Download as PDF, PPTX

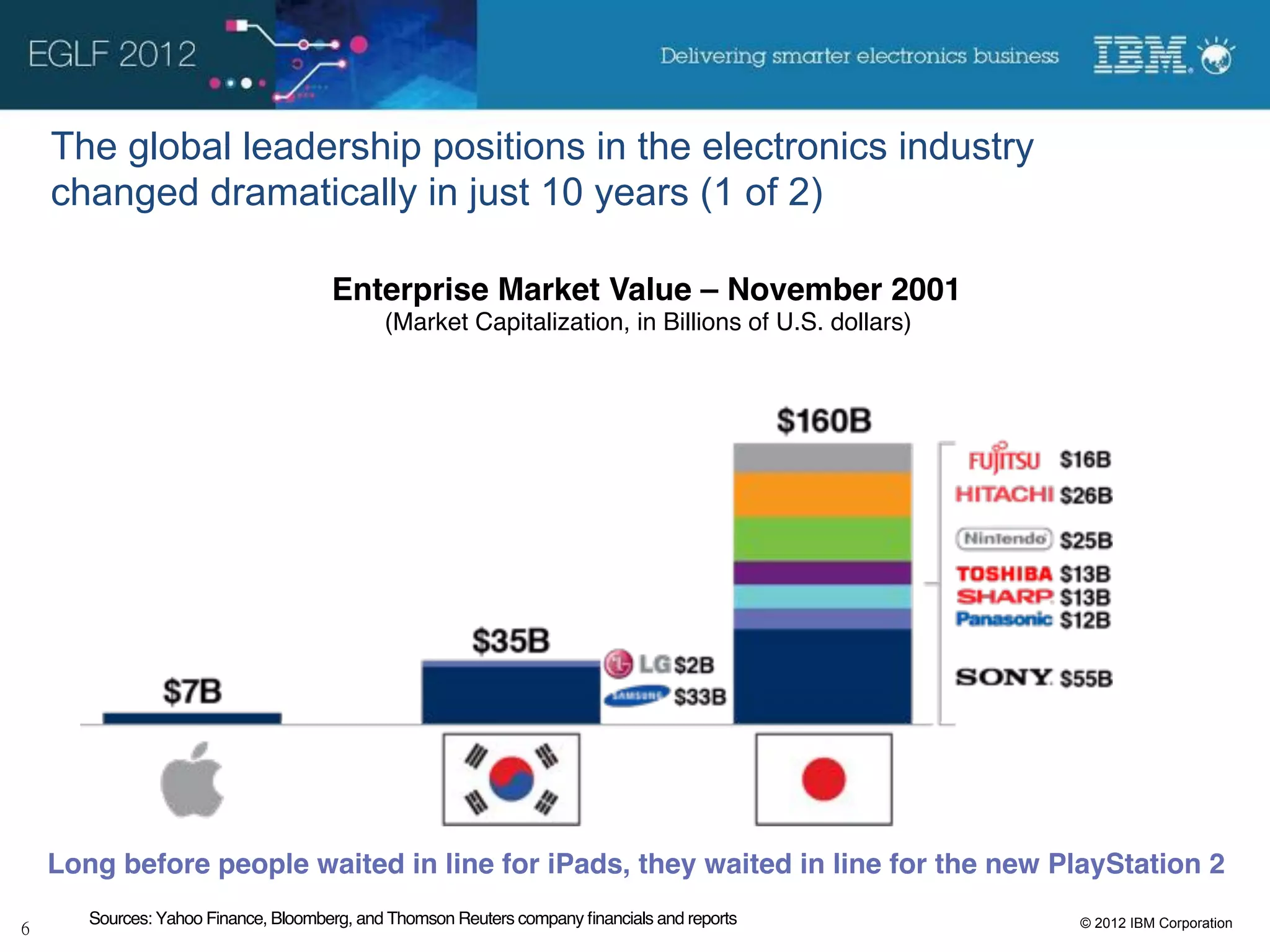

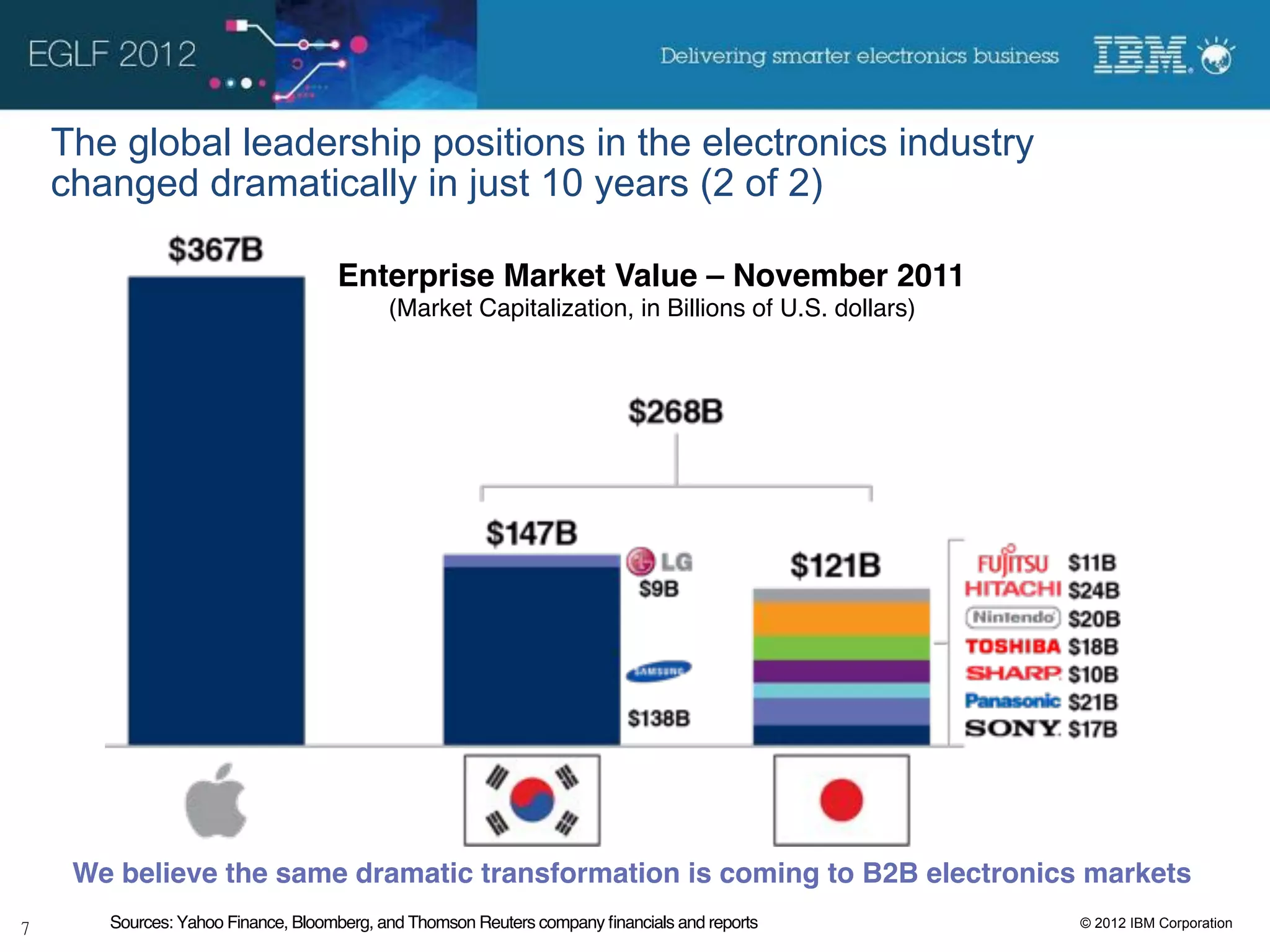

