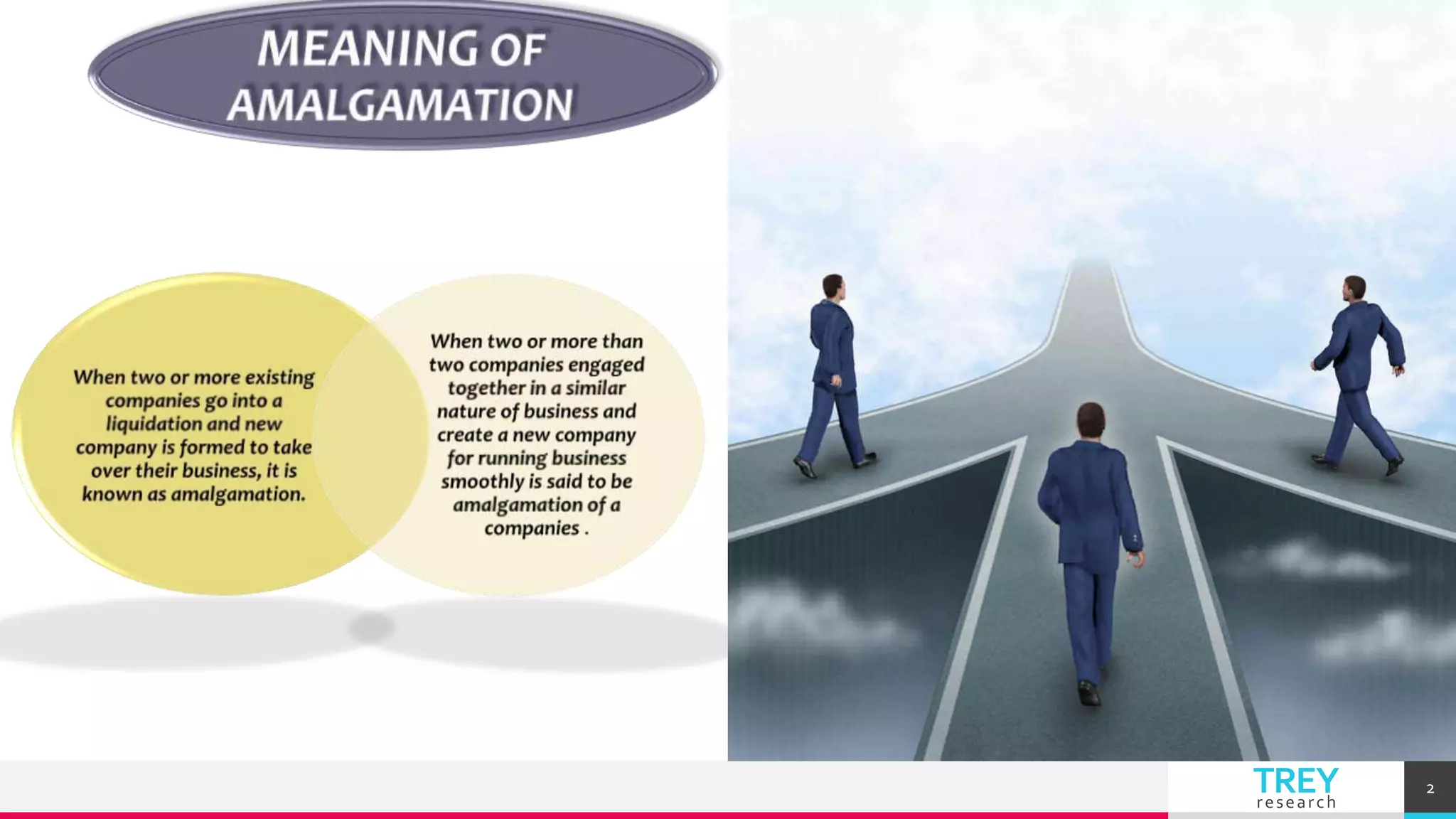

This document discusses different types of amalgamation of companies, including amalgamation in the nature of merger and amalgamation in the nature of purchase. It explains that in an amalgamation in the nature of merger, all assets and liabilities of the transferor company become assets of the transferee company, and shareholders of the transferor holding over 90% equity shares become shareholders of the transferee. It also covers the advantages and disadvantages of amalgamation, as well as the pooling of interest and purchase methods for accounting for amalgamation.