Downloaded 47 times

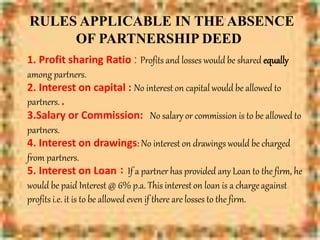

- The document discusses key aspects of partnership agreements and profit distribution among partners according to Indian partnership law. - It explains that a partnership is formed through an agreement to share business profits, and it's best to have this agreement in writing to avoid disputes. The written partnership agreement is called a partnership deed. - The partnership deed typically specifies details like the firm name, partners' names and capital contributions, the nature of business, profit sharing ratios, and rules around interest on capital, partner salaries, and interest charged on withdrawals.