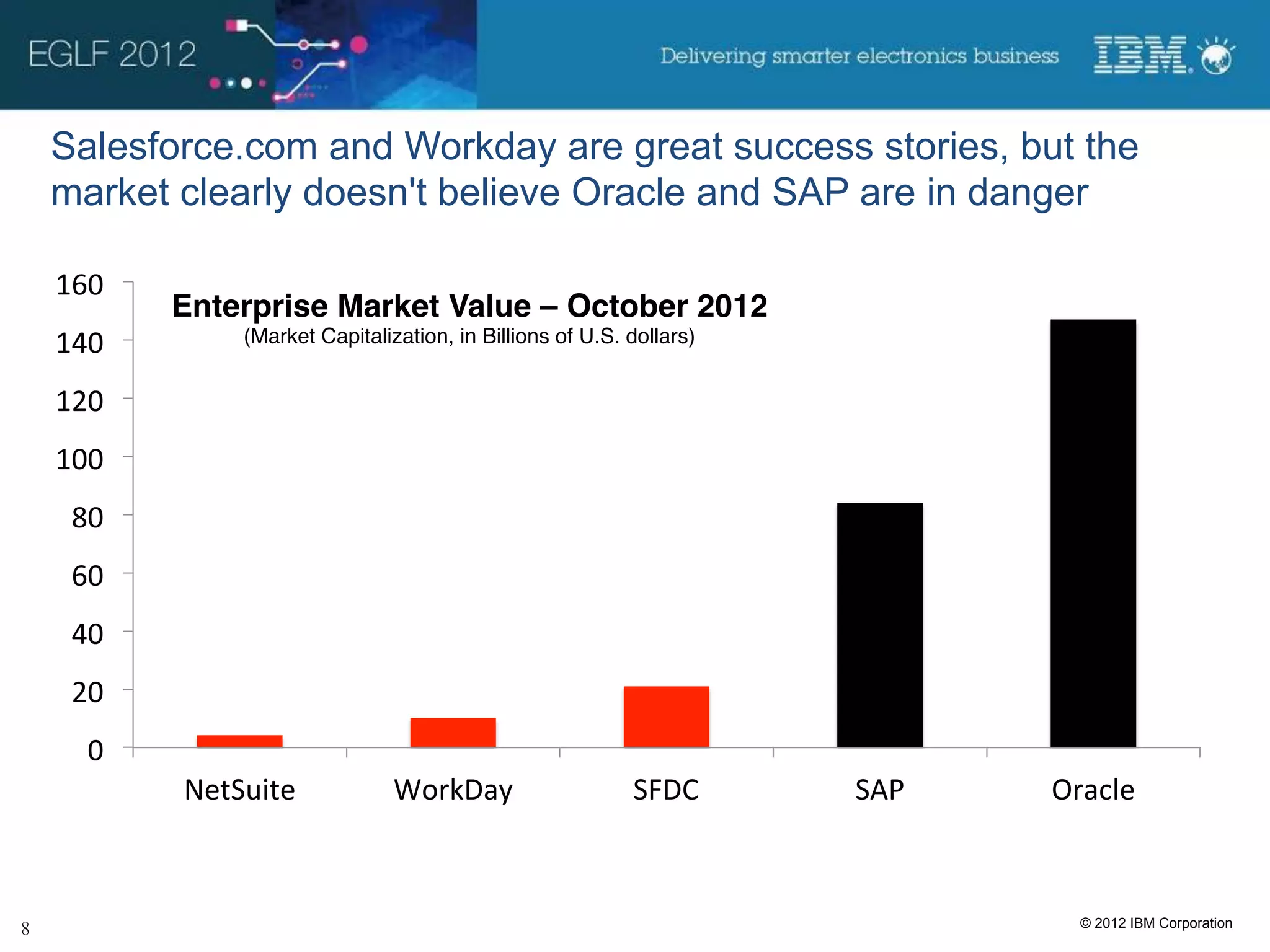

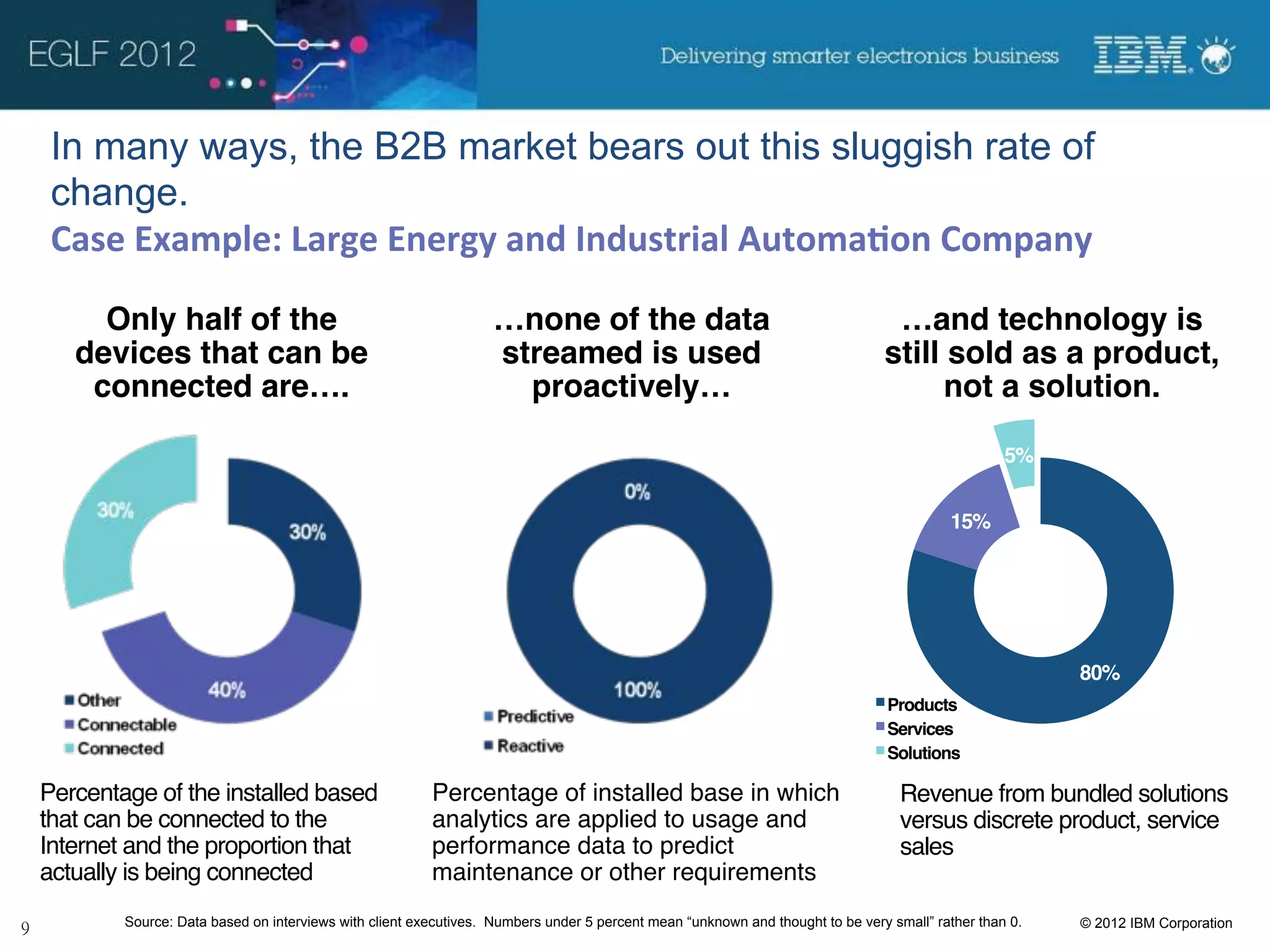

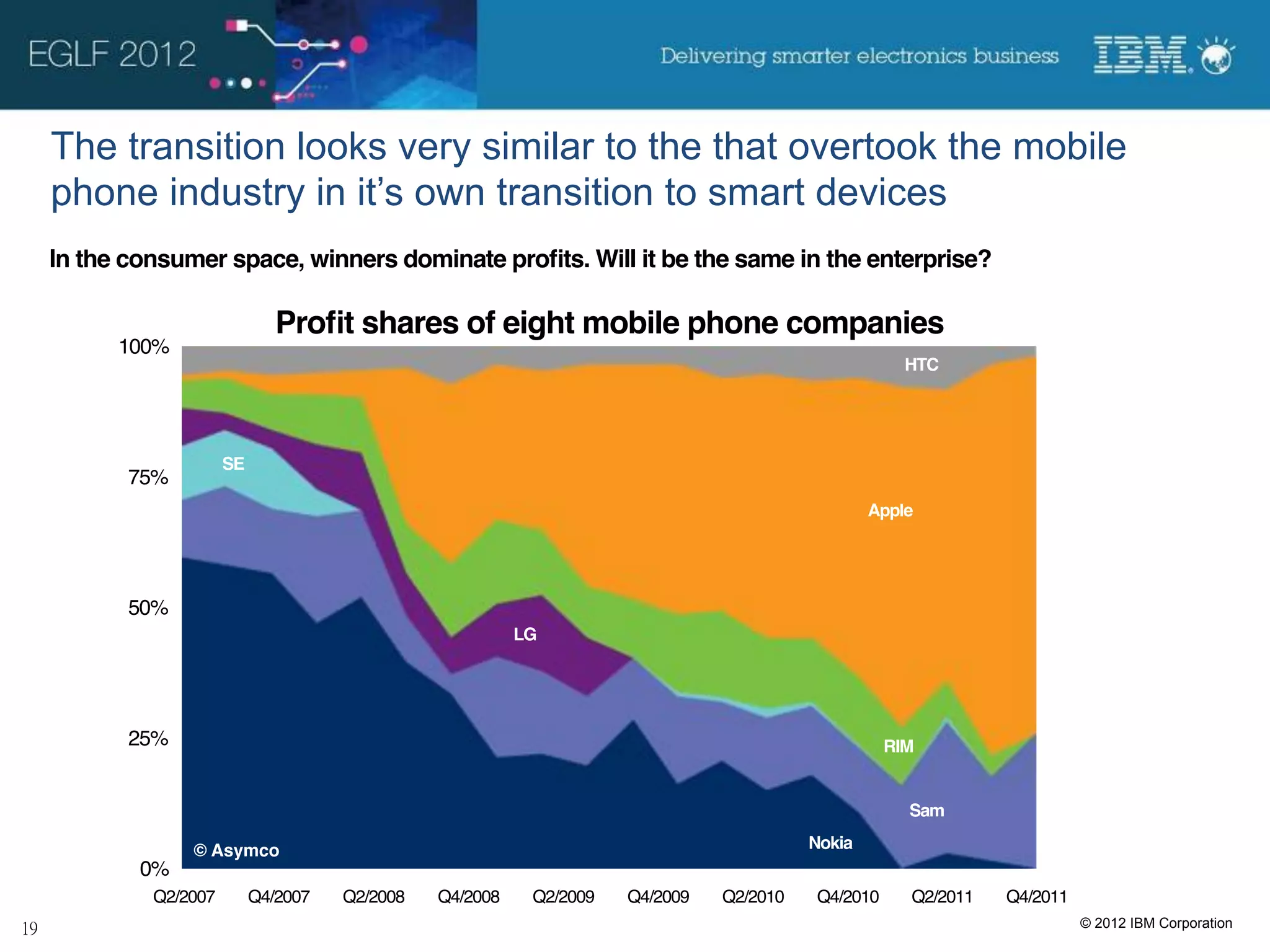

