-160302105905/85/CCP-Material-243-320.jpg)

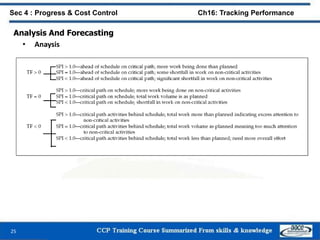

![17

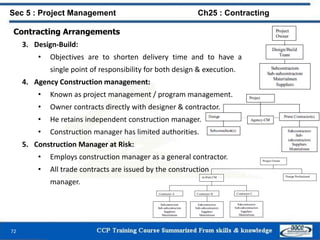

Sec 6 : Economic Analysis Ch27 : Basic Economics

Incremental Analysis

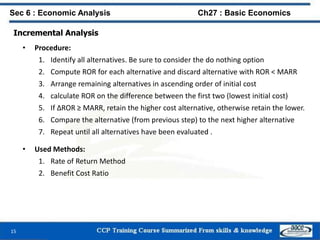

2. Benefit-Cost Ratio Method:

• Example:

Given the following alternatives

MARR = 5 % , which one should be chosen?

• Solution:

• Compute the Benefit-Cost Ratio for each alternative.

For alternative A: B/C = $3,191 (P/F, 5%, 5)/$2,500 = 1, acceptable

For alternative B: B/C = $650 (P/A, 5%, 5)/$2,738 = 1.03, acceptable

For alternative C: B/C = $350 (P/G, 5%, 5)/$3,000 = 0.96, rejected

• Arrange in ascending order of initial cost

• Calculate Benefit-Cost Ratio for (B-A)

B/C B-A = [$650 (P/A, 5%, 4)] / [$238 + $2,541 (P/F, 5%, 5)] = 1.03

B/C > 1

Accept the increment and retain the higher cost alternative, B.](https://image.slidesharecdn.com/ccpmaterial-160302105905/85/CCP-Material-281-320.jpg)

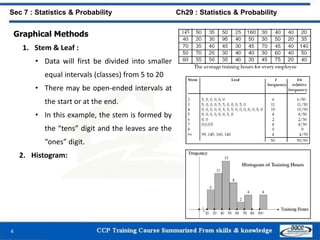

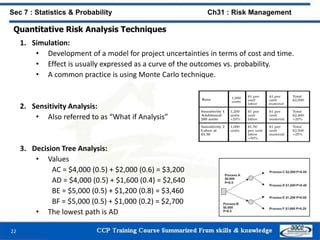

![Frequency Distributions

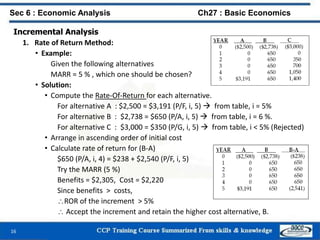

• Measure of Central Tendency:

1. Mean: Arithmetic average = 0.05375

2. Mode: Value occurs most often = 0.050

3. Median: Middle point when records are arranged in order

Mdn = L + [(N/2-cfb)/fw]i = .0475 + [(20/2 - 4)/7].005 = .05179

Where:

Mdn : Median

L : Lower limit (0.045 + 0.05) / 2 = 0.0475

N : Number of records

cfb : Cumulative frequency below

fw : Frequency of cases

i : Interval duration (0.05 – 0.045) = 0.005

17

Sec 7 : Statistics & Probability Ch30 : Basic Concepts](https://image.slidesharecdn.com/ccpmaterial-160302105905/85/CCP-Material-298-320.jpg)

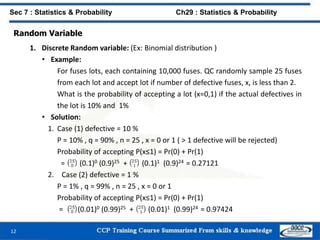

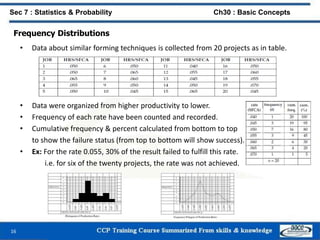

![Frequency Distributions

• Measure of variability:

1. Range: Difference between the lowest and highest records=0.065-0.04 = 0.25

2. Quartile Deviation: QD = (Q3 – Q1) / 2

Where:

Q1 = L + [(N/4 - cfb)/fw]i = 0.0475 + [(20/4 - 4)7] x 0.005 = .0482

Q3 = L + [(.75N - cfb)/fw]i = 0.0575 + [(0.75 x 20 - 14)2]x 0.005 = .060

QD = (Q3 – Q1) / 2 = (0.0482 + 0.060) / 2 = .0118

QD is more accurate than range but less accurate than standard deviation

3. Standard Deviation:

s = [ fX2 - ( fX)2/ N ] / (N - 1)

= [.226875 - (1.075)2/20](20-1) = 0.0088996

18

Sec 7 : Statistics & Probability Ch30 : Basic Concepts](https://image.slidesharecdn.com/ccpmaterial-160302105905/85/CCP-Material-299-320.jpg)

The document discusses key concepts related to engineering and production costs. It covers topics like product development processes, design considerations, and health and safety. Specifically, it describes the stages of research and development from basic research to prototypes. It also discusses factors that influence design decisions such as standardization, manufacturability, and the make-or-buy analysis. Finally, it emphasizes the importance of production health and safety to reduce accidents and interruptions.

![7_C's_OF_COMMUNIOCATION[1].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/7csofcommuniocation1-230801063320-9af405b3-thumbnail.jpg?width=640&height=640&fit=bounds)