Downloaded 786 times

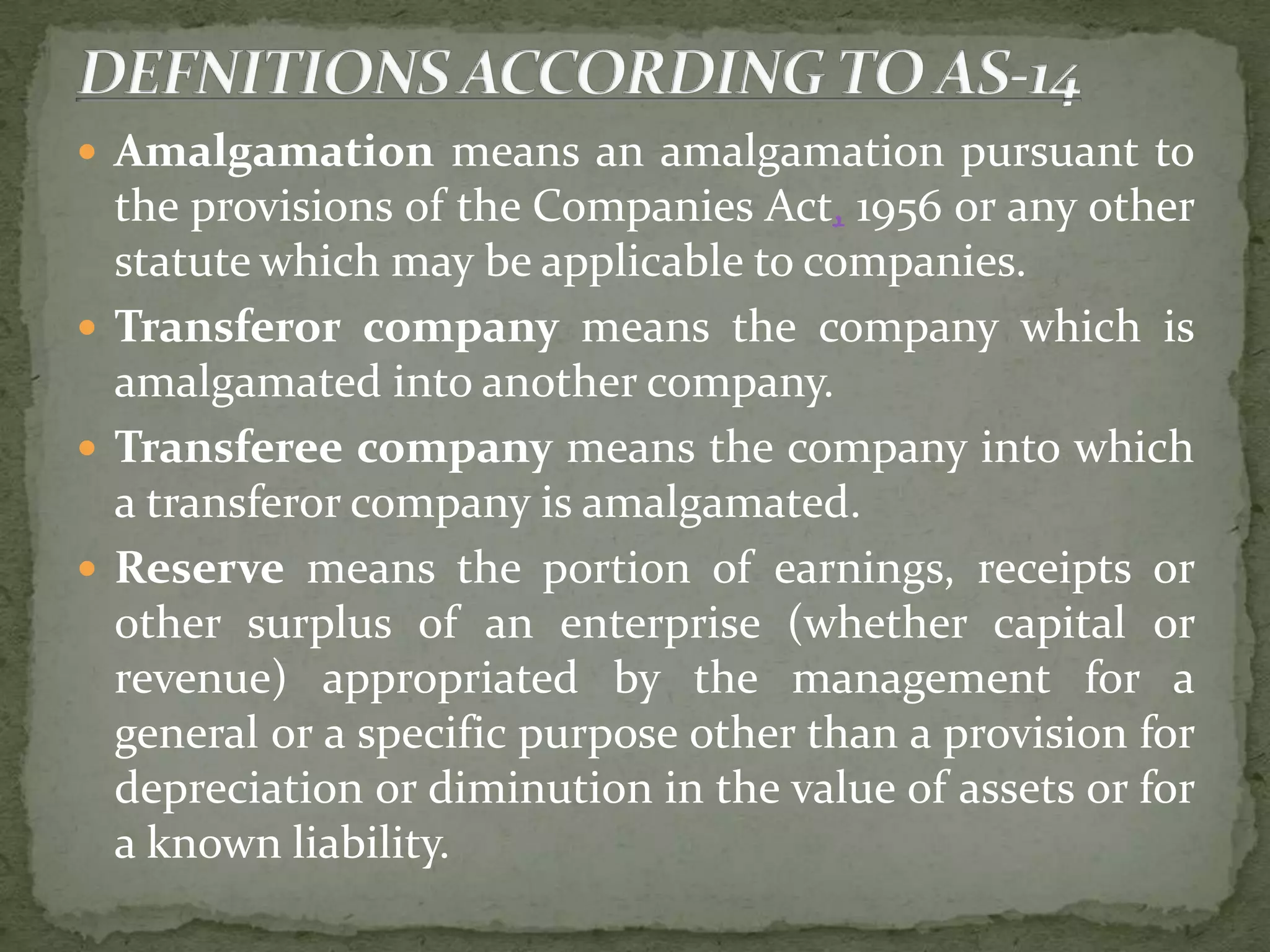

Amalgamation refers to the merger of two or more companies into one new company. It involves the transfer of two or more companies' businesses to a newly incorporated company. There are two types of amalgamation - amalgamation in the nature of merger and amalgamation in the nature of purchase. Amalgamation can be accounted for using either the pooling of interests method or the purchase method. Disclosures as per Accounting Standard 14 are required in the financial statements following an amalgamation.