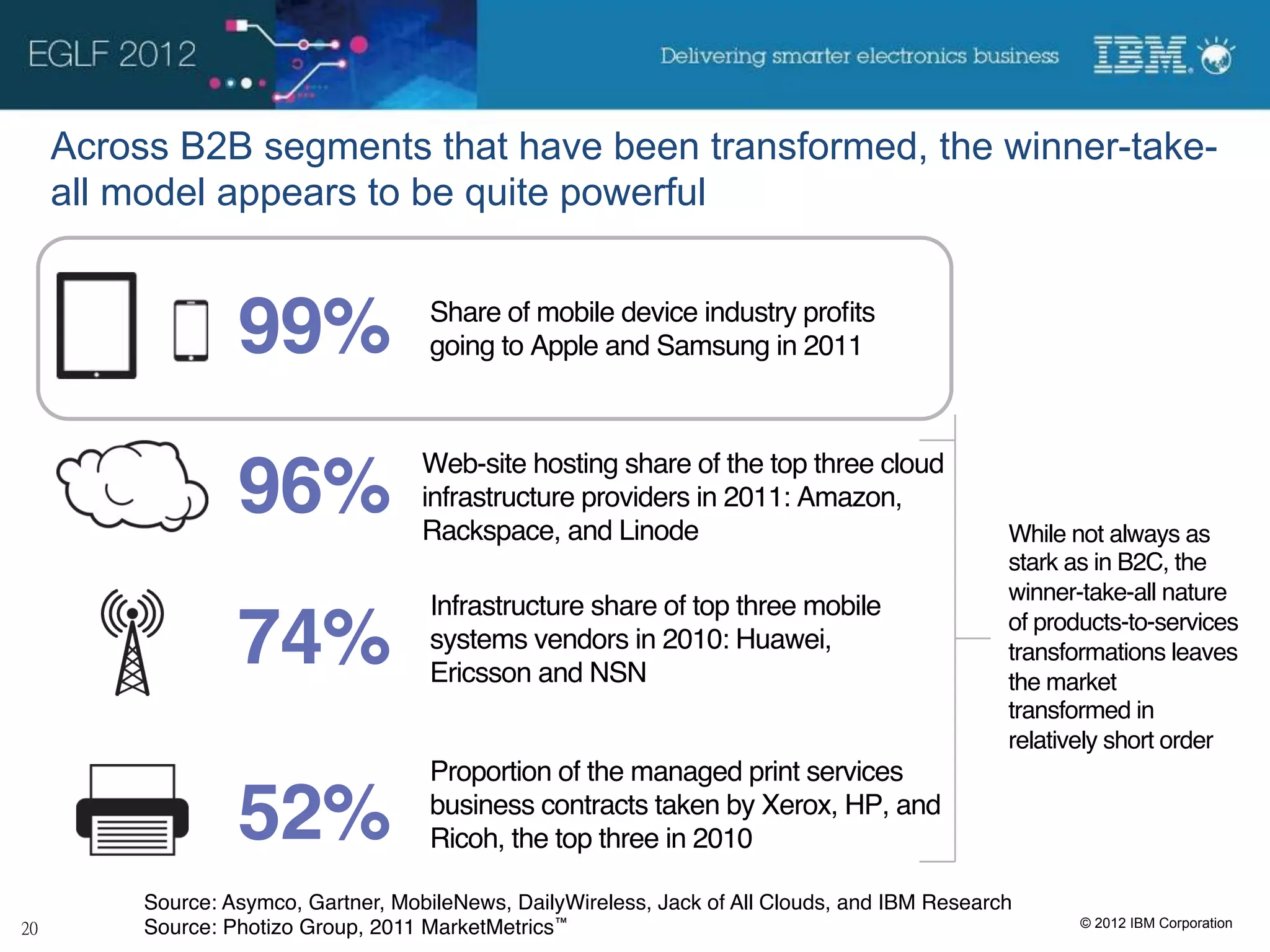

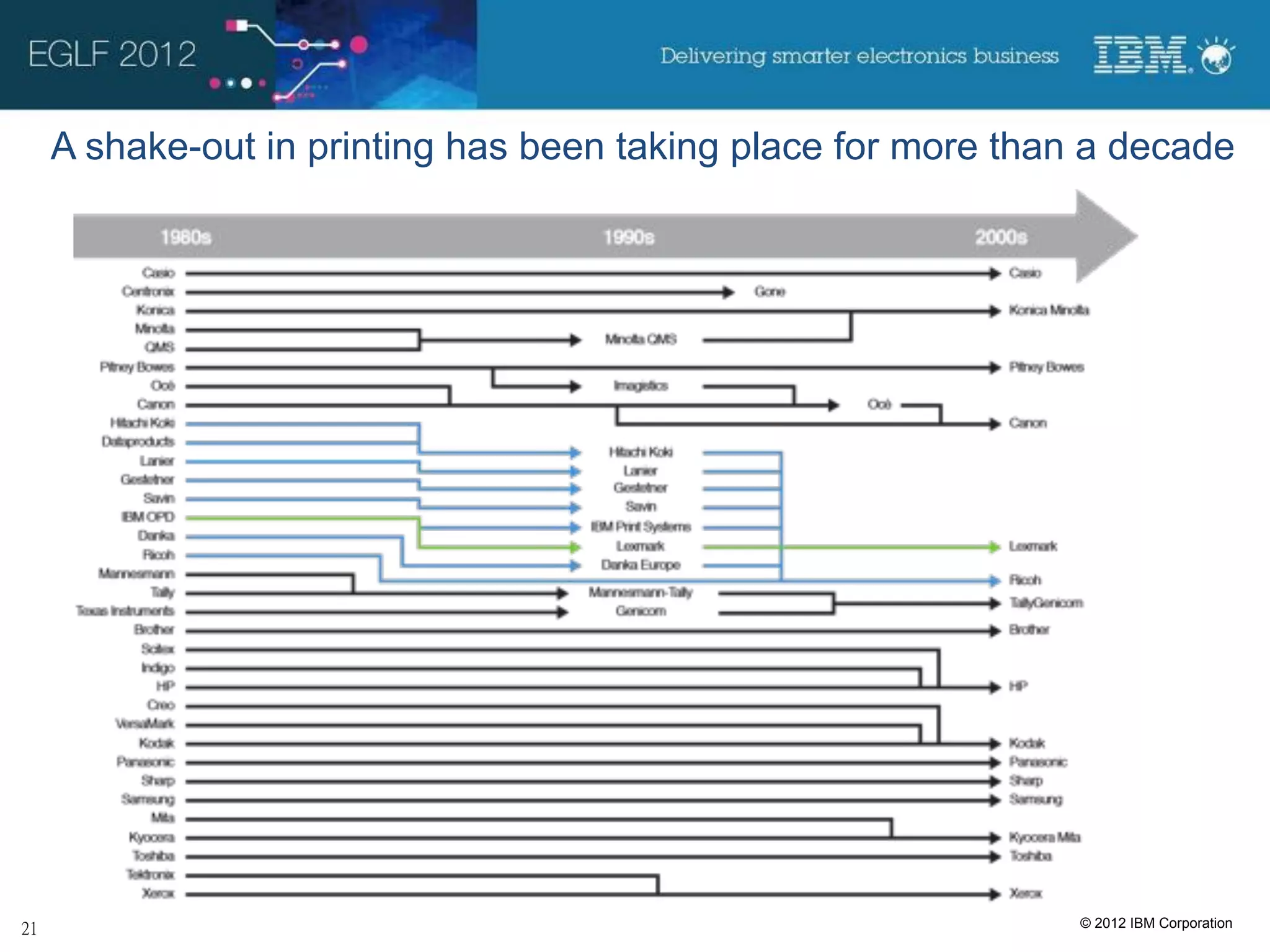

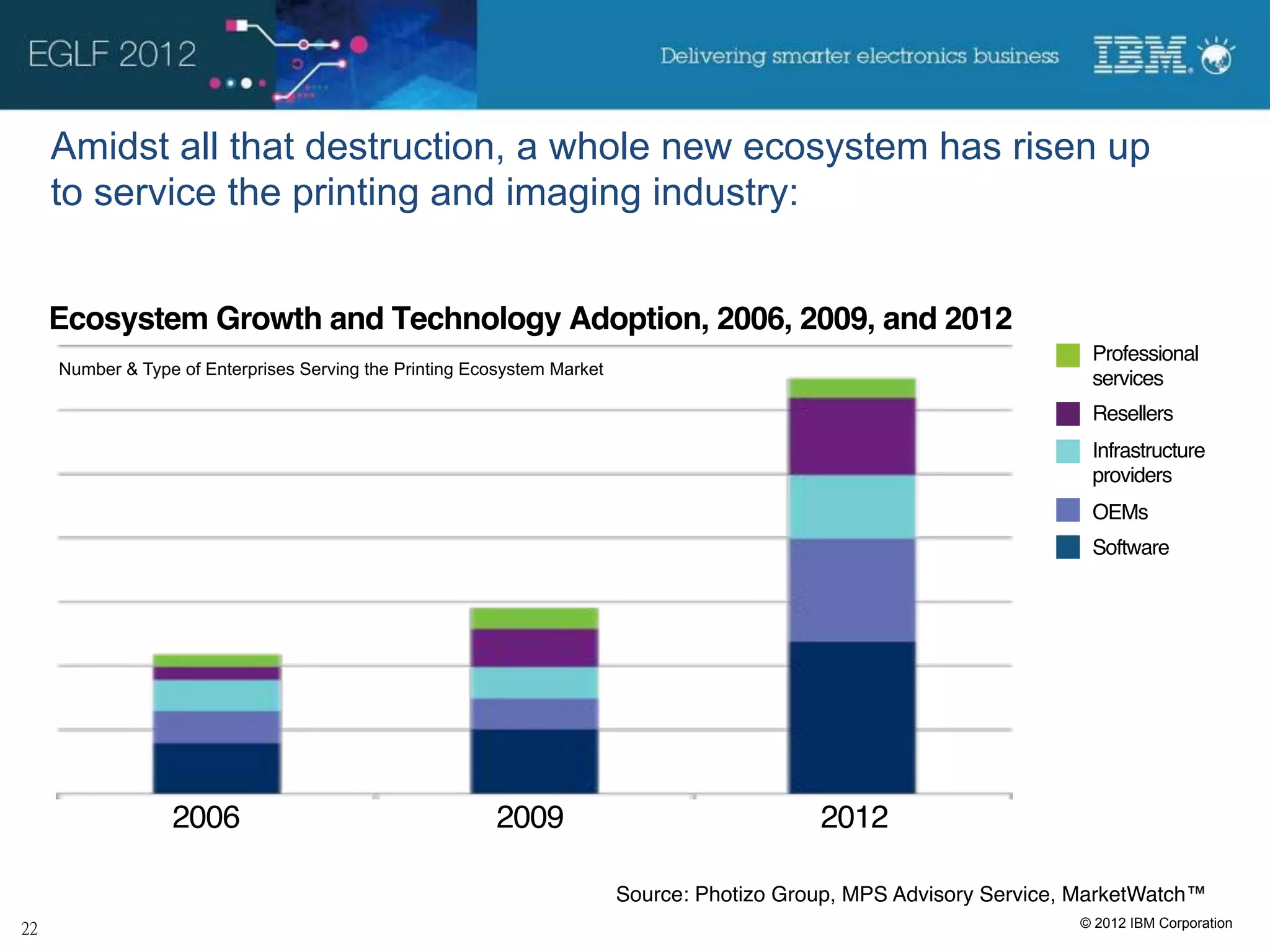

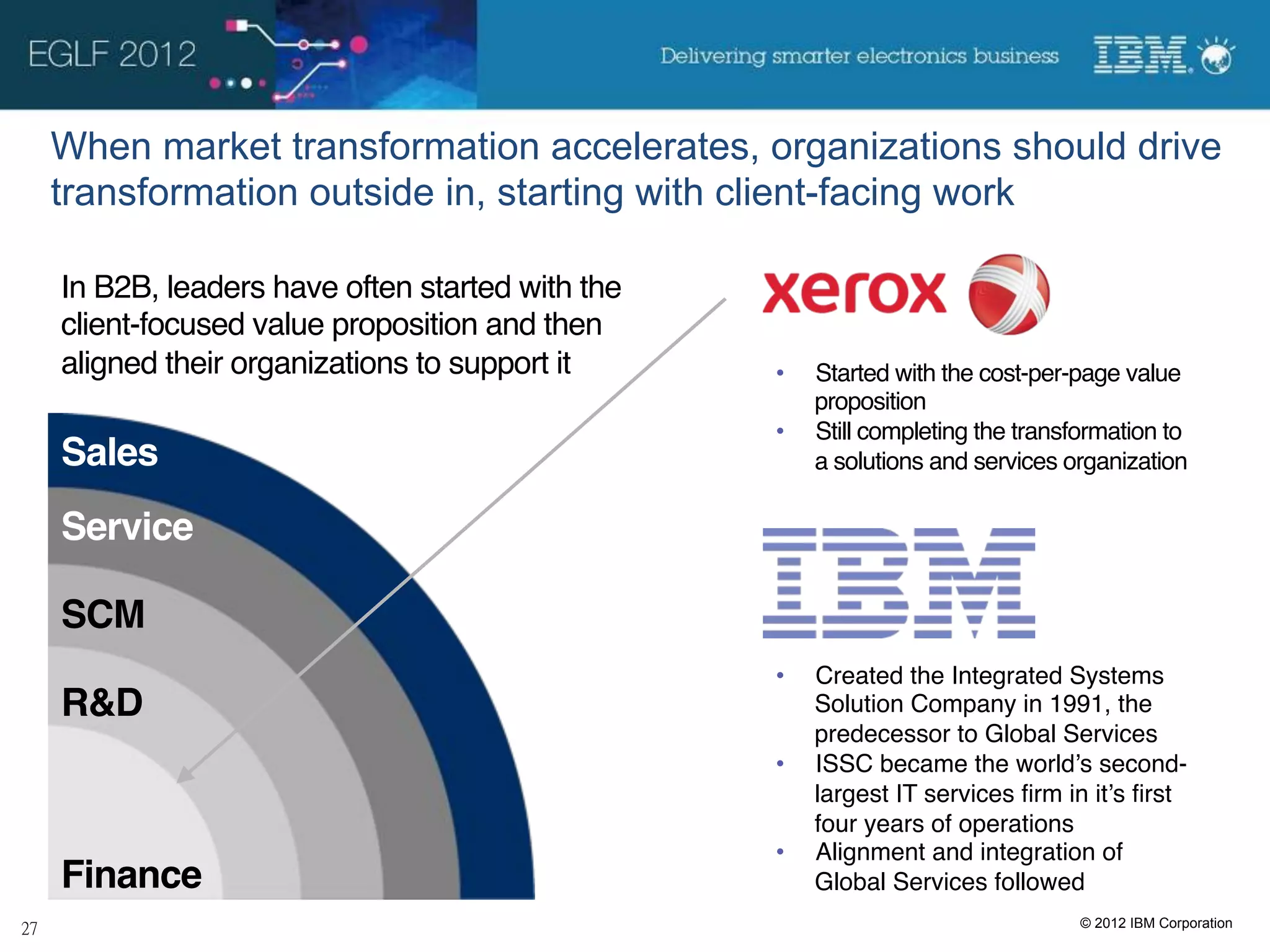

The document discusses the transformation in B2B electronics markets, highlighting that while consumers are quickly adopting new technologies, enterprises lag behind due to several barriers. Key insights include the shifting focus from products to services, the impact of analytics and online marketplaces on procurement, and the winner-take-all nature of transformed markets. As traditional impediments to change decline, organizations must adapt by aligning closely with customer needs to remain competitive in this rapidly evolving landscape.